Daily Updates

In this Issue:

Subprime Dubai

More Government Data Fun:

Unemployment Claims Were Not Down

Why I Am Optimistic About the Future

The Millennium Wave

New York and My Own Psychic Income

I admit that of late my writings have had a rather dark tone. There are certainly a number of severe long-term problems that we must deal with, and they’re going to serve up a lot of economic pain. But the Thanksgiving weekend with the kids has me in a reflective mood, and one that has only served to underscore my long-term optimism. This week we look at why 2007 will not be the good old days we will yearn for in 20 years, after we briefly visit Dubai and the latest unemployment numbers.

Subprime Dubai

While we in the US spent our Thursday eating turkey and watching football, the rest of the world’s markets went into a downward spiral as Dubai announced it wanted its lenders to give the country a six-month moratorium on some $80-90 billion in debt. This has the potential to be the largest sovereign debt default since Argentina. Somehow this was a shocking development. (How can too much debt and real estate be a problem?) And by markets I mean gold, commodities, oil, stocks, and risk assets everywhere. They all went down. Today the US markets experienced their own sell-off, though not as deeply as the rest of the world.

As I wrote last Friday, the world is now negatively correlated with the dollar, and as money went into the dollar and US treasuries, everything else went down. Vietnam devalues, Greece is looking increasingly risky, Russia wants to devalue some more, the world is still deleveraging, etc. Is this another repeat of 1998, when Russia and the Asian debt crisis tanked the markets?

To get an answer, let’s look at some facts about Dubai. It is one of the Arab Emirates; but unlike its neighbor Abu Dhabi, oil is only about 6% of the economy. While the foundations of the country were built with oil, the country has diversified into finance, real estate, tourism, trading, and manufacturing. It is a small country, with a little under 1.5 million residents, but with less than 20% being natural citizens – the rest are expatriates. The gross domestic product is around US $50 billion.

(Note: http://www.ameinfo.com/67802.html and then converting the currency. I found the numbers on various websites and services strangely at wide discrepancies. This seems close to a median number. I think the discrepancy is mostly people confusing the GDP for the United Arab Emirates as a whole, which includes Abu Dhabi, rather than just Dubai.)

Dubai has become a byword for thinking large. The world’s tallest building, underwater hotels, the largest manmade islands (plural), indoor snow skiing in the desert… For links to more information try this from Wikipedia: “The large-scale real estate development projects have led to the construction of some of the tallest skyscrapers and largest projects in the world, such as the Emirates Towers, the Burj Dubai, the Palm Islands and the world’s second tallest, and most expensive hotel, the Burj Al Arab.” The list goes on and on.

UBS suggests that the $80-90 billion in debt may not include rather large off-balance-sheet debt (where have we seen that one?). So, a country with a GDP of $50 billion borrows $100 billion. They build massive projects, which are now among the most expensive real estate in the world. The latest manmade island plans for one million people to buy property there. Seriously. Talk about Field of Dreams.

Then came the credit crunch. Property values dropped by as much as 50%. Sales, say the developers in understatements, have slowed. Seems there was a lot of debt used to speculate on real estate, not to mention buying Barney’s, Las Vegas casinos, banks, etc. And while US banks have little exposure, it seems England has about 50% or so of the debt, with the rest of Europe having the lion’s share of the remainder. Admittedly, the estimates seem to confuse the debt of Dubai with that of Abu Dhabi, so it is hard to know a reliable number, other than that European banks are the most exposed.

Now, here’s the deal. Abu Dhabi has the world’s largest sovereign wealth fund, at over $650 billion. Dubai has a “mere” $15 billion. If they cared to, Abu Dhabi could write a small check and make all the problems disappear. It just seems that they are not ready to do that, at least not yet. Abu Dhabi already got the world’s tallest building on past debt problems.

Construction and real estate were as much as 25% of the economy. Let’s see. Large leverage with maybe $5 billion in interest in a $50 billion economy that is 25% construction? A construction and real estate-driven economy. A real estate bubble. Sound like California, Florida, Spain? How can this be a surprise, except that everyone expected big brother Abu Dhabi to pick up the check?

While Abu Dhabi did advance $5 billion earlier, Dubai is not letting that money out of the country. There are projects to be finished, you understand. From where I sit, this is just rather hard-headed negotiations, a restructuring of who owns what and who will get what assets. It will all settle out. Given the massive losses that world banks have already taken, this is rather small potatoes.

So why the reaction by the markets? Because I think many participants know that the potential for there to be a serious correction is quite real. When anything as relatively small as Dubai spooks the market, it should serve as a warning sign. The world has priced in 5% GDP growth for the US and much of the developed world in the equity and commodity markets. Either we have to get that or the markets are going to have to come back to the reality of what I think is going to be a much lower growth figure.

But in any event, one of the lessons to be learned is that investors should pay attention to where the leverage is. Unsustainable debt trends end in tears. They always do. Spain, Greece, Italy, the UK, and Japan will all have to face major restructuring in the next decade due to leverage. And we in the US will also find that we cannot grow debt at our current levels. Will we pare our debt willingly or be forced to by the market? Either way, it will make for a less than optimal economy over the coming years. Muddle Through, indeed.

More Government Data Fun:

Unemployment Claims Were Not Down

The headlines said that initial claims dropped to 466,000 here in the US, finally falling below 500,000. This was greeted with proclamations of recovery. First, let me say that 466,000 people filing for unemployment is still way too high. That is a lot of people losing their jobs, and when we first crossed over 450,000 a few years ago that level was seen as a sign of recession.

Second, the headline number was a seasonally adjusted number. The actual number was 543,926. What is happening is that we are coming off of wickedly high numbers in 2008 and a seasonal number that was much lower in the preceding years. It is another part of the Statistical Recovery. And this trend is likely to keep on for the rest of the quarter. My friend John Vogel, who analyzes the unemployment numbers for me each week, shows pretty convincingly that the average for this current quarter will be over 500,000 per week on a non-seasonally adjusted basis. This is less than a 10% drop from last year for the same quarter. Job losses are continuing to mount, and we are on our way to an 11%-plus unemployment number by next summer. Statistical Recovery, indeed.

Why I Am Optimistic About the Future

….read more HERE.

Weighing the Dollar Alternatives: Part II

In last week’s Money and Markets column, I analyzed the three major liquid currencies as prospective alternatives to the U.S. dollar: The Japanese yen, the British pound and the euro. Fundamentally, they all fell short.

As I explained then, these three don’t offer any appeal over the dollar. That’s because the currency market is a beauty contest where the least ugly wins. And not only is the dollar the least ugly, but it offers refuge when fear and uncertainty grip the markets

So What about Other Currencies?

Other world currencies may not offer the liquidity to emerge as a primary reserve currency. Nonetheless, I’m frequently asked how they stack up against the dollar. Do they offer opportunities to preserve the purchasing power of your wealth … or at least make for a good trade?

This conditional statement I wrote last week applies to these other currencies as well:

“If the Fed and other central banks around the world fail to remove the emergency stimulus before those measures translate into inflation, then ALL currencies will fall in value relative to hard, tangible assets like gold, real estate and other commodities … even financial assets like stocks and bonds. That’s global inflation.”

That determination will likely be made years down the road. For now deflation remains the problem until global demand and credit growth bounce back, which I think will be a longer, bumpier road than most think.

But, like last week, I don’t want to debate inflation or deflation today, I want to take a look at some other potential alternatives to holding U.S. dollars in a world where dollar sentiment is profoundly negative.

So let’s take a look at …

Dollar Alternative #4 —

The Swiss Franc …

The historical safe-haven feature of holding the currency of the neutral Swiss should be an extra benefit these days. But the global nature of the financial crisis deteriorated the safe-haven quality of Swiss francs. And its preferred status has transferred to the U.S. dollar.

Switzerland’s banking system was (and remains) highly exposed to the financial crisis. And, even worse, the global crack-down on tax havens puts the Swiss private banking model in jeopardy.

In addition, the Swiss are printing money at a faster clip than the U.S. and have been intervening in the currency markets to weaken the franc and to attempt to curtail deflationary forces.

The Swiss economy is expected to underperform the U.S. in 2010 and 2011. And interest rates in Switzerland are as low as they are in the U.S. and are projected to follow U.S. rates higher in the coming years, but at a slower rate. Again, the advantage goes to the dollar.

Dollar Alternatives #5, #6 and #7 —

Commodity Dollars …

Canada’s banking system has held up better than its G-7 counterparts. And the Canadian economy has tracked the U.S. economy closely through the recession. Although Canada has a strong performance linkage to the price of oil, the economy has an even stronger link to the general health of the U.S. economy.

That’s why the Canadian dollar has tracked the U.S. stock market in lock-step since the crisis broke out. And I expect that trend to continue. So, if you think our stock market will go higher from here, the Canadian dollar offers a dollar alternative.

As for the other two commodity-centric currencies … the Australian and New Zealand dollars … there’s only one story worth telling here. It’s Australia. Australia is the bright spot in global currencies. Its economy weathered the global recession the best, and its central bank was the first in the world to raise interest rates … twice.

Australia also happens to be in the sweet spot to take advantage of growth in China and higher commodity prices. So Australia offers an alternative to the dollar, but only after it pulls back from its aggressive 60 percent surge of recent months. And only with an appreciation for the risks … as described below.

Dollar Alternatives #8, #9, #10 and #11 —

The BRIC currencies …

Brazil, Russia, India and China are still emerging economies. And these developing economies tend to come with imbalances and shortcomings that leave them exposed to excessive volatility. Therefore, they should be off-limits as passive, unmonitored currency investments.

In short, the currencies of these countries are high-beta. So when the risk environment is good, these currencies will do better than major currencies. When it’s not, look out.

For example, just last year Russia spent over a third of its $600 billion in currency reserves trying to defend the value of the plummeting ruble as global capital fled Russia in search for safety. And now, the Russians are talking about capital controls, like Brazil has done, to restrict speculative flows into their financial markets.

What a difference eight months makes. And that’s indicative of the volatile nature of these emerging market countries. And with protectionism picking up globally, the uncertainty surrounding these currencies is even greater.

China’s a different ball game. The managed currency policy in China, which I most recently wrote about in my November 14 column, prohibits the Chinese currency from playing a role globally, anytime soon.

Can China’s currency appreciate materially? Yes. Will it? Not likely. The Chinese will continue to do what’s in their best interest. And keeping the yuan artificially cheap creates plenty of advantages for the Chinese — and disadvantages for the rest of the world.

You Must Respect Risk …

We are in highly uncertain times, and, in my opinion, the markets are far too complacent in assessing risk. Rising stock prices have a way of making people feel good.

But keep this in mind, when considering alternatives to the dollar for the sole purpose of preserving purchasing power of your wealth: There is always the risk of a decline in these currencies, even when a fundamental indicator may seem positive.

Why? Because all of the currencies I’ve mentioned today are intimately tied to the performance of the global economy. And with that linkage, comes risk.

In fact, just last year:

- The Australian dollar dropped 38 percent in three months,

- The Canadian dollar fell 26 percent in one month,

- And the Brazilian real lost 59 percent of its value against the U.S. dollar in a little more than a month.

- And if you’re overly concerned about the recent weakness of the dollar, you need to put things into perspective …

The dollar still remains seven percent stronger than it was last year against the euro, 19 percent stronger against the pound and in better position than nine out of its top ten trading partners.

In this investment climate, investor perception trumps fundamentals. When investors feel confident, we see strong surges in global currencies. But when fear sets in, it’s just the opposite … investors look to the U.S. dollar.

Regards,

Bryan

Bryan Rich is an accomplished currency specialist with more than 12-years of experience in trading, research, and consulting in the global foreign exchange markets. He is President of Logic Fund Management, a currency management and consulting firm.

Bryan began his career as a trader for a $600 million family office hedge fund in London. The macro-oriented fund managed assets for a prominent European family, and was one of the largest players in global currency markets in the 1990s. Later, he was a senior trader for a $750 million leading global macro hedge fund located in South Florida. There, he helped manage and trade a multi-billion dollar foreign exchange options portfolio.

His consulting resume includes work for a boutique currency fund in New York, where he developed trading models and strategy for the core investment program of the company. He later joined the company as a partner, based in their Wall Street office.

Bryan has also served for several years in a management and consulting role for the Weiss Group, performing in a variety of analytical areas across its economic research, money management, ratings, and institutional research divisions.

He has a BA from the University of North Florida and an MBA from Rollins College.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

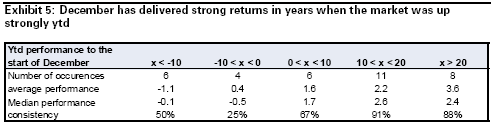

Goldman is increasingly confident in the end of year rally. In fact, a recent piece of research says December could be one of the strongest months of 2009 (not an easy feat considering the year we’ve had). Like other bullish investors, they believe seasonality will be an important influence on year-end action:

As we move into the year end, we take a look at the seasonality effect in equity markets. December stands out as one of the best months for equities, using both long- and short-term data; we think this year will be similar. In years when the first 11 months have yielded good returns, December has tended to be particularly strong.

December yields good returns on average

Based on monthly data going back to 1974, December has on average returned twice as much as the monthly average (1.7% vs. 0.8%). It is the third best month based on average data and the second best one using median data. It is interesting to note that January is also a good month for equities based on long-term data. December and January both yielded a positive return in more than 70% of the cases.

Goldman goes on to note that December is particularly strong when the current year has been strong:

The better the year, the better the December

There have been worries among market participants that the year end could see weakness in equities, following the strong year-to-date performance. However, historical data tell the opposite. In years when the return from January to November has been strong, December has tended to be very strong as well.

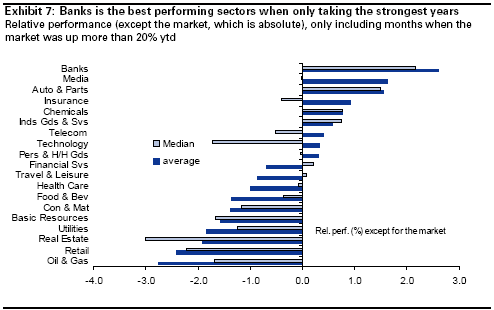

How to play it? Don’t rely on commodities to continue their inverse dollar surge. In fact, the best performing assets in big years have been financials cyclicals:

Oil & Gas has underperformed historically in December

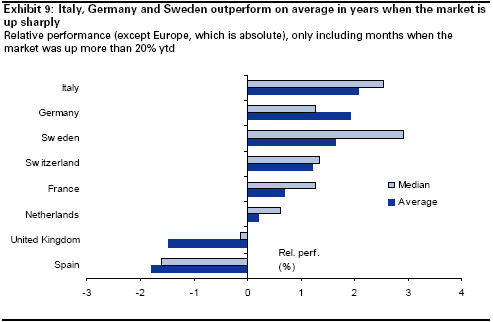

Commodity related sectors exhibit the lowest relative returns among all sectors in December. This holds even when restricting the sample to years when the market went up by more than 20% in the run-up to December. Conversely, Financials and selected Cyclicals have been the best performing sectors in December when the market has risen by more than 20% in the first 11 months. Looking at countries, the results are less interesting as the differentiation is less marked than between sectors. Germany stands out as the best performing country on average in

December.

Conditional seasonality: The better the year, the stronger the December

Recently, there has been a lot of talk in the investor community about de-risking and investors locking in their performance for the year. This has resulted in more bearishness going into the year end, as many have questioned the potential for further market upside based on the sustainability of the economic recovery. A seasonal analysis conditional on year-to-date performance tells a very different story. The better the performance has been from January to November, the more positive the return has tended to be in December (Exhibit 5).

Where to play it? Italy and Germany have been the best performers:

Quotable

“Credit is a system whereby a person who can’t pay gets another person who can’t pay to guarantee that he can pay” – Charles Dickens

….read Jack Crooks whole comment HERE.

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

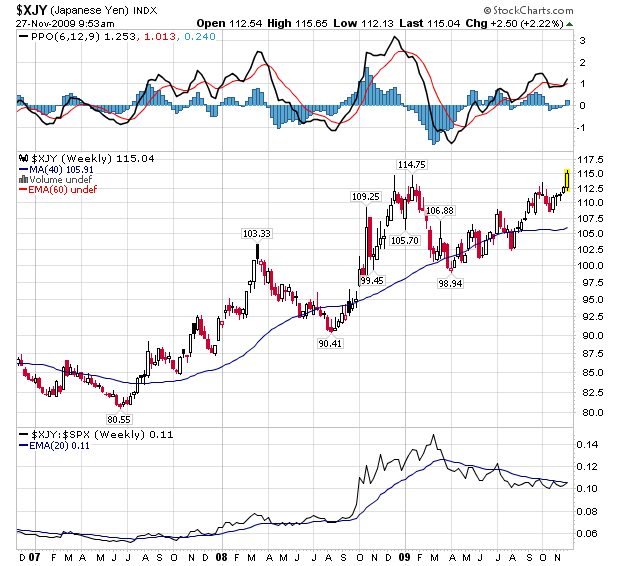

THE YEN AND THE US DOLLAR ARE SOARING AND PANIC IS IN THE AIR as the world is focusing again this morning on the news out of Dubai that Dubai World, the quasi-government controlled “investment” vehicle there has all but declared bankruptcy. Panic is indeed in the air, and well it should be, for this is amongst the worst of news one might conjure up and is one more spear driven into the heart of capitalism by greed and over-extension. We are seeing capital fleeing to safety

where it can, and we are seeing massive unwinding of short US dollar positions as the “carry trade” that had been wound up is now being unwound under duress.

This unwinding process shall not likely be a one-off, one or two day circumstance.

COMMODITY PRICES ARE UNDER MATERIAL, EVEN MASSIVE, DURESS EVERYWHERE and no one should be surprised given the severity of the dollar’s advance this morning. It matters not which commodities one is concerned with… base metals… grains… the “soft” commodities… precious metals… all are weak and all are weakening as the “carry trade” that helped sponsor the rise in these commodities is

now being unwound with a vengeance.

Dennis Gartman spoke about his timeless trading strategy at the Super Summitt go HERE for the Speaker Lineup and Sign Up HERE, Much more from some of the worlds best traders including:

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair