Bonds & Interest Rates

-

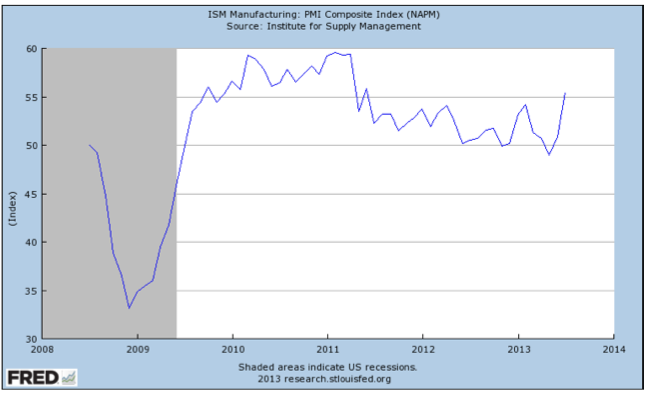

The ISM Manufacturing Index also exceeded estimates, delivering a reading of 55.4 – it’s highest reading since June 2011- indicating growth in the US manufacturing base

-

The overall numbers are good, but not great; today’s release of the non-farm payrolls data should help confirm whether or not the US recovery is set to continue and perhaps accelerate

-

If the economy does “find its legs”, higher interest rates are a given. What to do?

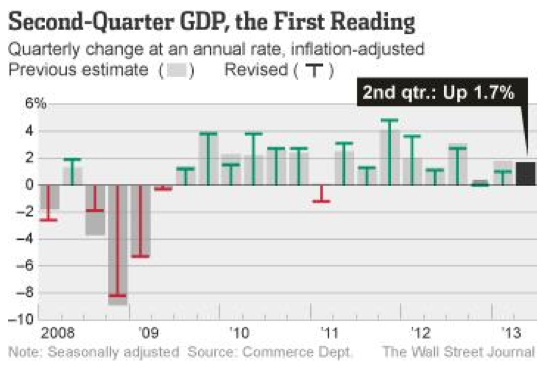

In light of the uncertainties surrounding global growth, the 1.7% Q2 GDP growth reading from the US earlier this week, was a welcome surprise. Estimates for growth were closer to 1.2%, so the upside has many now wondering if the US has turned a corner and better days are ahead.

The ISM Manufacturing Index (shown below), a widely watched gauge of manufacturing activity, topped economist estimates of 53.1 and blew past June’s reading of 50.9. In the report, new orders, production, employment, imports, and export orders all showed strength to varying degrees. Interestingly, delivery times were reportedly up as well – a sign of a clogged (read: increasingly active) supply chain.

I’ve discussed my preference for PMI and similar manufacturing-centric data, and looking at this type of data from not just the US, but other parts of the world – notably the Euro Zone – recently makes appear that manufacturing activity is accelerating.

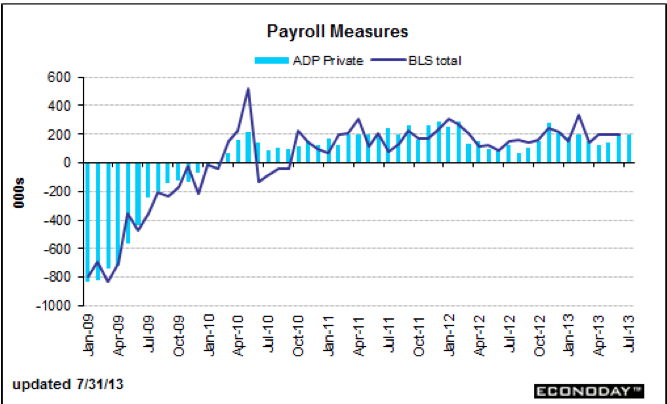

Additionally, the ADP Employment Report, typically a reliable precursor to the nonfarm payroll data, beat expectations of 179,000 new private sector jobs by showing a gain of 200,000. The June number was also revised upwards to show a gain of 198,000 private jobs. It’s important to remember that this report is only an estimate of data coming from 400,000 businesses employing approximately 23,000,000 citizens, so there can be wide variations from month to month when comparing the report to actual nonfarm data. Nevertheless, it has served to be a reliable indicator of what to expect from the “jobs number” and therefore many are expecting a positive surprise from this morning’s announcement.

Have We Turned the Corner?

Unfortunately, no. At least not yet. Though the initial Q2 GDP number came in above estimates, the Q1 number was revised lower to 1.1% (from 1.8%). Looking over the past nine months, the US economy has grown at .9% – hardly enough to get excited about.

The primary culprit appears to be the sting of sequestration, whose automatic spending cuts have clearly made themselves felt. I am not one to argue that government spending is the panacea for growth, but the absence of spending has clearly had an effect on US economic growth. Looking forward, the FT reports:

“On Tuesday, the non-partisan Congressional Budget Office said the sequestration will cost 900,000 jobs and .7% in GDP growth in the next year if it stays in place.”

Two other threats to growth later this year and into 2014 include the need for the US congress to come to terms on a budget for the 2014 fiscal year (in September) and the pending expiration of the debt ceiling – thought to be reckoned with (in November). A delay or outright refusal in resolving these two issues is a clear impediment to sustaining the economic recovery. Give the partisanship on display in the US Congress in recent years, the odds of speedy resolutions to the above issues are long, to say the least.

If the Economy Does Strengthen, Get Ready for Higher Interest Rates

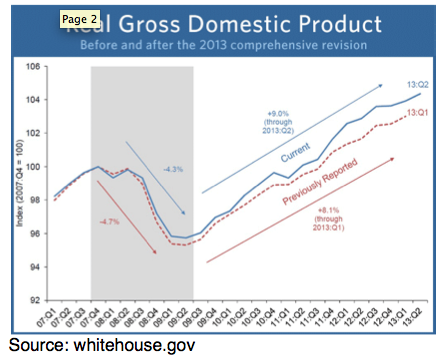

An interesting takeaway from this week’s GDP report was the announcement that the Bureau of Economic Analysis (BEA), responsible for calculating GDP, has revised their data back to 1929. The BEA does this to “better reflect the evolving nature of the US economy.” This makes sense as the US economy grows and evolves to take account for changes in various factors like research and development of technology, for example.

Based on these revisions, there were two primary takeaways. First, GDP in Q1 2013 was revised higher by 3.4% totaling an increase of $551 billion. Essentially, we are wealthier than we were first led to believe – though it may not feel that way! Of course, this is only true if you trust the methodology the BEA uses to calculate GDP. There are several million US citizens out of work who would likely disagree with the BEA’s assessment.

Second, as the chart shows above, the economic contraction during the Great Recession wasn’t as bad as we thought, and the resulting recovery has been stronger than reported. Again, this is likely to spark heated debate – and it should. During the recession, GDP fell by 4.3% versus a 4.7% initial drop and has risen by 9% since versus an 8.1% increase previously calculated.

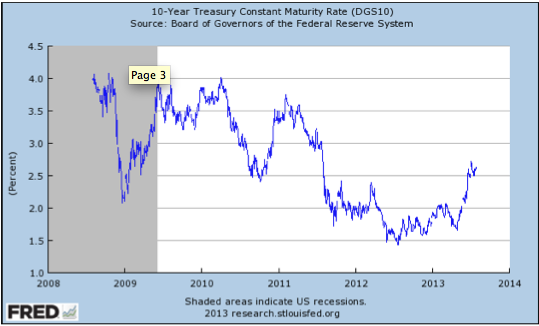

Debates aside, as the economy continues to recover it would appear that higher interest rates, a consequence of economic growth, are in the offing. The current US 10 Year Treasury yields 2.71%, versus 2.48% one month ago and 1.52% one year ago. It seems likely that the increase in yields is due to some degree to economic expansion and less so to Chairman Bernanke’s “taper talk”.

What to Do?

If higher interest rates are in the offing, what strategies should one employ to diversify from interest rate risk? Clearly, hard assets must play a role in your Discovery portfolio in a rising rate environment. Despite the downdraft in precious metals (gold and silver) prices, I still believe they can serve as a reliable and rational hedge against higher rates and the inflationary pressures higher rates imply.

Purchasing physical bullion seems to be preferable, but with the punishment that gold and silver miners have endured in recent months, buying cheap miners who can operate as the lowest cost producers is a prudent way to leverage the possibility of any increase in precious metals prices while hedging against higher interest rates. Billions of dollars in write downs are one indication that share prices may have bottomed and discipline in capital spending and operations can lead shares higher.

In light of this week’s economic data dump, it would appear that we may be at an inflection point, auguring higher interest rates. When the FOMC met earlier this week, the takeaway was that there would be no change in stated policy or rates. Given the economic numbers we’ve witnessed over the past five days, that stated policy may be about to change.

2. Quaterra Resources (QMM AMEX NYSE)

Quaterra (QMM) announced yesterday a $1 million non-dilutive cash infusion from Freeport McMoran (FCX NYSE). This is a long weekend in Canada so perhaps few will see this significant transaction.

Freeport paid Quaterra $1 million for the right to explore Butte. A small monetization but significant in this environment where money is hard to come by. Freeport may now explore the Butte complex and can, hopefully, take it to feasibility with drilling on the property. If so, QMM can take either a 70/30 working interest in the property (QMM 30%) or take a 2% royalty on the property.

We understand this is the third joint venture (JV) between Freeport and Quaterra, the others being the Utah’s South West Tintic and Cave Creek Moly potential in West Texas. Not many Juniors have 3 JVs with a major. Further Goldcorp owns 8% of Quaterra’s shares.

This $1 million non-dilutive contribution is significant to the company’s plans to move forward on its major target which is the Yerington copper property. We expect the company to focus on Yerington.

Terraco Gold’s Todd Hilditch also recently completed a largely non-dilutive $1 million deal. Please see Tuesday’s Morning Note for a description of this transaction by Terraco.

Ed Note: To Join the Mailing List to receive Discovery Investing Morning Notes apply HERE

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

Employers added fewer workers than anticipated in July and the U.S. jobless rate dropped to 7.4 percent, indicating uneven progress in the labor market.

The 162,000 increase in payrolls last month was the smallest in four months and followed a revised 188,000 rise in June that was less than initially estimated, Labor Department figures showed today in Washington. The median forecast of 93 economists surveyed by Bloomberg called for a 185,000 gain. Workers spent fewer hours on the job and hourly earnings fell for the first time since October.

“This isn’t a disaster of a report but it shows the U.S. remains vulnerable to a slower economic growth performance,” said Julia Coronado, chief economist for North America at BNP Paribas in New York, who had projected payrolls would rise by 165,000. “This isn’t the kind of progress the Fed would like to see. At the margin, it keeps them cautious.”

It should come as no surprise that the lessons that should be learned from the bankruptcy of Detroit, a city that once stood as the shining example of America’s industrial might, are being ignored by the American political establishment and its allies in the docile press corps. While the death spiral of the Motor City may be extreme in relation to conditions throughout the country, it is a difference of degree rather than design. In truth, Detroit is our canary in the coal mine. It is succumbing to the same combination of productive decay, government mismanagement, and unmanageable debt that is crushing the rest of us. But as the most sub-prime of all major American cities, the symptoms that are infecting all of us have first become fatal in Detroit.

It should come as no surprise that the lessons that should be learned from the bankruptcy of Detroit, a city that once stood as the shining example of America’s industrial might, are being ignored by the American political establishment and its allies in the docile press corps. While the death spiral of the Motor City may be extreme in relation to conditions throughout the country, it is a difference of degree rather than design. In truth, Detroit is our canary in the coal mine. It is succumbing to the same combination of productive decay, government mismanagement, and unmanageable debt that is crushing the rest of us. But as the most sub-prime of all major American cities, the symptoms that are infecting all of us have first become fatal in Detroit.

Proving that politicians want nothing more than to tell soothing lies to voters, Detroit mayoral candidate Tom Barrow has forcefully asserted that the city’s fiscal crisis is a fiction. In a recent TV interview he described a long term conspiracy by republican and private sector forces to steal assets from Detroit residents, bust the unions, and disenfranchise voters. Not to be outdone in absurdity, MSNBC host Ari Melber concluded that Detroit’s problems result from the libertarian movement to deny residents needed government services. He ignores the fact that Detroit’s government did not whither by choice, but by necessity. Thanks to years of excessive government the city lacks the resources to fund the basic services that even most libertarians support. Others claim that Detroit is just as deserving of federal bailouts as the Big Three or the communities wiped out by natural disasters such as Hurricane Sandy. But there is nothing “natural” about the fiscal disaster in Detroit, and the mistake of bailing out the auto companies should not be compounded on a municipal level.

The real story of Detroit is that its problems are entirely man-made, and can be summed up in seven words. Private enterprise built it, government destroyed it. That is the screaming headline that is unfortunately absent from the media coverage.

In the first half of the 20th Century, Detroit offered good manufacturing jobs to nearly 200,000 workers. The booming labor market caused the City’s population to swell to 1.8 million by mid Century. But the jobs did not come from government programs or public “investments” in education and training. They were in fact created by the vibrancy of American capitalism, the vision of forward thinking industrialists, the strong work ethic of the labor force, and the relative non-interference from government or organized labor. (“The Big Three” auto companies did not begin to bargain collectively with the United Auto Workers until 1941).

Anyone who has ever had the pleasure of encountering a classic American car like a 1934 Oldsmobile 8 Convertible Coupe or a 1941 Chrysler Town & Country should get a sense of why Detroit prospered as it did. Not only were these cars stunning pieces of engineering and craftsmanship, but they were surprisingly affordable for many middle class Americans. The wealth generated by the makers of these cars, and the myriad of lesser manufacturers that serviced them, flowed to all classes of people in Detroit, allowing the city to build great buildings and civic spaces, establish world class arts institutions, and contributed greatly to the country’s cultural achievements.

But as the city reached its zenith, organized labor and government at the state, federal and local levels combined to kill the goose that laid the golden eggs. Although Detroit continued to produce and prosper into the 1950s, the Vietnam era marked a turning point for the auto industry and the city it represented. While the bureaucratic structure and myopic hubris of the largely unchallenged American auto industry certainly contributed to its decline in the post war years, the real blame falls squarely on labor unions and government. Facing the unshakable power of a monopolized labor force backed by the full might of a democratically controlled political machine, the auto companies had to agree to wage hikes, restrictive work rules, and long-term pension commitments that they simply could not survive.

Politically, the voting block dynamics of a heavily unionized municipality created a perfect storm for Detroit. Mayors and councilman were elected based on the ability to continue to promise more to the unions, who of course showered their preferred candidates with campaign funds. And while the auto companies were free to back candidates of their own, there is no substitute for actual voters. As a result, Detroit has been saddled with generations of corrupt and incompetent governments funded by corrupt, incompetent unions. Both camps have essentially no understanding of how their city was built and how the promises they were making to future generations could never be kept once the industries succumbed under the heavy hand of taxation, regulation, and labor coercion.

Today the population of Detroit has declined more than 60% from its peak and the number of manufacturing jobs has fallen by 90% to fewer than 20,000. Meanwhile the city’s municipal debt is now more than $18 billion, which translates into $25,000 per citizen in a city where fewer than half the adult population is employedand nearly half are functionally illiterate. It has promised more than $3 billion to 20,000 city pensioners ($150,000 each) that it simply doesn’t have. Detroit’s Emergency Manager Kevyn Orr recently showed how the City spends 38 cents of every new tax dollar on these “legacy costs,” a figure he expects will grow to 65 cents. This means that there is no money left to run the city. But rather than acknowledging these problems, Detroit politicians, like the aforementioned mayoral candidate, like to pretend that they don’t exist.

Things are no different in Washington. On a national level we have also promised far more than we can deliver. In addition to our acknowledged current national debt of almost $17 trillion ($53,400 per citizen), there is another $87 trillion in unfunded obligations that the Federal government has promised to pay Social Security and Medicare recipients over the next 75 years. (These figures are over and above the projected revenues those programs are scheduled to bring in.) This difference comes to another $290,000 per citizen. Anyone remotely aware of the financial well-being of the average American will know these figures are well beyond our means. But this hasn’t motivated us to reform entitlements in a way that will render them affordable.

Very few politicians are prepared to level with the American people about our fiscal dead end. Similarly, they will not fully acknowledge the extent that government micromanagement of industry through the tax code and overly restrictive labor and health care policies has severely undermined the ability of U.S. industry to compete internationally. As a result, we have seen a steady disappearance of our manufacturing jobs nationally, just like Detroit has. The big difference of course is that Washington has a printing press. In the end, however, that will make little difference.

The good news is that the same forces that built Detroit could help turn it around, if only they were allowed to function. First off, Detroit needs to default on its debt. This means the bond holders and the citizenry will suffer. But after this painful process is complete, Detroit will have a few things going for it. It will boast abundantly cheap real estate and plenty of desperate workers. If government were to relax employment regulations, cut business and sales taxes, crack down on union intimidation tactics, and eliminate the minimum wage, the employers would sense the opportunity and return. Although industry could not offer the kinds of high paying jobs that it had in the past, Detroit would at least be hiring again. Although the city will be set back generations, at least it would be moving. But the left would erupt in fury. We are programmed to perceive such developments as greedy exploitation rather than the natural manner in which capitalism cures excess and starts again at square one. Liberals would rather the unemployed stay that way rather than suffer the degradations of capitalism. So instead of such honest cures, look for Detroit to borrow its way out of the crisis while pretending to fix its chronic problems. If we laugh at their foolishness, we should all look in the mirror.

To order your copy of Peter Schiff’s latest book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital, best-selling author and host of syndicated Peter Schiff Show.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor Newsletter.

Elliott Management’s 22-page letter to investors has something for everyone as Paul Singer ascribes his uniquely independent wisdom. From the fragility of the financial system to the hubris of academic pretenders; from inflation’s various devious impacts on assets and reality to the floundering of the world’s bankers; from America’s “cooked data” to the pending social unrest in Europe and the perils of centralized power, Singers stresses “the temptation to debase fiat currencies… means owning claims on paper money is an act of either faith or denial.” Recent market movements, Singer warns “indicate a world on life-support,” and “for every day, month and year that policymakers try to substitute failed, inappropriate and risky QE policies for pro-growth policies, the debt mounts, as does resentment among middle-income families that their situation is not improving.” The fact of the matter is that “no government has ever reached fiscal ‘nirvana,’ yet our central bank (and its peers) continues to push the envelope of risk, confidence and inflation.” Despite the confident and brave words in which they are wrapped, central bank actions currently seem underscored by quiet panic.

Elliott Management’s 22-page letter to investors has something for everyone as Paul Singer ascribes his uniquely independent wisdom. From the fragility of the financial system to the hubris of academic pretenders; from inflation’s various devious impacts on assets and reality to the floundering of the world’s bankers; from America’s “cooked data” to the pending social unrest in Europe and the perils of centralized power, Singers stresses “the temptation to debase fiat currencies… means owning claims on paper money is an act of either faith or denial.” Recent market movements, Singer warns “indicate a world on life-support,” and “for every day, month and year that policymakers try to substitute failed, inappropriate and risky QE policies for pro-growth policies, the debt mounts, as does resentment among middle-income families that their situation is not improving.” The fact of the matter is that “no government has ever reached fiscal ‘nirvana,’ yet our central bank (and its peers) continues to push the envelope of risk, confidence and inflation.” Despite the confident and brave words in which they are wrapped, central bank actions currently seem underscored by quiet panic.

….read a summary on recent market volatility, the Un-Taper after any Taper, inflation, The Global Economy Turning Up?, ‘Fiat currencies’ and much more HERE

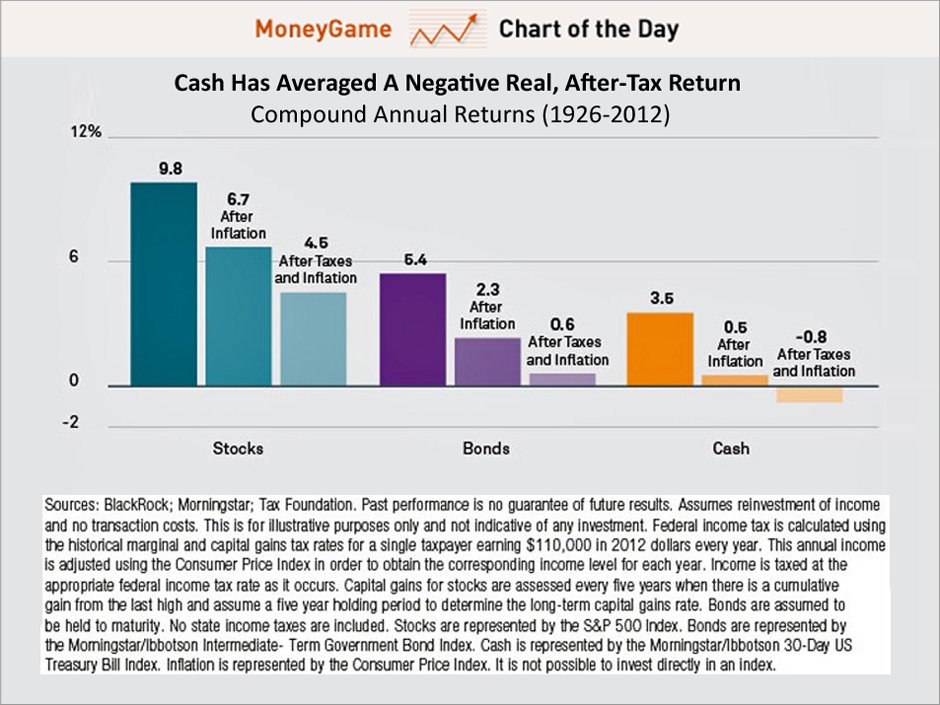

More Americans said they’d rather keep their savings in cold hard cash, even if they wouldn’t need the money for more than 10 years down the line.

After cash, real estate garnered 23% of the vote, followed by gold and other precious metals with 16%.

The stock market ranked the lowest of all, with just 4% of votes.

While no one can blame investors for shying away from the market after the volatile few years we just had, there’s a lot wrong with this line of thinking.

Read what a spooked investor is supposed to do HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair