originally posted July 29th, 2016

When the Federal Reserve raised interest rates a measly 0.25% last December, some investors thought it was about time.

After all, pundits had been warning of rising rates.

But many investors (KeyStone included) were skeptical that the U.S. economy was ready for liftoff. Instead, they saw a failure to launch.

Investors are now acting like another rate hike in 2016 is nigh impossible. After an ugly May jobs report, an expected June rate hike was quickly tabled.

While the writing continues to be on the wall for a continued extended period of low rates, investors still haven’t gotten the memo: Get used to low rates.

Action: Buy dividend growers (but we will get back to this).

To be sure, the vast majority of investors are hopeful that the recovery will stick, so it’s natural to believe the U.S. economy is stronger and more prepared for tighter monetary policy than what is reality. But like it or not, the U.S. continues to suffer the overhang from an unusually deep and long-lasting recession — a “secular stagnation” where output and employment measures remain weak in the long-term despite aggressive monetary policies.

The fact that the U.S. has not seen inflation-adjusted GDP growth above 3% for a decade, and still may not see a growth rate that robust for several more years is a bitter pill – but it’s the reality.

We also live in a new technological and globalized era, where the economic models of 2016 tend to conserve much more capital than in ages past when there was more demand for big investments in labor and brick-and-mortar facilities. The Amazon’s and Ubers of the world help us access goods and services more quickly and at lower cost, but there isn’t the same level of capital investment as there was under the old model of big-box stores and Yellow Cab buying a fleet of Ford Taurus’s.

The sad reality is that until and unless the U.S. posts employment metrics that are consistently strong, or inflation rises significantly and stays elevated, there simply isn’t a case for hiking interest rates this month, this year — and even next year.

So what does this mean for your portfolio – if you are seeking yield, bonds, t-bills, GICs, etc. will continue to leave you wanting.

The answer may continue to be Dividend Growth Stocks – or those stocks that consistently growth their dividends and the underlying business over time.

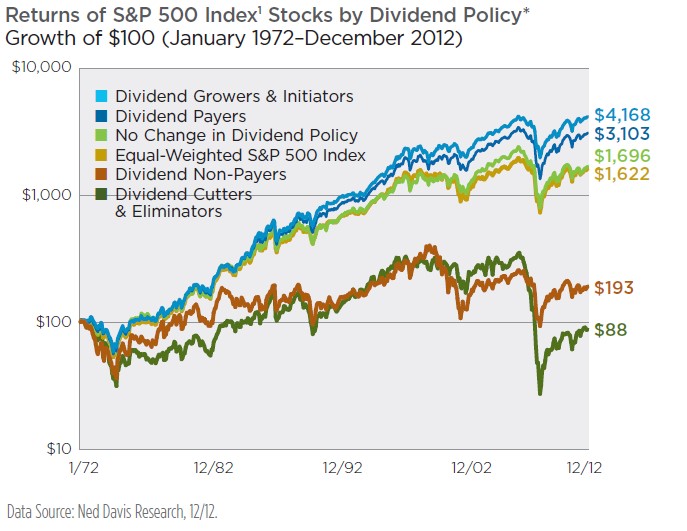

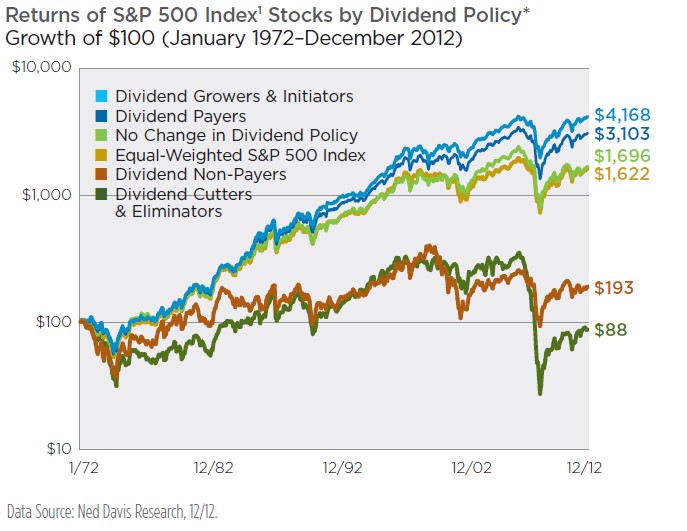

The graph below (from Ned Davis Research) clearly illustrates that over a 30 year time horizon, dividend stocks on the S&P500 generated a total return of 10.19% per year compared to the 4.39% generated from non-dividend stocks (a nearly 6% difference). We can also see from the graph that this margin of superior performance has widened in the more recent years.

The true out-performers were the dividend “growers” and those that initiated dividends due to their consistent and growing cash flow.

While no dividend – or stock – is 100% guaranteed, the market always provides some select opportunities to buy strong, well-capitalized companies with solid dividend yields and the potential to growth them long-term. These are the stocks you want to own.

Here’s how to find them

All dividend payers are not created equal, and you want to find the ones that have the businesses to back up their payments. Strong businesses will maintain or even increase their dividends, even in a market like this one.

So how do you tell if a business is strong? Many people use the earnings payout ratio (dividends per share / earnings per share), but those numbers aren’t always reliable because a company can strategically adjust net income for any number of reasons.

Rather, focus on the free cash flow payout ratio. It’s much more difficult to fake the cash flow, and that means investors can have more confidence in it as a measure of dividend health.

Ideally, you want to find companies with free cash flow payout ratios below 80% (we often see dividend growers with payout ratios of 50% and below), which demonstrates that the company has an adequate cash cushion to maintain its dividend payments — and even raise them.

But spread your bets.

It’s important to keep in mind that no individual company, however strong, is immune to the kind of sectorwide that brought down energy stocks in 2015 for example — even after many “big oils” paid uninterrupted dividends for years. That’s why diversification across sectors is important, even if that means sacrificing a little yield.

But do not over-diversify – we recommend selecting 10-12 individual dividend growth stocks. And take your time. Twelve to sixteen months is often necessary.

How to BUY Dividend Growers

One of the simplest ways is through and ETF. The iShares S&P US Dividend Growers Index Fund (CUD) aims to replicate the performance of the S&P High Yield Dividend Aristocrats CAD Hedged Index, net of expenses. The Index selects the 60 highest dividend yielding stocks in the S&P Composite 1500 Index that have increased dividends every year for at least 25 consecutive years. The Index is weighted by indicated annual dividend yield, with constituents being reweighed every quarter.

For our Canadian readers: iShares US Dividend Growers Index ETF (CAD-Hedged) (CUD.A)

Why CUD.A?

1. Exposure to high yielding U.S. companies with a track record of growing dividends over time.

2. Underlying index screens for high yielding U.S. stocks that have also increased dividends for at least 20 consecutive years.

3. Earn a regular, potentially growing, monthly dividend income stream.

Or you could buy big, stalwart, dividend growers like Johnson & Johnson (JNJ:NYSE).

Johnson & Johnson is the largest health care corporation in the world. The company was founded in 1886 and currently has a market cap of more than $280 billion.

There are two telling numbers to remember when analyzing Johnson & Johnson stock: 31 and 53. As in 31 consecutive years of adjusted earnings-per-share increases and 53 consecutive years of dividend increases.

In addition to these impressive metrics, Johnson & Johnson has one of the lowest stock price standard deviations of any company. With its low volatility and long history of predictable growth, Johnson & Johnson has more in common with a utility (except it has better growth prospects) than with most other health care corporations.

But we think there is a better way.

Create your own Canadian Dividend Grower Stock Portfolio composed of smaller, high growth dividend payers that remain “off the radar” of the broader market.

Select dividend growers that trade at great valuations.

Exco Technologies Limited (XTC:TSX) – a dividend growth small-cap from our coverage.

In each of the past 4 years since our recommendation, Exco has increased its dividend.

Industry: Manufacturing – Extrusion & Automotive

Recommended: June 2011

Recommendation Price: $3.90

Current Price: $12.66

Market Cap: $537,113,160

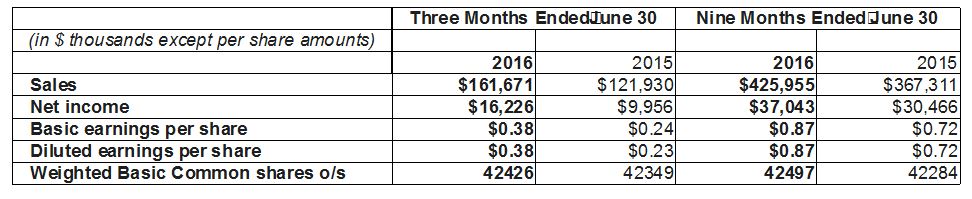

Shares Outstanding: 42,426,000

Fully Diluted: 42,693,000

With roots that date back to 1952, Exco is a global supplier of innovative technologies servicing the die-cast, extrusion and automotive industries. Through 18 strategic locations in 10 countries, the company employs 6,515 people and service a diverse and broad customer base.

Last Week the Company Posted Record Quarterly Revenues & Earnings

• Record Sales and Earnings in the quarter.

• EPS of $0.30 up 25% adjusted for non-recurring gain.

• AFX acquisition performing strongly.

• Financial position and liquidity remain solid.

Consolidated sales for the third fiscal quarter ended June 30, 2016 were a record $161.7 million – an increase of $39.7 million or 33% over last year. The acquisition of AFX Industries LLC (AFX) closed April 4, 2016 and performed strongly, contributing $31.0 million to sales.

Net income was $16.2 million or $0.38 per share including $3.4 million from the settlement of a commercial arbitration. Excluding the gain, EPS was $0.30, up 28% from the third quarter of fiscal 2015.

We see the recent drop in Exco’s shares as an opportunity. AFX has begun contributing to earnings in the current quarter, and we expect the acquisition produce meaningful growth for Exco as a whole once again. AFX had revenue of approximately C$115 million (equivalent) in 2015. Exco expects the acquisition will be highly accretive to its earnings per share and initial proof of this was seen in Q2. We expect the 12-month earnings run-rate (pro-forma) for the company with AFX included is in the range of $1.30 – the stock is now trading at and attractive 9.7 times that estimate. EV/EBITDA is approximately 6.3 based on pro-forma EBITDA – this is also relatively attractive.

While the company’s industry is cyclical, we believe the current environment appears positive for the next 12 months. As such, we maintain our BUY recommendation and the company’s place in our Focus BUY Portfolio.

Another long-time favourite dividend grower is Enghouse Systems Ltd. (ESL:TSX), a Canadian software-based company we recommended 6-years ago in the $8.00 range, which has also increased its dividend every year since. While it is no longer cheap, the company has the potential to continue to outperform long-term.

These are just two companies to begin building you Canadian Dividend Grower Stock