Inside Edge Sample Articles

Price is what you pay, value is what you get.

“Price is what you pay. Value is what you get”, a quote uttered famously by Warren Buffett in his 2008 annual letter to the Berkshire Hathaway’s shareholders. Price and value are two sides of the same coin. Understanding the difference between price and value is the core principle of value investing. It is also core to KeyStone’s hybrid strategy which involves buying growth & dividend growth stocks that offer GARP or growth at a reasonable price. We are not always looking for the cheapest stocks on the market, nor will we pay anything for a business – we look for a reasonable price, for a good business.

Unfortunately, particularly in the technology sector, that principle had been largely ignored over the past 12-18 months by investors chasing growth at any price and it is coming home to roost.

Let’s take a quick look at investor sentiment that has led us to where we are today. Under-communicated by the broader indexes has been the stealth crash in growth tech and risk-oriented stocks.

This chart authors an alarming story. While the NASDAQ index itself rose to the end of 2021, by the start of 2022, over 40% of NASDAQ stocks were down 50% from their highs on the year.

How can this happen? Two things are at play. Number one being the dominance of the “MegaCap-8”, Alphabet, Amazon, Apple, Meta, Microsoft, Netflix, NVIDIA, and Tesla. The combined market cap of these tech behemoths has surged over the past 10 years (including in 2021) to just under $10 trillion, giving them incredible influence on the broader indexes.

Chart created by: Yardeni Research Inc.

The MegaCap-8 now make up almost one quarter of the entire S&P 500 and over half the NASDAQ 100.

Chart created by: Yardeni Research Inc.

The result, a strong year of gains (as we saw for the MegaCap-8 in 2021) can mask losses, even significant losses, elsewhere in the index.

But why close to 50% of Nasdaq stocks down over 50% from their 2021 high?

A major theme heading up to the pandemic and immediately following has been massive capital inflow into “disruptors or innovation stocks” – stocks that promise to change the world and become the next Google, Microsoft or Apple. The problem being, while a number are excellent growth businesses, including the likes of CrowdStrike Holdings Inc. (CRWD:NASDAQ) and DocuSign Inc. (DOCU:NASDAQ), the multiples investors were willing to pay to sales and cash flow (if present) were historically high. In other names such as EV hopeful, Rivian Automotive Inc. (RIVN:NADAQ) and, in Canada, e-commerce payment enabler Lightspeed Commerce Inc. (LSPD:TSX), cash flow was negative, and price-to-sales multiples were 50-150 times plus.

Perhaps the poster child for the euphoric buying in tech disruptors is the Ark Innovation Fund, run by recent market darling, Cathie Wood. Outside of Tesla, the fund does not own the Mega-Cap-8 but rather a basket of disruptor and innovation stocks. As such, it is a decent proxy for the stealth crash. To be clear, the fund performed very well for a 3-4 year run as money piled into these stocks. But the Ark ETF has lost billions with its unit price down 34% in the last 3 months and approximately 51% over the past year. The Fund is down 36% to start 2022.

We took a quick look at the current valuations (post stealth crash) of the top holdings in the Ark Innovation Fund removing Tesla (as one of the MegaCap-8) from the equation. To give readers context, the average market PE is 23 trailing and 19-20 trailing at present. Only one of the fund’s top 12 holdings has a PE of under 30. Seven of the 12 companies do not appear to report current earnings or even adjusted earnings and while the price-to-sales multiples have decreased, historically they remain high.

Investors were buying stocks symbols (price) with little consideration for value. Remember, price is what you pay, value is what you get. Euphoric buying in these disruptor hopefuls fueled by cheap money, record stimulus and low rates has led to little value in this space over the past year and a significant correction, however stealthy it may be, is not surprising.

The market tends to remind you, that one cannot just pay any price for most stocks.

To give you an idea of how overvalued many of these disruptor hopefuls were trading at 50-150 times sales, below is a quick breakdown on the peak valuations on some of the best true disruptive tech companies over the past couple of decades.

Even in this list of true once in a lifetime investments, not one came close to a price-to-sales multiples of even 45.

It appears value is beginning to matter once again.

With that in mind, while we have continued to recommend long-term holding such as Microsoft and Alphabet, which remain at relatively reasonable valuations, we are keeping a keen eye on around 30 cash flow positive mid-to-large-cap US SaaS technology names. Stocks which have dropped in value in sympathy with the sector and may finally fall within our GARP model.

In the meantime, we are seeing some select value in unique Canadian tech and diversified names that, while not the sexiest stories on the Street, provide growth with reasonable value.

The first, Calian Group Ltd. (CGY:TSX) ($64.50), a diverse products and services company providing innovative healthcare, communications, learning and cybersecurity solutions, recently announced a solid acquisition in its IT/cyber-security division.

Calian trades with a forward EV/EBITDA multiple of approximately 11 times. We expect revenue growth of ~18% in 2022. If Calian can achieve the mid-range of F2022 guidance and we add in ~$40 million from Computex (IT/Cyber-security), at an EV/EBITDA multiple of 13 times, we see fair value at ~$76.

The second, TELUS International (TI) Inc. (TIXT:TSX) ($32.45), a digital customer experience innovator that designs, builds, and delivers next-generation solutions, including AI and content moderation, for global and disruptive brands (I see innovator & disruptive in that description), just reported solid FY2021 growth numbers and a solid growth outlook for FY2022.

TI trades at 22 times FY2022 expected earnings and with an EV/EBITDA of approximately 13x. While we expect EBITDA margins to moderate in the first half of 2022 as the company ramps growth investments to support anticipated organic growth acceleration next year, margins should pick up by the end of 2022 and still remain at the top end of its segment. Our fair value for the stock is $44 over the next 12 months with an estimated holding period of 2-3 years. Following a slight disappointment in terms of margin guidance, the stock may weaken near-term, which should be an opportunity with revenue and earnings expected to grow 17% and 21% respectively in the coming year without including further acquisitions.

Finally, we will highlight a unique cash rich, but higher risk business which continues to perform well from our Canadian Small-Cap coverage. Dynacor Gold Mines Inc. (DNG:TSX) ($3.20), has seen its share price jump over 75% over the past year powered by tremendous growth. The company is engaged in gold production through the processing of ore at its modern mill in Southern Peru purchased from the ASM (artisanal and small-scale mining) industry.

FY2021 revenues jumped 93% to US$195.9 million or CDN$245.6 million for the year. We expect earnings to exceed guidance of between $9.0 to $9.5 million (US$0.23 to US$0.25 per share). Dynacor’s shares trade at just 8 times current year’s expected earnings. FY2022 guidance is expected shortly, and we expect further growth and the potential of another dividend increase in 2022 after two significant increases in 2021. The stock currently yields 3.15%.

Dynacor holds a strong balance sheet with US$17.8 million in cash and no debt to fund expansion at its existing plant in Peru and geographic expansion. Management intends to expand its processing operations in other jurisdictions (West Africa or other Latin American Countries are options) over the next 3-5 years. We maintain our SPEC BUY rating on the stock with near-term fair value in the range of $4.00-$4.25 – a figure we expect to update through FY2022.

Disclosures:

Ryan Irvine is the founder of KeyStone Financial an independent financial research firm established in 1998. KeyStone provides BUY/SELL reports on profitable growing Canadian & U.S. growth & dividend growth stocks to help Canadians construct simple 15-25 stock portfolios. More information found at: www.keystocks.com or 1-888-27-STOCK. Disclosures: KeyStone or employees own positions in GOOG, MSFT, CGY, and DNG. The information provided is general in nature and does not represent investment advice. Every effort has been made to compile this material from reliable sources; however, no warranty can be made as to its accuracy or completeness. Before acting on any of the above, please consult an appropriate professional regarding your particular circumstances.

Sample inside edge postings

Greg breaks down the market response to Monday’s US political debate, offers his macro market updates and dives into Stephen Poloz’s recent comments and the technical implications for the Canadian dollar.

originally posted July 29th, 2016

When the Federal Reserve raised interest rates a measly 0.25% last December, some investors thought it was about time.

After all, pundits had been warning of rising rates.

But many investors (KeyStone included) were skeptical that the U.S. economy was ready for liftoff. Instead, they saw a failure to launch.

Investors are now acting like another rate hike in 2016 is nigh impossible. After an ugly May jobs report, an expected June rate hike was quickly tabled.

While the writing continues to be on the wall for a continued extended period of low rates, investors still haven’t gotten the memo: Get used to low rates.

Action: Buy dividend growers (but we will get back to this).

To be sure, the vast majority of investors are hopeful that the recovery will stick, so it’s natural to believe the U.S. economy is stronger and more prepared for tighter monetary policy than what is reality. But like it or not, the U.S. continues to suffer the overhang from an unusually deep and long-lasting recession — a “secular stagnation” where output and employment measures remain weak in the long-term despite aggressive monetary policies.

The fact that the U.S. has not seen inflation-adjusted GDP growth above 3% for a decade, and still may not see a growth rate that robust for several more years is a bitter pill – but it’s the reality.

We also live in a new technological and globalized era, where the economic models of 2016 tend to conserve much more capital than in ages past when there was more demand for big investments in labor and brick-and-mortar facilities. The Amazon’s and Ubers of the world help us access goods and services more quickly and at lower cost, but there isn’t the same level of capital investment as there was under the old model of big-box stores and Yellow Cab buying a fleet of Ford Taurus’s.

The sad reality is that until and unless the U.S. posts employment metrics that are consistently strong, or inflation rises significantly and stays elevated, there simply isn’t a case for hiking interest rates this month, this year — and even next year.

So what does this mean for your portfolio – if you are seeking yield, bonds, t-bills, GICs, etc. will continue to leave you wanting.

The answer may continue to be Dividend Growth Stocks – or those stocks that consistently growth their dividends and the underlying business over time.

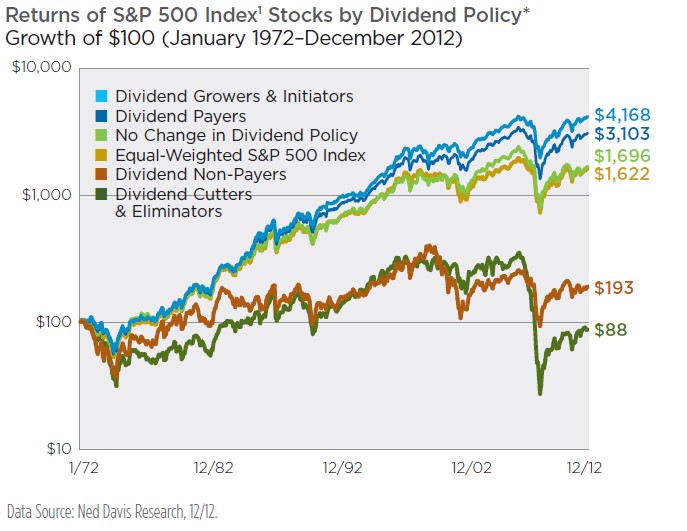

The graph below (from Ned Davis Research) clearly illustrates that over a 30 year time horizon, dividend stocks on the S&P500 generated a total return of 10.19% per year compared to the 4.39% generated from non-dividend stocks (a nearly 6% difference). We can also see from the graph that this margin of superior performance has widened in the more recent years.

The true out-performers were the dividend “growers” and those that initiated dividends due to their consistent and growing cash flow.

While no dividend – or stock – is 100% guaranteed, the market always provides some select opportunities to buy strong, well-capitalized companies with solid dividend yields and the potential to growth them long-term. These are the stocks you want to own.

Here’s how to find them

All dividend payers are not created equal, and you want to find the ones that have the businesses to back up their payments. Strong businesses will maintain or even increase their dividends, even in a market like this one.

So how do you tell if a business is strong? Many people use the earnings payout ratio (dividends per share / earnings per share), but those numbers aren’t always reliable because a company can strategically adjust net income for any number of reasons.

Rather, focus on the free cash flow payout ratio. It’s much more difficult to fake the cash flow, and that means investors can have more confidence in it as a measure of dividend health.

Ideally, you want to find companies with free cash flow payout ratios below 80% (we often see dividend growers with payout ratios of 50% and below), which demonstrates that the company has an adequate cash cushion to maintain its dividend payments — and even raise them.

But spread your bets.

It’s important to keep in mind that no individual company, however strong, is immune to the kind of sectorwide that brought down energy stocks in 2015 for example — even after many “big oils” paid uninterrupted dividends for years. That’s why diversification across sectors is important, even if that means sacrificing a little yield.

But do not over-diversify – we recommend selecting 10-12 individual dividend growth stocks. And take your time. Twelve to sixteen months is often necessary.

How to BUY Dividend Growers

One of the simplest ways is through and ETF. The iShares S&P US Dividend Growers Index Fund (CUD) aims to replicate the performance of the S&P High Yield Dividend Aristocrats CAD Hedged Index, net of expenses. The Index selects the 60 highest dividend yielding stocks in the S&P Composite 1500 Index that have increased dividends every year for at least 25 consecutive years. The Index is weighted by indicated annual dividend yield, with constituents being reweighed every quarter.

For our Canadian readers: iShares US Dividend Growers Index ETF (CAD-Hedged) (CUD.A)

Why CUD.A?

1. Exposure to high yielding U.S. companies with a track record of growing dividends over time.

2. Underlying index screens for high yielding U.S. stocks that have also increased dividends for at least 20 consecutive years.

3. Earn a regular, potentially growing, monthly dividend income stream.

Or you could buy big, stalwart, dividend growers like Johnson & Johnson (JNJ:NYSE).

Johnson & Johnson is the largest health care corporation in the world. The company was founded in 1886 and currently has a market cap of more than $280 billion.

There are two telling numbers to remember when analyzing Johnson & Johnson stock: 31 and 53. As in 31 consecutive years of adjusted earnings-per-share increases and 53 consecutive years of dividend increases.

In addition to these impressive metrics, Johnson & Johnson has one of the lowest stock price standard deviations of any company. With its low volatility and long history of predictable growth, Johnson & Johnson has more in common with a utility (except it has better growth prospects) than with most other health care corporations.

But we think there is a better way.

Create your own Canadian Dividend Grower Stock Portfolio composed of smaller, high growth dividend payers that remain “off the radar” of the broader market.

Select dividend growers that trade at great valuations.

Exco Technologies Limited (XTC:TSX) – a dividend growth small-cap from our coverage.

In each of the past 4 years since our recommendation, Exco has increased its dividend.

Industry: Manufacturing – Extrusion & Automotive

Recommended: June 2011

Recommendation Price: $3.90

Current Price: $12.66

Market Cap: $537,113,160

Shares Outstanding: 42,426,000

Fully Diluted: 42,693,000

With roots that date back to 1952, Exco is a global supplier of innovative technologies servicing the die-cast, extrusion and automotive industries. Through 18 strategic locations in 10 countries, the company employs 6,515 people and service a diverse and broad customer base.

Last Week the Company Posted Record Quarterly Revenues & Earnings

• Record Sales and Earnings in the quarter.

• EPS of $0.30 up 25% adjusted for non-recurring gain.

• AFX acquisition performing strongly.

• Financial position and liquidity remain solid.

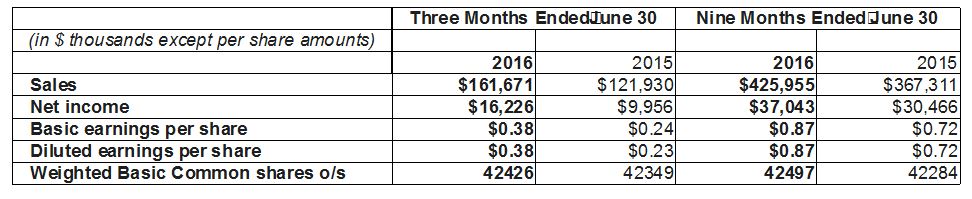

Consolidated sales for the third fiscal quarter ended June 30, 2016 were a record $161.7 million – an increase of $39.7 million or 33% over last year. The acquisition of AFX Industries LLC (AFX) closed April 4, 2016 and performed strongly, contributing $31.0 million to sales.

Net income was $16.2 million or $0.38 per share including $3.4 million from the settlement of a commercial arbitration. Excluding the gain, EPS was $0.30, up 28% from the third quarter of fiscal 2015.

We see the recent drop in Exco’s shares as an opportunity. AFX has begun contributing to earnings in the current quarter, and we expect the acquisition produce meaningful growth for Exco as a whole once again. AFX had revenue of approximately C$115 million (equivalent) in 2015. Exco expects the acquisition will be highly accretive to its earnings per share and initial proof of this was seen in Q2. We expect the 12-month earnings run-rate (pro-forma) for the company with AFX included is in the range of $1.30 – the stock is now trading at and attractive 9.7 times that estimate. EV/EBITDA is approximately 6.3 based on pro-forma EBITDA – this is also relatively attractive.

While the company’s industry is cyclical, we believe the current environment appears positive for the next 12 months. As such, we maintain our BUY recommendation and the company’s place in our Focus BUY Portfolio.

Another long-time favourite dividend grower is Enghouse Systems Ltd. (ESL:TSX), a Canadian software-based company we recommended 6-years ago in the $8.00 range, which has also increased its dividend every year since. While it is no longer cheap, the company has the potential to continue to outperform long-term.

These are just two companies to begin building you Canadian Dividend Grower Stock

Here are the two key items to watch in the aftermath of the Brexit vote. But first, allow me to say how pathetic it is that you won’t read about either one of them in the Canadian media. Why? Because with the notable exceptions of Rex Murphy, Terrance Corcoran and Colby Cosh – the media continually sings from the establishment songbook – along with organized labour, crony capitalists, politicians and the educational establishment.

I’ll get lots of time to go into that further in my editorials, so for now let me say that not one commentator in the country predicted Brexit and shows any sign of understanding it. To say the outcome was a surprise is mindboggling – given the massive rise of anti-EU sentiment through-out Europe well before this vote.

Obviously not a surprise to Moneytalks listeners given I have been talking about the demise of the EU since April, 2010 – and once the vote was announced in 2013 unequivocally stated that it would mark a key date in the EU’s demise. And there is so much more to come.

The Key Points

1. It’s a big mistake to think that this was about politics. Just like the volatility in currencies, stocks etc – the political volatility is a by-product of economics and finance. Hence look to events in those two areas to illuminate what comes next.

The changes through-out the Western World will be driven by debt problem, lack of economic growth and massive entitlement failures. Issues like the gross mishandling of the refugee influx simply exacerbates social problems and becomes a lightening rod for the underlying economic and financial problems.

The anti-establishment sentiment that has seems to have just dawned on media commentators is rooted in economic and financial failure – not politics, which guarantees so much more turmoil to come.

2. This is huge. The euro is no longer going to be consider a global currency. There will be a massive rebalancing of portfolios to reflect that. But where will the money go? My consistent position has been that the first choice will be the US dollar. Before Brexit – there were only 3 ½ currencies in the world that can absorb major capital flows – the US dollar, the euro, the yen – and the half part, the pound.

The euro is now out – Japan’s economic stagnation and demographic problems make it less attractive – and the future of the pound is up in the air. Hence – I continue to look to the US dollar and US denominate assets as the big beneficiary.

Stocks

The markets reacted to the uncertainty – fueled by the outrageous remarks of the “remain” side leaders like David Cameron who said that a “leave” vote would result in a world war – the International Institute of Finance called it Europe’s Lehman Moment – ie triggering another global credit disaster.

As usual they overreacted so now the short term tug of war will be between those forced to meet margin calls by selling – and bargain hunters. Keep in mind that this is a single story driven market event and those moves usually last 2 to 3 days. In this case it may be even shorter. If you were going to sell because of Brexit – you probably already have – Monday at the latest.

So the key for the markets is – what’s next in terms of big stories. The one that worries me is the precarious financial position of the Euro banks, who are already in big trouble. If negative news on that front hits then expect a lot of negative market follow- through. I promise the central banks are well aware of this and are prepared to do whatever it takes to prevent a credit induced liquidation.

Overall – I still think that in the long term a major bull market in US stocks will be fueled by huge outflows of capital from Europe over the next four years.

One more warning

China’s currency manipulation is a major threat to global finances. Further devaluation or floating it would cause massive disruption. More on this later…

Gold

For the first time in 6 years, gold reacted as a safe haven along with the predictable up moves in the US$ and bonds, Swiss bonds and German bonds. The fact that gold joined this group in the immediate aftermath of the vote is significant in the short term.

I don’t know if I’m stuck on my own scenario but I still think the big move comes when confidence in the US drops. The move right now is a reflection of waning confidence in the EU.

What’s promising is that major investors are considering gold as an alternative currency. They’re taking long term positions – and I think they’ll be rewarded when the US dollar comes into question.

Here are the two key items to watch in the aftermath of the Brexit vote. But first, allow me to say how pathetic it is that you won’t read about either one of them in the Canadian media. Why? Because with the notable exceptions of Rex Murphy, Terrance Corcoran and Colby Cosh – the media continually sings from the establishment songbook – along with organized labour, crony capitalists, politicians and the educational establishment.

I’ll get lots of time to go into that further in my editorials, so for now let me say that not one commentator in the country predicted Brexit and shows any sign of understanding it. To say the outcome was a surprise is mindboggling – given the massive rise of anti-EU sentiment through-out Europe well before this vote.

Obviously not a surprise to Moneytalks listeners given I have been talking about the demise of the EU since April, 2010 – and once the vote was announced in 2013 unequivocally stated that it would mark a key date in the EU’s demise. And there is so much more to come.

The Key Points

1. It’s a big mistake to think that this was about politics. Just like the volatility in currencies, stocks etc – the political volatility is a by-product of economics and finance. Hence look to events in those two areas to illuminate what comes next.

The changes through-out the Western World will be driven by debt problem, lack of economic growth and massive entitlement failures. Issues like the gross mishandling of the refugee influx simply exacerbates social problems and becomes a lightening rod for the underlying economic and financial problems.

The anti-establishment sentiment that has seems to have just dawned on media commentators is rooted in economic and financial failure – not politics, which guarantees so much more turmoil to come.

2. This is huge. The euro is no longer going to be consider a global currency. There will be a massive rebalancing of portfolios to reflect that. But where will the money go? My consistent position has been that the first choice will be the US dollar. Before Brexit – there were only 3 ½ currencies in the world that can absorb major capital flows – the US dollar, the euro, the yen – and the half part, the pound.

The euro is now out – Japan’s economic stagnation and demographic problems make it less attractive – and the future of the pound is up in the air. Hence – I continue to look to the US dollar and US denominate assets as the big beneficiary.

Stocks

The markets reacted to the uncertainty – fueled by the outrageous remarks of the “remain” side leaders like David Cameron who said that a “leave” vote would result in a world war – the International Institute of Finance called it Europe’s Lehman Moment – ie triggering another global credit disaster.

As usual they overreacted so now the short term tug of war will be between those forced to meet margin calls by selling – and bargain hunters. Keep in mind that this is a single story driven market event and those moves usually last 2 to 3 days. In this case it may be even shorter. If you were going to sell because of Brexit – you probably already have – Monday at the latest.

So the key for the markets is – what’s next in terms of big stories. The one that worries me is the precarious financial position of the Euro banks, who are already in big trouble. If negative news on that front hits then expect a lot of negative market follow- through. I promise the central banks are well aware of this and are prepared to do whatever it takes to prevent a credit induced liquidation.

Overall – I still think that in the long term a major bull market in US stocks will be fueled by huge outflows of capital from Europe over the next four years.

One more warning

China’s currency manipulation is a major threat to global finances. Further devaluation or floating it would cause massive disruption. More on this later…

Gold

For the first time in 6 years, gold reacted as a safe haven along with the predictable up moves in the US$ and bonds, Swiss bonds and German bonds. The fact that gold joined this group in the immediate aftermath of the vote is significant in the short term.

I don’t know if I’m stuck on my own scenario but I still think the big move comes when confidence in the US drops. The move right now is a reflection of waning confidence in the EU.

What’s promising is that major investors are considering gold as an alternative

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair