Daily Updates

Regular Guest on Money Talks, and one of Michael Campbell’s favorites Jack Crooks of Black Swan Capital is offering Exclusively for readers and listeners of MoneyTalks a very SPECIAL OFFER. When looking at investments or the Economy – “Its all about the price of currencies” – Michael Campbell

In Today’s Currency Currents….

FX Trading – “[We Won’t Be] Waiting on the World to Change.”

Quotable

“The stimulus that we have still got to give the world economy is greater than the stimulus we have already had. What we want to do is safeguard a recovery from a recession we feared would develop into a depression.” – Gordon Brown

FX Trading – “[We Won’t Be] Waiting on the World to Change.”

Some of you may not know this … but this week is Climate Week. The goal is to spread the word about climate change and the importance of enacting climate change legislation that addresses key problems associated with man-made global warming.

I will not be participating in Climate Week.

More of you may know that this week Pittsburgh, PA plays host to the G-20. The goal is to spread the word about economic status quo and the importance of enacting stimulus policy that addresses the major deficiencies associated with man-made financial crisis.

I’m not buying the G-20 summit.

Ideally, the market process would handle both the above issues on its own. But leaders don’t want to leave it to the free market; the free market is the problem, they’ll tell you.

So in an effort to look out for our best interest, the top-most officials on each matter will see to it that the market does no more damage and that legislation, regulation and policy take over the role of destroying saving the world.

But it doesn’t matter what I think. If what I thought actually mattered, then I’d be independently wealthy. Instead, it is what the market thinks that matters. And right now the market thinks (regarding the G-20 initiatives anyway) that the world has been rescued.

And if Gordon Brown’s quotable from above means anything, then the global economy should have no trouble getting back on its feet and global markets should run into few obstacles as the road to prosperity is paved for them.

So it shouldn’t come as a surprise when the US dollar can’t string together more than two days of corrective rally. Despite what the charting mechanisms may forecast, risk appetite in this market is running on high and the US dollar is hated.

This morning has already been a monster day for currencies. Using the US Dollar Index as the broad indicator, traders have wiped away the last two days of dollar advances and the index is testing last week’s low, which happens to be the lowest level for the US dollar index since this time last year.

To demonstrate my point about market sentiment here, the Asian Development Bank has made waves with their recent comments about growth in Asia. Markets love the fact that growth estimates have been revised upwards. They also love the fact that China has imported a whole bunch of crude – the second-highest monthly increase on record in August.

Logically, this could be taken as a sign that China is revving up the engines and is ready to pull out of pit road.

The market, though, found a way to avoid the comments from the ADB regarding China’s binge on stimulus and record lending. They particularly noted the decision to push back or ignore necessary rebalancing efforts that would help mitigate the dependence on investment and exports and spark some much needed growth in domestic consumption.

But why should that matter? Everyone’s having a good time now; nobody likes a party- pooper.

Pushing back the imbalances for another day, huh? The ADB seems to think this is what China’s doing. I’m not going to argue with them … as you probably already know.

But what about the G-20? Are they ignoring imbalances, are they pushing back the need

for rebalancing? If so, can they succeed in forcing growth on a global economy that’s not ready for it?

Call me old school, but the free market has been known to correct imbalances of yesteryear. No? Come to think of it, hasn’t the market already taken steps toward correcting such imbalances this time around?

John Ross Crooks III

Black Swan Capital LLC

www.blackswantrading.com

Exclusively for readers/listeners/members of MoneyTalks a very SPECIAL OFFER.

Three Full Months of EVERYTHING We Do For Just $99!

Dear MoneyTalks Reader/Listener,

Exclusively for fans of MoneyTalks with Michael Campbell, we’d like to make you an EXCLUSIVE OFFER.

Sign up now to receive 3-months of ALL our advisory trading services and we’ll discount the price by more than 80% – three full months for less than one month’s cost! Plus if you like what you see you’ll continue getting all our trading services at the discounted rate of just $99 per month for as long as you want.

You see, we recently segmented our all-in-one newsletter, Currency Strategist, into four brand new, separate, focused newsletters. As we launch we thought we’d extend an opportunity for you to get in early …

At a very special price.

Everything listed below for 3 months … for just a onetime payment of $99.00.

The value of all these services together is $2,434.00 per year … or about $200 per month. We’re offering you the opportunity to get three full months for just $99.

That’s a difference of over $500.00 for the first three months, and …

With this offer you lock in forever additional savings of more than $100 each and every month off the total value of these services for as long as you remain a member.

As a member you’ll receive…

Currency Currents

Description: Macro view of the global economy and how it may impact currency prices.

Frequency: Daily

Price: Free

Currency Investor

Description: Designed to help investors ride intermediate- and long-term trends in major and select emerging market currencies.

Frequency: Monthly

Recommendations: Exchange Traded Funds (ETFs) [*Analysis and time frames also support multi-currency deposit investors.]

Everyday Price: $149 per year

Currency Options

Description: Designed to provide speculators with trading recommendations covering both the FX options listed on the International Securities Exchange (ISE)and currency futures options listed on the Chicago Mercantile Exchange (CME).

Frequency: Bi-weekly

Average Holding Period: Days or Weeks to months

Recommendations: International Securities Exchange (ISE)-listed FX Options or Chicago Mercantile Exchange (CME)-listed currency futures options

Everyday Price: $595 per year

Emerging Market Currencies

Description: Designed to help traders and speculators exploit short- and intermediate-term trading opportunities in the highly volatile and potentially profitable world of emerging market currencies.

Frequency: Bi-weekly

Average Holding Period: Weeks to months

Recommendations: Spot Forex

Everyday Price: $695 per year

Forex & Currency Futures Description: Designed to help short-term traders, using high leverage, spot trading opportunities among major currency pairs and cross rates.

Frequency: Daily

Average Holding Period: Intraday to several days

Recommendations: Spot Forex and Currency Futures

Everyday Price: $89 per month or $995 per year

[Note: All services include Flash Alerts delivered outside of regular publication dates to enter or exit positions as the market dictates.]

THIS IS WHERE YOU WIN …

As a fan of MoneyTalks, we’re offering you an outstanding deal.

Get three months of all our services for just a onetime payment of $99. That’s a savings of more than 83% on your first three months, and …

You lock in forever an additional savings of over 50% each and every month after that for as long as you remain a member.

Here’s some explanation on the different newsletters you’ll receive …

Our Emerging Market newsletter is geared towards specific emerging market commentary and takes time to evaluate individual countries and themes in depth. We will also recommend a balanced portfolio of currencies to hold as an emerging currency speculator.

In our Currency Options newsletter we are technical-minded, active, and a bit medium-term oriented … occasionally diverging from our longer-term fundamental market views. In addition to that, we incorporate a strict stop-loss guideline in our recommendations, usually around a 50-60% loss threshold, as well as a level at which to take partial profits. We believe this helps reduce the downside and allows for you to be more proactive in grabbing gains when you have them.

In the Forex & Currency Futures newsletter we are active and base most of our trade analysis on short-term technical setups — shooting to grab small open gains when we have them and keeping a skin in the game if we are fortunate to have latched on to a trend. That means you will consistently see recommendations to trade with at least two lots at a time. But remember: the size you trade and amount of leverage must make sense for your own account size and circumstances.

Within the monthly newsletter — Currency Investor — will reside the longer-term trend analysis work and thematic fundamental views incorporating a detailed look at weekly and monthly inter-market relationships between currencies, stocks, bonds and commodities.

Everything you read about above plus access to archives, webinar notifications, audio updates, special reports and more.

We work hard to consistently deliver, what we consider, the best currency trading newsletters available on the market today. We hope you’ll agree.

I urge you, if you were thinking about trading currencies, whether through options, ETFs, futures or Spot FX then don’t wait.

If you want an honest approach and a realistic look at currencies, you’ll have come to the right place.

If for any reason whatsoever you try us out and are unsatisfied with Black Swan’s currency newsletters within the first 30-days of your Membership, we’ll issue a full refund and our thanks for giving us a try.

Take advantage of this 30-day Risk Free offer!

So, if you’re ready to give us a try, Click Here to Sign Up

we’re looking forward to having you onboard with us!

P.S. As a BONUS, subscribe today and receive this 20-page Special Report:

Preparing for a Breakup in the European Monetary System

Most people are worried about the US dollar … and for good reason. These same people tend to see the euro as a real competitor vying for world reserve currency status. Many have been conditioned that way by the financial press. But we believe the risk of breakup in the European Monetary System is building rapidly. We examine the structure of this “artificial fiat currency” and why another downturn in the global economy could mean lights out for the euro. Be prepared.

Even if you decide to cancel, keep the report – it’s yours as a ‘thank you’ for giving us a try!

Even in tough times, which we recognize is on everyone’s mind these days, that’s a very reasonable price for the versatility and money-making potential packed into these newsletters. Of course, at a little over $3 per day you could instead put that money towards you’re morning cup of coffee on the way to work, I guess.

If you want to learn how to implement a solid approach to currency investing … or even if you’re just looking for well-researched trading and investing ideas …

Sincerely,

David Newman

Director of Sales and Marketing

Black Swan Capital

dnewman@blackswantrading.com

Toll-Free 866.846.2672

Futures, Forex and Option trading involves substantial risk, and may not be suitable for everyone. Trading should only be done with true risk capital. Past performance either actual or hypothetical is not indicative of future performance.

Black Swan Capital newsletter services are strictly informational publications and do not provide individual, customized investment advice. The money you allocate to futures or forex should be strictly the money you can afford to risk. Detailed disclaimer can be found at http://www.blackswantrading.com/disclaimer

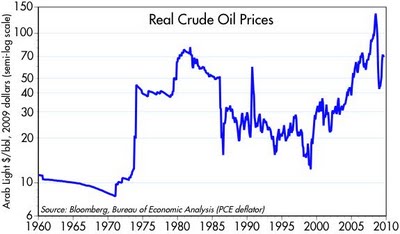

It’s been awhile since I’ve posted anything on the energy market, and I happen to have some interesting charts on the subject to share. This first chart is the real (in constant 2009 dollars, per the PCE deflator) price of crude oil going back to 1960. Oil has been trading around $70 for the past 3 months, and there is lots of talk about how inventories have risen and demand is on the verge of weakening, and thus we could see a big decline in oil prices soon. I’m not an expert on oil, so I don’t have any strong views one way or another.

But I would note that oil today is almost as expensive as it was in the early 1980s. It stayed up at these levels for a few years, then it came crashing down and remained relatively cheap from the late 1980s to the late 1990s. The reasons for the big drop in oil prices were simple: the economy became more energy efficient, and world oil production increased. High prices do indeed work to bring prices down over time, though sometimes it takes many years for this to play out.

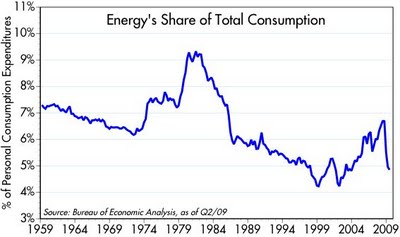

This next chart shows the percentage of personal consumption expenditures that is devoted to energy goods and services. Note that spending on energy was exceptionally high in the early 1980s, when oil was about as expensive then (in real terms) as it is now. Yet today, consumers are spending about half as much of their budget on energy as they were in the early 1980s. This is truly remarkable, and one reason that we are able to spend so much more of our budgets on healthcare.

This next chart shows why it is that energy consumes so little of households’ budget. Simply put, it takes about half as much energy to produce a unit of output today as it did in 1980. Our economy has become far more energy efficient, thanks to technological improvements in fuel efficiency changes in consumers’ buying habits (e.g., smaller and more fuel efficient cars, etc.).

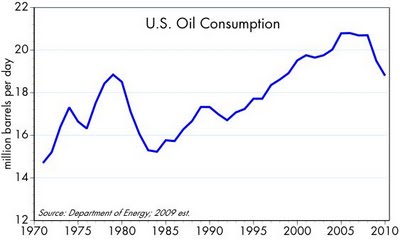

The last chart shows how remarkable all of this is. Despite the fact that the U.S. economy has more than doubled in size since 1980 and the population has increased by some 35%, we consume about the same amount of oil today as we did back then. That’s a truly remarkable fact: U.S. oil consumption has not changed on balance for the past two decades.

This collection of facts tells me a few things.

For one, it will likely be very difficult for the U.S. to increase its energy efficiency as much in the next 20 years as it did in the past 20 years, regardless of whether we impose some form of carbon tax on ourselves. That’s because there is likely a limit to the efficiencies that can be wrung out of oil-based energy technology—surely we have picked much of the low-hanging fruit already.

Two, while energy is still quite expensive in real terms today, it represents a relatively small part of households’ budgets; thus households don’t have as much incentive to become more energy efficient today as they had two decades ago. Thus, a carbon tax might have to be punitive in order to produce the desired effect, and that in turn would have very negative (and politically undesirable) consequences for the economy. Finally, all of this illustrates that the free market is able to respond rather dramatically—given time—when rising prices signal a relative shortage of some key commodity like energy.

Scott Grannis was Chief Economist from 1989 to 2007 at Western Asset Management Company, a Pasadena-based manager of fixed-income funds for institutional investors around the globe. He was a member of Western’s Investment Strategy Committee, was responsible for developing the firm’s domestic and international outlook, and provided consultation and advice on investment and asset allocation strategies to CFOs, Treasurers, and pension fund managers. He specialized in analysis of Federal Reserve policy and interest rate forecasting, and spearheaded the firm’s research into Treasury Inflation Protected Securities (TIPS). Prior to joining Western Asset, he was Senior Economist at the Claremont Economics Institute, an economic forecasting and consulting service headed by John Rutledge, from 1980 to 1986. From 1986 to 1989, he was Principal at Leland O’Brien Rubinstein Associates, a financial services firm that specialized in sophisticated hedging strategies for institutional investors.

Visit his blog: Calafia Beach Pundit (http://scottgrannis.blogspot.com/)

Editor Note: Highly recommend that you take a monday morning visit to Don Vailoux’s monday report where he analyses an astonishing 40 plus Stocks, Commodities and Indexes.

Trading strategies remain the same. Equity and bond prices are not compelling at current prices. Intermediate upside is limited and downside risk is significant (e. 10-15% for major U.S. and Canadian equity indices between now and late this year).

Tech Talk’s Weekly Column in the Financial Post

Why Bother Investing in the U.S.

Canadian investors owning U.S. equities have been sadly disappointed with their performance this year. Currency fluctuations have significantly impacted returns. Although the Dow Jones Industrial Average has gained 11.1% to date in 2009, the Dow Jones Industrial Average in Canadian Dollars has declined 3.4% due to weakness in the U.S. Dollar and corresponding strength in the Canadian Dollar. Should Canadian investors continue to own or buy U.S. equities? That depends partially on the outlook for the U.S. Dollar.

Seasonal influences on the U.S. Dollar

The U.S. Dollar has a history of peaking at the end of April, trending lower to the end of December and moving higher to the end of April. Seasonal trends are influenced by international financial transactions near year end and annual international trade patterns.

Technical influences

The U.S. Dollar has established an intermediate downtrend. A high on the U.S. Dollar Index was established at 89.62 on March 4th. Since then, the Index has taken a series of stair step drops. Its downtrend recently was confirmed when support at 77.43 was broken. Next support is at 75.88. Thereafter, support is at 70.70. A recovery bounce within the intermediate downtrend is likely in the short term. Momentum indicators such as Moving Average Convergence Divergence, Relative Strength Index and Stochastics are short term oversold.

Chart courtesy of StockCharts.com www.stockcharts.com

Fundamental influences

Rising supply and falling demand will lead to a lower U.S. Dollar. The supply of U.S. Dollars is rising rapidly due to an easy monetary policy and a liberal fiscal policy. The U.S. government is literally printing money in order to boost the economy out of its current recession. Meanwhile, the demand for U.S. Dollars is declining. Central banks of foreign countries including China, Japan and the Middle East oil producers already hold large positions in U.S. Treasury bonds valued in U.S. Dollars and have expressed concerns about the plethora of new bonds coming to market to finance the economic recovery. International bond buyers have become increasingly reluctant to add to their positions due to fear that the value of the U.S. Dollar will decline, U.S. interest rates will rise, and bond prices will fall.

What to do

Protect your equity investments against a likely decline in the U.S. Dollar until at least the end of the year. Investment opportunities include ownership of Exchange Traded Funds that are fully hedged against weakness in the U.S. Dollar. Exchange Traded Funds that track gold and gold equities are particularly interesting. Barclays Global Investors, Claymore Investments, Bank of Montreal and Horizon Beta Pro offer a wide variety of fully hedged Exchange Traded Funds that track major U.S. equity indices and commodities priced in U.S. Dollars. Please check their websites for background information and selection.

ETF News

Interesting comments on the harmonization of sales taxes in Ontario and British Columbia in Friday’s Globe Investor! Harmonization could add 8% to management fees in Ontario and 7 percent in British Columbia. Detrimental impacts include:

- Higher costs for investors in Ontario and British Columbia. Given that MERs on mutual funds are much higher than the MERs on ETFs, investors holding mutual funds will be particularly hard hit. Many mutual fund holders will consider the possibility of switching from mutual funds to comparable ETFs

- A decline in institutional interest in Canadian ETFs when comparable investment products are available in the U.S. Institutional investors will gravitate to the lowest cost investment product. Individual investors are less likely to follow because currency conversion costs frequently would more than offset the benefit of a lower MER.

- Volume in ETFs will decline and bid/ask spreads likely will rise as institutional investors move their trades to the U.S.

Mutual fund companies and ETF sponsors are considering the possibility of moving location of their funds to Alberta where no sales tax is charged.

Actively managed ETFs have arrived in the U.S. and Canada. Last week, Harry Dent, a U.S. economist and author known as the “sage of doom and gloom” launched the DentTactical Fund, an actively managed ETF.

In Canada, AlphaPro Management has three offerings and expects to launch 10 to 12 over the next year. According to AlphaPro President Howard Atkinson,”We certainly see an opportunity to build an actively managed ETF family”.

Interesting Comment From CNBC.com

Hirschhorn: Why You May Never Make Money as a Trader

While there are a lot of traders out there, many of them don’t make any money. Well, it’s time for a wake-up call folks. Here are six reasons why you do not — and may not ever — make money as a trader:

You don’t put in the proper amount of effort. You don’t put in the full-time commitment it requires to be profitable in trading because you treat it like a hobby. Trading is not a part-time job. It’s serious business.

Failure to be disciplined and consistent with your process. There’s no excuse for this. It’s all up to you.

Trading like a gambler instead of a trader. You’re taking irresponsible risks rather than thinking in terms of probabilities and trading when you have an edge.

Actually putting on trades without a solid game plan. What are you thinking? You must know your game plan and execute it.

You over think things. Trading is a simple game — up, down, sideways. Keep it simple and make money.

Not trusting yourself to do what you know you need to do. You spend too much time listening to other people. Trust yourself and execute what you know.

The good news: every one of these things is entirely in your control. All you have to do is choose to make things happen.

Following is an excerpt from the IMF announcement on Friday:

IMF to Proceed with Limited Sales of Gold

By Glenn Gottselig

- Sales conducted under safeguards to avoid disruption of the gold marketEssential part of IMF’s new income model

- Gold sale to boost IMF’s capacity to assist low-income countries

The Executive Board of the International Monetary Fund (IMF) has approved the sale of a limited portion of the institution’s gold holdings, stressing that the Fund will conduct the sales in a manner that does not disrupt the international gold market.

The Board approved the sale of up to 403.3 metric tons, or about one-eighth of the Fund’s total gold holdings. The proceeds will help finance a new income model for the IMF, making the 186-member institution less dependent on its lending revenue to cover expenses, which include surveillance of members’ economic and financial policies and other non-lending activities. Part of the money raised will also help boost financing for concessional lending to low-income countries.

“I am delighted that the Executive Board has given its overwhelming backing to limited gold sales to put the financing of the IMF on a sound long-term footing, and to enable us to step up much-needed concessional lending to the poorest countries,” Managing Director Dominique Strauss-Kahn stated. “These sales will be conducted in a responsible and transparent manner that avoids disruption of the gold market.”

Precautions to prevent market disruption

As the third largest official holder of gold after the United States and Germany, the IMF recognizes that it needs to pay close attention to the potential effect of its actions on the gold market. Certainly, unexpected large sales of gold could disrupt the gold market.

The IMF is therefore taking a number of precautions to prevent market disruptions. Importantly, a firm limit on the amount of gold to be sold has been set at 403.3 metric tons, and the gold market has been aware of this amount for some time, as it has not changed since the Executive Board endorsed the new income model in April 2008.

Transparency will play a key role in the gold sales, with the IMF set to inform markets before any sales on the gold markets begin. Prior to any sales on the market, the IMF would be prepared to sell gold directly to central banks or other official sector holders if they expressed interest. These sales to official sector holders would be conducted at market prices, and would shift official gold holdings without changing total official holdings.

Any gold sales on the market would be phased over time, following an approach similar to the one used successfully by the central banks participating in the Central Bank Gold Agreement.

Under this agreement, which was renewed in August, the participants announced ceilings on total sales of 400 tons annually, and 2,000 tons in total during the five years starting on 27 September 2009, and noted that the Fund’s sales can be accommodated under these ceilings.

As a result, on-market gold sales by the IMF will not add to the announced volume of official sales.

Regular external reporting on gold sales will also be provided to assure markets that the gold sales are being conducted in a responsible manner.

Gold equity indices and ETF have a similar technical pattern to gold. Intermediate trend remains up. However, short term momentum indictors (RSI and Stochastics) are showing early signs of rolling over. According to Thackray’s 2009 Investors’ Guide, the period of seasonal strength for gold equity indices ends on September 25th. Technical indicators suggest that the current period of seasonal strength is ending. Investors keying on September 25th should start to take profits. Other investors will want to hold until the end of the next period of seasonal strength in the first week in February.

Silver added $0.23 U.S. per ounce last week. However, short term momentum indicators are rolling over from overbought levels.

Chart courtesy of StockCharts.com www.stockcharts.com

Ditto for Platinum!

Chart courtesy of StockCharts.com www.stockcharts.com

Copper continues to struggle. It slipped $0.06 U.S. per lb. last week and may be forming a modified head and shoulders pattern. A break below $2.66 U.S. per lb will complete the pattern. Short term momentum indicators continue to trend lower. The Chinese have reduced their buying. World inventories are rising.

Chart courtesy of StockCharts.com www.stockcharts.com

Aluminum has a similar technical profile.

Chart courtesy of StockCharts.com www.stockcharts.com

Disclosure: Mr. Vialoux does not own securities mentioned in this report.

Disclaimer: Comments and opinions offered in this report at www.timingthemarket.ca are for information only. They should not be considered as advice to purchase or to sell mentioned securities. Data offered in this report is believed to be accurate, but is not guaranteed.

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

Impossible! That’s what institutional investors say about “Timing the Market”. Mr. Vialoux will explain that, indeed, it can be done with the appropriate analysis. He also will explain why timing the market will be important during the next decade. Buy and Hold strategies are not working anymore; Investors are looking for alternatives. Mr. Vialoux will demonstrate four techniques that can be used to time intermediate stock market swings lasting 5-15 months. The preferred investment vehicles for investing in intermediate stock market swings are Exchange Traded Funds.

Comments in Tech Talk reports are the opinion of Mr. Vialoux. They are based on technical, fundamental and/or seasonal data that is believed to be accurate. The comments are free. Mr. Vialoux receives no remuneration from any source for these services. Comments should not be considered as advice to buy or to sell a security. Investors, who respond to comments in Tech Talk, are financially responsible for their own transactions.

Interesting day in gold market. After umpteen times over several years, the sale of some IMF gold has finally become a reality:

China Said to Consider Buying Gold From IMF, Market News Says

bloomberg.com

“China may purchase some of the 403.3 metric tons of gold being offered by the International Monetary Fund, Market News International reported, citing two unidentified government sources. China will consider the purchase to diversify its reserves if the price is right and the potential return relatively high, the report said, citing one of the sources. There is no indication China is seeking to buy all of the gold on offer, the report said, citing no one. The IMF board approved the sales, valued at about $13 billion, pledging to avoid disrupting the market with the transactions and saying it would “stand ready to sell gold directly to central banks,” according to a statement Sept. 18″…. Full Story

HOORAY! This has been a carrot the gold bears have used numerous times and is now being discounted in the market. Given this fact, a super big commercial short position on the Comex and both bears and correction-calling bulls knocking each other over calling a top in gold, one could have seen a far worse sell-off in gold today. Hmmm. While one day does not make a market, you’ve to ask yourself what this very large group of gold bears and weak bulls will think if by weeks-end, the market is higher than where it started the week? Stay tuned!

Northern Dynasty Minerals saw some buying support as it was added to a key Canadian Index. Coincidentally, I reached out to a Hunter-Dickinson partner to ask about a 1.2 million share block cross on Continental Minerals today and discovered He was in Europe promoting NDM (that also could explain the strength). Mums the word still from HD on KMK in regards to potential suitors. All I can say is KMK is not widely known so big blocks have more importance to me because of that. The fact that the stock traded higher on the day was also a plus.

The more I look at the results of Evolving Gold the more I like the project and the area.

I will be on BNN’s “Market Call” this Friday at 1PM EST.

I look forward to seeing many of you at the Toronto Investment Conference this weekend. Please note I will be hosting a workshop after the conference ends. I especially like these periods as I get to do Q & A and end up speaking to attendees long after the official time is over.

It probably won’t be as bad as the early-1990s commercial real estate collapse.

But local bank and real-estate leaders are bracing for conditions to worsen within the local commercial real estate market that’s already seen Boston’s John Hancock Tower and Waltham’s Bay Colony Corporate Center dumped by owners due to heavy debt, tight credit, and falling building rents and values.

“There’s no way in hell with rents and values falling by up to 50 percent that landlords will be able to get new debt financing,” said Joseph Sciolla, managing director of CresaPartners, a commercial real estate brokerage firm. “They’ll either have to get lots of equity or give the keys back.”

…..read more HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair