Daily Updates

Ed Note: Selling covered calls and selling puts has always been one of Michael Campbell’s favorite Strategies.

Writing covered calls is one of my favorite ways to generate additional income from stocks already owned, especially if they also pay dividends. That’s because you basically get two cash flows from one stock — without adding any additional downside risk at all.

However, if your goal is collecting additional income without having to sell the underlying shares, the ongoing run-up in share prices hasn’t provided an ideal environment for writing covered calls.

That’s why today I want to talk about another options strategy that can also generate income without undue risk. As you’ll see, this approach is perfect for anyone who wants to get into new positions without “chasing” rising share prices …

Why Going Naked Doesn’t

Always Leave You Exposed!

The strategy I want to talk about today is writing naked puts.

Now, whenever the subject of options comes up, I always stress the fact that investors should avoid writing naked calls. That’s because doing so exposes you to unlimited risk.

However, writing naked puts is a completely different ball of wax.

To see why, let’s recap the general subject of writing options.

When you write a covered call, you already own 100 shares of stock. And you don’t expect the shares to go up substantially over the short term.

So you basically offer another investor the opportunity to buy your shares — at a much higher price than the current rate — during a set amount of time into the future.

In doing so, you collect a nice little premium … which is yours to keep no matter what happens next.

As for consequences, your best-case scenario is that the stock never goes above the price of the options contract you sold. You get to keep the stock (and related dividends) as well as the premium from the covered call.

The worst case is that you have to sell your stock at the contract’s strike price — profiting from both the upside and the premium collected, but missing out on any additional gains beyond the contract’s strike price.

In contrast, if you sell an investor the right to buy shares of stock from you without owning them already, you’re writing an “uncovered” or “naked” call.

And in the event of a massive move up in the underlying stock’s price, you could find yourself losing a lot of money in a hurry. That’s because you’d have to go out and buy the shares at the current price to fulfill your obligation under the options contract.

The critical difference is that PUTS give investors the right to SELL shares at a specific price during a stated time period.

Therefore, writing a naked put is almost like the reverse of writing a covered call …

Options are always in demand, so writing them is a great way to collect income!

You are essentially telling someone that you’d be willing to buy their shares if they fall to a certain level.

The investor buying your “insurance policy” is hedging against potential downside.

And you’re collecting a nice premium upfront!

In short, naked put writing is yet another solid way to get income from options trading.

However, the key here is that you must be ready to take ownership of the underlying stock, too!

As with all options contracts, a naked put covers a round lot of stock, or 100 shares.

So let’s say you want to buy 100 shares of XYZ stock, but you think it’s overpriced at today’s level.

Well, instead of placing a good-till-cancelled limit order with your broker — or watching the ticker tape relentlessly for weeks on end

— you could write a naked put near your buy price instead.

Then, if the stock falls to that level (or below it), odds are very good that the contract holder will “put” his shares to you. And since you also get to keep the options premium, you’ve actually gotten them a little cheaper than you expected!

Alternatively, if the stock doesn’t reach your strike price during the life of the contract, you keep the premium and are free to write another put.

If you keep pursuing the same strategy, you could really make a lot of money just for waiting around!

Of Course, There Are a Couple Things You

Need to Know Before You Write a Naked Put …

First, you could start off with an immediate paper loss when you take possession of your shares.

Second, those losses could be substantial if the price implodes.

Third, you must have enough cash in your brokerage account to cover the potential stock purchase under the put contract.

For all these reasons, I consider naked put writing a bit riskier than covered calls. But in this rising market, it can be a great approach when done correctly.

For more information on the strategy, the Chicago Board Options Exchange website is a great place to start.

Best wishes,

Nilus

Richard Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe.

Richard has been Bullish Gold since below $300. He also loaded up on bonds in the early 80’s when US Treasuries where yielding 18%+. A 30 year bonds through compound interest would turn $1,000 into $300,000 at maturity. (include reinvestment of interest income, which Richard does as his view is compounding interest is the ROYAL ROAD to RICHES)

Many years ago, when I was still living in NYC, I had a subscriber, a Swiss man named Jay Pfister. Jay owned a chemical company. During the early 1930s Jay sold his company to American Cyanamid. That sale made Jay quite wealthy, and he had a home in NYC and one in La Jolla. It was Jay who first told me about La Jolla. Jay suggested that I leave Manhattan and enjoy “a better life” in La Jolla. I thought a lot about Jay’s advice. In 1961 I followed his advice, and it proved to be one of the best pieces of advice I’ve ever received.

One day I met Jay at the Plaza Hotel on 59th Street. We were sipping coffee, when Jay said, “I want to tell you an interesting story. My apartment overlooks the Hudson River. Last Sunday I was looking out over the Hudson, and I saw two large boats heading towards each other. They continued to close in on each other, and I said to myself, ‘This is ridiculous’. The captains must be drunk. If they continue on this path, they’re surely going to crash.”

I looked wide-eyed and asked Jay, “So what happened?”

Answered Jay, “The ‘impossible’ happened. The two boats continued toward each other, and they crashed.”

I never forgot that story. And I apply it to the current economic situation in the US. America has created, according to the experts, 50 to 100 trillion of dollars in unfunded liabilities including Social Security, Medicaid, money spent for stimulus, money promised for future Federal construction plans. The arguments and warnings are that if the US continues to spend in this manner, the dollar will collapse and the nation will be broke. Impossible, you say, but then I think of Jay Pfister’s story about the two boats.

And the question I ask myself is this — will our vote-sensitive politicians have the guts to do what’s necessary to save the nation? This will mean that for the first time since World War II the US will have to cut back and live within its means. I try to envision how this will happen and what it will be like, and I really have trouble envisioning it.

Here’s what I think will happen. Before the potential catastrophe actually occurs, the markets will sound the alarm. The dollar will lose its reserve status, and the US will sink into a serious slump. If the dollar becomes an unwanted currency, fiat or central bank-created currencies (all are currently backed with dollars) all over the world will cave in. The knowledgeable money will rush to the only money that cannot go bankrupt — gold. The panic for gold will be unprecedented, and new currencies will have to be created. To have any authority, the new currencies will have to be backed by gold. In the panic to buy gold, the metal will rise to undreamed-of heights.

Question — Russell, if there is a stampede to buy gold, how do you think it will start?

Answer — If there’s a panic to buy gold, I think it will start in China, aided by other Asian nations and probably by Russia. I think China seriously doubts that the US will cut back and do what has to be done to save the dollar. Therefore, I believe China is on a path of accumulating as much of the world’s gold as possible (they’re doing the same thing with rare earths). At some point, the Chinese renminbi will be seen as the world’s strongest currency. The Chinese will then partially-back the renminbi with gold, at which point the renminbi will be the world’s new reserve currency. The dollar will be an unwanted “has-been.” I’ve said many times that the Achilles Heel of the US economy is the dollar and its reserve status. The Chinese know that very well.

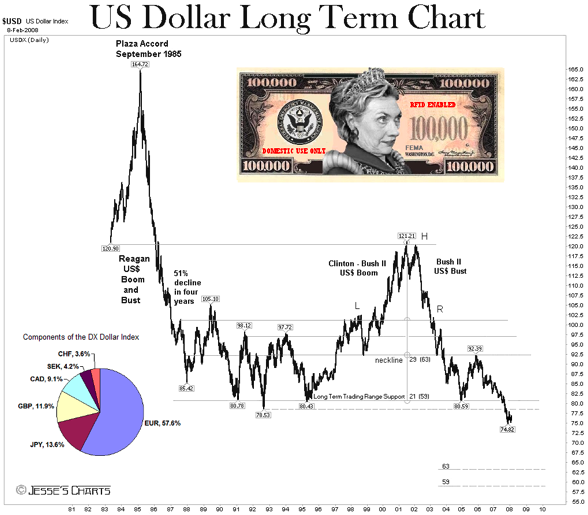

Bigger Chart HERE.

Bigger Chart HERE (since only 1982)

Richard Russell

Ed Note: Saturday Night Live skit last Saturday of Obama Jintao (Warning, its a bit racy).

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold. There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Ed Note: Below is a small excerpt from Mark Leibovit’s 12 page The VR Gold Letter with a trading recommendation from the VRPlatinum Newsletter Letter.

A bigger rally in the U.S. Dollar Index may be underway. I have mixed feelings about this issue. Sooner rather than later I believe Gold and the U.S. Dollar Index will diverge from their current inverse relationship. We have seen this happen on several occasions already. In the meantime there remains the risk that such a rally could trigger a correction (in Gold) of unknown proportions which we would have to monitor day to day.

Gold could still become quite explosive to the upside at any moment. I have still have an unfulfilled upside target of 1300 based on the previously displayed reverse ‘headand-shoulders’ pattern, the fact that most investors (maybe 5% in the U.S.) are in the Gold market and the fact that there is still near universal skepticism regarding the efficacy of its advance. My $3000 upside target for the long-term still stands and it is always possible we could see prices even much higher. Should a correction unfold, current downside risk is back to the 1070 area.

Under 1020-1030 I would get concerned that a bigger top (not permanent) would be in place. All we can do is take one day at a time. We’ve seen sharp corrections in Gold before and we know there is significant government manipulation in this market (see last week’s newsletter or go to HERE. For now, my belief is that should a decline unfold, it would be temporary.

Update via VRPlatinum Daily Newsletter Precious metals rallied to new highs yesterday morning as the Dollar fell and tensions between Iran and the west escalate. But the metals pulled back from their morning highs in the afternoon, though they still closed with nice gains. Gold was up 13.20 to 1164.10, its seventh straight up day, and set a new all time record high of 1174.60 yesterday morning. Silver was up just 0.07 to 18.58, but set a new recovery high of 18.95. Platinum was up 10 to 1455 and hit a new recovery high of 1482. Palladium was up 9 to 370 and set a new recovery high of 382.

We took trading profits yesterday in our Gold index positions with a view to re-enter on a retracement. Platinum subscribers stay tuned.

Take a moment and read the following Reuter’s news story proclaiming that banks to be net buyers of gold ahead which is something I have written about for many years. This will certainly change the complexion of the gold market. I also still subscribe to the view that we’re in a 20 year up cycle in gold (chart in the November 9 edition of the VR Gold Letter):

BlackRock says c.banks to be net buyers of gold

SYDNEY (Reuters) – Central banks will be net buyers of gold this year as they diversify away from the U.S. dollar, marking a reversal of a decades-old trend, global commodities investment fund BlackRock said on Monday in comments that helped drive bullion to fresh record highs.

Investment in gold by central banks has picked up recently, with India buying 200 metric tons from the International Monetary Fund, and Taiwan’s central bank is studying whether to raise the amount of gold in its forex reserves, with China and South Korea also debating the issue.

BlackRock is one of the world’s largest fund managers, boasting a total $1.4 trillion under management across all asset classes. It is manager and adviser to the U.S. Federal Reserve and its views can influence the direction of global markets.

Evy Hambro, who runs two of the world’s largest commodities funds, BlackRock World Mining Fund and Gold & General Fund, gave an upbeat outlook for gold during a media briefing in Australia.

His forecast for net central-bank purchases of gold this year would, if met, mark the first year in two decades when the world’s central banks bought more gold than they sold. They have been net sellers each year since 1988.

Gold stored in central banks worldwide has dropped more than one-sixth since 1989.

“The most recent break-out in the gold price in U.S. dollars has caused most gold prices to start trending higher at the same time,” Hambro said, adding that investors were now looking for gold to rise in other commodities as well as U.S. dollars.

“When you start to see the price rising in a range of different currencies, it is a clear sign of a very strong market to come,” he added.

Spot gold stood at $1,123.70 by 9:16 p.m. EST after touching $1,126.30 per ounce, a record, versus the notional New York close of $1,118.50, helped higher by Hambro’s bullish outlook, according to financial broking group IG Markets.

Bullion has been on an upward spiral as a hedge against the U.S. dollar’s weakness and rising inflation risks, traditional reasons to lap up gold.

Based on the dollar index of major currencies, the U.S. dollar has dropped 7.5 percent this year versus a 33 percent rise in the U.S. dollar gold price.

In other currencies, gold has not reached new highs since early 2009. In Australian and Canadian dollars and the South African rand, it peaked in February.

But Hambro said investors were now “looking for price rises across all currencies” as central banks built up their gold holdings and global supplies tapered off.

“Gold’s role is gathering a lot more attention in terms of risk diversification,” he said.

By 1999 central bank selling was so commonplace that the big European banks signed a pact capping sales at 400 metric tons a year to keep the price from collapsing.

It worked. Gold has gone up just about every year since.

Hambro also said the high level of gold production in China, which has replaced South Africa as the world’s biggest producer, was not sustainable, pressuring world supply.

China’s output rose 13.49 percent in the first half of 2009 from a year earlier to 146.505 metric tons, according to the Ministry of Industry and Information Technology.

China is widely assumed to be buying domestic gold production after revealing in April it held 1,054 metric tons of gold, a jump of 76 percent from its last word on the subject six years earlier.

The Reserve Bank of India last month bought 200 metric tons of gold from the International Monetary Fund, and Sri Lanka’s central bank governor told Reuters this month his bank had been buying gold for the past five or six months.

But not all banks are trading foreign currencies for gold.

Korea has the world’s sixth largest foreign exchange reserves but ranks 56th in terms of gold holdings. Its governor has said it would not be easy for the bank to suddenly increase gold holdings because of the market impact.

Japan has kept its gold reserves steady at 24.6 million troy ounces since mid-2001. The Royal Bank of Australia has not bought any gold since selling two-thirds of its reserve in 1997.

Hambro also said U.S. demand for commodities was starting to show signs of recovery. This, along with stronger Asian demand, set the stage for a prolonged bull market, he added.

This small excerpt was from Mark Leibovit’s 12 page The VR Gold LetterThe VR Letter is published WEEKLY and Mark Leibvit has been the Awarded #1 Gold Timer by Timers Digest in 2007, 2008 and is in postition to win 2009 with his fine Gold forecasts throughout the year so far including Gold zooming to another new High of $1,131 in tonights overnight trading. Money Talks highly recommends subscribing to Mark’s Gold

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

My boss emailed me this afternoon telling me the former governor of the Bank of Canada, David Dodge, was in Montreal. He asked me whether I would like to go listen to his speech and I immediately jumped at the opportunity.

David Dodge is one of the smartest people in finance and listening to him speak was a real treat. If I were running a big global macro hedge fund, I’d hire him as a senior advisor. His knowledge of economics and global economic issues is deep and comprehensive.

Mr. Dodge was the guest speaker at CIRANO. His presentation was entitled “Emerging from the Crisis: the Fiscal and Monetary Policy Challenges Ahead”.

He began by going over the origins of the crisis, paying close attention to global imbalances, financial market innovation and underpricing of risk.

He then discussed how central banks and governments dealt with the crisis through liquidity provisions and government bailouts. He emphasized that automatic fiscal stabilizers accounted for over 50% of the fiscal deficits and that it wrong to think that the bailouts were the only driving force behind mushrooming fiscal deficits.

Mr. Dodge then listed four factors driving the economic rebound (he did not call it a recovery but a rebound):

1) reversal of inventory cycle

2) huge fiscal stimulus

3) extraordinary low interest rates

4) house price stabilization

And he listed two factors driving the financial rebound:

1) pessimism of last winter was overshot

2) extraordinary liquidity provision by central banks

According to Mr. Dodge, the rebound has come one or two quarters earlier than predicted last winter because of the size and speed of coordinated monetary and fiscal policy. The global economic contraction in 2009 now seems likely to be only 1% 9versus 2% last winter). Growth in 2010 now likely to be 3% (versus 2% last winter). Inflation is well contained.

But Mr. Dodge warned that private demand is still weak, household balance sheets in OECD remain problematic, and unemployment still to peak in 2010.

As far as the global financial system, Mr. Dodge said catastrophe was averted in 2009 but a substantial “hangover” remains:

- government ownership of financial institutions

- huge government deficits and high debt

- central banks expanded balance sheets

- securitization very weak and bank credit tight

- And rebuilding of the system still to come

On the last point, Mr. Dodge notes that banks starting to rebuild capital with steep yield curve, substantial investment banking profits and equity issues. Risk management models are being recalibrated and “derisking” process underway. But he noted that little progress yet on reform of financial instruments and markets.

In particular, he noted the following key issues for market regulators:

- standardization of instruments

- building of continuous markets

- regulating credit default swaps

- need to develop a sustainable private mortgage market

- need to harmonize accounting standards

Mr. Dodge then got to the core of his presentation, the fiscal outlook, noting the following:

- In 2007, Canadian federal and provincial bugets show a small surplus (1.3% of GDP)

- Big reduction in net debt to to about 52% of GDP

- Favorable terms of trade led to stronger nominal income growth (2002-2007)

But the global financial crisis dealt a severe blow to government revenues and automatically increased some expenditures. Moreover, governments undertook stimulus spending. The combined Canadian federal and provincial deficit in 2009-10 rose to about 6% of GDP, with slightly more than half of this increase due to automatic stabilizers. The comparable deficit in the US was over 10% of GDP.

In his fiscal outlook, Mr. Dodge went over several factors affecting future spending:

- Assume temporary programs expire more or less as scheduled in 2011/12

- Spending programs then largely driven by changing demographics

- Health care costs continue to increase driven by aging (6%+)

- Elderly benefit costs set to increase

To restore fiscal balance, Mr. Dodge says it would require discretionary fiscal action of roughly 3% of GDP (federal plus provincial). If all is done on spending side, program spending growth would have to be constrained to below 3% (nominal) and all temporary spending eliminated.

Restraint of this magnitude is very difficult and disruptive so some tax increases will be necessary.

To cut spending by 1 1/2% (1/2% of GDP per year), Mr. Dodge said you need to:

- hold real capita spending to 1% growth p.a.

- cut other real spending on other programs by 2% p.a.

To raise revenues by 1 1/2% of GDP by 2014-15, Mr. Dodge noted that you need to:

- raise the harmonized sales tax (HST) by 2%

- some form of carbon tax

- raise user charges (eg. student fees)

Mr. Dodge ended with the implications for monetary policy:

- Hold interest rates at zero ’til mid 2010 but reduce non-conventional initiatives

- With credible fiscal plan, policy can remain accomodative through 2015, i.e. slow increase in policy rates to 2% (zero real) in 2010-2011 and hold below “neutral” through remainder of period to compensate for fiscal drag and continuing (small) output gap

And finally the implications for global policy coordination:

- Canada is not an island

- USA must reduce net absorption and Asia 9especially China) increase net absorption (he mentioned that other EM can also start to run current account deficits)

- Canada will have to adjust for global policy changes and unforeseen events

- Adjustments can best be accomplished if baseline fiscal plan is credibly set to achieve balance (less than 1% deficit) by 2015 and monetary policy set to keep inflation at 2%

During the discussion period, Mr. Dodge said that the risks of deflation and inflation remain. On the elusive issue of productivity, he repeated several times that Canada has not found a way to increase total factor productivity, something which he also recently lectured on to Laurentian University graduates.

Ed Note: Be sure to check out the excellent ZeroHedge site where there are many many fascinating articles and also Leo Kolivakis Pension Pulse website

“If the American people ever allow private banks to control the issue of their money, first by inflation and then by deflation, the banks and corporations that will grow up around them [the banks], will deprive the people of their property until their children will wake up homeless on the continent their fathers conquered.” – Thomas Jefferson

Richard Russell Comment — And that’s exactly what has happened. And it’s the reason why the Federal Reserve must be abolished. The Fed is an affront to the Constitution of the United States. The Fed is a private banking cartel, created by bankers, run by bankers, for the benefit of bankers. On top of that, the Fed’s actions are secret, and the Fed has never been audited.

Click HERE to watch the video below. The Video starting with Dr. Marc Faber, Peter Schiff and a load of other experts on the issue. Be aware, it is a 30 minute video.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair