Bonds & Interest Rates

The Federal Reserve’s increased transparency, such as indicating last week that it may taper quantitative easing (The Fed’s massive easing itself can hurt markets, El-Erian tells CNBC.

“The longer they stay unconventional, the deeper they venture with these experimental policies, the more the costs and the risks start to become large relative to the benefits,” he notes.

But, “there’s a second really interesting issue, which is, are they giving us too much guidance?”

The openness can accelerate market declines, El-Erian says. (Ed Note:

Just look at the amount of information the Fed has given investors, he states, adding that the Fed has thrown out lots of numbers for when it will start tapering QE, such as a 7 percent unemployment rate, a 6.5 percent unemployment rate, a date this year and a date next year.

“When you give so much guidance to the market, you risk over-determining,” El-Erian explains. “So what happens, people jump to the terminal values. They don’t even wait for the journey. They go immediately to the destination and the re-price. Then the bad technicals kick in.”

Even St. Louis Fed President James Bullard questioned whether Bernanke went too far in specifying the central bank’s intentions.

Bullard said in a statement that he “felt that the committee’s decision to authorize the chairman to lay out a more elaborate plan for reducing the pace of asset purchases was inappropriately timed.”

Ed Note: It would seem investors are favoring the strategy indicated by both of these charts

“We know it has to happen. And when it does, we’ll get out.”

“We know it has to happen. And when it does, we’ll get out.”

One of the speakers at a conference we attended in London last week, a professional money manager, talking about the most important bit of investment information you are likely to get in your lifetime.

He was probably speaking for thousands of his colleagues. All confident that they would be able to spot the turn in the bond market when it happens… and all leave the party in good order.

We’re still in the wee hours of a bear market in bonds that will probably last until the middle of the century. In fact, we’re so early that when the sun finally rises we may find we are not yet in a bear market after all. The action over the last two months – and especially the last two weeks – may be just another of Mr. Market’s famous fake-outs.

(We think Mr. Market is doing a great fake-out job in gold, by the way. More on that tomorrow…)

But in the bond market, it looks like the real thing. The Dow rose 100 points yesterday. Gold fell by a couple of bucks an ounce. And Treasury bonds continued their slide. And, since it has to happen sometime, we will suppose that the bond market has put in its top now. If we are too early… we’ll enjoy a leisurely cup of coffee while other investors are scrambling for the doorway.

Meanwhile, the New York Times reports that the exits are getting jammed:

Wall Street never thought it would be this bad. A bond sell-off has been anticipated for years, given the long run of popularity that corporate and government bonds have enjoyed. But most strategists expected that investors would slowly transfer out of bonds, allowing interest rates to slowly drift up.

Instead, since the Federal Reserve chairman, Ben S. Bernanke, recently suggested that the strength of the economic recovery might allow the Fed to slow down its bond-buying program, waves of selling have convulsed the markets.

The value of outstanding United States government 10-year notes has fallen 10% since a high in early May.

The selling has been most visible among retail investors, who have sold a record $48 billion worth of shares in bond mutual funds so far in June, according to the data company TrimTabs. But hedge funds and other big institutional investors have also been closing out positions or stepping back from the bond market.

“The feeling you are getting out there is that people are selling first and asking questions later,” said Hans Humes, chief executive of the hedge fund Greylock Capital Management.

That, by the way, is our advice. Get out now. You can ask all the questions you want later.

Everyone saw (or still sees) a turn in the bond market coming. Bonds have been going up for 33 years. They can’t go up forever. What can’t last forever has to stop sometime. This seems like as good a time as any.

But everyone cannot get out of their bond investments at the same time in a calm, orderly way. After three decades of bringing investors into the room, no trade is more crowded. When bond prices begin to go down… as they did the first week of May… the longer you wait to get out, the more you will lose.

So what do investors do? They head for the exits. All at once. And the bond market becomes an “owl market.” Everyone wants to sell. But “to who… to who?”

Owls are not trained in English grammar. They don’t know that the preposition “to” is followed by “whom,” not “who.” But they are good investors. And they know a developing disaster when they see one. Clever bond investors chose to stay at the party – even when they saw a little smoke rising in the corner. Now they have to decide what to do.

Some will hesitate… wait too long… and then, every bounce will encourage them to wait longer, hoping to recover their losses. Others will stumble and be crushed underfoot, selling their bonds at panic prices.

Is the panic happening already?

No. We’ve only smelled the first faint whiffs of fear. The 10-year T-note still yields only 2.58%. The really nasty odor will come later… when smoke fills the room… someone hits the fire alarm… and those clever investors find the exits blocked.

Regards,

![]()

Bill

About Bill Bonner

Bill Bonner founded Agora Inc. in 1978. It has grown into one of the largest independent newsletter publishing companies in the world. In 1999, along with Addison Wiggin, Bill founded The Daily Reckoning. Today, this daily e-letter reaches over 500,000 readers around the globe.

Bill has also co-written two New York Times bestselling books, Financial Reckoning Day and Empire of Debt. He has written or co-written other widely read books as well, and has penned a daily column at The Daily Reckoning for over 12 years. Recently, Bill decided to “retire” from his role at The Daily Reckoning and begin writing his Diary of a Rogue Economist.

Bill Bonner’s Diary of a Rogue Economist is your gateway to Bill’s decades of accrued knowledge about history, politics, society, finance and economics. Sometimes funny, sometimes frightening – but always entertaining and packed with useful insight, Diary of a Rogue Economist can help you make sense of the complex world we live in today.

Stock Market Rebounds From 6% Plunge After Central Bank Pledges More Liquidity; Wet Nurse Action

In the past few week, China intraday lending rates as measured by SHIBOR got as high as 25% (See China Cash Crunch: 1-Day Interest Rate Spikes to Record High 25%).

With rates spiking, global stock markets plunged.

On Monday China insisted banks had significant liquidity sending a message that banks need to manage their own risks.

A translated message by the People’s Bank of China on liquidity states “Commercial banks should concentrate storage for taxes and statutory reserve deposit and other factors impact on liquidity in advance to arrange sufficient positions to maintain adequate levels of reserve ratio, to ensure the normal settlement” while warning“expansion of credit and other assets too fast may lead to liquidity risk“.

That message sent the Shanghai stock market index down about 6% as shown in the following chart.

…….read more HERE

Ed Note: In line with Morgan’s Optimistic thinking & much to the surprise I am sure of pessimists, a Majority of U.S. Economic Data Beats Expectations this morning. Of the large number of economic releases that came out, 11 of the 12 beat estimates and some where well above expectations. Also, durable goods, new home sales, consumer confidence, and manufacturing all trended higher this month, with consumer confidence and new home sales near 5-year highs. You can read

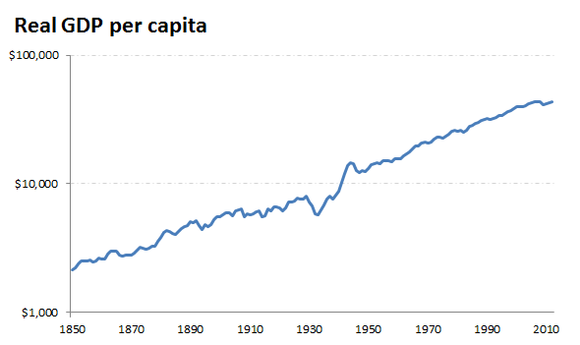

Why I’m an Optimist

The 2002 book Bringing Down the House told the true story of how six MIT math geniuses mastered blackjack card counting and took Las Vegas for millions. It had money, sex, drugs, and power. People loved it.

But part of the story often went misunderstood. The card-counters didn’t win every hand of blackjack, or anything close to it. The casino normally has a slight edge over players. The MIT crew’s strategy tipped those odds just barely in their favor. That meant they still lost a lotof bets. “Even the most complex systems seemed to aim at an overall edge of around 2 percent,” author Ben Mezrich wrote.

But that tiny edge was all the crew needed to succeed, provided they played long enough. When the odds are even slightly in your favor, you will win over time, even if you lose often in between.

That’s why I’m an optimist on the economy and the market. Maybe even a permanent optimist.

Take a look at this chart, showing GDP per capita adjusted for inflation since 1850:

……continue reading HERE

As usual the Federal Reserve media reaction machine has fallen for a poorly executed head fake. It has fallen for this move many times in the past, and for its efforts, it has tackled nothing but air. Yet right on cue, it took the bait once more. Somehow the takeaway from Wednesday’s release of the June Fed statement and Chairman Ben Bernanke’s press conference was that the central bank is likely to begin scaling back, or “tapering,” its $85 billion per month quantitative easing program sometime later this year, and that the program may be completely wound down by the middle of next year.

The global economy has changed radically in recent years but most Americans seem to continue to invest as if it hasn’t.

Euro Pacific Capital offers a means for American investors to gain exposure to those areas of the global economy that have largely avoided the crushing debt burden that has swamped many developed economies.

Based on the irresponsible policies of the Federal Reserve and the continued failure of the United States to put our fiscal house in order, we believe that the U.S. dollar is at risk of falling relative to currencies of more economically vibrant nations. Changes in currency valuation, often ignored by many investment consultants, could make significant impact on long term results.

Our firm’s mission, as is widely articulated by our founder and CEO Peter Schiff, is to offer globally diversified investment options to discerning retail investors and forward thinking institutions. Operating from seven offices nationwide, Euro Pacific brokers develop individual relationships with customers to determine their unique investment needs.

Are you a Retail Investor?

Individuals, families, trusts, and corporations can open a variety of investment and retirement accounts with Euro Pacific, including IRAs, and Roth IRAs. Those with $50,000 or more to invest can choose Euro Pacific’s signature managed account portfolios that rely on active management to achieve specific investment goals. While these accounts offer varied asset class allocations, all seek exposure to those nations, currencies and sectors that are favored by Euro Pacific’s global economic outlook.

Find out more about how we work with clients:

Traditional Brokerage Accounts

Are you an Institutional Investor?

Euro Pacific equity analysts provide in-depth research in commodity, energy, transportation, basic materials, manufacturing, and consumer stocks in developed and emerging markets worldwide. We compliment this research with an institutional trading desk that operates in local markets around the globe. Euro Pacific Asset Management offers international portfolio management services to all types of institutional investment funds, including pension funds, endowments, and foundations.

Find out More:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair