-

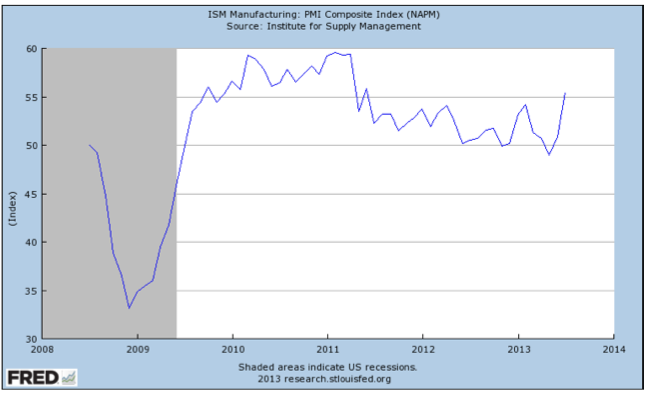

The ISM Manufacturing Index also exceeded estimates, delivering a reading of 55.4 – it’s highest reading since June 2011- indicating growth in the US manufacturing base

-

The overall numbers are good, but not great; today’s release of the non-farm payrolls data should help confirm whether or not the US recovery is set to continue and perhaps accelerate

-

If the economy does “find its legs”, higher interest rates are a given. What to do?

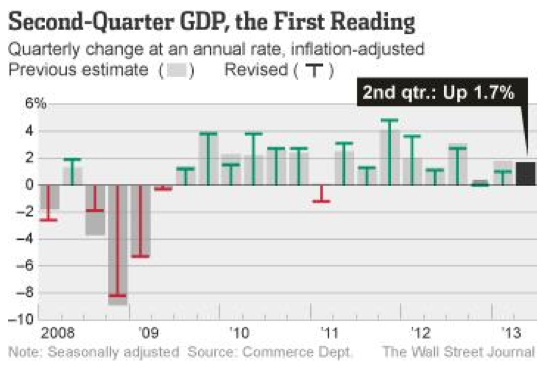

In light of the uncertainties surrounding global growth, the 1.7% Q2 GDP growth reading from the US earlier this week, was a welcome surprise. Estimates for growth were closer to 1.2%, so the upside has many now wondering if the US has turned a corner and better days are ahead.

The ISM Manufacturing Index (shown below), a widely watched gauge of manufacturing activity, topped economist estimates of 53.1 and blew past June’s reading of 50.9. In the report, new orders, production, employment, imports, and export orders all showed strength to varying degrees. Interestingly, delivery times were reportedly up as well – a sign of a clogged (read: increasingly active) supply chain.

I’ve discussed my preference for PMI and similar manufacturing-centric data, and looking at this type of data from not just the US, but other parts of the world – notably the Euro Zone – recently makes appear that manufacturing activity is accelerating.

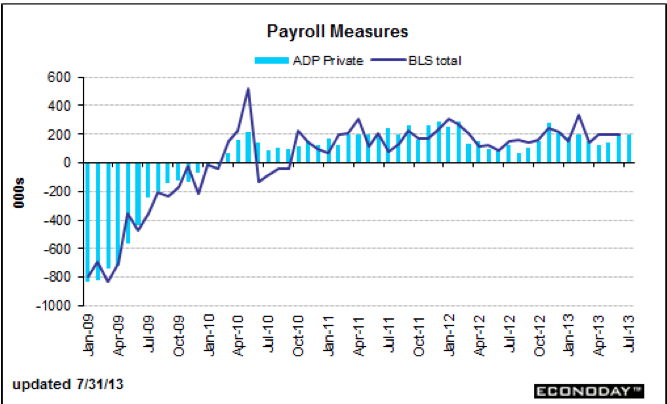

Additionally, the ADP Employment Report, typically a reliable precursor to the nonfarm payroll data, beat expectations of 179,000 new private sector jobs by showing a gain of 200,000. The June number was also revised upwards to show a gain of 198,000 private jobs. It’s important to remember that this report is only an estimate of data coming from 400,000 businesses employing approximately 23,000,000 citizens, so there can be wide variations from month to month when comparing the report to actual nonfarm data. Nevertheless, it has served to be a reliable indicator of what to expect from the “jobs number” and therefore many are expecting a positive surprise from this morning’s announcement.

Have We Turned the Corner?

Unfortunately, no. At least not yet. Though the initial Q2 GDP number came in above estimates, the Q1 number was revised lower to 1.1% (from 1.8%). Looking over the past nine months, the US economy has grown at .9% – hardly enough to get excited about.

The primary culprit appears to be the sting of sequestration, whose automatic spending cuts have clearly made themselves felt. I am not one to argue that government spending is the panacea for growth, but the absence of spending has clearly had an effect on US economic growth. Looking forward, the FT reports:

“On Tuesday, the non-partisan Congressional Budget Office said the sequestration will cost 900,000 jobs and .7% in GDP growth in the next year if it stays in place.”

Two other threats to growth later this year and into 2014 include the need for the US congress to come to terms on a budget for the 2014 fiscal year (in September) and the pending expiration of the debt ceiling – thought to be reckoned with (in November). A delay or outright refusal in resolving these two issues is a clear impediment to sustaining the economic recovery. Give the partisanship on display in the US Congress in recent years, the odds of speedy resolutions to the above issues are long, to say the least.

If the Economy Does Strengthen, Get Ready for Higher Interest Rates

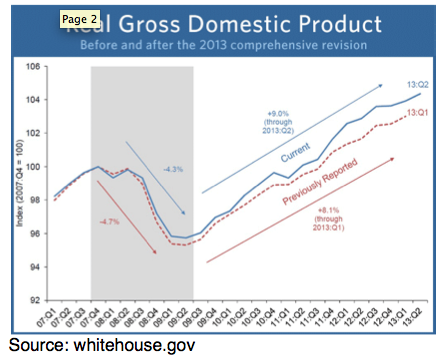

An interesting takeaway from this week’s GDP report was the announcement that the Bureau of Economic Analysis (BEA), responsible for calculating GDP, has revised their data back to 1929. The BEA does this to “better reflect the evolving nature of the US economy.” This makes sense as the US economy grows and evolves to take account for changes in various factors like research and development of technology, for example.

Based on these revisions, there were two primary takeaways. First, GDP in Q1 2013 was revised higher by 3.4% totaling an increase of $551 billion. Essentially, we are wealthier than we were first led to believe – though it may not feel that way! Of course, this is only true if you trust the methodology the BEA uses to calculate GDP. There are several million US citizens out of work who would likely disagree with the BEA’s assessment.

Second, as the chart shows above, the economic contraction during the Great Recession wasn’t as bad as we thought, and the resulting recovery has been stronger than reported. Again, this is likely to spark heated debate – and it should. During the recession, GDP fell by 4.3% versus a 4.7% initial drop and has risen by 9% since versus an 8.1% increase previously calculated.

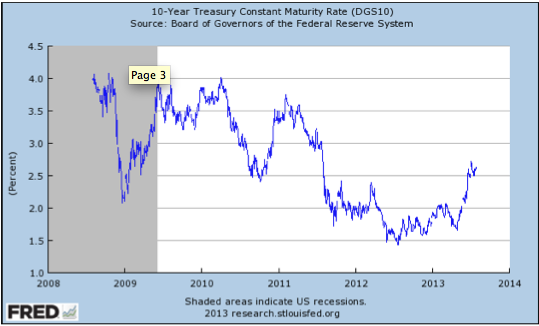

Debates aside, as the economy continues to recover it would appear that higher interest rates, a consequence of economic growth, are in the offing. The current US 10 Year Treasury yields 2.71%, versus 2.48% one month ago and 1.52% one year ago. It seems likely that the increase in yields is due to some degree to economic expansion and less so to Chairman Bernanke’s “taper talk”.

What to Do?

If higher interest rates are in the offing, what strategies should one employ to diversify from interest rate risk? Clearly, hard assets must play a role in your Discovery portfolio in a rising rate environment. Despite the downdraft in precious metals (gold and silver) prices, I still believe they can serve as a reliable and rational hedge against higher rates and the inflationary pressures higher rates imply.

Purchasing physical bullion seems to be preferable, but with the punishment that gold and silver miners have endured in recent months, buying cheap miners who can operate as the lowest cost producers is a prudent way to leverage the possibility of any increase in precious metals prices while hedging against higher interest rates. Billions of dollars in write downs are one indication that share prices may have bottomed and discipline in capital spending and operations can lead shares higher.

In light of this week’s economic data dump, it would appear that we may be at an inflection point, auguring higher interest rates. When the FOMC met earlier this week, the takeaway was that there would be no change in stated policy or rates. Given the economic numbers we’ve witnessed over the past five days, that stated policy may be about to change.

2. Quaterra Resources (QMM AMEX NYSE)

Quaterra (QMM) announced yesterday a $1 million non-dilutive cash infusion from Freeport McMoran (FCX NYSE). This is a long weekend in Canada so perhaps few will see this significant transaction.

Freeport paid Quaterra $1 million for the right to explore Butte. A small monetization but significant in this environment where money is hard to come by. Freeport may now explore the Butte complex and can, hopefully, take it to feasibility with drilling on the property. If so, QMM can take either a 70/30 working interest in the property (QMM 30%) or take a 2% royalty on the property.

We understand this is the third joint venture (JV) between Freeport and Quaterra, the others being the Utah’s South West Tintic and Cave Creek Moly potential in West Texas. Not many Juniors have 3 JVs with a major. Further Goldcorp owns 8% of Quaterra’s shares.

This $1 million non-dilutive contribution is significant to the company’s plans to move forward on its major target which is the Yerington copper property. We expect the company to focus on Yerington.

Terraco Gold’s Todd Hilditch also recently completed a largely non-dilutive $1 million deal. Please see Tuesday’s Morning Note for a description of this transaction by Terraco.

Ed Note: To Join the Mailing List to receive Discovery Investing Morning Notes apply HERE

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.