Currency

“Everything we hear is an opinion, not a fact. Everything we see is a perspective, not the truth”

“Everything we hear is an opinion, not a fact. Everything we see is a perspective, not the truth”

– Marcus Aurelius

It seems pretty clear the Japanese stock market and the Japanese yen are moving in unison, i.e. higher Japanese stocks and higher USD/JPY (yen weakens as stocks rally). Below is an overlay of the Nikkei 225 Index and USD/JPY from early 2012 through today:

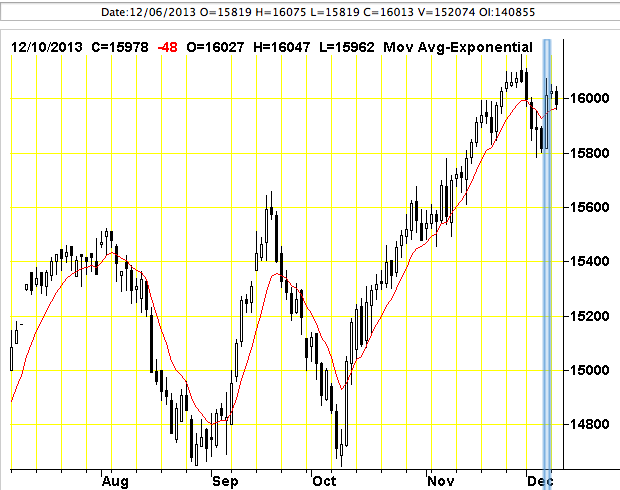

(Reuters) – The dollar gained across the board on Thursday, helped by an upbeat U.S. retail sales report that suggested recovery in the world’s largest economy is on stable footing.

That report, however, does not alter expectations for how soon the Federal Reserve will start reducing its economic stimulus, analysts said. Market participants still expect the Fed to pare back its asset purchases no later than March and this has been reinforced after Thursday’s weaker-than-expected U.S. jobless claims data.

U.S. retail sales rose 0.7 percent in November, while initial jobless claims rose 68,000 to 368,000 last week, the largest weekly increase November 2012.

“The strong U.S. retail sales number was definitely a positive factor for the dollar. This could lead to some upward revisions in the gross domestic product for the fourth quarter,” said Brian Dangerfield, currency strategist at RBS Securities in Stamford, Connecticut.

The rise in jobless claims was a result of seasonal factors given last week’s big drop due to the Thanksgiving holiday, he added.

“I think the market is looking at today’s outsized increase in jobless claims as not necessarily an indication of a weakening U.S. labor market,” he said.

In early New York trading, the dollar index .DXY rose 0.2 percent to 80.071, gaining after three days of losses.

The euro fell 0.2 percent against the dollar to $1.3762, ending a seven-day winning streak. It has gained nearly 4 percent since November 11 and is close to its 2013 peak of $1.3832.

The dollar advanced 0.5 percent versus the yen to 102.90, rising after two days of losses. The euro also gained, up 0.4 percent at 141.65 yen, not far from a five-year peak of 142.17 yen.

The Swedish crown, meanwhile, was a big mover of the day, falling to a 1-1/2 year low against the euro after data bolstered the case for a rate cut by Sweden’s Riksbank. The euro, however, remained supported by higher money market rates and year-end repatriation by banks.

The Swedish crown fell to its lowest since May 2012 at 9.0749 crowns per euro after inflation data showed falling price pressures with jobless numbers also painting a grim picture about the Swedish economy.

“The market is extrapolating the data will see some action from the Riksbank next week. This is driving down the crown,” said Jeremy Stretch, head of currency strategy at CIBC World Markets in London.

SWISS FRANC COOL TO SNB

The Swiss franc rose against the euro, helped by year-end flows into safe-haven Switzerland. It shrugged off comments from the Swiss National Bank, which reiterated its commitment to the euro/franc peg of 1.20 euros.

The euro fell to a seven-month low of 1.2197 francs, while the dollar climbed 0.2 percent to 0.8879 franc.

“Investors are concerned about the impact on risk appetite of Fed tapering and this could underpin the Swiss franc,” said Jane Foley, senior currency strategist at Rabobank.

“Also, given the recent increase in disinflationary pressures in the euro zone, it seems likely that ECB interest rates will also remain at rock bottom for longer. This indicates that there is less reason for euro/Swiss to appreciate soon,” she said.

(Additional reporting by Anirban Nag in London; Editing by Meredith Mazzilli)

Faber – The Asset Class Hated Even More Than Gold & Silver

Faber – The Asset Class Hated Even More Than Gold & Silver

As 2013 comes to a close, Marc Faber spoke with King World News about the asset class that is hated even more than gold and silver. Faber also gave his thoughts on where we are headed with regards to inflation/deflation. This is part III of a series of written interviews which have now been released on KWN.

Eric King: “What are you buying and selling right now?”

Faber: “Well, actually the most hated asset at this time, aside from gold and silver, hated even more so is cash. Nobody wants to hold cash because everybody knows that the purchasing power of cash is diminishing….

Continue reading the Marc Faber interview HERE

“When I read dozens of advisories, I sometimes dream that economics could be simple. How about this: the US Treasury issues bonds, the Federal Reserve buys these bonds with money it creates with the computer, money brought about from thin air. It’s money that nobody worked for an nobody took risks for. The newly created money amounts to over one trillion a year. It’s taking more and more newly created money to produce less and less in the Gross Domestic Product. That’s a trend that could easily end in hyperinflation.

Friday’s market provided a hint of a melt-up. (Ed Note: Friday he refers to is Dec 6th)

Subscribers with strong stomachs may be indulging in this melt-up. Others with weaker stomachs are probably on the sidelines. My original thinking is that this melt-up would be so powerful and so insistent that few would be able to sit on the sidelines and watch. In investing, the ticket to success is to take big profits and small losses.

Philosophically, what do you gain when you make a killing in the market? Probably a more luxurious life, and a feeling of well being. But nobody can take his profits with him. Which is why Warren Buffett and Bill Gates are giving their money away while they are alive.

I never ask subscribers to do what I wouldn’t do. And what am I doing? If I buy anything here, unless I hold it for a year, I’ll be subject to short-term capital gains tax. Since I can’t be sure that this advance will last for over a year, and thus give me tax break, I’m not going to enter this market.

Gold is another story. I continue to think that gold is building a base and that somewhere ahead gold is going to surge. For now I’ll sit with my bullion and cash and patiently await developments.

Is this the beginning of the melt-up I’ve been talking about? It’s too early to tell. But if there was a time to speculate, this may be the time. Personally, I haven’t got the nerve to join in on the festivities. Boils down to a matter of – to each his own. I like the gold action. And this is where I put the bulk of my money.

By the way Sotheby’s just sold a pink 59-karat diamond for $83.1 million, a world’s record for any jewel. It’s a mad, mad world. Who can forget the Graff Pink that sold for $46 million by Sotheby’s in Geneva. Big money is putting millions into one-of-a-kind tangibles. Like Chinese gold-buying, it’s all an escape from the dollar. And it may well lead to hyperinflation, assuming the Fed continues on its course. I continue to believe that gold is constructing a huge base.

Everybody knows that it’s dangerous to arrive late at the party, but it seems that’s where we are. Is the stock market really on thin ice? And is the gold market really on the edge of an upside explosion? Nobody knows. Meanwhile the Fed controls the sword of Damocles, which is hanging over the market.

I can’t prove it but I suspect an inflection point for gold is close at hand. The Chinese, who own a massive amount of US securities, have become openly worried about the US dollar. The gold that has been shaken out of weak and worried US hands, has been shipped to the East, and particularly China. China has imported a net 986 tons of gold through Hong Kong during the first 10 months of the year.

China may not be so much intent on backing its currencies with gold, but in protecting itself from a potential collapse in the US dollar. From the US standpoint, it’s now a case of “inflate or die,” and much of the world knows this. Thus if the US decides not to default on its massive debts, it will have to resort to hyperinflation. If this happens, the US will single-handedly tear the world monetary system apart.

What worries me is that governments will do whatever they have to in order to remain in power. This can result in confiscation of the assets of US citizens. In the end, we only borrow the wealth during our lifetimes. We don’t take it with us. But the government can take it from us. Should this happen, I’m afraid we’ll see blood in the streets. America’s massive debts will ultimately upset the world’s monetary system. There will be no escape, but there will be a diversion into spirituality. This is not the time to give up on your gold. I suspect gold’s inflection point is near.

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE. (Ed Note: Richard Russell is 89 years old and began writing a newsletter he still writes every day in the early 1950’s)

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

(Reuters) – The euro inched higher against the dollar on Wednesday, driven by dwindling excess cash in the euro zone banking system, but fell against the yen as investors locked in profits from this year’s rally.

The euro was up 0.1 percent against the dollar at $1.3767, not far from the six-week high of $1.3795 it hit on Tuesday. It was 0.2 percent down against the yen at 141.15 yen but up 23 percent this year.

The single currency has shrugged off some poor recent economic data – particularly inFrance, where industrial output is declining – to surprise many analysts and move higher since the summer.

A key driver has been tighter money markets, as banks repay borrowing from the European Central Bank. Liquidity usually tightens towards the end of the year anyway, when banks hold off from lending to each other.

And the ECB’s unwillingness to ease monetary policy soon, despite inflation low enough to prompted talk of deflation, has seen a rise in two-year swap rates.

This year, another factor driving euro strength is European banks repatriating funds to shore up their capital bases before an ECB Asset Quality Review (AQR).

“There still seems to be decent underlying euro support,” said Simon Smith, head of research at FxPro. “We’re still seeing money market rates moving higher.”

He said the euro could hold “around the upper 1.30s level” early next year. It might weaken fall after the AQR, but Smith expects it to fall less against the dollar than other currenciesdecline when the U.S. Federal Reserve begins slowing its huge bond-buying program.

One-year risk reversals – which compare demand for options on a currency’s rising or falling – show a bias for euro puts, or bets that it will weaken. That suggests many speculators think the rally will not last.

The euro also took heart from news that euro zone countries were edging towards a deal on how to handle ailing banks. Divisions remain over key parts of the reform, which is needed to underpin confidence in the bloc’s lenders.

The Swiss franc hit a seven-month high against the euro of 1.22055 francs per euro in early trading, before falling back to 1.22150 francs per euro, as banks repatriated francs.

The yen rose for a second day as global stock markets fell and investors locked in profits. The dollar was 0.3 percent lower against the yen at 102.55 yen.

Global shares were lower on Wednesday, as investors booked profits on a range of once-crowded positions. The Nikkei .N225 and the yen tend to move in opposite directions, with a rally in the index a signal for speculators to sell the yen. A weaker currency then boosts Japanese exports, which helps shares.

Both the euro and the dollar have rallied strongly against the yen this year thanks to the Bank of Japan’s ultra-loose monetary policy and expectations that it will provide even more stimulus next year.

“It’s a bit of profit-taking from high levels,” said Peter Kinsella, a currency strategist at Commerzbank.

Analysts at Morgan Stanley said they remain bullish on dollar/yen over the longer-term but added: “We … note that the current uptrend is showing some signs of exhaustion, suggesting that it would not take too big a shock to trigger a correction of the strong gains seen over the past year.”

The dollar showed little reaction to news that budget negotiators in the U.S. Congress have reached a two-year deal aimed at avoiding a government shutdown.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair