Daily Updates

Continued Boom or Epic Bust

In a recent article, How China Ate America’s Lunch, Clif Carothers described what China has accomplished in the last thirty years:

In thirty short years, China was able to accelerate her GDP from $216 billion to $6 trillion. She amassed reserve capital of $3 trillion. She reversed America’s fortunes from the greatest creditor nation to the greatest debtor nation. She gutted America’s factories while creating the world’s largest manufacturing base in her own country. A measure of output that highly correlates to GDP is energy consumption. In June of this year, 2011, China surpassed the United States as the largest consumer of energy on the planet. While the U.S. consumes 19% of the world’s energy, China consumes 20.3%.

While China was growing their economy by a phenomenal 2,800%, the U.S. GDP grew from $2.3 trillion to $15 trillion – a mere 650% increase, of which 420% was due to inflation. There is no question that China’s progress has been remarkable. The question is whether that growth is sustainable and built upon a solid foundation.

The competition among non-Chinese junior mining companies to successfully mine rare earth elements (REEs) began as a footrace and evolved into a full-on stampede. That race is now unraveling, thanks to slower global economic growth and the sheer number of exploration companies involved in rare earth exploration. We have seen estimates of over 300 companies involved in this global search, and when you factor in the relatively tiny size of the rare earth market (approximately 130,000 tons produced in 2010, according to the U.S. Geological Survey) we still stand by what we’ve said all along—there is room here for a few major players and not much else. We believe the rare earth industry is in the beginning stages of a phase we call “The Great Reset.” We base this theory on four ideas:

- Everything reverts to the mean. This includes rare earth oxide (REO) prices. While we believe we will see a permanently higher price for select REOs, this is not the case for the entire suite of oxides, and prices cannot continue rising indefinitely. The laws of supply and demand have proven this.

- Demand projections for REOs are being re-evaluated downward due to anemic global economic growth prospects. With a tremendous debt overhang in the United States and Europe and evidence of growth slowing in China (the three biggest economies in the world), lower aggregate demand for finished goods that use REOs is a given. We have seen forecasts for REO demand in 2015 that are higher than they are today, and don’t disagree, but the downward revision is indicative of lower demand for most REOs.

- Companies such as Toyota and General Motors are actively researching substitutes for REOs in their products. This type of research has been in progress for some time and we think that these companies would not be spending the R&D dollars if they didn’t want to avoid high REO prices.

- Demand projections for “green” or “clean tech” applications such as hybrid electric vehicles, wind turbines and solar cells are not factoring in whether or not manufacturers of these goods can ensure a steady supply of raw materials (specifically REOs) to meet their production forecasts. The rare earth industry is a customer-driven business in that the customer needs REOs of a highly specific type and purity. If a wind turbine manufacturer can’t procure a specific purity of neodymium oxide, for example, the wind turbine may get built without neodymium, implying demand destruction. We have seen estimates of the use of up to one ton of neodymium needed to produce one megawatt of generating capacity from a wind turbine. China alone has plans to install 100 gigawatts of generating capacity from wind (up from 12 gigawatts in 2009). When you factor in European and American projections for wind power (not to mention other parts of the world), this begs the question of whether or not there is enough neodymium to go around and if there currently is not, will there be enough to satisfy these growth targets in wind generating capacity? We are well aware of the benefits of neodymium-iron-boron magnets in miniaturization and efficiency, but think that if a product can be manufactured economically without REOs, then the manufacturer will choose that path or abstain from building the product at all.

To be clear—we have not “thrown in the towel” on REOs and the important role they play in certain sectors of the economy. What we are saying is that the role will be different from what many in the sector currently suggest. Like many other facets of life, the rare earth sector is Darwinian in nature and will evolve to equilibrate supply and demand. The gratification that comes along with healthy and growing demand for a product (in this case REOs) will be delayed, to the chagrin of investors and rare earth mining company CEOs alike. This “reset” shapes how we think about the rare earth space now and in the future and in deciding how and where to invest. Below is a price chart of the Bloomberg Rare Earth Mineral Resources Index and its one-year performance.

The One Sector Where Supply and Demand Don’t Matter

There is one area of the economy, however, which we think is immune to the vagaries of supply and demand of REOs: the military. While the potential for substitution exists with consumer products, we believe there is no such “wiggle room” when analyzing a country’s defense capabilities. The neodymium-iron-boron magnets we mentioned above are critical in actuators of precision-guided bombs and are designed specifically around these magnets. Actuators are responsible for control of the bomb, and this is just one of several products (lasers and radar being two significant other products) that must use rare earths to function optimally. Without the magnets in the bombs, performance is reduced—implying an inferior product—something nobody should be willing to accept. The U.S. Military is responsible for a small overall percentage of REO demand in the United States, but it is significant nonetheless.

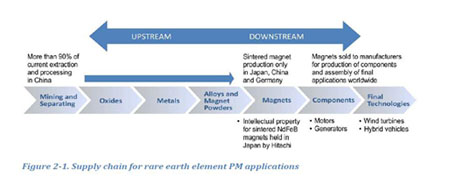

The Rare Earth Supply Chain: The Key to It All

So at this point, we believe two things: first, demand for most REOs will decrease in the near term, and second, that it will be exceedingly difficult for the majority of the junior mining companies involved in rare earth exploration to achieve commercial production of REOs. Despite this, the singular crucial issue that put the rare earth story on the front page of every newspaper around the world in the first place still haunts us—Western dependence on a critical resource from a strategic adversary. While a seemingly endless amount has been written about China’s control of the supply of REEs, what we think is most important (and most often missed by the pundits) is the fact that China also effectively owns the entire mine-to-magnet supply chain. This is the crucial vulnerability. The mining of rare earths is the easy part. It is the resulting steps where intellectual property is created that really matter. In 2010, the United States Government Accountability Office (GAO) was commissioned to deliver a report on the use of rare earth elements in the Department of Defense supply chain. Regarding military capabilities, the report states (Ed. Note: bold text is ours),

“For example, the M1A2 Abrams tank has a reference and navigation system that uses samarium cobalt (SmCo) permanent magnets. The samarium metal used in these magnets comes from China.”

Whether we’re discussing heavy rare earth elements (HREEs) or light rare earth elements (LREEs), a particular concern is the fact that the West is realistically years away from having a supply chain built that can diminish foreign dependence on REOs. Viewed that way, reduced demand for certain REOs could be a blessing in disguise in that it can give Western policymakers more time to formulate a viable strategy, though based on recent behavior in Washington DC (i.e., the debt ceiling debate), we’re not holding our breath. The chart below shows the supply chain for rare earth permanent magnets used in wind turbines and hybrid vehicle motors, among other products. China is responsible for the entire upstream portion of this chain and has designs through mercantilist export policies on owning the entirety of the downstream portion of the chain as well.

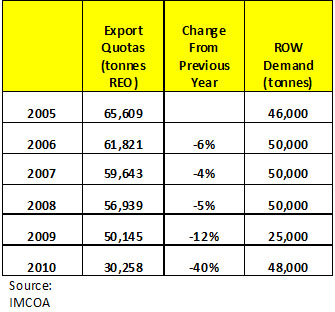

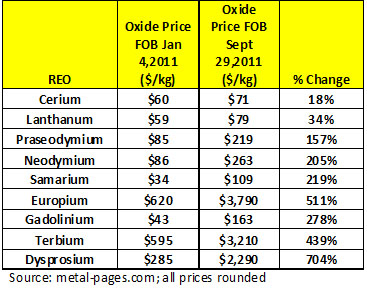

To get a sense of how Chinese export quotas of REOs have decreased in recent years and the resulting increases in prices of REOs, see the charts below:

There are numerous important factors to consider when undertaking due diligence of a mining opportunity (management capability, grade, tonnage, etc.) that we use in the Discovery Investing Ten-Point Factor Model, but we think that there are three keys one must consider initially before looking further at a given rare earth exploration company as an investment.

Despite the fact that we believe the “easy money” has already been made in this sector, we do believe that opportunities for profit exist. Much has been made in recent months of “critical” or “strategic” metals and what constitutes a metal joining this group. We would certainly include rare earths here and, in fact, take this one step further. We consider rare earths to be “political metals.” In the rare earth sector, geopolitics trumps all, and this is the first factor to consider when investing in the junior mining rare earth sector. It should be clear that we have our doubts about permanently increasing demand for REOs. However, due to the significant enhancements REOs provide in military applications, access to a reliable supply of these metals is now on the radar (pardon the pun) of politicians from Brussels, to Ottawa, to Beijing, to Washington DC. In the United States, Sen. Lisa Murkowski (R-Alaska) has been an ardent supporter of rebuilding the U.S. industrial base and supply chain for critical minerals, including rare earths. Rare earth deposits are of strategic significance. A deposit in a safe and stable political jurisdiction is an absolute must.

Second, when comparing rare earth deposits, a decidedly large slant towards HREE mineralization is also a must. After all, the HREEs are truly “rare,” and forecast to be in deficit going forward. In our opinion, investing in a large LREE deposit that promises tens of thousands of tons of REO production per year, when the Chinese dominate this portion of the market and are set to do so going forward, is not a wise move. In the price chart we printed above, dysprosium oxide and terbium oxide (two of the most sought-after HREOs) have increased in price by 704% and 439% respectively, year-to-date. We do not expect continued triple-digit gains in these REO prices, but do believe that deposits with a high percentage of HREEs have potential to outperform going forward.

Finally, while the geopolitics and HREE content are important, without a solid understanding of the metallurgy of a deposit, you could quite literally be investing in moose pasture. This is one of the ultimate differences between rare earths and other metals. Separating 17 metals from each other is an enormously difficult task both technically and financially. This is also a competitive advantage the Chinese have over the West—they have “cracked” the metallurgy of their primary rare earth deposits. While we don’t expect miracles, we do want to see Western rare earth companies making steady progress into understanding the mysteries of the metallurgy. This is one of the biggest risk factors when analyzing a rare earth exploration company.

The Future Is Never Certain, but There Will Always Be a Place for REOs

It appears to be a rather hazy future for the rare earth sector as slow economic growth, potential for substitution, manufacturers potentially misreading demand for their own products that use REOs and price mean reversion all come together to take some of the “froth” out of this market. We think this is a good thing. Regardless, the big picture issues surrounding the need for REOs in various military and clean tech applications are going to keep the industry front and center, but it will evolve much differently than many expect. The Great Reset will ensure that.

Chris Berry, with a lifelong interest in geopolitics and the financial issues that emerge from these relationships, founded House Mountain Partners in 2010. The firm focuses on the evolving geopolitical relationship between emerging and developed economies, the commodity space and junior mining and resource stocks positioned to benefit from this phenomenon. Chris holds an MBA in finance with an international focus from Fordham University, and a BA in international studies from The Virginia Military Institute.

Want to read more exclusive Critical Metals Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about critical metals companies, visit our Critical Metals Report page.

Two things stand out in the just released September holdings update of Pimco’s flagship Total Return Fund: first, what appears to be a record cash short of 19% of the fund’s total unchanged AUM of $245 billion, doubling the previous short of -9%. The incremental cash was used almost entirely to purchase Mortgage Backed Securities, which jumped to 38% of total from 32%, even as the fund kept its government exposure virtually flat at 22%( 21% previously). (click on chart for larger image)

(click on image for larger image)

That’s either what is called betting one’s farm on Operation Twist, or, betting one’s farm that the next thing to be purchased by the Fed in QE3 or QE4 depending on how one keeps count, will be Mortgage Backed Securities. As a reminder, the last time Gross saw such a surge in MBS holdings in the TRF was side by side with the phased out roll out of QE2 when it was unclear if the Chairman would be buying USTs or MBS.

Pimco is a global investment management firm with over 1,700 dedicated professionals focusing on a single mission: to manage risks and deliver returns for our clients. For four decades, we have managed the retirement and investment assets for a wide range of investors, including public and private pension and retirement plans, educational institutions, foundations, endowments, corporations, financial advisors, individuals and others around the globe.

Ed Note: With volatility rampant and markets in 2011 and a wide range of markets all down whether its the Stock Markets in Greece -45%, Hong Kong 25%, Denmark -24%, the TSE -20 % or a sharp collapses in Silver -40%, Gold -15% and Copper down suddenly -30% it’s a painful time for investors who’ve been caught in the turmoil. With this backdrop Michael Campbell asked Danielle Park how she and her firm has managed exceptional results since the markets began going haywire in 2007, and how an ideal portfolio ought be constructed to cope with and ultimately buy the bottom of this bear market.

Michael Campbell: A lot of investors must be wondering if they should have sold at or near the markets highs this summer. For those that are caught in this decline, what kind of advice would you give those individuals?

Danielle Park: These cycles are not “buy and hold” environments. You can’t just ride things up, and expect dividends to be as sufficient protection on the down aside. I think we are probably half way through what we could end up seeing in this particular down turn. This is like a déjà vu of about February of 2008 for me when markets had come off a bit and the main stream was still not pricing for a recession but all of our indicators were suggesting extreme risk warnings, net cyclical decline and when you are in a secular bear market cyclical declines tend to last 18 to 24 months and you tend to get a 45% drop in the stock market. So those are the facts that the we have to cope with and I think that it’s a mistake to think you can just hold through. Just one other thing, volatility is a word that I think is used to mask the reality of what’s going on here Michael, this is not just volatility this is capital destruction. The trend has been fully down since April you know major markets like the venture exchange is off +40%. Copper is down more than 30% the Canadian market is off about 20%. I mean this is not volatility I think that’s a misnomer, that’s the word people say to say “Oh well you should just ignore it.” I don’t think you should ignore it you should raise cash. You should have done it already but I still don’t think it’s too late.

Micheal: Danielle why don’t people act? If I look at an equity portfolio and it’s an uncertain time I say “Well you sure have a lot more certainty than I do.” I am just wondering so why don’t people take action from your experience?

Danielle: I think it’s not being aware of how bad the declines can be in this type of environment and since the investment management business never give advice that’s proactive, they never tell people at the peak they should start selling. I think its programming from the investment management business that tells people they are never supposed to panic or react and when people start to sell in the down turn their always told that they’re panicking, that they shouldn’t do anything. This programming results in people becoming trend following sheep and fall right off the cliff and no sane person reacts well to big capital losses. The whole idea that people can just buy and hold and not worry about the big declines is absolutely not my experience. The trauma comes whether you want to admit it or not. At some point people just start to panic, they get insomnia, they can’t sleep and the capitals destruction that happens Michael takes years to recover and that’s I think the point that is so glossed over when they say “Oh, it will come back”. I have heard that lately a lot. People will say “My advisor says not worry because it will come back just like it did in ’09.” But I think that people have a very short memory because ’09 was this really anomalous bounce back in stock markets that happened because of all the money coming in from governments but it’s not the normal experience to see a stock market bounce back 80% in a matter of months. In fact this time once this decline happens and governments are now pretty much out of bullets I wouldn’t be surprised to see a recovery that takes a five or six years from here before people see perhaps the April highs revisited.

Michael: I hate the question when someone asks me “What do I do now?”because I am thinking “Well you should have done it before.” Regardless Danielle, if an investor is loosing sleep, the uncertainty is killing him or her, what would you tell them to do right now?

Danielle: You know at Venable Park we haven’t lost any money in this down turn, and we didn’t lose money in 2008. It’s not necessary to go through this god awful cycle every couple of years, that’s the first thing I try and explain to people. Unfortunately they think that they are strapped on a rollercoaster and they don’t know there is a belt buckle so you can actually get off of the damn thing. You don’t have to just stay there frozen in spot. Most peoples reaction is “What? I thought you’re supposed to just stay with it.” Right now we are getting a lot of calls from people that are fully long at your typical brokerage and investment planning houses. Unfortunately they have already lost a ton of money and we are not through the secular bear yet. So this is the third cyclical decline in the secular bear. If we are lucky this one will go in long enough and deep enough that we will finally squeeze the excess out of valuations, squeeze the over leverage out of the system and we we’ll get another really amazing buying opportunity sometime in the future, perhaps within the next 12 months. But here is the thing, you still have to know how to manage risk going forward from there. So yes it would have been better if you would have sold your equities any time in the last 12 months but in my view the right time to get on the correct risk controlled method is still today. So when people are calling me today saying here is my portfolio and they got a bunch of the usual suspects, Canadian portfolios that are full of energy and resources and all the high beta stuff. I say “Listen, you probably will see further declines here and the point is that we need to get your account structured correctly now.”

Michael: Danielle, pick any age group or characteristics you want but what should an ideal portfolio look like?

Danielle: Well I can tell you how we have made money in year to date and how we made money in 2008, it’s amazing it’s almost exactly the same. Basically we got a sell on all the equity units in late 2007 and that happened to us in 2010 as well. So no equity exposure presently here year to date. We found bonds sold off last December giving us a great buying opportunity to add back come high quality credit. Some of those bonds are up 6 to 10% already on top of the income. In addition the US dollar broke out in our work and we’re expecting that we could see the Canadian dollar fall considerably further in this particular cycle in which case you could make excellent very low risk returns. We made 20% on that trade in 2008 and we’re up several percent on it already in 2011. So the ideal portfolio is 50% high quality credit, 25% US T-bills and 25% Canadian cash. That is not something I am talking about holding for a few years, I am talking about holding it while things sell off and make whatever bottom they are going to do this time, so that you have optionality to buy things when they are on sale and everybody else is panicking.

Michael: Thank you Danielle. Danielle Park is the President and Portfolio Manager of Venable Park Investment Counsel Inc. and author of the book Juggling Dynamite and blog by the same name.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair