Daily Updates

If you are wondering why investors are focusing so much attention on the spreads between sovereign debt yields of Italy, and now France, take a look a the charts below. In each chart, the blue line represents the price of French and Italian benchmark equity indices, while the red line shows the spread between each country’s 10-year sovereign debt yields and the yield on German 10-year debt. For both France and Italy, their benchmark stock indices both went into a free-fall just as debt yields became unanchored from the yields on German debt.

Today, spreads have tightened by between 5% and 8% in both countries, and not surprisingly equities in both countries are higher.

Oil Now Solidly Above its 200-Day

While the S&P 500 has been stymied by its 200-day moving average recently, oil (West Texas) has made mince meat of it. As shown below, oil had a bit of trouble with resistance at its 200-day last week, but this week it has broken solidly above it. Now oil’s 200-day should act as some nice support as the commodity makes another run towards the $100 mark. Just what the consumer needs heading into the holidays!

Brent – WTI Spread Drops to Lowest Level Since June

Is the debt crisis in Europe beginning to make its presence felt in the oil market? A look at the spread between Brent and WTI crude oil suggests that the answer is yes. Even though the price of WTI has recently been soaring, thanks to a lack of a meaningful rally in Brent North Sea crude, the spread between the prices of the two benchmark oil prices dropped to $15.30 today for its lowest close since mid-June. It’s for this reason that the higher price of WTI crude hasn’t yet worked its way to the gas pump, and consumers can only hope that it stays that way.

Subscribe to Bespoke Premium to receive more in-depth research from Bespoke.

‘GoldNomics’ is an excellent short video showing how gold has retained value throughout history. Legendary investor & central banks are buying gold today. ‘GoldNomics’ makes the case that gold is an important safe haven asset and an essential investment a nd saving diversification in these uncertain times.

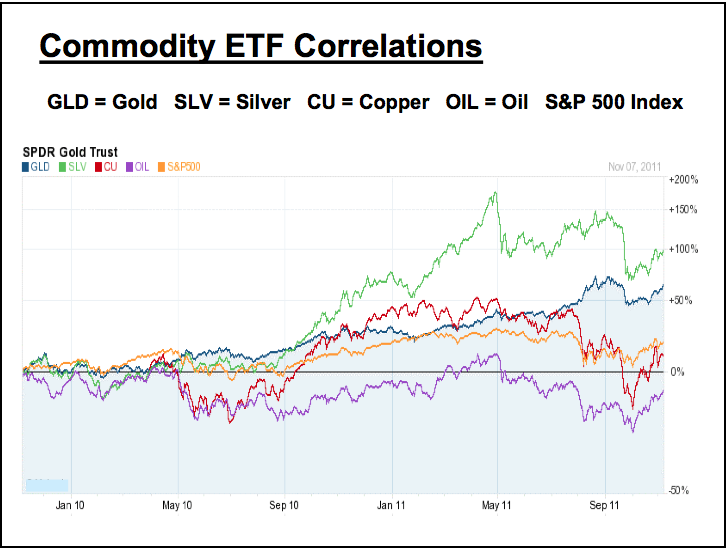

Calendar yearend is approaching, and the next six weeks have always been a prudent time to review one’s portfolio, fine tune a yearend tax plan, and make adjustments in ownership positions based on one’s best guess of what’s hot and what’s not for the ensuing twelve months and beyond. Emerging economies of the world and Gold have been the big performers over the past decade. A broad basket of commodities were the “rage” in the latter part of 2010, but their rush to record highs has lately been tempered to a degree. Have commodities lost their “glamour” status for global investors?

As can be expected, the answer to this question varies by commodity sector, but as most industry experts agree, there are not enough commodities to go around if you accept the growth data published by the International Monetary Fund. If supply cannot keep up with demand, prices will surely go up based on fundamentals alone, and if central banks keep printing money to resolve their debt issues, then additional pressures in the positive direction will only materialize.

The diagram below tells the story over the past two years:

Commodities languished in the shadows until September of last year when nearly every category of the sector rocketed to prominence in the investment community. Economic data suggested that a global recovery was taking form. Copper, the perennial “bellwether” of increasing economic activity, was the first commodity to record a significant move, two months ahead of the “pack”. The metal quickly doubled in value over the subsequent six months, signaling an aggressive bull market for the entire sector.

When the anticipated recovery began to show signs of stalling in May of this year, the inevitable pullback in commodities occurred, most correlating tightly with the S&P 500 index for the months that followed. Gold and Silver were exceptions, displaying modest corrections, but maintaining material returns for the full two-year period. What will the future bring? Here are a few comments:

· Gold: The past decade for Gold has been remarkable, but analysts are even more impressed that the shiny metal has remained perched above its 200-day moving average for the past three years, reflecting strong underlying support. Appreciation is still in the cards as long as this condition continues;

· Silver: Silver is presently in a “consolidation” phase, which is actually healthy, allowing profits to be taken and an opportunity for new investors to climb onboard. As experts understand, Silver is more than a store of value. Industrial demand is another force behind its appreciation potential. When inflation picks up, as it surely will, demand will remain strong. Gold “owned” the past decade, but many experts profess that Silver will own the next one;

· Copper: Copper and related commodities like coal (“KOL”) and iron ore (“MXI”) will flourish once again when strong economic activity returns. China and India are short on energy and natural resources, as are most of the emerging economies of the world. The ascendance of their respective middle classes will create long-term demand that will outstrip the supply side of the equation;

· Oil: Oil prices have a long way to go to recover to the pre-recession levels in 2008, but all indications are that this retracement will occur sooner, rather than later. Timing is the issue. Stable global growth will fuel the recovery.

These comments pertain to only four members of this sector. The lesson learned over the past year is that commodity prices are super-sensitive to any signs of a global economic recovery. From precious metals to rare earths, from corn to cotton, demand demographics frame a positive portrait for future price appreciation.

Tom Cleveland is a writer and market analyst for http://www.forextraders.com/ , an online resource for the foreign exchange market and currency news. He has over 30 years of experience in executive management, corporate governance and business development, having served as CFO for various Visa International entities from 1980 until his retirement in 1999. Tom’s writing on business issues has appeared in the NY Daily News and BusinessInsider among others.

Alert!

Mark’s Timers Digest Buy signal of Friday November 4th has been reversed and is now a Timers Digest “Sell” signal!

“Bulletin

With broad-based Leibovit Negative Volume Reversals forming today, I have no choice but to switch to a SELL signal. – Mark Leibovit of VRTrader

The Friday November 4th Message: Mark moves to a “Buy” Signal Friday November 4th

After moving from TIMERS DIGEST “SELL” Signal to a TIMERS DIGEST NEUTRAL signal on Oct. 7th at S&P 1155.00, Mark Leibovit has moved to a TIMER DIGEST ‘BUY’ signal on November 4th expecting that will at rise higher than the Oct. 27th high of S&P 1292.66 and also test the May 2nd high of S&P 1370.68 between now and the end of the first quarter 2012.

In Mark’s detailed daily VRTrader Letter, Mark mentions that the cutting of Europe’s interest rates to 1.25% underscores the Government determination to support markets, as well there are positive seasonality factors between now and May 2012.

The above is just a portion of Mark’sVRTrader. Much more analysis contained every day in Mark’s VRTrader. Just send an email to mark.vrtrader@gmail.com or call 928-282-1275 if you wish to sign up for his trial subscription and follow his analysis throughout this move.

Mark’s bullishness and comments on seasonality match those Money Talks regular Don Vialoux in this video: http://www.moneytalks.net/daily-updates/6114-sap-500-has-worst-opening-of-the-month-since-1932.html

Daily Chart S&P 500 Futures Contract for December

Ed Note: Some great charts

The companies in a race to produce critical heavy rare earth elements by 2016 are already way ahead of their smaller competitors. In this interview with The Critical Metals Report, Kaiser Research Online editor John Kaiser handicaps the players on the end-user, producer and investor side—believe it or not, China may have the largest stake in developing sources outside its borders.

…..read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair