This Inside Edge commentary was originally posted by Mike on July 8th, 2015 – Ed.

For regular readers of this site – nothing’s changed with the outcome of the Greek referendum. The European Union single currency is still not workable. The euro is still in a long term decline. Interest rates are staying low in Europe, Canada and Japan. Gold’s bear market continues and the US dollar is king.

Any questions?

Oh yeah, oil is going to break $50 and then test the January low.

Forgive my glibness but what we’re witnessing is precisely the scenario I’ve outlined for years. It’s a financial world dominated by central bank action in response to debt with unfunded liability problems just gaining momentum.

On the short term – the challenge with assessing the impact of the Greek debt problem is that we’re not party to all the facts surrounding the response and motivations of the European Central Bank and the European Union. The only certainty is that the Greeks are screwed. For how long depends on the steps taken but given the track record, it’s difficult to be optimistic.

The International Monetary Fund, the EU and the European Central Bank’s primary concern is the protection of the financial system including the European banks while the welfare of Greek citizens is way down their list. And the lenders hold all the cards.

One consideration that has garnered little attention is the strategic importance of Greece to NATO. I suspect the US wants to see Greece stay in the EU even if it does cost the EU billions by cutting a deal on their debt. There are so many options on the table from reducing and extending the debt to giving no further concessions to Greece.

It’s not about what makes sense financially or economically – this is politics.

Short term market gyrations aside, the important point to understand is that Cyprus, Greece and Puerto Rico are the first shoes to drop in the next leg of the debt crisis and there is so much more to come.

China is scary

The waterfall declines of the three prominent stock exchanges in China are a scary reminder of what happens when everyone heads for the exits at the same time. Think about the fact that on Wednesday the Hong Kong index fell 1,458 points (5.8%). The decline from the highs for Shanghai Index of June 12 is over 32% but what’s amazing is that the decline has continued with such ferocity despite overt manipulation by the central bank acting in concert with brokerage houses and major pools of capital.

The problem is that the amount of money borrowed to invest in China has skyrocketed over 450% in the last year (margin debt) – and stocks are now being liquidated to meet margin calls.

This is a reminder that liquidation can happen at a moments notice and the big fear in the stock and bond markets is what happens when sentiment changes and there is a stampede towards the exits. Who will be on the buy side? (see stocks below)

Investments

Gold – the problems in Greece and China gave gold every excuse to rally but it couldn’t break out. That’s consistent with the market action over the last three years and indicative that the downtrend is still in tact. Markets that won’t go up – inevitably do down. I remain on the sidelines.

Oil

I’m very clearly on record as saying since April that the downtrend in oil isn’t over. I would have like to have seen a stronger bounce off the January lows but the low $60s is all it could muster. I stated that this year’s downtrend could mirror last year’s in terms of timing. In other words the downturn starts in late June and gathers momentum.

The 2 million barrels in excess production along with Iran’s increased supply – juxtaposed against flat lining demand from Europe and China should push prices lower. I’ve been saying for months that $50 is the first stop, which then puts the January lows of $42 in play.

Interest rates

Canada’s economy has not recovered from the resource price drop – especially oil. Whether we have just witnessed two consecutive quarters of negative growth in order to satisfy the definition of a recession is irrelevant – the economy’s weak. The Bank of Canada meets on July 15 amidst mounting pressure to lower rates.

Whatever their decision – the low rate environment is here to stay for a good while longer, which will help quality dividend paying stocks whether a correction.

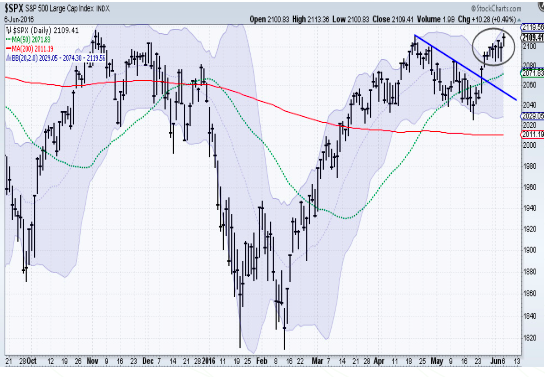

Stocks

The message is that you can’t wait til everyone else wants to exit to get out. There is a herd mentality evident in the 79 trillion investment dollars under management that could turn an ordinary correction into something more nasty.

The question I’m considering is whether the troubles in China, Europe and Japan will encourage capital to come to the US and make its way into quality US stocks. My answer is yes. On the short term I won’t be surprised if credit worries drag stocks down but longer term I remain bullish on quality yield plays and the overall market.

The warning is that it could be nasty along the way, which is why I continue to raise cash by selling some growth oriented stocks that have had a good run. I only want to own companies with very high quality balance sheet . With this much uncertainty what’s wrong with a little “safe than sorry” approach.

The US dollar

The uncertainty in Europe and the accompanying rush into US dollars verify the advice I’ve given since Oct 2012 – and that is sell the loonie on bounces and buy US dollars.

The loonie looks ready to test the March low in the 78 cent range and test 76 cents, which puts the 70 cent level in play.

For regular readers of this site – nothing’s changed with the outcome of the Greek referendum. The European Union single currency is still not workable. The euro is still in a long term decline. Interest rates are staying low in Europe, Canada and Japan. Gold’s bear market continues and the US dollar is king.

Any questions?

Oh yeah, oil is going to break $50 and then test the January low.

Forgive my glibness but what we’re witnessing is precisely the scenario I’ve outlined for years. It’s a financial world dominated by central bank action in response to debt with unfunded liability problems just gaining momentum.

On the short term – the challenge with assessing the impact of the Greek debt problem is that we’re not party to all the facts surrounding the response and motivations of the European Central Bank and the European Union. The only certainty is that the Greeks are screwed. For how long depends on the steps taken but given the track record, it’s difficult to be optimistic.

The International Monetary Fund, the EU and the European Central Bank’s primary concern is the protection of the financial system including the European banks while the welfare of Greek citizens is way down their list. And the lenders hold all the cards.

One consideration that has garnered little attention is the strategic importance of Greece to NATO. I suspect the US wants to see Greece stay in the EU even if it does cost the EU billions by cutting a deal on their debt. There are so many options on the table from reducing and extending the debt to giving no further concessions to Greece.

It’s not about what makes sense financially or economically – this is politics.

Short term market gyrations aside, the important point to understand is that Cyprus, Greece and Puerto Rico are the first shoes to drop in the next leg of the debt crisis and there is so much more to come.

China is scary

The waterfall declines of the three prominent stock exchanges in China are a scary reminder of what happens when everyone heads for the exits at the same time. Think about the fact that on Wednesday the Hong Kong index fell 1,458 points (5.8%). The decline from the highs for Shanghai Index of June 12 is over 32% but what’s amazing is that the decline has continued with such ferocity despite overt manipulation by the central bank acting in concert with brokerage houses and major pools of capital.

The problem is that the amount of money borrowed to invest in China has skyrocketed over 450% in the last year (margin debt) – and stocks are now being liquidated to meet margin calls.

This is a reminder that liquidation can happen at a moments notice and the big fear in the stock and bond markets is what happens when sentiment changes and there is a stampede towards the exits. Who will be on the buy side? (see stocks below)

Investments

Gold – the problems in Greece and China gave gold every excuse to rally but it couldn’t break out. That’s consistent with the market action over the last three years and indicative that the downtrend is still in tact. Markets that won’t go up – inevitably do down. I remain on the sidelines.

Oil

I’m very clearly on record as saying since April that the downtrend in oil isn’t over. I would have like to have seen a stronger bounce off the January lows but the low $60s is all it could muster. I stated that this year’s downtrend could mirror last year’s in terms of timing. In other words the downturn starts in late June and gathers momentum.

The 2 million barrels in excess production along with Iran’s increased supply – juxtaposed against flat lining demand from Europe and China should push prices lower. I’ve been saying for months that $50 is the first stop, which then puts the January lows of $42 in play.

Interest rates

Canada’s economy has not recovered from the resource price drop – especially oil. Whether we have just witnessed two consecutive quarters of negative growth in order to satisfy the definition of a recession is irrelevant – the economy’s weak. The Bank of Canada meets on July 15 amidst mounting pressure to lower rates.

Whatever their decision – the low rate environment is here to stay for a good while longer, which will help quality dividend paying stocks whether a correction.

Stocks

The message is that you can’t wait til everyone else wants to exit to get out. There is a herd mentality evident in the 79 trillion investment dollars under management that could turn an ordinary correction into something more nasty.

The question I’m considering is whether the troubles in China, Europe and Japan will encourage capital to come to the US and make its way into quality US stocks. My answer is yes. On the short term I won’t be surprised if credit worries drag stocks down but longer term I remain bullish on quality yield plays and the overall market.

The warning is that it could be nasty along the way, which is why I continue to raise cash by selling some growth oriented stocks that have had a good run. I only want to own companies with very high quality balance sheet . With this much uncertainty what’s wrong with a little “safe than sorry” approach.

The US dollar

The uncertainty in Europe and the accompanying rush into US dollars verify the advice I’ve given since Oct 2012 – and that is sell the loonie on bounces and buy US dollars.

The loonie looks ready to test the March low in the 78 cent range and test 76 cents, which puts the 70 cent level in play.