Daily Updates

Who says central bankers can’t inflate an economy to prosperity? To head-off the worst economic downturn since the Great Depression, the “Group-of-20” central banks have slashed interest rates to record lows, while politicians have funneled trillions into the coffers of the most powerful Oligarchic banks. So far, the cost of mopping up after the world financial crisis is a staggering $12-trillion, or equivalent to around a fifth of the world’s annual economic output.

The hefty price tag includes capital injections pumped into banks in order to prevent them from collapse, the cost of soaking up toxic assets, guarantees over debt, and liquidity support from central banks. Most of the cash, about $10.2-trillion, was spent by the so-called developed countries, while the emerging countries spent only $1.8-trillion, mostly in the form of liquidity injections into banks.

In return for this hefty investment, the pace of job losses has slowed, and there’s been a recovery in industrial output. At the same time, global stock markets have bounced back with startling speed. Since hitting bottom in March, the MSCI World Index has rebounded by 50%, and key industrial commodities, such as crude oil, copper, rubber, and iron-ore have also rebounded in synchronization.

In return for this hefty investment, the pace of job losses has slowed, and there’s been a recovery in industrial output. At the same time, global stock markets have bounced back with startling speed. Since hitting bottom in March, the MSCI World Index has rebounded by 50%, and key industrial commodities, such as crude oil, copper, rubber, and iron-ore have also rebounded in synchronization.

World markets were ecstatic, after the G-20 finance ministers pledged to continue to underwrite the global recovery with massive stimulus, in the form of deficit spending, ultra-low interest rates, and expanding the money supply. On Sept 2nd, US Treasury chief Timothy Geithner said although the global economy has pulled back “from the edge of the abyss,” it’s too early to let up on inflating stock market bubbles. “We’ve come a very long way. We still have a very long way to go,” he said.

The G-20 central banks have pumped an ocean of high-powered liquidity into the world banking system, designed to artificially inflate asset markets. Under the radical “Quantitative Easing” (QE) scheme, the Fed is printing $1.75-trillion in order to buy Treasury and mortgage backed bonds. The Bank of Japan is printing 1.8-trillion yen each month, and monetizing half of Tokyo’s budget deficit this year. The Bank of England has expanded its hallucinogenic QE program to 175-billion pounds.

Even so, US President Barack Obama said on Sept 9th, the G-20’s work is far from complete. “As the leaders of the world’s largest economies, we have a responsibility to work together on behalf of sustained growth, while putting in place the rules of the road that can prevent this kind of crisis from happening again. To avoid being trapped in the cycle of bubble and bust, we must set a path for sustainable growth while steering clear of the imbalances of the past,” Obama declared.

….read this extensive article and view 6 more charts HERE.

Gary Dorsch, editor of the Global Money Trends newsletter

Background and Experience

Worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group, members of the CME and CBOT. Gathered news and information from trading pits and newswire sources on the Chicago Mercantile Exchange, and telexed daily and weekly analysis of foreign exchange, global interest rates, gold and other commodities to clients in Hong Kong, London, the Middle East, and dozens of commodity trading advisers across the United States. After the closing bell, Mr Dorsch broadcasted a half-hour talk show on the financial markets to 40 customer branch offices around the United States via live hook-up from the trading pits of the Chicago Merc.

Brief comment below from the Ledendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

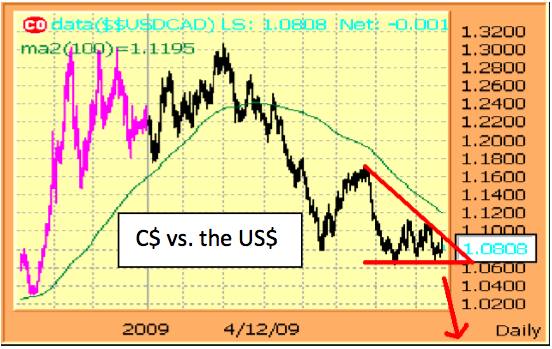

We note that as the US dollar is under pressure once again, the “other” dollars are not. The Canadian, Australian and New Zealand dollars are strong once more and that is as it should be, for their economies are stronger than is that of the US; their exports more viable and the propensity on the part of foreign nations to buy Canadian, Aussie and “Kiwi” goods seems to be rising at the expense of buying American goods. Let’s chalk this off to the simple notion that all things being otherwise equal, Chinese buyers of wheat, or steel, or crude oil, or coal, or water or any of the “stuff” of day- to-day economic growth will have a greater propensity to buy from these countries than from the US. Friendlier relations between Beijing and Ottawa, or between Beijing and Canberra or between Beijing and Wellington drive trade. With China’s buyers of raw materials scouring the world for these things, it is reasonable… it is even logical… to expect those buyers to find sellers in Vancouver, in Sydney and in Auckland.

We have been and we remain this morning concerted bulls of the Canadian dollar relative to the US dollar for the same reasons we have been bullish for the past several years on balance. The world needs energy: Canada has energy to go; The world needs food; Canada’s got food; The world needs base metals; they can be found in Canada…and Canada has the ports to ship those needs; it has the laws to protect contracts signed, and it has favourable and friendly relations with everyone… something the US cannot say it has or enjoys.

Ed Note: The Legendary Trader Dennis Gartman will be speaking at the:

The Money Talks All Star Trading Super Summit

Saturday, October 24, 2009 -The Sheraton Vancouver Wall Centre

Click HERE for the Speaker Lineup and to REGISTER if you want to take advantage of this Event.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

IN THIS ISSUE

• While you were sleeping: German ZEW index came in below market expectations — Euro sold off on the news despite the index being at its highest level in three years; U.K. RPIX inflation as expected

• Reviewing some secular themes: We are in a post- bubble credit collapse environment; the transition to the next sustainable bull market and economic expansion is likely years away

• San Francisco Fed President Janet Yellen supports our cautious view

….read pages 1-6 HERE

(Ed Note: One short but interesting section below)

REVIEWING SOME SECULAR THEMES

We are in a post-bubble credit collapse environment. The transition to the next sustainable bull market and economic expansion is likely years away. The most notable “non-confirmation” signpost for this bear market rally in equities is the 3-month Treasury bill yield, which is just 13 basis points away from zero. This could be Japan all over again.

The global economy is being held afloat by rampant fiscal stimulus, which is accounting for all of this year’s growth rate and 80 pct of next year’s. This is very much like the 1930s when the pace of economic activity was in need of major stimulus. The sharp downdraft in the equity market and the steep recession in 1937-38 after the government had the temerity to remove the life support fully eight years after the initial shock is case in point.

As for the U.S.A., real GDP would have contracted at a 6% annual rate in 2Q, not 1%, if not for the dramatic fiscal stimulus out of Washington. As for the current quarter, that 2-3% annualized GDP gain penned in by the consensus would actually be flat to negative without all of the fiscal help (ie, Cash for Clunkers) While policy reflation is massive, there are limits and to date, the initiatives have only helped cushion the blow. The key to the inflation process is not what the Fed is doing to the money supply but the extent to which, if at all, the “liquidity” is being circulated in the real economy. Velocity is still contracting. You can bake a cake as a central banker, but that doesn’t mean anybody is going to eat it. Rents are declining for the first time in 17 years. Consumer credit is contracting at a rate not seen in 65 years, and this not only reflects a desire to bolster depleted savings rates but also rising charge-off rates among lenders; and, wages/salaries are shrinking at an unprecedented annual rate of nearly 5%. Between rents, credit and wages, we have a deflation on our hands of epic proportions.

“There are no rules here – we’re trying to accomplish something.” – THOMAS EDISON

Dr. Tatyana Koryagina, a senior research fellow in the Institute of Macroeconomic Research in Moscow, stated in a Pravda interview that “the U.S. is engaged in a mortal economic game. The known history of civilization is merely the visible part of the iceberg. There is a shadow economy, shadow politics and a shadow history.” She went on to say, “It is possible to do anything to the U.S…whose total debt has reached $ 26 trillion. Generally, the Western economy is at the boiling point now. Shadow financial activities of $300 trillion are hanging over the planet. At any moment, they could fall on any stock exchange and cause panic and crash.” She further stated, “The U.S. has been chosen as the object of financial attack because the financial center of the planet is located there.” 1

This is a very interesting statement from an individual who is known as a personal advisor to Vladimir Putin, the Russian Prime Minister. What do the Russians know – what is Vladimir Putin privy to? Why were institutions and individuals blindsided by the financial tsunami of 2008? They did not understand that liquidity can be an illusion. It is there when you don’t need it but “gone with the wind” when you do.

Ed Note: You can Order the Book “New World Order Ecomomics – What you can do to Protect Yourself – HERE.

Tatyana is telling us with some dark speech that the only thing we don’t know about investing is the investment history we don’t know. It’s not necessarily confined to a matrix. We’re in the very beginning stages, depending on who you listen to, of the worst financial crisis since the Great Depression. It’s the ‘shadow financial system’ that has created the current crisis that we’re in. The shadow financial system consists of non-bank financial institutions that, like banks, borrow short, and in liquid forms, and lend or invest long in less liquid assets. They are able to do this via the use of credit derivative instruments. The system includes SIVs (Structured Investment Vehicles), money market funds, monolines, investment banks, hedge funds and other non-bank financial institutions. These are subject to market risk, credit risk and particularly liquidity risk.

We have learned that Investment Banks (and active managers in general, such as hedge funds) cannot protect from bear markets. They themselves were unprotected. One exception (if you consider a 2-year history) were the Paulson Credit Opportunities and Paulson Credit Opportunities II hedge funds, which produced net returns of about 590% and 352% in 2007 and lesser returns of about 19% and 16% in 2008. The Paulson Event Arbitrage Fund returned 100%, and the Paulson Merger Arbitrage fund returned 52.0% in 2007. The amount of money generated by Paulson and Co., both for themselves and their partners can only be described as ridiculous. These funds generated tens of billions of dollars in profit in 2007. If the fund operates with a traditional “2 and 20” (2% management fee, and 20% performance fee), that means that the fund likely generated at least 3-4 billion dollars in profits for the principals. Not a bad year. 2008 was more subdued. The primary leverage against the sub-prime market was effectively utilized in 2007 by these funds. I list these because they’re an excellent example of principle – innovative think-tank type planning and execution. Once it was planned it was as good as done.

The opposite of this thinking is reflected in how the State I happen to be from lost $ 61.4 Billion in state-administered funds last year and a half. The State Board of Administration protects $ 97.3 billion in pension money for retired state employees, and invests another $ 25.3 billion for school districts and state and local governments. A close friend of mine sat on the Board for ten years. Auditors warned them year after year about complex and high-risk investments but these warnings were ignored. Now I just read in the Sunday paper that in the last 18 months $ 61.4 Billion was wiped out. The chief internal auditor who wrote one of the more recent reports stated “Risk is an inherent component of doing business. To appropriately manage risks, organizations should have mechanisms to identify, measure and monitor relevant key risks not only at the business or product level, but at the institutional level.” The SBA took on real estate and private partnership investments, and added leverage to the equation. One investment, $ 5.4 Billion into an apartment complex in Manhattan, is now valued at 10% and Wall Street credit firms have downgraded bonds tied to the deal. They were also using complicated financial instruments called derivates, which billionaire investor Warren Buffet once called “financial weapons of mass destruction.”

In the 18-month period covered by the audit, the unit handled $ 1.1 trillion of transactions with limited oversight. One trader bet $ 1.4 billion on a single trade. The audit also revealed that the unit let an unauthorized trader, a trainee, deal a total of $ 30 billion in securities. In the audit period, 70% of the trades were done with only four brokers – Bank of America, Goldman Sachs, UBS and the now-defunct Lehman Brothers. While they delayed finalizing the audit, the 2006 State Legislature passed two bills allowing the SBA to use even riskier financial strategies, and the other made it more difficult for outsiders to scrutinize some SBA investments. In August 2007 they were finally required to attend risk training. A former senior investment analyst at one of Canada’s largest pension funds says our state is on a “disaster course.” Deloitte & Touche, a firm my uncle used to be Washington DC partner of, recently completed a $ 198,750. Investment Performance Risk Review and another firm has been hired for a $ 182,500 contract (plus expenses). The SBA says it’s a pittance and “money well spent.”2

The auction-rate securities market, hundreds of billions, seized up in 2008. Indy Mac failed in 2008. Lehman left the country with a $ 168 Billion bankruptcy in 2008. The AIG entry into the credit default swap field required a government bailout in 2008. Hedge fund losses were huge, the worst in 15 years in 2008. The current crop of LBOs for the most part failed in 2008.

Let’s look at Mortgage Backed Securities and CDOs. The complex market for asset-backed securities took a major blow. A U.S. Federal Judge ruled to dismiss a claim by Deutsche Bank National Trust Company. The US subsidiary was seeking to take possession of fourteen homes from Cleveland residents living in them, in order to claim the assets. The Judge asked DB to show documents proving title. No mortgage was produced, needless to say. The net result is that hundreds of billions of dollars worth of CMOs in the past seven years are not securitized. One source places the number at $ 6.5 Trillion.

Global securitization was a phantom idea – when large banks bought tens of thousands of mortgages, bundled them into Jumbo securities and then had them rated prior to sale to pension funds or accredited investors, they believed they were selling (and the counterparties believed they were buying) AAA or at the least investment grade quality. They never realized the bundle contained a significant toxic factor rated “sub-prime.” No one opened the risk models of those who bundled them.

In 2008 Investment Banks took on more risk than they had ability. Their baskets of risk were highly correlated. The leverage made no sense. When LTCM fell in 1998, this is exactly what happened. Banks as you know leverage 10:1 or greater. A $200 Billion loss in the financial system leads to a $2 Trillion contraction of credit. Lehman was at least 30:1 with just assets. Off-balance sheet risks were not considered which probably brought the leverage to over 100:1. Systemic damage has been done.

This is the worst financial crises this generation has ever faced. The housing sector is literally in free fall. New home sales started to fall since the beginning of 2006 and in some regions they are down over 30% since a year ago. The statistics are amazing. Calculated Risk, a very credible web site, estimates that a 10% drop in prices will create 10.7 million households in default. A cumulative fall in home prices of 20% implies 13.7 million households with negative equity while a cumulative fall of 30% implies 20.3 million households with negative equity. What is the size of these losses for financial institutions and investors? If a 15% total price decline occurs, and a 50% average loss per mortgage, the losses for lenders and investors is in the $ 1 Trillion category. Assuming a 30% price decline you can double that. 3 The whole spectrum of financial and credit markets is being effected. Commercial real estate is following the trend of residential.

You have to consider geostrategic and long-term issues before allocating assets. This would include foreign policy, energy supply risks and G7 bond and stock markets. You have to consider financial deleveraging on the currency market. You need to game out the scenarios of the IMF on this chess board, among many other players. Alternative investments holdings such as non-US denominated bonds (AAA rated in hard currencies), South African gold shares, direct holdings in strong currencies and diversifications into alternative investments are a must if you are to survive the coming seven to nine years as this L-shaped recession moves into progressive phases.

A synopsis of reasons I believe this is correct is deductive logic from a Global Economic Analysis site:

Roubini nailed three reasons for a severe recession but dismisses “L” because the U.S. acted faster than Japan. I do not buy that argument for these reasons.

U.S consumers are in much worse debt shape than Japan.

There is global wage arbitrage now that did not exist to a huge degree in the mid to late 1990’s. Even white collar jobs are increasingly at risk.

The savings rate in the US is in far more need of repair than what Japan faced. This will be a huge drag on future spending and slow any recovery attempts.

Japan faced a huge asset bubble (valuation) problem. The US faces both a valuation problem (what debt on the books is worth) and a rampant overcapacity issue as well.

Japan had an internet boom to help smooth things out. There is no tech revolution on the horizon that will provide a huge source of jobs.4

93% of stock market newsletters lost major capital for the readers last year. As opposed to market newsletters, at a recent conference in Dubai a speaker said that credit crisis losses could hit $ 3.6 trillion, up from $ 1 trillion worth of writedowns and losses estimated by Bloomberg. If losses are this great, the U.S. banking system is effectively not solvent since it starts with a capital of $ 1.4 trillion. The Royal Bank of Scotland is facing an estimated $ 41 billion loss.

In fact, this has indirectly caused a boom in the class-action field. In 2008, the number of federal securities filings reached a six-year high, with 267 filings. That’s a 37% increase from the previous year. Almost half were related to the credit crisis. Investors are claiming they have lost approximately $ 856 billion, according to the Stanford Law School Securities Class Action Clearinghouse. That’s a 27% increase over 2007. Most of the actions are against firms in the financial industry. A director of Stanford Clearinghouse said he hasn’t seen this much litigation against a single industry in over a decade. One-third of all major financial firms were named as defendants in these actions. Most of the cases allege securities fraud, or altering values. Underwriting practices were allegedly misrepresented. The firms that sold auction-rate securities, bonds with interest rates reset by bidding, were all hit with class-actions, as the market completely dried up last year.

California is bankrupt ($42 billion deficit) and it’s public knowledge that it is delaying payments as of February 1st on vendor payments and tax refunds. Active mutual fund managers cannot protect anyone. In the last twelve months their returns have approached in some cases 50% losses. Investors, both corporate and individual, took on risks they did not have the ability to handle. Many investors in the Madoff scheme were guilty themselves of concentrating virtually their entire portfolios in his hands. “The only difference between myself and a madman is that I am not mad” – Salvadore Dali stated this but it looks like it will be the defense of Madoff according to his lawyer.

A memorable quote from Dorothy in the Wizard of Oz is “Toto, I’ve a feeling we’re not in Kansas anymore.” To re-balance your portfolio you’ve got to come to the same realization. You’ve got to devote a lot of due diligence to a Performance Review and game out scenarios just like the CIA does every day. I wrote one of the most detailed treatises of Corporate Risk Management, and the Enron debacle ever published (by the parent company – Thomson Reuters) – a book called “Protecting Your Company Against Civil and Criminal Liability.” I learned you cannot trust your future to Princeton economic professors – they work best only in ivory towers.

With regard to bailouts, US dollar injections have not so far encouraged the market. Unless they are handled properly they can trigger a major devaluation of the dollar or lead the nation further into stagflation, then deflation and ultimately depression. The UN has predicted a dollar collapse in 2009, according to a team of UN economists who foresaw a year go that this US downturn would bring the economy to a standstill. They have stated that the US debt position is approaching unsustainable levels.

Rense, a top alternative news source reference, in an article on economic protocols, reports:

Therefore, if the planet can no longer generate any more liquidity to lend to the United States, one of three things have to happen: A) There has to be a sudden and dramatic reduction in federal spending. There are only two places that can come from. There would have to be an immediate cut in defense spending and entitlements. This is highly unlikely.

The other option, B, is a dramatic increase in the rate of federal income taxation from the current nominal rate to 65%, which is what the Treasury Department estimated would be required post-2009 to provide the U.S. Treasury with sufficient revenues to continue to service debt.

The third option, or C, becomes the declaration of a force majeure on credit service of U.S. Treasury debt by the United States Treasury, which is tantamount and would be accurately construed as de facto debt repudiation by the United States of America. That is the classic definition of a devaluation. What institutional and large corporate investors (as I work with) call ‘fast market conditions’ would occur. There would be the declaration of ‘no more stop orders,’ the declaration of ‘fill at any price,’ etc. in a desperate bid to maintain liquidity. 5

Let’s Take A Brief Look At 2008:

Housing – down 18% nationally and 30% plus in cities

Emerging market funds – down 55%

Bonds – Rates on 10 year Treasuries dropped 42%

US Treasury yields – very low and for a time close to zero

Bond values – down 6-24% on average depending on the funds and quality of bonds

DJIA – down 33%

S & P 500 – down 38%

NASDAQ – down 40%

Financial sector ETFs – down 55%

Very weak economic data reflecting deteriorating economies continues to be released from the U.S. and the U.K. As of the end of January 2009 March crude is now at a low of $ 41.67 a barrel. In the U.S., the S&P/Case Shiller home price index experienced its largest single-month drop in November, indicating no bottom was near in the housing market. The Conference Board reported that the January consumer confidence index fell to an historic low. US retail sales fell for a sixth consecutive month in December – retail sales were down by 2.7%. According to the Federal Reserve’s Beige Book the economy is expected to weaken further into 2009. The Fed funds rates are expected to be kept at 0 to .25% as the Committee continues to anticipate that economic conditions warrant low levels for Fed funds rates for some time. US GDP figures indicate the economy contracted by 3.8% in the fourth quarter of 2008. A recent Federal loan survey indicated tightened lending standards for 60% of the banks on credit card and consumer loans. Moreover, 80% said they tightened lending standards on commercial real estate loans. The commercial sector has significant excess capacity. S & P, based on a substantial worsening of the economy and financial environment, expects the default rate in the US corporate speculative-grade segment to catapult to an all-time high of 13.9%, meaning 209 issuers may default by December 2009.

Protocols for environmental disasters are called ‘scaling-circle scenarios.’ ‘Scaling circles’ is a Department of Defense euphemism. It’s also used in FEMA, OEM and other emergency management services. The risk has got to start someplace. It’s going to start in one very small, specific area. Therefore what happens is that the immediate force containment is the greatest in the first circle, to try to contain the spread of the disaster and keep it within that circle. That’s what you have to do.

You have to consider macroeconomics before you reposition your assets. You have to reposition assets. You have to close all major risks. Exit the majority of money funds and currency time deposits, step up gold and oil positions, and move into non-US government bonds in First World nations. Switzerland is a prime consideration, but there are first-class world banks with branches just a short flight from Florida. You have to modify your thinking as if you are on a special ops tour of duty. Otherwise the current toxic economic environment will continue to deplete non-repositioned assets. Let’s begin this journey together…

You can Order the Book “NEW WORLD ORDER ECONOMICS -WHAT YOU CAN DO TO PROTECT YOURSELF – CRISIS INVESTING FOR 2009 – WELCOME TO THE NEW WORLD” HERE.

Article and Book via Chris Vermeulen, founder of TheGoldAndOilGuy newsletter. I provide you with unparalleled trading newsletter with charts, signals and email support. Unlike other investing newsletters, I’m a one man show. That’s because I don’t want some hired hand giving you advice while I take it easy on a beach somewhere. You ALWAYS get precise, valuable information DIRECTLY from ME. You can sign up HERE.

One of Michael Campbell’s favorites, Black Swan Capital is offering Exclusively for readers and listeners of MoneyTalks a very SPECIAL OFFER.

In Today’s Currency Currents….

“A headline I came across this morning stated plainly: Economic Recovery May Prove Much Stronger than Expected.”

Quotable

“Don’t ever average losers. Decrease your trading volume when you are trading poorly; increase your volume when you are trading well. Never trade in situations where you don’t have control. For example, I don’t risk significant amounts of money in front of key reports, since that is gambling, not trading.” – Paul Tudor Jones, in Market Wizards

FX Trading – The Feel-Good Measure

France’s per capita GDP is roughly 14% lower than per capita GDP in the US. But that’s only a mirage … and only factors in economic figures, rather than the actual mood of those who make up the economy. The differential between the two economies should actually be much narrower, or so we’re told.

Perhaps France isn’t the only economy bogged down by its economic numbers. Germany keeps reporting stronger levels of consumer, investor and business confidence. Just today the ZEW index of investor confidence rose to highs not seen since the end of 2006.

Bear in mind that lofty confidence numbers at that time were no surprise – it marked the peak of the global credit bubble; times were good.

Despite the fact that kneejerk reaction to today’s ZEW number is poor because analysts were actually expecting a much stronger number, it begs the question: what are they putting in the water over there in Germany?

Whatever it is, don’t forget to factor that into their GDP figures.

It’s obvious just by looking at the markets of late that the consensus is looking for a solid recovery, perhaps having already commenced. A headline I came across this morning stated plainly: Economic Recovery May Prove Much Stronger than Expected.

Ok, very well then. But someone better tell the UK so they don’t miss out on the happiness boat.

The Bank of England is considering ratcheting down their deposit rate a bit further, in an attempt to encourage banks to lend all that money the BOE has shared with them; it seems UK banks (and most others for that matter) haven’t conveyed the same confidence in recovery as global investors. The Bank governor noted today that the country’s major banks are still dependent on public sector aid.

Darn – I can’t imagine how this somber tone must be influencing the GDP mood of the United Kingdom.

And is the European Central Bank at risk of falling victim to similar feelings? Sure, Germany and France seem to have their minds focused on the ultimate goal. But the ECB doesn’t have the luxury of governing just France and Germany. As the article in the Key News section above discusses:

“Europe’s economies are rebounding at different speeds, complicating the European Central Bank’s efforts to put the region back on a more stable footing.”

Now that just doesn’t seem fair that the ECB has that demonstrative hurdle impeding its effectiveness. And on that note, China’s Ministry of Commerce spokesman, Yao Jian, chimed in on the recent tariff imposed on Chinese tire exports to the US.

He said, “It’s not fair if the U.S. only cares about its own employment and not China’s growth,” noting the potential for social instability should Chinese industry begin to feel the pain of this decision.

Not fair? It seems, though, that what the US has done here fits within the guidelines of the WTO agreements (assuming one has time to read through tens of thousands of pages highlighting how “free trade” is supposed to work).

So what’s not fair? Looking out for the interests of the economy that’s under your direction? China should know something above favoring its own economy, in a very perverse sort of way.

Perhaps Joseph Stiglitz has it right. He’s part of the fine crew that’s responsible for proposing measures of societal well-being, or as it could be also called: economic fairness accounting.

“A political leader attempting to promote the well-being of his citizens is pulled in different directions: he will be graded on economic performance but there are many other dimensions to the quality of life, including the state of the environment. While there is no single indicator that can capture something as complex as our society, the metrics commonly used, such as gross domestic product, suggest a trade-off: one can improve the environment only by sacrificing growth. But if we had a comprehensive measure of well-being, perhaps we would see this as a false choice. Such a metric might indicate an increase in wellbeing as the environment improved, even if conventionally measured output went down.”

Karl Marx would be so proud. This should work wonders on drowning out the capitalistic shortfalls of the markets.

We are all psychiatrists now.

Jack and JR

Black Swan Capital LLC

www.blackswantrading.com

Exclusively for readers/listeners/members of MoneyTalks a very SPECIAL OFFER.

Three Full Months of EVERYTHING We Do For Just $99!

Dear MoneyTalks Reader/Listener,

Exclusively for fans of MoneyTalks with Michael Campbell, we’d like to make you an EXCLUSIVE OFFER.

Sign up now to receive 3-months of ALL our advisory trading services and we’ll discount the price by more than 80% – three full months for less than one month’s cost! Plus if you like what you see you’ll continue getting all our trading services at the discounted rate of just $99 per month for as long as you want.

You see, we recently segmented our all-in-one newsletter, Currency Strategist, into four brand new, separate, focused newsletters. As we launch we thought we’d extend an opportunity for you to get in early …

At a very special price.

Everything listed below for 3 months … for just a onetime payment of $99.00.

The value of all these services together is $2,434.00 per year … or about $200 per month. We’re offering you the opportunity to get three full months for just $99.

That’s a difference of over $500.00 for the first three months, and …

With this offer you lock in forever additional savings of more than $100 each and every month off the total value of these services for as long as you remain a member.

As a member you’ll receive…

Currency Currents

Description: Macro view of the global economy and how it may impact currency prices.

Frequency: Daily

Price: Free

Currency Investor

Description: Designed to help investors ride intermediate- and long-term trends in major and select emerging market currencies.

Frequency: Monthly

Recommendations: Exchange Traded Funds (ETFs) [*Analysis and time frames also support multi-currency deposit investors.]

Everyday Price: $149 per year

Currency Options

Description: Designed to provide speculators with trading recommendations covering both the FX options listed on the International Securities Exchange (ISE)and currency futures options listed on the Chicago Mercantile Exchange (CME).

Frequency: Bi-weekly

Average Holding Period: Days or Weeks to months

Recommendations: International Securities Exchange (ISE)-listed FX Options or Chicago Mercantile Exchange (CME)-listed currency futures options

Everyday Price: $595 per year

Emerging Market Currencies

Description: Designed to help traders and speculators exploit short- and intermediate-term trading opportunities in the highly volatile and potentially profitable world of emerging market currencies.

Frequency: Bi-weekly

Average Holding Period: Weeks to months

Recommendations: Spot Forex

Everyday Price: $695 per year

Forex & Currency Futures Description: Designed to help short-term traders, using high leverage, spot trading opportunities among major currency pairs and cross rates.

Frequency: Daily

Average Holding Period: Intraday to several days

Recommendations: Spot Forex and Currency Futures

Everyday Price: $89 per month or $995 per year

[Note: All services include Flash Alerts delivered outside of regular publication dates to enter or exit positions as the market dictates.]

THIS IS WHERE YOU WIN …

As a fan of MoneyTalks, we’re offering you an outstanding deal.

Get three months of all our services for just a onetime payment of $99. That’s a savings of more than 83% on your first three months, and …

You lock in forever an additional savings of over 50% each and every month after that for as long as you remain a member.

Here’s some explanation on the different newsletters you’ll receive …

Our Emerging Market newsletter is geared towards specific emerging market commentary and takes time to evaluate individual countries and themes in depth. We will also recommend a balanced portfolio of currencies to hold as an emerging currency speculator.

In our Currency Options newsletter we are technical-minded, active, and a bit medium-term oriented … occasionally diverging from our longer-term fundamental market views. In addition to that, we incorporate a strict stop-loss guideline in our recommendations, usually around a 50-60% loss threshold, as well as a level at which to take partial profits. We believe this helps reduce the downside and allows for you to be more proactive in grabbing gains when you have them.

In the Forex & Currency Futures newsletter we are active and base most of our trade analysis on short-term technical setups — shooting to grab small open gains when we have them and keeping a skin in the game if we are fortunate to have latched on to a trend. That means you will consistently see recommendations to trade with at least two lots at a time. But remember: the size you trade and amount of leverage must make sense for your own account size and circumstances.

Within the monthly newsletter — Currency Investor — will reside the longer-term trend analysis work and thematic fundamental views incorporating a detailed look at weekly and monthly inter-market relationships between currencies, stocks, bonds and commodities.

Everything you read about above plus access to archives, webinar notifications, audio updates, special reports and more.

We work hard to consistently deliver, what we consider, the best currency trading newsletters available on the market today. We hope you’ll agree.

I urge you, if you were thinking about trading currencies, whether through options, ETFs, futures or Spot FX then don’t wait.

If you want an honest approach and a realistic look at currencies, you’ll have come to the right place.

If for any reason whatsoever you try us out and are unsatisfied with Black Swan’s currency newsletters within the first 30-days of your Membership, we’ll issue a full refund and our thanks for giving us a try.

Take advantage of this 30-day Risk Free offer!

So, if you’re ready to give us a try, Click Here to Sign Up

we’re looking forward to having you onboard with us!

P.S. As a BONUS, subscribe today and receive this 20-page Special Report:

Preparing for a Breakup in the European Monetary System

Most people are worried about the US dollar … and for good reason. These same people tend to see the euro as a real competitor vying for world reserve currency status. Many have been conditioned that way by the financial press. But we believe the risk of breakup in the European Monetary System is building rapidly. We examine the structure of this “artificial fiat currency” and why another downturn in the global economy could mean lights out for the euro. Be prepared.

Even if you decide to cancel, keep the report – it’s yours as a ‘thank you’ for giving us a try!

Even in tough times, which we recognize is on everyone’s mind these days, that’s a very reasonable price for the versatility and money-making potential packed into these newsletters. Of course, at a little over $3 per day you could instead put that money towards you’re morning cup of coffee on the way to work, I guess.

If you want to learn how to implement a solid approach to currency investing … or even if you’re just looking for well-researched trading and investing ideas …

Sincerely,

David Newman

Director of Sales and Marketing

Black Swan Capital

dnewman@blackswantrading.com

Toll-Free 866.846.2672

Futures, Forex and Option trading involves substantial risk, and may not be suitable for everyone. Trading should only be done with true risk capital. Past performance either actual or hypothetical is not indicative of future performance.

Black Swan Capital newsletter services are strictly informational publications and do not provide individual, customized investment advice. The money you allocate to futures or forex should be strictly the money you can afford to risk. Detailed disclaimer can be found at http://www.blackswantrading.com/disclaimer

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair