Daily Updates

At this point, I am a little reluctant to state this is the final blast-off and that we will not see gold below US$1,000 ever again. Certainly the percentages are with the precious metals investors and it seems gold has nowhere to go but up. As we know, you’re at a level that has been resistance in the past ($1,000), and that area has been resistance for gold for quite some time. And once that level is penetrated for three days in a row then you have a strong probability that the trend is going to continue. In fact, we alerted our subscribers to that very fact!

The biggest caveat is that the big, big picture is very tenuous going forward in the October/November timeframe. The powers that be seem to think that the recession is over, but the facts send a different message. Some of these concerns are as follows:

Confidence in the dollar is all we have left. Almost anyone paying attention knows the dollar has lost over 95 percent of its value. This was addressed by this writer about eight years ago in an article titled, “Dollar Dotcom”.

This faith has probably reached its limit. China, Russia, and some of the Middle Eastern countries have all expressed interest in some alternative to the U.S. dollar. Since in real terms the U.S. economy has been declining for several years, the ability for the U.S. to make good on all of the debt obligations be comes highly questionable.

Credit seems to be contracting at a local level and exploding at a bank/financial institution level, as long as your (bank/institution) is favored by the powers in the government. Have any of you tried to get a loan on your home or apart ment building lately? How about a loan for your small business? Credit is con tracting on Main Street but exploding on Wall Street; this does not yield a strong economy going forward.

The U.S. government seems to be progressing into that legislation that we have kept in mind for almost 30 years—the “Monetary Control Act of 1980.” I hon estly have not read it in many years, but to the best of my memory, this “act” provides the ability to monetize almost anything. Have some confederate cur rency you’d like to swap for some Federal Reserve Notes? The bailout schemes are risking the integrity of the U.S. debt previously issued. This is an area to watch very closely.

Derivatives had a profound influence on bringing the system down and yet most of the derivatives in the system are still “open,” meaning these bets are not resolved at this time and the value of many is highly questionable. Deriva tives pose one of the greatest risks to the entire banking and financial system.

Bank failures continue: the FDIC is broke and the balance sheets of many are of grave concern to investors. It is worth your time to check out the safest banks and limit your exposure!

Real estate problems are far from over, in our view. The Alt-A and even conventional mortgages have rollovers into 2010 and 2011 and are equal in size to the sub prime fiasco. This does not even consider fully what is taking place in the commercial real estate sector.

Social Security is simply a wealth-transfer scheme and I have written about it in the past. With tax revenues down, funding of this program and hundreds of other government obligations can only be funded by more borrowing—but from whom?

One of the questions we are getting quite frequently is . . .

If the recession is over officially, doesn’t that, along with the thousand-dollar gold mark, trigger inflation and suggest getting in now potentially (if you’ve been sitting on the fence about gold)?

Investors are always looking for certain signs or indicators to help with their decision-making process. This is especially true in the technical community, and more people are in the technical community today than probably ever before. That is because you have trade stations and all these software programs that anyone can buy and basically run the numbers and come up with a conclusion that gold is break ing out. However, there are no guarantees on this; it’s only a probability.

Deflation concerns still enter into my thinking. Looking at it as I do from a perspective of the real world, things are not really picking up. Not that there isn’t some of that going on, but it certainly isn’t widespread, and this breakout that we had is not very strong.

The easiest thing to say with conviction is, if you’re not in this market you absolutely need to buy physical gold and silver here. Whether it stays above a thousand or drops below is a moot point. When gold goes to 2,000 or 3,000 or more, if you bought it as it broke through 1,000 and then went back under 1,000 for a while, it might make you sad for a day, a week, maybe a month . . . but it’s going much higher in the longer term. So that’s one thing to keep in mind.

Many ask, how to buy silver? Secondly, it’s the general equity market or the overall health of the financial asset market. The general market has a great influence on the mining shares, at least on a temporary basis. So that could color your view as far as what to do now. Personally, I’d be much more favorable toward buying the physical metal rather than the mining equities at this point.

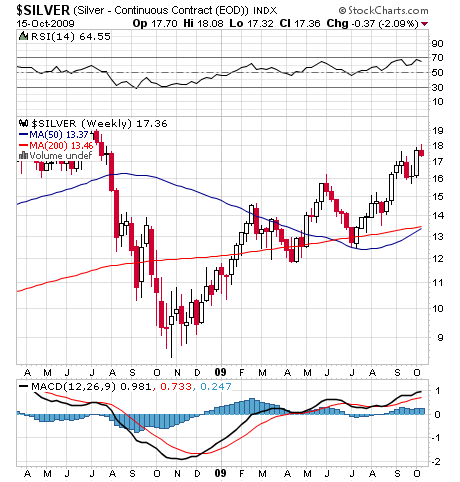

Technically, both gold and silver are overbought. The markets can stay overbought for a very long time and continue to move up and up and up in price, being over bought the whole time. So that doesn’t concern me, as far as will it go higher or not, at this point (October 7, 2009). I do want to advise our readers that, if they’re mak ing a decision on what to do now, be cautious. I’m very, very skeptical of what could happen in the October/November timeframe, so look out ahead.

I was cautious last year through the end of September; that was a good call, except that it wasn’t for a long enough period. If it had been extended through the end of November, we would have gotten back in with our trading portion of the portfolio at the perfect time, in stead of getting back in a bit too early. Regardless, that position certainly made good gains if you were in the correct mining stocks. Take a look at Silver Standard from the November low of 2008 until present time, going roughly from around the five-dollar level to over twenty. Four hundred percent on this company! Compare that with some of the junior mining companies, and not many have had that type of recovery.

Oftentimes, I am criticized for my “conservative” approach of putting serious money into a serious company. At this point, let the facts speak for themselves. No one in this market is perfect, and timing is extremely difficult but we do our best and can probably hold our own against almost anybody. However, this isn’t day-trading—I’m not a real in-and-out kind of a trader. I’m much more a position trader, where big moves down occur and no one wants to buy gold or silver anymore—that’s the time to jump on board and add to your position. Then at these highs (which we may or may not be at right now, time will tell) I’m a little bit more inclined to lighten up.

You want to sell in the strength. Very few people seem to learn that, because there’s a philosophical adherence to gold as money and silver as money, and I hold those views myself. However, I also hold the view that if you can take a profit on part of your position—which is what we do—you might as well take it, because it’s available to you.

The idea is to stay fully invested with roughly 75 percent of your funds, and to trade with about 25 percent. That is a good approach, because if the market just takes off and blasts upward from here, you still have the lion’s share of your investment and have left only 25 percent behind. Shorter-term trading with the 25 percent can make you feel good.

Markets do move quite a bit and they are quite volatile, so when you do catch a nice move in one direction or the other, both can help you weather these long consolida tion periods. That’s exactly what we did the last time we got a huge move up in the gold and silver price—when gold got up to the $1,000 level or actually beyond it and silver at that time was at $21.00.

I would be much more comfortable saying this is the final blast-off if silver were hitting $21.00 right now as gold is trading over $1,000—that would be confirmation in my book, and I’d be very, very bullish. Unfortunately, silver isn’t leading the charge at this time and that is acceptable. It’s certainly shown some good strength this whole year, but not quite the amount of strength I would expect if we were to see all this inflation pouring into the financial markets. Again, I still suspect that there’s probably some more recessionary, deflationary, depression type of news coming.

It is an honor to be.

Sincerely,

David Morgan

Mr. Morgan has followed the silver market for more than 30 years. He wrote the book Get the Skinny on Silver Investing. Much of his Web site, Silver-Investor.com, is devoted to education about the precious metals; it is both a free site and does have a members-only section. Mr. Morgan has just written a free report titled, Silver Fundamentals, Fundamentally Flawed, which can be accessed here: Free Silver Report. To receive full access to The Morgan Report, click the hyperlink.

His name was Dick Baker. Mark Twain called him an old friend and wrote about him in Roughing It (1872). He was the pocket miner of Dead Horse Gulch.

Twain and Baker would wander up in the hills of California, panning for gold. Pocket mining was a specific method in which miners hoped to zero in on the richest deposits “whose vagrant grains of gold have escaped and been washed down the hill,” as Twain wrote, “spreading farther and farther apart as they wandered.”

Sometimes all you needed was to find one spade’s worth of gold. That alone might pay $500 back then. “Sometimes the nest contains $10,000,” Twain relates, “and it takes you three or four days to get it all out.” The pocket miners told tales of finding $60,000… even $120,000 worth of gold, a fortune in those days.

Investing in 2009 is a little like pocket mining: A lot of panning around looking for that worthy payoff. But for the first time in a couple of years, the business of gold mining itself looks attractive, for two important reasons. One has to do with the big picture. The other involves the underlying economics of gold mining, which are attractive even if the price of gold goes nowhere.

As to the first, I’ll be brief, because it’s not the most compelling reason to buy gold stocks in my opinion, yet it’s the one most everyone spends most of their time talking about. It’s that the U.S. government is spending money like there is no tomorrow, which is bound to lead to printing a lot of money (read: inflation) and hence a rising gold price. It’s true, though: You couldn’t draw up a better scenario for gold than what’s going on right now.

Even some sharp-eyed value types – usually buried in the footnotes of their favorite companies, rather than speculating on the price of gold – find themselves drawn to the yellow metal. Indeed, some even seem apologetic about it. “We never thought we would ever buy gold or gold stocks,” writes David Einhorn in his latest quarterly letter to shareholders of his Greenlight Capital.

He talks about his grandfather, who was a gold bug and for the last 30 years of his life bought only gold and gold stocks. Since the age of 10, Einhorn heard warnings from his grandfather about the ravages of inflation and the dangers of the government’s printing press. And of course, for most of those 30 years, gold was a lousy investment. “Being patient is one thing,” Einhorn writes. “Being ‘wrong’ for three decades is quite another.”

Today, Einhorn admits to seeing old Grandpa’s ideas playing out. He’s buying gold and call options on a basket of gold miners.

Behind the bigger picture, though, there’s a more compelling reason to buy gold stocks today. First: The price of gold miners as a group is off more than 20% in the last year, even though the price of gold has held firm. Add to that mix falling mining costs in 2009 and you have a recipe for explosive earnings.

As gold analyst John Doody points out, oil accounts for about 25% of the costs of running a mine. Gold miners use a lot of energy to power big shovels and dump trucks and to haul ore. The price of oil, as you need not reminder, has collapsed. It’s down more than 70% from its high in July. For the first three quarters of 2008, gold miners had to contend with an average oil price around $118 a barrel. Barring a huge rally in oil, gold miners will reap a windfall in lower oil costs oil since then. As I write, oil is $36 a barrel.

Not only will gold miners get the benefit of lower oil costs, the currencies of the gold-producing countries have all fallen against the dollar. This means their costs are lower today in dollar terms. Consider, for a moment, where the gold comes from. In the mid-1990s, four countries dominated gold production and made up more than half of global production. They were Canada, Australia, South Africa and the U.S. But by 2006, these four producers made up only about one-third of global production. Today, you see China produce a lot of gold, as well as Peru, Mexico, Chile and countries in Africa. (This according to Frank Holmes’ book The Goldwatcher. The book, by the way, is a must-have manual for gold investors. Part II, in particular, has a wealth of gold investing strategies and insights.)

Many gold mining stocks today have assets in countries where the currency is falling against the dollar. As Doody says, “All the commodity nation currencies – the Canadian dollar, the Australian dollar, the South African rand, the Brazilian real, the Mexican peso – they’re all up 20-40%. When your mining costs in those countries are translated back into U.S. dollars, they’ll be 20-40% lower.”

Those two factors – lower oil costs and currency effects – mean gold profits should be higher in 2009 than in 2008 even if the price of gold goes nowhere.

I’ll add one other reason to like gold stocks here: They did pretty well in Great Depression I. And history may repeat. Even at their lowest prices in 1933, the stocks of Alaska Juneau Gold Mining and Homestake Mining were still well above their 1929 highs. At their highest prices, they were 230% and 300% higher, respectively.

Old Bernard Baruch was a principal stockholder in Alaska Juneau. It was his largest holding in 1931. Baruch was a savvy old trader and investor. He knew where the soup would stick to the spoon after Roosevelt’s New Deal policies. It would mean a devaluation of the dollar and a rise in the gold price.

Eventually, gold did surge, and so did gold stocks. “Baruch reaped an especially large profit,” his biographer James Grant writes, “for he had been buying stock and bullion.”

Obama’s stimulus plan smells a lot like Roosevelt’s New Deal. And if this is the greatest financial test we’ve faced since the Great Depression – as I believe it will ultimately be – then gold stocks may also be among of the few stocks to make new all-time highs in 2009.

If Twain were still kicking, I think he’d go look for his old friend Dick Baker, the pocket miner of Dead Horse Gulch, and head for those California hills.

Joel’s Note: Want all of Chris Mayer’s best research for a buck?

Well, here it is: A no muss, no fuss offer to test drive Mayer’s Special Situations for one month…for a single dollar.

Here is a link directly to the sign-up page.

About Mayer’s Special Situations

Everybody knows that making bigger profits means taking bigger risks. That’s why conservative investors avoid promises of super-sized gains.

But Chris Mayer, the value-minded genius behind Capital & Crisis, is working hard to change that myth. His Mayer’s Special Situations is dedicated to taking you to the edge of risk-versus-reward.

You’ll be surprised how easy it is to enjoy speculative gains without giving up your conservative investment values. Chris only recommends buying stocks with “special situations” — rare events like stock spin-offs, buybacks, turnarounds and much more.

Most investors don’t understand how these things work — or how lucrative they could be. And that gives you a chance to swoop in and buy shares at a bargain-basement price.

Even better, because these are simple stock plays, you never have to worry about taking on too much risk or making complicated plays. And if you think it’s a slow path to profits, guess again. Mayer’s Special Situations readers have watched stocks soar 106% in eight months… 132% in four months… 194% in 13 months… and more!

If you don’t know Chris Mayer’s work, you’re missing out one of the best analysts working today. His essays have appeared on a number of Web sites and publications, including The Mises Institute, the Freeman, The Daily Reckoning, GoldEagle.com, LewRockwell.com, FiendBear.com, PrudentBear.com, Grant’s Investor and Individual Investor Magazine. His views on financial matters have also been widely quoted, including in the highly regarded Grant’s Interest Rate Observer.

With his help, you’ll never miss a single winning Special Situation.

Today I offer you an insightful look at China’s real estate market – a “burgeoning bubble” that deserves a close eye as the possibility for breaking increases. Remember the chaos in Japan after their own housing dreamscape got violently yanked back to earth? As investors, we have to recognize opportunities – and know what to avoid. With a global economic crisis – and now surging housing prices in China – investors in any global market need to keep watch on political and economic developments around the world.

Today’s analysis comes courtesy my friends at STRATFOR, a global intelligence company. They provide unique and on-the-money analysis and forecasts on all things global, essential for any alternative investment strategy. They’ve got a free newsletter as well, for which I encourage you to sign up by clicking here – so you’re not limited to my caprice.

John Mauldin

Editor, Outside the Box

![]()

Summary

The real estate market in China, particularly the residential side, is a burgeoning bubble that is growing bigger and more breakable by the day. Land and housing prices were already rising steadily when Beijing’s stimulus package hit the sector in early 2009. Now prices are surging, with developers, bureaucrats and investors cashing in while urban Chinese – once encouraged to invest in home ownership by the central government – become less and less able to buy.

Editor’s Note: This analysis is part of a series that explores China’s industry, finance and statistics.

Analysis

Related Special Topic Page – The China Files (Special Project)

On Sept. 10, China Overseas Land and Investment, a Hong Kong-listed company and a subsidiary of state-owned China State Construction Engineering Corp., purchased a prime piece of real estate in the Putuo district in downtown Shanghai. The company paid 7.006 billion yuan ($1.026 billion) for the undeveloped property, which will amount to an average of 22,409.3 yuan ($3,283.9) per square meter of floor space (just in land costs) once the designed residential building is constructed.

The purchase created China’s newest “land king,” a term for the real estate developer who pays the highest price for a piece of real estate during a land auction. And 7.006 billion yuan was the highest price ever paid for a piece of Chinese real estate for any purpose – residential or commercial. The milestone is a result of an increasingly intense competition for land in major cities that began early in the year, when Beijing began distributing stimulus money to various industries – including the real estate sector – to sustain the economy. As a result, land prices have soared throughout China. And with increasing speculative investment in residential real estate, the market faces a surging bubble that jeopardizes the country’s long-term economic development.

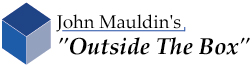

Since 1998, real estate investment in China has accounted for more than 10 percent of the country’s gross domestic product (GDP), compared to only 3 percent to 5 percent in the United States. Such investment is also closely associated with many other industries, such as construction and finance, and it provides an abundance of jobs. Therefore, it is seen as a critical pillar of China’s economy and enjoys favorable policies from the government and state-owned banks (more than 70 percent of real estate investment in China comes from bank loans). At the same time, real estate developers, local government officials and investors have escalated housing prices across the country by acquiring massive land holdings, limiting the supply and inflating prices, creating a real estate bubble that is not sustainable in the long run.

The bubble has grown mainly on the residential side of the market, where there is more demand and higher profits to be made. However, while fewer developers and investors have been chasing nonresidential projects, Beijing’s 4 trillion yuan ($586 billion) stimulus package in early 2009 has generated more interest and activity in the commercial side. Indeed, there are signs that commercial real estate may also be headed for a bubble, and STRATFOR will be watching the situation closely.

Origins of the Bubble

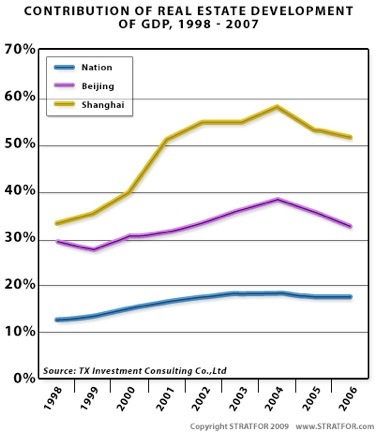

Since 1978, China’s pace of urbanization has increased dramatically, with the number of middle-size and large cities (those having nonagricultural populations of more than 200,000) growing rapidly. Beginning in 1985, economic reforms implemented in urban areas to make China’s planned economy more market-oriented added even more momentum to the real estate boom, with real estate investment increasing by 71 percent by 1987. The government’s macroeconomic policy of monetary belt-tightening helped cool this overheated market, which was further tempered by the government’s continuing to provide housing for state employees (fu li fen fang, or “welfare housing”).

However, when the state significantly cut back on its welfare housing program in 1998, the Chinese perception of personal property changed, and this would have an important impact on the real estate sector. The government began this privatization process by making a private dwelling a “commodity” and granting the purchaser the right to own a newly built house for 70 years. (Likewise, the developer who buys the property on which residential or commercial buildings are to be constructed may own that property for 70 years.) Home ownership in China could now be a sound financial investment.

Thus, the residential real estate market would boom in almost every urban area in China – and particularly in the “first-tier” and “second-tier” cities (only Beijing, Shenzhen, Guangzhou and Shanghai are in the first tier, with more than 20 cities, and mostly provincial capitals or coastal ports are in the second tier). But rising land prices would eventually put housing prices out of reach for the general public. In Dongguan, a coastal second-tier city in Guangdong province, land prices averaged 4,957 yuan ($726.42) per square meter in 2007, a more than 500 percent increase from 2003, while personal disposable income increased 24 percent during the same period (from 20,526 yuan [$3,008] to 27,025 yuan [$3,960] per year).

A 2006 survey conducted by the National Development and Reform Commission showed that the average ratio between housing prices and income was approaching 12:1 in many large and middle-size cities in China (in Beijing it had reached 27:1). Twelve to one is significantly higher than the World Bank’s suggested affordability ratio of 5:1 and the United Nations’ 3:1. The problem was compounded by the fact that, of the more than 80 percent of Chinese who owned their own homes in urban areas (generally considered cities with populations of more than 20,000), 54.1 percent were making monthly mortgage payments that constituted 20 percent to 50 percent of their monthly incomes.

The Recovery Bubble

Following a temporary drop toward the end of 2007, land prices rose steadily, then began surging again with Beijing’s stimulus package and a flood of easy credit in 2009. With much of this money flowing into the real estate sector, major beneficiaries included large state-owned enterprises (SOEs) involved in speculative real estate and housing investment, contributing to the inflating bubble. Among the 10 highest-priced land purchases in major cities in the first half of 2009, 60 percent went to SOEs.

Paradoxically, as the global financial crisis continues, China sees little choice but to loosen its monetary policy even further, fearing the opposite would curtail economic growth and result in massive unemployment, which could lead to social instability. Beijing knows that one of the country’s underlying economic problems continues to be an overheated real estate market, but it also knows that the real long-term solution – limiting the flow of cash and credit – could have dire socio-economic ramifications. Meanwhile, real estate developers, government officials and investors continue to speculate on real estate, raising land and housing prices.

As housing prices continue to rise, a parallel trend is manifesting itself – rising vacancy rates in urban areas. A 2009 report by the Shanghai Yiju Real Estate Research Institute revealed that, by the end of 2008, the average vacancy rate for “commodity housing” (as opposed to welfare housing) in Beijing was 16.64 percent, and vacancies reached as high as 30 percent in some districts. Most of these vacant houses, however, are not unsold ones. They have been purchased by investors as speculative investments. While there are fewer and fewer ordinary people who can afford to buy houses, there is still excessive demand for investment housing – pressure that continues to drive up the prices.

This closed loop in the Chinese real estate market is facilitated by the country’s political and bureaucratic system. In China, all land is initially owned by the state, and local governments have the sole authority to sell it. And income from property taxes and land sales are a primary source of revenue for local jurisdictions. According to estimates by the State Council’s Development and Research Center, tax revenue from the land in some jurisdictions accounts for 40 percent of the local budget. Moreover, net income from land sales accounts for more than 60 percent of the local governments’ extra-budgetary revenue. The soft budget and lack of accountability to the people reinforces the local governments’ incentive to expand their real estate investments without much concern for cost or impact on public services.

Economic performance also is the prime prerequisite for bureaucratic advancement, which gives local officials the incentive to generate as much revenue as possible through land auctions. And this generally involves a level of collusion – and corruption – among government officials, real estate developers and investors.

One typical strategy is for a developer to buy a big chunk of urban land from the local government but leave the land undeveloped, or build on only a small portion of it, thereby keeping the housing supply limited. Despite various state policies to lower land prices in order to make homes more affordable, local government officials and real estate developers control the land auctions. When a lower sale price is dictated from above, it is easy enough for the local sponsors to officially deem the auction a failure. Even when the developer does build houses on the property, a speculative investor, working hand in hand with the developer and government officials, can bribe both parties to ensure that he can buy all the houses at a low volume price and keep them off the market, thereby maintaining a limited supply and high prices.

Another factor that enters the equation is a cultural one. The Chinese people generally prefer to buy new houses, as opposed to renting homes or buying secondary houses in which people have already lived. Indeed, in urban areas, marriage proposals often include a promise to buy a new commodity house. As a result, the secondary housing market remains very small in comparison (due also to fewer available bank loans for lived-in houses and the complicated process involved in transferring ownership).

All of these factors contribute to the burgeoning real estate bubble – and make it difficult to predict when that bubble will burst. With 70 percent of real estate investment in China coming from bank loans, a dramatic drop in land values could send shock waves throughout the economy. There are already signs of decline. In Shenzhen, one of China’s first-tier cities, real estate prices have been dropping for the past two years (30 percent for housing), and many developers and speculators have suffered great losses. The threat looms in other large cities such as Beijing and Shanghai and may be emerging in many second-tier cities as well.

Given the current global economy and the economic balancing act it must maintain domestically, Beijing has few good choices. It must keep enough cash flowing to maintain economic growth and social stability in the short term while tightening credit to avoid a tsunami of bad loans and a market collapse over the long term. Certainly, Beijing does not want to face the kind of collapse in the housing market that Japan experienced in the 1990s, which triggered a financial crisis and more than a decade of economic malaise.

But in China’s real estate, as in most sectors of this vast and complex land, implementing and enforcing prudent regulation has never been an easy task

John F. Mauldin

johnmauldin@investorsinsight.com

Stratfor has a free newsletter as well, for which I encourage you to sign up by clicking here

John Mauldin reads hundreds of articles, reports, books, newsletters, and anything that stirs up his thought process each week.

Outside The Box is his weekly letter that highlights the one essay from another analyst that will stimulate your thinking.

John will not agree with all the essays, and some will make us uncomfortable, but the varied subject matter will offer thoughtful analysis that will challenge our minds to think Outside The Box.

To subscribe to this weekly newsletter and Thoughts from the Frontline, both free letters, please go HERE.

STRATFOR is the world’s leading online publisher of geopolitical intelligence. Our global team of intelligence professionals provides our Members with insights into political, economic, and military developments to reduce risks, to identify opportunities, and to stay aware of happenings around the globe.

STRATFOR provides three types of intelligence products:

Situational Awareness – News is a commodity that you can get anywhere on the Internet. Situational Awareness is knowing what matters, and an intelligence professional’s responsibility – STRATFOR’s responsibility – is to keep you apprised of what matters without wasting your time with clutter. We provide near real-time developments from street revolutionary movements to military invasions. OJ’s latest arrest and mudslinging in Washington and Brussels don’t make the cut.

Analyses – STRATFOR tells its Members what events in the world actually mean. We also tell you when events are much ado about nothing. Oftentimes the seemingly momentous is geopolitically irrelevant and vice versa. We discern what’s important objectively – without ideology, a partisan agenda, or a policy prescription.

Forecasts – Knowing what happened yesterday is helpful; knowing what’s going to happen tomorrow is critical. STRATFOR’s intelligence team makes definitive calls about what’s next. These aren’t opinions about what should happen; they’re analytically rigorous predictions of what will happen.

STRATFOR provides published intelligence and customized intelligence service for private individuals, global corporations, and divisions of the US and foreign governments around the world. STRATFOR intelligence professionals routinely appear at conferences and as subject-matter experts in mainstream media. STRATFOR was the subject of a cover-story article in Barron’s entitled The Shadow CIA.

STRATFOR was founded by Dr. George Friedman in 1996. STRATFOR is privately owned and has its headquarters in Austin, TX.

MARKET WRAPUP

The Dow closed above the 10,000 market for the first time in a year, October 3, 2008 was the last time the Dow was at 10,000. The media are certainly going to town on this news but it is, in fact, old news; it’s only the 26th time the Dow has managed to cross this milestone.

Much was made over the Intel beat but INTC was up 0.34 cents to $20.83 (1.66%), so that was hardly the lone catalyst.

This still seems to be a purely technically driven market, though excitement continues to build over a company’s ability to surpass low-balled expectations on earnings and revenues. This next up-leg may be the last gasp, but the strength could carry it to the 1,098 gap or the 1,121 50% Fibonacci retracement (that’s 3% more).

U.S. RETAIL SALES CAME IN BETTER THAN EXPECTED

….read more HERE.

In my September 9 Money and Markets column I showed you this gold chart:

On that date, I said, “This breakout of a huge triangle is a clear technical buying signal.” I added that the minimum price target of this triangle formation was roughly $1,100. This was well above major resistance in the $1,000 area, thus hinting that another major breakout and buying signal would take place soon.

Well, that’s exactly what happened last week!

Gold Hit 1,059 …

Triggering Another Major Buy Signal

Take a look at the weekly chart below. It gives you a good perspective of how important this breakout to new high ground actually is. As you can see, it signals the end of a medium-term correction that began in March 2008 and the beginning of the next medium-term up trend of a secular bull market that started in 2001.

The minimum price target of this huge consolidation pattern is $1,300. And I believe much larger gains are certainly possible.

Also consider this: Four weeks ago the Hulbert Gold Newsletter Sentiment Index (HGNSI) stood at 25.2 percent. Now, four weeks later and gold nearly $100 higher, the HGNSI has actually fallen to as low as 18 percent! A rising market accompanied by a declining number of bulls is a rare development. And it’s clearly bullish.

Longer Term Fundamentals

For Gold Are Very Bullish, Too

Besides the technical buying signals I’ve given you today, I want to repeat the major fundamental arguments for owning gold:

- As a consequence of the current financial and economic crisis, government debt is going through the roof — not just in the U.S., but all over the world.

- Worldwide central banks are printing money like there is no tomorrow.

- Gold demand is rising due to wealth creation in emerging economies where gold still plays a large role as a store of value.

- Gold demand is even rising in the West as more investors doubt the wisdom of central banks and governments.

- Gold supply is stagnating or even slightly shrinking — despite the metal’s price rise since 2001. This is because it’s getting ever more difficult and expensive to get gold out of the earth.

- Finally, central bankers who were eager to sell government gold at much lower prices a few years ago, are getting increasingly reluctant to keep doing so. Emerging market central banks are even buying.

As long as most of these catalysts for higher gold prices remain in place, I expect the long-term bull market to continue. And much higher highs are very likely.

Best wishes,

Claus

Claus Vogt’s Page »

Claus Vogt is the editor of Sicheres Geld, the first and largest-circulation contrarian investment letter in Europe. Although the publication is based on Martin Weiss’ Safe Money, Mr. Vogt has provided new, independent insights and amazingly accurate forecasts that, in turn, have contributed great value to Safe Money itself.

Mr. Vogt is the co-author of the German bestseller, Das Greenspan Dossier, where he predicted, well ahead of time, the sequence of events that have unfolded since, including the U.S. housing bust, the U.S. recession, the demise of Fannie Mae and Freddie Mac, as well as the financial system crisis.

He is also the editor of the German edition of Weiss Research’s International ETF Trader, which has delivered overall gains (including losers) in the high double digits even while the U.S. stock market suffered its worst year since 1932.

His analysis and insights will be appearing regularly in Money and Markets.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair