Market Opinion

Richard Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe.

Russell Comment: If you really want to know what’s going on in the world, you must read the Financial Times. The article below appeared in the Financial Time on December 3. I didn’t see this news or this information in any other newspaper, which is why I read the Financial Times every day.

China is key to next rally in gold prices

By David Hale

The recent gold price rally is the first stage of a multi-year bull market that will drive the gold price to at least $2,000 an ounce by 2015. A mixture of economic factors and innovations in how institutions can purchase the metal have moved prices. But the biggest driver of gold prices is yet to come.

First, a recap of the factors that have taken gold prices to current levels.

The economic causes center on monetary policy and the risk of inflation. Some industrial countries are striving to devalue their currencies and will use monetary policy to support the goal. Japan recently spent $24bn on unsterilized intervention trying to weaken the yen. The policy succeeded, albeit briefly. In 2003-04, Japan spent more than $350bn on intervention and could easily do so again. This policy would increase dollar liquidity while nurturing more monetary growth in Japan itself.

The Federal Reserve has been dropping ever-bigger hints that it will embark on further quantitative easing. A significant policy move will trigger immediate selling of the dollar, and could set the stage for competitive devaluations elsewhere.

The gold price has also benefited from the introduction of exchange traded funds five years ago. These funds allow investors to purchase gold bullion as effortlessly as a share of stock. In the second quarter of 2010, investors bought more than 274 tonnes of gold through ETFs. Their holdings now exceed 2,000 tonnes, and are the sixth largest in the world after the official stocks at the International Monetary Fund and the central banks of the US, Germany, France and Italy. At current growth rates, these ETFs could rank third by the end of 2012.

After a long period of selling gold, central banks are re-emerging as buyers. China revealed last year that it had purchased 450 tonnes. India bought 200 tonnes last October. Russia has bought 71 tonnes of gold this year while there have been small purchases by Mauritius, Thailand, Bangladesh and Sri Lanka. South Korea announced last week that it might use some of its $290bn of foreign exchange reserves to buy gold. During the previous two decades, central banks sold nearly 4,500 tonnes.

But potentially the most important new factor in the gold market is China. China now has more than $2,400bn of foreign exchange reserves, but only 1.7 per cent of this is invested in gold. The IMF is projecting that China will run a current account surplus of $2,600bn during the next five years. If it does, its forex reserves could rise to the $5,000bn-$6,000bn range. Even if it keeps the gold share of its reserves constant, it will have to buy a further 1,000-1,500 tonnes. Yet the odds are high that China will want to expand the gold share of its reserves in order to lessen its vulnerability to dollar devaluations and strengthen the renminbi’s status as a global currency.

As with the US 100 years ago, China will probably regard large gold holdings as a way to project financial power. In 1913, before the dollar had emerged as a global currency, the US had 2,293 tonnes of gold compared with 248 tonnes for Britain, 439 tonnes for Germany, 1,030 tonnes for France and 1,233 tonnes for Russia. The Americans’ large gold reserves made the dollar a natural replacement for sterling when the first world war crippled Britain’s financial position. The US is now running a fiscal policy that has parallels with Britain during wartime, which could undermine the dollar’s global role at some point.

Some Chinese officials have publicly called for the central bank to purchase 10,000 tonnes of gold. The central bank has declined to comment on these proposals, but they will become increasingly attractive if the US pursues a policy of dollar devaluation while the renminbi emerges as a global currency.

It is also possible that the massive expansion of China’s foreign exchange reserves could spawn faster monetary growth and increase China’s inflation rate. If it does, there could be a sharp rise in Chinese private demand for gold.

China has deregulated its gold market since 2008 and private demand is increasing rapidly. It totalled 143 tonnes during the past 12 months compared with 73 tonnes in 2009 and 17 tonnes in 2008. It could easily rise to several hundred tonnes if investors perceive that China’s monetary growth is going to produce higher inflation.

The US government has been critical of China’s policy of pegging the renminbi to the dollar, but it would abandon this criticism if China pursued a policy of unsterilized currency intervention and allowed inflation to accelerate. The renminbi would then appreciate in real terms, and make Chinese goods less competitive.

There is no way to predict the timing of China’s future gold purchases, but there can be little doubt they will create a demand for gold that will dwarf all other factors during the next quarter-century and guarantee large price gains irrespective of what happens to Federal Reserve policy.

Russell Comment — I continually talk to educated people who refuse or seem incapable of understanding the difference between intrinsic (tangible) wealth and wealth created by government command (fiat currency). Tangible wealth must be a product of search, risk, capital expenditure, or artistic creativity. Wealth by government’s command (fiat) is a product of government edict and government command.

Without thinking or analyzing its short-comings, most people now passively accept fiat money for trade and as a store of value. Fiat money (although I think it’s immoral) might work if politicians were disciplined, far-thinking and patriotic. Alas, they are not. Greed and the lust for power seems to be built into the DNA of mankind and particularly into the souls of politicians.

Scoreboard percentages for 2010 so far —

Dow……….+9.15%

S&P……….+9.83%

Gold……….+28.3%

Silver……….+73.8%

Palladium……….88%

Coffee……….+50.4%

Cotton……….+88.3

There’s a lot of rumor, buzz, innuendo, chitchat and scuttlebutt about the precious metals markets these days. Most of the chitchat is about J.P. Morgan and silver. Rumor has it that J.P. Morgan has amassed a whopping short position in silver.

The scuttlebutt, according to SFGate.com, is that “J.P. Morgan holds a giant short position in silver. Furthermore, some observers are accusing the bank of acting as an agent for the Federal Reserve in the market…I.e., a lower silver price helps maintain the relative appeal of the US dollar…

“By selling massive amounts of paper silver in the futures market,” SFGate continues, “J.P. Morgan has been able to suppress the price of the precious metal. It is believed that these short positions are naked (i.e. they are not backed by any physical silver).”

If the silver price were falling, Morgan’s (alleged) short position would be lauded as a stroke of genius. But since the silver price is soaring, Morgan’s (alleged) short position looks much less laudable.

“In recent days,” SFGate notes, “rumors have been swirling on the Internet that J.P. Morgan’s massive short position is about to blow up in its face in the form of an almighty short squeeze and potential COMEX default, as large traders demand physical delivery of silver that COMEX does not have in its vaults.”

Based on some of the latest conjecture, Morgan’s short position totals a whopping 3.3 billion ounces. If, therefore, the buzz about J.P. Morgan and silver is even half true, the prestigious investment bank could be cruisin’ for bruisin’.

For perspective, 3.3 billion ounces is roughly equal to:

1) One third of all the world’s known silver deposits;

2) Two times the world’s approximate stockpiles of silver bullion;

3) Four times the annual mined supply of silver;

4) 30 times the inventory of silver at the COMEX.

To repeat, short positions – even titanic ones – are no big deal, as long as the price of the underlying asset is falling. But if, inconveniently, it is rising, the spaghetti can hit the fan in spectacular and gruesome fashion.

The silver price is rising…a lot. From less than $10 an ounce two years ago, the silver price has more than tripled. Therefore, if J.P. Morgan does, in fact, hold a 3.3 billion ounce short position, every one-dollar increase in the silver price would produce a loss of $3.3 billion…at least on paper.

Unfortunately, Morgan cannot simply unwind this trade with a couple of mouse-clicks in an E*trade account. The position is too large, both in relation to the world’s physical supplies of silver and in relation to the paper “supplies.” (Morgan holds almost half of all short positions on the COMEX, which is essentially a “paper market” – participants rarely take delivery of physical silver).

To make matters even more dicey for Morgan, the supplies of physical silver are disappearing rapidly from the marketplace. Increasingly, the kinds of folks who invest in precious metals are also the kinds of folks who distrust intermediaries. These precious metals investors want to know that the shiny stuff is in their personal possession.

Meanwhile, the ETFs that hold precious metals are soaking up massive quantities of physical metal. Over the last 12 months, the silver ETFs around the globe have increased their holdings by nearly 100 million ounces – or almost as much silver as the entire inventory of the COMEX. The trend in gold is identical.

Therefore, as a result of soaring demand from both individual investors and ETFs, the physical stockpiles of gold and silver are atrophying in relation to the paper claims on both metals. This is not a pleasant picture for a short seller of silver.

Furthermore, the kinds of folks who tend to buy gold and silver are also the kinds of folks who have contempt for Wall Street…and for Wall Street banks like J.P. Morgan. So it should come as no surprise that a grassroots campaign has formed – the sole purpose of which is to punish J.P. Morgan for its attempted manipulation of the silver market.

“A viral campaign (Crash JP Morgue Video [below]) to buy a physical silver and ‘crash’ the bank is now spreading like wildfire on the Internet,” SFGate reports. “Just Google, ‘Crash JP Morgan Buy Silver’ [to learn more about it]… Those who wish to participate in squeezing the living daylights out of J.P. Morgan, may want to consider buying physical silver, silver futures and SLV.”

Maybe this story about J.P Morgan’s short position in silver is mere innuendo. Maybe not. But two facts are irrefutable:

1) J.P. Morgan is already under investigation by the CFTC for manipulating the silver market. “The investigation into the bank can be traced back to November 2009,” SFGate reports, “when London metals trader and whistleblower Andrew Maguire contacted the CFTC to report market manipulation prior to it actually occurring.”

2) Precious metals investors are increasingly keen to get their hands on physical gold and silver, rather than mere paper facsimiles.

Eric Fry

for The Daily Reckoning

Special Report: BETTER THAN GOLD! One investment should rocket even faster than gold over the next 12-24 months… yielding at least 3-to-1 gains on every dollar invested… GUARANTEED. Access your report….

Eric Fry

Eric J. Fry, Agora Financial’s Editorial Director, has been a specialist in international equities for nearly two decades. He was a professional portfolio manager for more than 10 years, specializing in international investment strategies and short-selling. Following his successes in professional money management, Mr. Fry joined the Wall Street-based publishing operations of James Grant, editor of the prestigious Grant’s Interest Rate Observer. Working alongside Grant, Mr. Fry produced Grant’s International and Apogee Research — institutional research products dedicated to international investment opportunities and short selling.

Identifying Top Seeds in the Potash Boom

As growing middle classes in developing nations feed the need for fertilizer, how to increase production has become the real issue in agriculture. Major potash producers are lining up to fill that need. The Energy Report spoke with Adrian Day Asset Management Chairman and CEO Adrian Day and Wellington West Capital Markets Analyst Rob Winslow to get their take on the potash sector, and which companies have the sustainable competitive edge.

The Energy Report: Adrian, in our last interview with you, while discussing the sustained commodity boom that you foresee, you said you were talking about the whole shebang—from precious and base metals to uranium, oil and gas to geothermal. You also included agriculture, noting that you expect agricultural assets to be among the best-performing assets over the next decade. Would you expand on that thought for us?

Adrian Day: Absolutely. As you may recall, we also talked about how China has been driving the resource market and will continue to drive it for the next decade. Even if China’s economic growth slows from 9.5%–5%, the demand for resources will still be very dramatic—much higher than now. As China becomes more industrialized, increasingly more people in its massive population will move up into the middle classes.

Middle class people want houses with electricity, running water and indoor plumbing. They want to have cars, as well as bicycles, which takes copper, aluminum, platinum, rubber, oil, etc. And as more Chinese go from eating the chickens and goats they raise in rural China to an urban environment, they lose their taste for goat meat and want beef instead. Cows consume more wheat than do goats. That’s just an example. The point is, the basic factors driving all the resources are also driving agriculture.

TER: As Wellington West Capital Markets’ agricultural expert, Rob, what underpins this rush toward potash companies, including the failed BHP Billiton Ltd. (NYSE:BHP; OTCPK:BHPLF) bid for PotashCorp (NYSE:POT; TSX:POT), the upcoming transaction between K+S Aktiengesellschaft (Fkft:SDF) and Potash One Inc. (TSX:KCL)?

Robert Winslow: Whether you’re looking at fertilizers or farm equipment, really what underpins all the agricultural (ag) cycle is the grain complex. If you were to pull up a chart of the corn, wheat and soybean prices, for example, you’d see that grain prices bottomed out in early June, down to around the cost of production in the U.S. Corn Belt. They started rallying from there, spurred a little by dollar weakness but also by the supply/demand situation globally. We’re in the neighborhood of 50%–55% above those June lows.

TER: Has the hike been more a function of growing demand or supply shortages?

RW: We had some supply shocks, particularly on the wheat side. In western Canada, it was very wet; in Russia, it was very hot and dry. As a result, two of the world’s three-largest wheat exporters saw their production cut by about 20%. That showed us how tight the stocks-to-use ratio became globally, which is the metric we use—it measures supply/demand for any given commodity.

TER: Could you elaborate on what that stocks-to-use measurement tells us?

RW: It tells us supply/demand levels are down to those last seen in 2007 and early 2008 when the grain complex rallied, as well. The bottom line is we get to a situation where we have insufficient inventory to protect us from supply shocks. That will drive up grain prices. As grain prices go, farm income goes. As farm income goes, so go expenditures on seed, fertilizer, chemicals, tractors, short-line equipment, you name it. The entire complex rides on the back of those grain prices.

TER: That would bode well for a company you told us about the last time we talked, Adrian. You described it as one of your favorites in the general resource area.

AD: Yes, Sprott Resource Corp. (TSX:SCP). If you buy Sprott, which is quite a liquid company, you get it at a discount to NAV. Net asset is about $5.20. The stock’s been trading at about $4.65. You also get great management—Kevin Bambrough and company—and a great balance sheet. As you know, Sprott has direct and indirect investments in different resource areas—buying whole companies, sponsoring companies or growing them. When the companies reach a certain level, ideally it’ll spin off a certain amount of the shareholding into a public company.

TER: You said it’s currently in gold, oil and gas, agriculture and fertilizer. Tell us about the last two on that list.

AD: The agriculture play is very interesting, a joint venture (JV) with First Nations—One Earth Farms Corp. First Nations owns more than a million acres of farmland. It’ll be a big business, one of the largest commercial farms in North America—really quite staggering. It’s still a private company, but it’s selling some shares in a secondary offering, raising $40M–$80M. If it brings in the maximum, it will take Sprott’s stake down to 24%. In a year or two, it’ll IPO. That’s what it’s trying to do—take a direct investment, build up the company and IPO it.

TER: News has been coming in pretty fast and furious on the potash front; and, Rob, you recently raised your targets on several potash juniors. Without discounting the demand factor, what can you tell us about the rationale behind that decision?

RW: The impetus for that was the bid by K+S for Potash One. On the back of that, we also raised the targets on Allana Potash (TSX.V:AAA), Intercontinental Potash Corp. (TSX.V:ICP) and Western Potash Corp. (TSX.V:WPX), as there’s a scarcity factor that needed to be embedded in the valuations of those companies. We’re seeing consolidation in the space, with the big players coming and buying up the juniors. When that happens, obviously, the value of those left standing—presuming they’re still quality assets—tends to go up.

TER: How did your targets on these three companies change?

RW: We raised Allana’s target $0.15 to $1.15 (and have since raised it again to $1.20) and we rate it as a strong buy. Intercontinental is $1.50/share and Western Potash is $1.05. Among the three, I have a more favorable view on Allana and Intercontinental than on Western Potash because the former two are advantaged juniors.

TER: What do you mean by “advantaged” juniors?

RW: They have some edge, a sustainable competitive advantage that makes them stand out from the crowd. For example, Allana’s potash concessions are in Ethiopia’s Danakil Depression.

TER: What makes that special?

RW: The potash deposit there may be as shallow as 150 meters or so, which suggests the possibility of an open-pit operation. That would cost less than sinking a shaft in Saskatchewan, where the company would likely have to go down to a depth of 1 km. That’s more than $1 billion just to get the shaft down. Parts of the Danakil Depression potash deposit appear to be 600–700 meters, so solution mining would be possible there also.

TER: Some of our readers may know, Saskatchewan supplies one-third of the world’s potash demand. But, apparently, Ethiopia has one of the world’s largest potash deposits—up to 150 million tons (Mt.) concentrated in the Dallol area.

RW: That area, in the Danakil Depression, has enormous potash potential. Water has been running down from the surrounding mountains for millennia, carrying minerals to this low-lying basin. Over time with heat and evaporation, it has produced this giant dish of salt. When you go far enough down into the layers, you reach salt containing a tremendous amount of potassium—that’s the potash. I’ve never seen anything quite like it; it’s remarkably hot and salty.

The Danakil Depression is among the hottest places on earth. I was there not long ago, and it was 114°F in the shade. The idea with solution mining is to inject a heated solution (or water) down into the salt bed, dissolve the salt, bring it up to surface, and then use wind or solar to evaporate it. At the surface, you can heat up your water quickly with solar panels. Considering all of that, operating costs are potentially materially lower than in a solution mine—or any other kind of mine—in Saskatchewan.

TER: That would clearly be a competitive advantage. Compared to conventional mining, solution mining means not only lower capex requirements but also operation scalability and a quicker timeline to production—not to mention less technical risk and environmental impact.

RW: There’s even more to the Allana story. It’s quite a bit closer to one of the largest importing nations in the world. Depending on the year, India ranks as the second- or third-largest potash importer in the world. If Allana gets this mine built and the proper infrastructure in Ethiopia to get it over to the coast, transport alone could be $20 or even up to $40 cheaper per ton. So, once the infrastructure is in place, the cost of those logistics on a run-rate basis would be significantly lower than they would be in western Canada. That’s another reason we like Allana. It’s also lower on a price-to-NAV valuation on our comp table.

TER: As a Canadian-domiciled company, one might expect to see French and English banners on Allana’s website but it has English and Chinese banners.

RW: Of course, China is interested in potash all over the world, but a Chinese investor has put in a modest amount of capital and bought some equity in Allana, about $2 million. The company’s also negotiating with this investor to put up something like 35% of the capex to help finance the project. In turn, Allana has committed to give this partner discount-to-market prices on potash until it gets its capital back. The terms have yet to be finalized, but it’s an interesting way to finance the project. The day the Chinese actually put up $300M will be the day we’re excited. Right now, it’s not concrete; it’s just in negotiations. Even so, a lot of things separate Allana from some of the others.

TER: It sounds as if there’s minimal jurisdiction risk in Ethiopia.

RW: Ethiopia is not Canada. Having said that, it’s interesting; it’s almost paradoxical. Africa welcomes the Chinese with open arms. They’re the largest investors in Africa. They promise infrastructure. They’ll create jobs. They want to stimulate the economy. There’s a lot of collaboration between the African nations and China. I met with some government officials when I was there, and the government’s conviction is pretty strong. It wants to produce potash—the goal is to produce 2 Mt. annually by 2015. It’s racing toward potash production and is more focused than anybody else out there. The government’s going to spend money on infrastructure. It’s talking about an $8 billion rail system that, obviously, would facilitate getting potash to the coast for export. China probably will be constructing most of that railway.

TER: Wherein lies the paradox?

RW: You don’t see the Chinese doing a heck of a lot in Canada’s potash space, and I think that’s primarily because they don’t want to get egg on their face. Think of what we saw with BHP in its bid for PotashCorp. I suspect the Chinese view Canadians as slightly protectionist when it comes to some of these strategic resources.

TER: Right. You weren’t too hot on the BHP takeover attempt, anyway. In August, The Globe and Mail quoted you as saying that a successful takeover by BHP would “complicate the situation for Canadian junior potash companies in a number of ways, making access to capital somewhat more challenging for them.” Further to your comment about that protectionist sentiment, PotashCorp, after all, is the world’s largest fertilizer company by capacity, producing all three primary crop nutrients—phosphate, nitrogen and potash. As the world’s leading potash producer, it accounts for about 20% of global capacity—a national treasure.

RW: Yes, and frankly I think China would find it more difficult to get something done in Canada than it would in Ethiopia. As I said, Ethiopia’s government is looking for investment with open arms. That’s the paradox.

TER: China’s investment will do a lot for Ethiopia’s GDP, too—2 Mt. at $500/ton. What’s the story with Intercontinental?

RW: It’s early days yet, but it’s looking at producing a specialty fertilizer called potassium sulphate (SOP) by extracting potassium (K) from polyhalite. It has to mine the stuff—polyhalite’s an unusual mineral, but it has a lot of K in it—and bring it up to surface. But if it all pans out, Intercontinental could be among the world’s lowest-cost SOP producers.

Most SOP producers use the Mannheim process, mixing potassium chloride (KCl), or regular potash, with sulfuric acid in a big furnace. Some fancy chemistry goes on when it heats up, and SOP comes out the other end along with some byproducts. The SOP cost will fluctuate with the price of potash, but it can be costly.

In contrast, the conversion process that Intercontinental Potash proposes would use the polyhalite the company mines as its input instead of KCl. Suppose the polyhalite costs $60–$70/ton to mine and conversion takes it to $180–$200/ton to produce SOP. If you’re using the Mannheim process to produce SOP, you’re buying KCl at approximately $400/ton in the marketplace, which already puts you at a disadvantage compared to a competitor who can use a much-cheaper raw material input. That’s a really interesting project, and one of the lowest-cost producers in the world delivering a high-margin potash product makes for a really compelling story.

TER: Is potash garnering about $500/ton now?

RW: It depends on where it’s being sold. In Brazil, I believe it’s a little bit over $500. In parts of the Midwest, in the Corn Belt, it’s approaching $500. In Vancouver, I believe it’s $400. So it depends. Wherever you are in the world, there’s a slightly different price because you have to factor in the transportation cost.

TER: Getting back to your advantaged companies, why isn’t Western Potash in that category?

RW: We raised our target on Western Potash, too, but we’re less optimistic on its prospects given that it’s maybe the fourth or fifth junior in the Saskatchewan Basin. Over the past couple of years, BHP has acquired Anglo Potash Limited and Athabasca Potash Inc.; and now, Potash One is bidding for K+S. Already these three juniors are arguably further advanced than Western Potash. Plus, you’ve got the brownfields, the incumbents and the big players—PotashCorp, The Mosaic Company (NYSE:MOS) and Agrium Inc. (NYSE:AGU). They could well expand their capacity for potash in the basin in western Canada.

So, Western Potash is late to the game by comparison and the cost of capital is significantly higher than it is for the brownfields. This isn’t to say the stock price can’t go higher, because clearly it went through our target; but we’re somewhat tempered on our optimism. A lot of things have to go right for that Western Potash mine to be built and we’re just not persuaded it’s likely to happen.

TER: Back to you, Adrian. You’ve brought us up to speed on Sprott. What are some of the ag companies you like?

AD: We favor companies that actually produce somewhat more than do the explorers. So, some of those we like include farmers and agribusiness companies like Cresud (NASDAQ:CRESY) in Argentina, which raises wheat, corn, soybeans, beef and dairy cattle. Cresud exports a lot to China, which says an awful lot about China’s need for agricultural commodities. It has evolved from a country that met all of its own needs and actually exported agricultural products. Now, China has to import wheat from halfway across the world.

In addition to agribusiness companies that produce, we like Bunge Ltd. (NYSE:BG; NASDAQ:BG), which had its origins in Brazil and still has most of its assets there but is headquartered in New York now. Bunge buys, sells, stores, processes and transports crops to make staple foods, food ingredients and animal feed. Its corporate brochure contains an eye-opening statistic from the United Nations—that global food production will need to increase 70% by 2050 to feed a larger and more prosperous world population.

How to increase production has become the real issue in agriculture. Of course, one way is with fertilizer. We have to use fertilizer if we’re going to feed people; there’s no way around it. This is a well-known story, and the fertilizer companies are going to do remarkably well over the longer term. The fertilizer stocks got a little expensive in the wake of BHP’s bid for PotashCorp. Now that it’s been withdrawn, I would wait for a pullback.

Right now, my favorite potash is a great company—Mosaic. Germany-based K+S is another good company. Various fertilizers already comprise about 85% of revenues for K+S, which looks to expand its portfolio with the Potash One transaction soon. I also like Syngenta AG (NYSE:SYT), which is also based in Germany. If we’re going to feed people, we have to find a way to increase our core production not only with fertilizer but also with genetic engineering of seeds, etc. I know it’s controversial, but that’s the only way we’re going to do it.

TER: Any other companies?

AD: There are also explorers. For instance, Lara Exploration Ltd. (TSX.V:LRA) isn’t a phosphate explorer but it has some phosphate exploration in its portfolio. So, I like diversified companies that give me exposure to different areas.

TER: Adrian, you’re a commodities bull no matter how you cut it—in this case, with agribusinesses. And you’ve given some strong bullish signals on the ag sector too, Rob.

RW: We’re obviously bullish on grains and fertilizers. We’re bullish on grains because we think the supply/demand situation could remain tight for some time. USD weakness also tends to drive these commodities higher because they’re denominated in U.S. dollars. For example, it takes more dollars to buy a bushel of corn as the USD devalues. In our view, a number of factors support robust grain prices and, therefore, a strong ag sector for investors.

TER: Thank you very much, gentlemen.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

Adrian Day is a British-born writer and money manager who graduated with honors from the London School of Economics, Adrian Day has made a name for himself searching out unusual investment opportunities around the world. As president and CEO of Adrian Day Asset Management, he generously shares his thoughts, opinions, insights and analyses via Barron’s, Forbes, Bloomberg Markets, Kitco, Casey, The Stock Advisors, Dick Davis Digest, MSN Money, Financial Times, The Daily Reckoning, The Herald Tribune, The New York Times and, of course, The Energy Report—among others. A frequent speaker at international seminars and a regular guest on CNBC and The Wall Street Journal Radio Network, he has been interviewed by Money, Straits Times, Good Morning America and others. He also writes the quarterly Portfolio Review newsletter for clients, serves as editor of Adrian Day’s Global Analyst and has authored three books on global investing: International Investment Opportunities: How and Where to Invest Overseas Successfully and Investing Without Borders and the just-published Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks, which is now available in hardcover and e-book formats.

As an analyst with Wellington West Capital Markets Inc. in Toronto, Robert Winslow, CFA, covers 16 companies wearing his “Agriculture and Special Situations” hat. Before joining Wellington West, Rob served as an equity research analyst with Orion Securities Inc. (Toronto), strategy consultant with Bain & Co. (Toronto and Brussels), and senior engineer with Caterpillar Inc. (Dallas). Rob earned his master’s in science degree in engineering at Texas A&M, and his MBA from Cornell.

Streetwise – The Energy Report is Copyright © 2010 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

The Energy Report does not render general or specific investment advice and does not endorse or recommend the business, products, services or securities of any industry or company mentioned in this report.

From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Energy Report. These logos are trademarks and are the property of the individual companies.

Streetwise Reports LLC

P.O. Box 1099

Kenwood, CA 95452

Tel.: (707) 282-5593

Fax: (707) 282-5592

Email: jmallin@streetwisereports.com

I have always loved Canada. From the time I read the biographies of Bobby Orr and Bobby Hull, as a kid, to the times I travelled to Toronto, Montreal, Quebec City, Prince Edward Island, and the Gaspe Peninsula as a teenager, to more recent visits to Vancouver for the World Outlook Conference …

…. not to mention my love of the national sport, Hockey, or my time living with a bunch of “crazy Canucks” at Delta Kappa Epsilon, the “hockey frat” at Colgate University, I have always had a place in my heart for Canada, and for Canadians. From the Maple Leaf flag, to the Montreal Canadian’s home hockey jersey, I still feel warm when I hear the Canadian National Anthem …

…”Oh Canada, glorious and free, we stand on guard, we stand on guard for thee”.

Indeed,

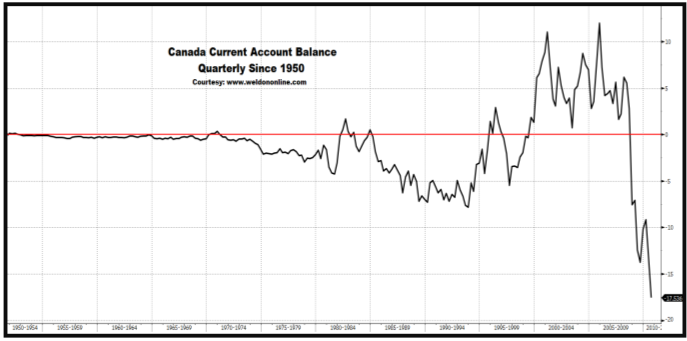

Indeed, as noted in the chart below, Canada‟s Current Account Balance plunged to its DEEPEST DEFICIT EVER during the 3Q.

**Ed Note: this article goes on for 14 pages with some extraordinary charts to give the visual picture. One of the closing comments is “… Gold stands on guard, as the best “protector” of wealth in Canada”. See how to read more at the bottom below.

More from Greg: Finally, in keeping with today’s Canadian theme, we would like to formally “introduce” the latest addition to Weldon Financial, Katelyn Ellis, math-physics whiz, and graduate of Canada’s McGill University. Ms. Ellis will serve as my new “trading assistant”, hired to help handle the inflow of “demand” linked to our Managed Futures business, and the re-opening of our Macro- Discretionary, Diversified Global “trading” Program, along with the introduction of our new Long-Short Commodity Only “portfolio” Program.

Welcome Katelyn, who just passed her Series 3 Exam with flying colors …… as in the red and white of the Canadian Maple Leaf Flag.

To read more of this penetrating 14 page article & Charts Titled MACRO-CANADA: We Stand On Guard For Thee …

…..Weldon’s Money Monitor offers a FREE 30 Day Trial Subscription. For subscription information contact Eileen @Weldononline.com or Visit www.Weldononline.com for a FREE Trial.

A FREE 30 Day Trial Subscription is defined as a single Trial that is limited to a one-time Signup. Signing up for multiple trials under different names, Fraudulent contact information is illegal. Weldon’s Money Monitor takes this seriously..

Martin Armstrong is currently in prison. Indicted in 1999 on charges of defrauding Japanese investors. He was in jail for seven years for contempt of court before pleading guilty in 2007 to the fraud charge for which he received an additional five year prison term. Armstrong claims his legal problems started when he failed to play ball with “The Club”. His imprisonment is one of the longest under a contempt of court order without a trial. Coincidentally, prior to his guilty plea, his final appeal for release (relating to indefinate imprisonment for contempt of court) was denied by (recently promoted) U.S. Supreme Court Justice Sonia Sotomayor.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair