Daily Updates

Despite India’s Optimism, There May Be a Better Time to Buy

BY MARTIN HUTCHINSON, Contributing Editor, Money Morning

The Indian government announced Monday that the country’s economy was expected to expand by 7.2% during the fiscal year that ends next month.

Agriculture – which had been expected to be a major drag on the economy because of a poor monsoon season – contracted a mere 0.2%. That is a truly stellar performance, showing that India – like China – has emerged almost unscathed from the global economic meltdown. It would pretty well justify the Bombay Stock Exchange Ltd.’s rich Price/Earnings multiple of 20 and would make Indian stocks a “Buy” even at these levels.

Unfortunately, when looked at closely, the picture is not quite so rosy.

…..read more HERE (scroll down)

02/09/10 Melbourne, Australia

If you’ve been thinking about reducing exposure to stocks, now might be a good time. And if you’ve been thinking about increasing your exposure to precious metals, now might be a good time.

According to Morgan Stanley economist Gerard Minack, the stock market is in for a correction after its 9-month “relief rally.” In a note to clients Minack wrote, “We see the rise from March 2009 as a typical relief rally that follows major bear markets. Those relief rallies can occur regardless of underlying macro conditions, regardless of liquidity conditions and – most importantly – regardless of what happens next… We think risk assets have swung to pricing a better outlook than is likely.”

Minack says that a 25% correction is now in order. To be fair though, he doesn’t think the market will make new lows after that, only that it’s gotten way ahead of itself at these levels. The Grand Old Man of Dow Theory, Richard Russell, is even more direct. He’s predicting a “second round of pain” for stock markets. “I note that most analysts are now bullish,” he observes, “and that they are recommending stocks for the ‘continuing advance.’ At the same time, most economists are optimistic, arguing that the ‘longest recession since World War II has ended.’

“Typical,” Russell gripes, “last March everyone was bearish and the market was establishing a temporary bottom. Now that everyone is optimistic, the stock market is topping out and the public (the amateurs) are about to receive their second round of pain.”

What to do?

…read “what” HERE

Dan Denning is the author of 2005’s best-selling The Bull Hunter. A specialist in small-cap stocks, Dan draws on his network of global contacts from his base in Melbourne, Australia, and is a frequent contributor to The Daily Reckoning Australia .

Special Report: From Hulbert’s No 1-Ranked Advisory Letter Over 5 Years, GOLD $2000 REPORT : Five entirely new ways to play the gold trend and a hidden way to snap up gold- for less than one penny per ounce!

Click HERE if you want to learn from some of the timeless advice from some of worlds best traders including Steve Todd, author of this report and 3 times ranked # 1 by Timers Digest in the past ten years.

Todd Market Forecast for Tuesday Feb. 9, 2010

Available Mon- Friday after 6:00 p.m. Eastern, 3:00 Pacific.

DOW + 150 on 1700 net advances

NASDAQ COMP + 25 on 1100 net advances

SHORT TERM TREND Bearish

INTERMEDIATE TERM TREND Bullish

The market awoke to word that the EU, mainly Germany would bale Greece out in exchange for austerity measures. This sent the Euro up and the dollar down, which in turn pushed our stock market higher. Got that?

There was no official word however and there are also concerns that austerity measures could cause social unrest. And then there are also concerns about Portugal, Spain and Italy. It never ends.

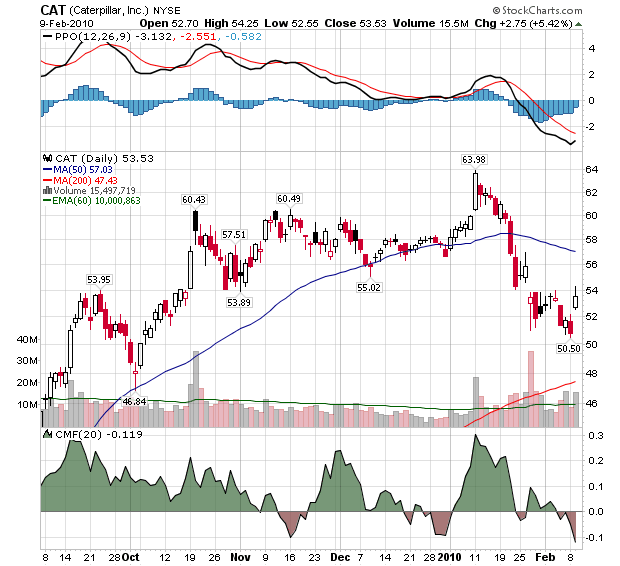

A Morgan Stanley upgrade of Caterpillar, which surged 5 ½% also helped the bullish case on Tuesday.

Chart inserted by Moneytalks

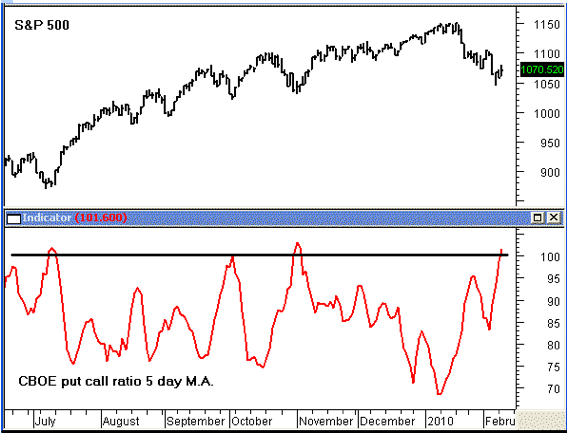

Help may be on the way with sentiment also. When the CBOE put call ratio’s 5 day m.a. moves above 1.00, there is a tendency for the market to move higher. We can see this in the chart below.

The dollar’s drop helped push a rally in gold, silver, copper and crude oil. Bonds were down on the session.

BOTTOM LINE:

Our intermediate term systems are on a buy signal.

NEWS AND FUNDAMENTALS:

There were no important news releases on Tuesday. On Wednesday we get the trade deficit and crude oil inventories.

OTHER MARKETS

We’re on a buy for bonds as of Jan. 12.

We’re on a buy for the dollar and a sell for the Euro as of January 26.

We’re on a sell for gold as of Feb. 4.

We’re on a sell for silver as of January 21.

We’re on a sell for Copper as of Jan. 12.

We’re on a buy for crude oil as of Feb. 2.

We are long term bullish for all major world markets, including those of the U.S., Britain, Canada, Germany, France and Japan.

No guarantees are made. Traders can and do lose money. The publisher may take positions in recommended securities.

STEPHEN TODD – A SHORT BIOGRAPHY

Editor and publisher of the Todd Market Forecast, a monthly stock market

newsletter with an included nightly hotline.

Steve has published articles on the stock market in the following

publications: Barron’s, Stock Market Magazine, Futures Magazine, The

National Educator, and others.

His stock market commentary is heard on the following stations: CNBC,

Bloomberg, CNNfn, Associated Press Radio, Business Radio Network, CKNW in

Vancouver, British Columbia, KFWB, Los Angeles and ROBTV in Toronto,

Ontario.

RANKED # 1 – BY TIMER DIGEST

Timer Digest of Greenwich, CT monitors and ranks over 100 of the nation’s

best-known advisory services. If you have heard of an advisor, it is

likely that he or she is monitored and ranked by Timer Digest.

Once per year, in January, Timer Digest editor Jim Schmidt gives the

rankings for all services monitored for multi year time frames. We were

ranked # 1 for the past ten years at the end of 2003, 2004 and 2005. At

the end of 2006 we slipped to #3 and at the end of 2007, we were ranked #

5.

With all the volatility in the markets this past week and my absence from the office, I thought I write a short update on the markets and model portfolio. Hopefully with it and the special update with George on Thursday, you will know my latest thoughts.

U.S. Stock Market – On a very short-term basis, it’s oversold and due for a bounce. The close Friday suggests that’s a good likelihood as of this writing. While you can never ever say the “Don’t Worry, Be Happy” people are done, one should be out of long positions except those related to metals. Long equity positions outside of the U.S. are at a minimum, the lesser of two evils. If for some reason the “Happy” people can muster one more run to new recovery highs, I don’t believe such a rise would be higher enough to justify playing from the long side here.

I can’t emphasize enough that I’m quite negative on the U.S. economy and equity market for years to come. Again for the umpteen time, I believe it should mirror the Japanese economy and market of the last 20 years.

Precious Metals – Many forget that platinum and palladium are precious metals along with gold and silver. They’re both fairly priced. The same can’t be said for gold and silver.

Gold – If a picture is worth a thousand words, than I don’t need to say much about the long-term direction of gold. Back in 2004, 2006 and 2008, many were calling a top in gold. While there was a correction, gold eventually went to much higher levels. Such shall be the case IMHO. In fact, I believe we shall look back at this period and conclude it turned out to be the last great buying opportunity for quite some time. Yes, arguably one could make a case for another $100 down given the recent technical sell-off. But given the selling has been limited to the paper market on the Crimenex (Comex) and the reversal seen late Friday both in gold and gold shares, I think the chances of a substantial fall from here are remote.

Silver – The “Rodney Dangerfield” of precious metals. The concentrated short positions on the Crimenex are ridiculous. Like it or not, it plays “second fiddle” to gold and while it can briefly lead, gold remains the big brother. Like gold, downside from here appears very limited.

Base Metals – The serious correction in copper and zinc has led me to feel they’re no longer fully priced and to remove my suggestion to overweight in precious metals. I think both precious and base metals are now equally weighted. But unlike gold and silver, I think base metals rallies are likely to be limited to their previous highs because economies worldwide are net not strong enough to warrant higher levels.

U.S. Dollar – I continue to believe this bear market rally can get to the 83-84 area basis the U.S. Dollar Index. But make no mistake about it, longer term we should see new lows on the dollar.

U.S. Bonds – I think this article says it all as far as I’m concern. (Ed Note: Article titled ‘Every Human’ Should Short U.S. Treasuries)

Oil and Gas – I’ve begun to look at oil again possibly from the long side if we get into the $60s and the dollar gets to the 83-84 area so stay tuned. Pass on gas (pun?).

Select Model Portfolio Comments

I would like to put FXE and FXC back on the buy list if the Euro gets below $1.35 and the Loonie $.90

More good news on Prosperity continues to support TGB as a buy under $4.50. The financing on Nevsun should remove most of the fears that came from the U.N. sanctions against Eritrea. Both NSU and Sunridge Gold hosted an analyst’s tour. Unless news gets worst regarding Eritrea, SGC should see better days ahead.

Given the latest results on Evolving Gold, the stock appears the cheapest since I first became involved with it. There’s a teleconference on Tuesday.

Live Participant Dial In (Toll Free): (877) 407.8035

Live Participant Dial In (International): (201) 689.8035

![]()

Click HERE to hear Don Vialoux and other masters forecast market risk and opportunity on January 22 – 23rd 2010 at the World Outlook Conference Vancouver.

The Bottom Line

The seasonal trade is lining up, but its not there yet. Please be patient. Stay tuned.

More below:

Technical Action Yesterday

Technical action by S&P 500 stocks was quiet yesterday. One S&P 500 stock broke resistance (Hasbro) and one stock broke support (Genuine Parts). The Up/Down ratio slipped from 1.96 to ((267/137=) 1.95.

Technical action by TSX Composite stocks was non-existent despite weakness in the Index. No TSX stocks broke resistance or support. The Up/Down ratio was unchanged at (126/57=) 2.21.

Setting Up for the Seasonal Trade in the Canadian Energy Sector

Seasonal influences

The TSX Energy Index has a period of seasonal strength from February 25th to May 9th. The trade has been profitable in 14 of the past 15 periods. Average return per period was 13.7%. Following is a seasonal chart on the sector recently developed by Brooke Thackray:

The period of seasonal strength in the TSX Energy Index coincides with the period of seasonal strength in North American gasoline and crude oil prices. Other annual recurring events that favourably influence the sector during this period include fourth quarter results, results from the winter drilling season, annual reports, annual meetings and annual revisions to reserves.

Technical Influences

The TSX Energy Index currently does not have an attractive intermediate technical profile. The Index recently broke support at 273.30 and established an intermediate downtrend. In addition, the Index closed below its 200 day moving average yesterday. Strength relative to the TSX Composite has been negative during the past month.

The TSX Energy Index is short term oversold on the charts. MACD is oversold, but continues to trend down. RSI at 32.52% also continues to trend lower, but is more oversold now than last February. It is near the 30% level where a bottom frequently occurs. Stochastics recently fell below 20% and are showing early signs of bottoming.

In conclusion, the technicals are lining up at an oversold level for the seasonal trade, but are not sufficient yet to trigger the trade.

Fundamental influences

Fourth quarter reports released by companies in the sector to date have not been greeted favourably by the market. Stock prices quickly moved lower on news. Cash flow and earnings by companies such as Imperial Oil and Suncor were significantly lower in the fourth quarter compared to the same period last year and compared to consensus estimates. Other major Canadian companies are scheduled to release fourth quarter results later this week and into next week.

And now the good news! Cash flow and earnings by the sector resume a strong upward trend beginning in the first quarter of 2010 thanks to a year-over-year increase in crude oil prices. Crude oil prices have more than doubled since December 2008.

Seasonality in key energy equities in the sector

Seasonality by key stocks in the sector varies significantly. The following table shows the frequency of profitable trades and average return per period from February 25th to May 9th based on the past 10 periods:

Stock Frequency of Average Return

Profit out of 10 Per Period (%)

Nexen 7 12.3

Imperial Oil 8 6.7

Penn West Energy 8 8.8

Husky 8 11.1

Suncor 9 15.5

Cdn. Natural Res. 9 19.4

Encana 8 14.8

Talisman 8 12.7

Cdn. Oil Sands 8 16.0

The Bottom Line

The seasonal trade is lining up, but its not there yet. Please be patient. Stay tuned.

Possible ETF Candidates for the trade:

They include iShares TSX Energy Index (XEG), Claymore Oil Sand Sector (CLO), BMO TSX Equally Weighted Oil Index (ZEO) and Horizons BetaPro TSX Bull + ETF (HEU)

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Don earned his Chartered Market Technician (CMT) designation from the Market Technician Association in 1995. His CMT paper entitled “Seasonality in Canadian Equity Markets” was published in the Spring-Summer 1996 edition of the MTA Journal. Don also has extensive experience with Exchange Traded Funds (also know as Index Participation Units) as well as conservative option strategies. In 1990 he wrote a report that was released in the International Federation of Technical Analyst Journal entitled “Profiting from a Combination of Technical and Fundamental Analysis”. The report introduced ” The Eight Phases of the Stock Market Cycle”, an investment concept that continues to identify profitable entry and exit points for North American equity markets. He is currently a member of the Toronto Society of Fundamental Analyst’s Derivatives Committee. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair