Daily Updates

Please Note – Our offices will be closed from April 1st to April 12th and blog posts will be very limited.

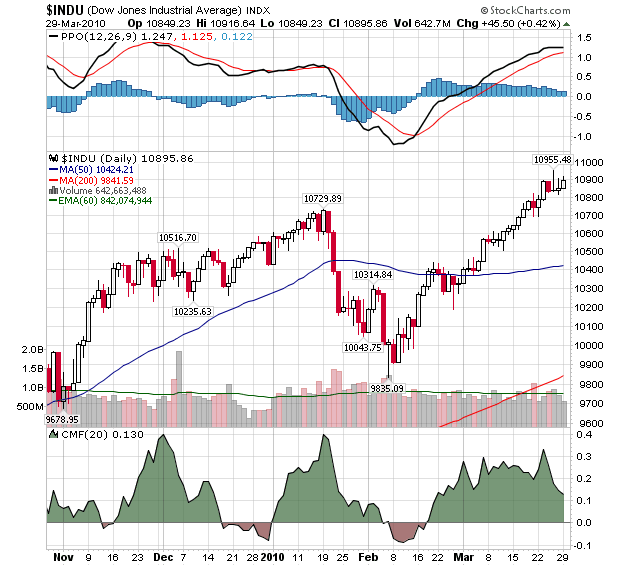

U.S. Stock Market – DJIA 11,000 – ALL ABOARD! Its been my contention that we shall break above 11,000 on the DJIA in order to create the media frenzy of “happy days are here again” and for the shorts to finally throw in the towel. I’ve stated for over a year that my economic model was pointing to a peak in the June/July 2010 time frame and not to expect the stock market to truly top out before that. I continue to look for this occurrence.

Chart via Money Talks

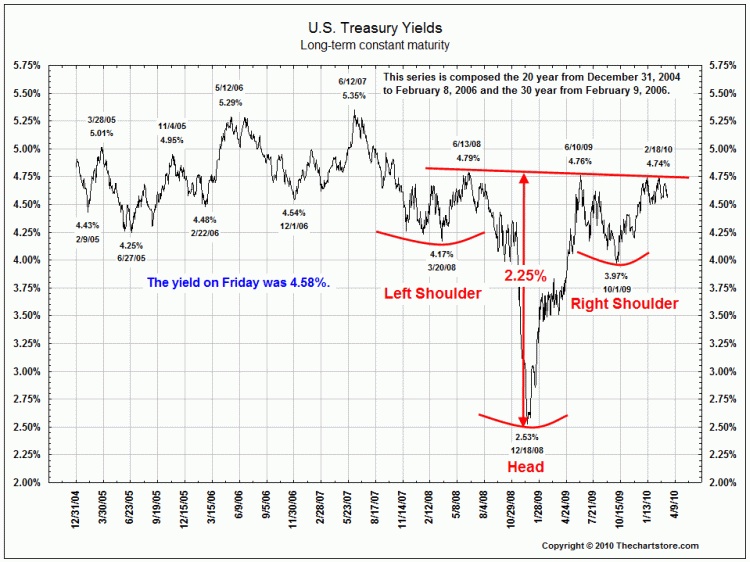

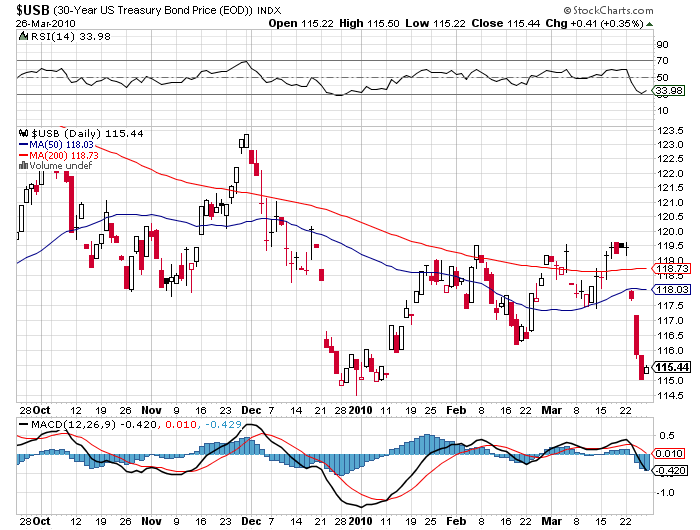

U.S. Bonds – A massive head and shoulders pattern has formed and strongly suggests when the neckline is broken to the upside, interest rates are going to head much, much higher.

It’s critical to appreciate that after almost a 30-year bull market in bonds the bear market unfolding is not going to be just a matter of months.

Gold – What can I say that I haven’t said already? Despite the almost daily onslaughts of some advisers saying gold is in a bubble, ready to tumble, nothing but a relic and blah, blah, blah, gold has once again weathered another assault despite a dramatically shrinking base of ardent bulls like yours truly, Bill Murphy and Jim Sinclair. The perma-bears would suggest we should be called the three stooges. Me? I fancy the three musketeers!

We remain in a secular bull market that is turning a ceiling of a four-digit price into a floor. The eventual top from this process will be many hundreds, if not a thousand or more dollars from this floor. The road will remain rocky as gold is the #1 hated investment by the vast majority of people in and around the financial arena. You’re never going to wake up and find the masses proclaiming its virtues. In fact, the day you wake up and the “Senior Analyst” actually likes gold, run, don’t walk to sell. But, for now continue to use him and other perma-bears as the ultimate contrary indicators.

Chart via Money Talks

US Dollar – The countertrend rally continues and my target of 83-84 is still intact. This is by no means the dawn of a new bull market but a necessary and welcomed occurrence in the secular bear market the dollar remains in.

Chart via Money Talks

The U.S. stock market would like you to believe this is our future:

But sadly, after this summer, reality should begin to set in and many Americans shall realize (like many do now around the world) we are really this:

Model Portfolio and Grandich Clients Update

On Major Moves, Peter Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website

To HERE Peter speak and others speak on Trading go HERE:

‘Food commodities are at 200 year lows in real time dollars” – Marc Faber

The biggest economic threat is…

(Jim Rogers)

This may bring to your mind problems related to high leverage, cheap liquidity, rising inflation and the like. But the gravest problem facing global economy is far from these. And as per investors like Jim Rogers it has the potential to derail global growth. It also holds promise of leading to social unrest. We are referring to food scarcity. With the world’s biggest food producers producing lesser food and instead concentrating on other segments of the economy, food scarcity has come to be the most perilous threat.

Ironically, the economies that carry the weight of global growth on their shoulders also have the potential to feed the world. The BRIC nations supply nearly half of the basic food requirements of the world. Be it wheat or meat. These nations house 42% of the world’s population and produce between 30% to 40% of all major food crops consumed around the world. However, this share has been gradually falling as the economies get more industrialized.

Take the case of India for instance. For the first time ever, India’s manufacturing will contribute more to its GDP than agriculture this year. While one may perceive it to be the result of faster industrial and service sector growth, the reason underlies a productivity disaster in India’s agriculture output. Soil is getting insensitive to the use of fertilizers and dependence on monsoons has barely come down. The truth is that while India has freed industry, agriculture remains a tightly controlled sector. Just to give an example, fixed prices exist for 25 commodities even now and input like fertilizers are subsidized. The result is that there is no incentive for the farmer to switch to other crops. Interestingly however, the Prime Minister’s Economic Advisory Council (EAC) is of the belief that a revival in farm output in the next fiscal will help the Indian economy move closer to the 8% growth rate.

Nonetheless, the BRIC nations have now have agreed to boost efforts to achieve food security and increase their role in global farming. The respective agricultural ministers will share information on technology and farm related inputs in the coming days.

We believe that improved growth in industrial activity is certainly critical to long term growth of Indian economy. However, India is also the nation with the world’s second largest population. Further, it is endowed with one of the most agriculturally conducive natural environments. Given these, Indian policymakers have their primary duty in ensuring food security for the nation. But nothing like coordinating with other large producers to ensure food security for the world.

The article “The Biggest Economic Threat is….” appeared in EquityMaster 03/29/10

The Bottom Line

Preferred strategy is to purchase equities and Exchange Traded Funds on a pull back in sectors with favourable seasonality including silver, platinum, mines & metals, oil services, energy and materials.

….Go view the commentary and the 45+ Charts Don Vialoux analyses in this great Monday comment HERE

Go view the commentary and the 45+ Charts Don Vialoux analyses in this great Monday comment HERE

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Don earned his Chartered Market Technician (CMT) designation from the Market Technician Association in 1995. His CMT paper entitled “Seasonality in Canadian Equity Markets” was published in the Spring-Summer 1996 edition of the MTA Journal. Don also has extensive experience with Exchange Traded Funds (also know as Index Participation Units) as well as conservative option strategies. In 1990 he wrote a report that was released in the International Federation of Technical Analyst Journal entitled “Profiting from a Combination of Technical and Fundamental Analysis”. The report introduced ” The Eight Phases of the Stock Market Cycle”, an investment concept that continues to identify profitable entry and exit points for North American equity markets. He is currently a member of the Toronto Society of Fundamental Analyst’s Derivatives Committee. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

Successful bullion dealer Greg McCoach brings more than 20 years of business experience and a vast network of mining contacts to the mining investment newsletter he launched in 2001, The Mining Speculator. In this exclusive interview with The Gold Report, Greg discusses his strategies to prepare for what he says will be a real buying opportunity.

The Gold Report: In your January newsletter you project that “the Fed will continue to create liquidity and the dollar will continue to fall. As the dollar falls, the bond market will sink. This will send interest rates higher, and rising interest rates in turn will put additional pressures on the economy.” You are monitoring three measures as the indicator of beginning of big changes economically and politically. These are (1) a collapse in the bond market, (2) a crash in the stock market, (3) an explosion in the price of gold.

We’ve had a stock market crash, gold has increased 400% in the last 10 years—which could be considered an explosion—and the bond market has pulled back. Are we in or about to begin the period of “big changes” you write about and what are the big changes?

Greg McCoach: The price of gold right now is nowhere near its high in this particular cycle. In other words, gold is still dirt cheap compared to where it will be by the end of this year, next year, and in the years to come. The Fed is caught between a rock and a hard place and will do what governments always do when they put themselves in these positions. They will try to inflate their way out of the mess they created. The problem thus far is that their inflationary tactics are not working the way they would like as deflationary pressures continue to exert their influence on markets. So expect even bigger and further massive injections of money into the system as the Fed tries to maneuver their way out. History clearly shows that governments caught in such a scenario will soon reach the inflection point where the fiat currency implodes and the credibility of the issuing government collapses. This is not just the case with the United States, but Japan, England, and Euro land as well.

Thus far investors have been playing the game of musical chairs with these fiat currencies as they jump from one to the other, depending on the circumstances of the day. In the end, the only currency that will be left standing will be gold, and when the rush comes to take a position in the yellow metal, it will be a move for the record books. The reason for this is simple. When oceans of fiat money suddenly try to take a part in this tiny market called gold, the move will be astounding. If you took all the physical gold that exists in the world above ground (not what is still in the ground) and melted all that gold into a giant cube, the cube would measure 20 yards by 20 yards by 20 yards. That’s it. That is why they call it precious. When the big move into gold occurs, there simply will be no room to receive it, thus driving the price into the stratosphere.

The big changes I talk about refer to the consequences that decades of abuse of our system of credit will have on the everyday lives of citizens not only in the United States but around the world. Aside from the obvious financial implications just mentioned, I believe will we see turmoil in the form of civil unrest, revolution, and wars. This is why I believe it is so important to think about preparing for such events. I hope for the best, but prepare for the worst.

TGR: You predict the TSX Venture Index will be 4,000 by the end of this year because investors will flood to a sector that won’t lose money. To what extent are you predicting another market crash and will it test the March 2009 lows? Will we see DOW/Gold parity? Will this all occur in 2010 and if so, what do we have to look forward to in 2011?

GM: I believe we will see another stock market meltdown as we saw in the latter part of 2008 and early 2009. This will take the DOW, in my opinion, lower than the March 2009 low. These events will occur primarily because of the problems related to commercial real estate derivatives, which will cause yet another horrendous ripple effect throughout the financial world. The loss of confidence in the markets at that point will be staggering as the world financial system goes through further rounds of bailouts and smoke and mirror cover-ups. The resulting loss of confidence on the part of investors will drive them to the safe-haven investments such as precious metals and their related mining stocks. This titanic shift in asset allocation on the part of investors, when it happens, will drive the TSX Venture Index to well over 4000, in my opinion. As to when this will occur, it is hard to say, but I believe we could see this happen before the end of 2010, and for sure by 2011.

The DOW/Gold ratio will drop precipitously as these events unfold. Right now the DOW/Gold ratio is roughly 10 to 1, but I would not be surprised to see this ratio around 5 to 1 by end of this year, early next year. Eventually as the world financial system completely implodes under the enormous and unsustainable debt loads, derivative losses, and fiat currency debacles, the DOW/Gold ratio will once again hit a 1-to-1 ratio. The gold price at that point could easily be $5,000 or more.

TGR: Greg, in our last interview with you, you mentioned real estate derivatives would blow up this year. To what extent do you think this will affect the resource sector in 2010?

GM: I think this could be one of the biggest catalysts for driving investors into the precious metals sector this year. The sub-prime mortgage derivative problem we experienced in the first meltdown pales in comparison to the commercial real estate derivatives that now lurk on the horizon. The general public is absolutely clueless about these instruments and their potential nightmare fallout.

TGR: Will the projected commercial collapse in real estate help gold only and not other metals/resources?

GM: Prices of all the precious metals would benefit in such a collapse.

TGR: Are we seeing the metals prices/stocks disconnect from the rest of the market?

GM: No, this has not yet occurred as I expect it will. I have been telling my subscribers to watch for the moment when this disconnect from the general market activity begins. In other words, as the move toward safe haven investments greatly increases, the precious metals prices along with their associated mining stocks will be the best performers while other markets tank.

TGR: Back in September you predicted gold hitting $1,500 before year end. In your opinion, why hasn’t that happened yet? Do you think we’re on our way to that goal in short order?

GM: The pattern for gold the past nine years has been this: gold runs to a new high every year and then retraces upwards to 14% before moving on to the next new high. The last new high of $1,226 per ounce for gold was reached on December 3, 2009. Since then we have retraced as much as 14%, briefly hitting the $1,055 level before rebounding to $1,155. We now reside right around the $1,100 level, but will once again be on the move towards another new high before the end of the year. This will occur because of the problems I have already mentioned and the unsustainable debt structure of the U.S. government. I maintain my outlook of a $1,500 gold price before the end of this year.

TGR: You’re maintaining that the price of gold is going to ultimately hit $6,500 an ounce with silver at $400 an ounce. How are we getting there and in what time frame?

GM: Yes, I believe we will see gold hitting a minimum of $6,500 an ounce as the U.S. dollar collapses. I also believe that the silver/gold ratio will go back to its 15-to-1 (15 ounces of silver to buy 1 ounce of gold) benchmark. As this happens silver will be roughly $400 an ounce. ($6,500 /15 = $433.00).

The time frame as to when this will occur is much more difficult to predict since you are trying to predict the collapse of the U.S. dollar. In my opinion, the collapse of the U.S dollar is as certain as death and taxes. It is not a matter of “if,” but when. The dark clouds that surround the issues of the U.S. dollar are growing by the day and getting much darker by the moment. If I had to make a guess, I can’t imagine we will get past the year 2012 without significant fallout. So I guess I’m saying I predict the ultimate collapse of the U.S. dollar within the next two and half years.

TGR: With regard to the physical metal, are you still recommending accumulating and holding it or at these prices should investors focus on investing in the juniors?

GM: My mantra for the past 10 years is to get the leverage with the precious metals juniors and take profits when they are running hot to build a significant position in the precious metals. I recommend buying gold, silver, platinum, and palladium and taking delivery of those metals. Don’t rely on ETFs, pooled accounts, or certificate programs to do this for you. In the end, I believe all of these products will be proven to be fraudulent. In other words, you won’t be seeing the benefit in those investments as the gold prices rise because the gold doesn’t exist the way they say it does. Those who want to protect themselves need to own the physical precious metals themselves and take delivery.

You want own the juniors and you also want to own the physical precious metals. I look at my holdings of physical metals as the ultimate bank account that cannot frittered away by corrupt, power-seeking politicians who seek our destruction. I use the juniors as my way to get big leverage in my investments. The combination of owning both the mining stocks and the physical precious metals is the best way for investors to protect themselves from the debacle of fiat currencies and utterly corrupt politicians and financial corporations.

Also, be very careful when selecting a place to purchase precious metals. There are good and bad dealers out there and unsuspecting buyers need to beware. Make sure you do your due diligence before purchasing.

TGR: For individuals just starting investing in metals, do you recommend focusing on gold or is silver a better opportunity now given the gold/silver ratio?

GM: In general, most investors will want to start with purchases of gold, but should not ignore the potential in silver. From the lessons of history, whenever we have a secular bull market in the precious metals, silver usually outperforms gold, dollar for dollar invested. While gold typically runs first and gets most of the attention at the earlier stages of the bull market, it is silver that typically sling shots past gold towards the latter stages.

Personally, I own both silver and gold. The problem I see with silver is that it is not as portable as gold. You can hold $50,000 worth of gold with your two hands cupped in front of you. You could put that gold into your coat pockets and walk down the street without anybody knowing what you are carrying. $50,000 dollars worth of silver, on the other hand, would take a handtruck to move.

Overall, I believe investors should hold both gold and silver in a well-diversified precious metals portfolio. They should hold gold as the ultimate store of wealth that protects their hard work and savings. They should also hold some silver for the potential use to buy day-to-day items such as bread, prescriptions drugs, etc., for when the government declares a “bank holiday” as the crisis in the banking sector exacerbates. During a bank holiday, checks and credit cards will no longer be accepted as payment for goods and services. This is another reason why I recommend keeping some cash on hand at all times. I am not recommending stuffing the mattresses; I am just saying it is probably smart to keep a few thousand dollars in 1s, 5s, 10s and 20s around the house. Silver Eagles would also be very useful in such an event as they are considered legal tender in the United States and could be used to purchase groceries.

TGR: You predict 2010 is going to be a great year for the metals and the juniors! So let’s go to your list of top juniors and discuss some of those.

GM: I don’t mind sharing a pick or two in interviews such as this, but I need to protect my subscribers who pay for my services, so I will talk about two.

First, let’s talk about Explor Resources (TSX.V:EXS). When investing in junior mining stocks, you want to put some money on the best cross-section of companies you can find. In other words don’t put all your money on any one company. I have found that by spreading the risk over 10 quality junior mining companies you can do rather well over time as these companies go through the process of discovery, development and then production. Out of 10 junior mining stocks you will typically lose on a few, gain on a few, and break even on a few. But, you will also tend to see one or two of these stocks that do phenomenally well delivering at 10 times or more.

When you invest in a junior mining stock you want to make sure it has big potential. EXS is a company that is looking for big, high- grade discoveries and can deliver such returns if successful. This company is unique in that they have not one, but multiple projects that could deliver such returns if drilling activity were to make a major discovery.

Thus far EXS seems to be on the right track, but is still in the early stages of discovery on three major projects that they are currently working on. Because of what they have, I feel the stock is worth buying up to $1.00 per share in hopes of making a major discovery that could deliver a $10, $20 or $30 stock if we have drilling success. This is what makes the junior mining stocks so exciting—the big leverage that can come with a discovery of merit.

EXS is hunting for an elephant gold discovery and they are hunting in elephant country. Exploration drilling represents plenty of risk, but if you balance the risks with the potential rewards, I think it is a wise speculation particularly in a time of rising gold prices.

U.S. Silver Corp. (TSX.V:USA) is another company I will talk about. I think they are well positioned to take advantage of higher silver prices that I see in our near future. The company expects to produce upwards of 2.7 million ounces of silver in 2010 at an average cash cost of roughly $14.00 an ounce. You don’t need to be a rocket scientist to see how quickly the profits will add up as silver prices go to higher levels, especially the kinds of levels I predict in the next few years.

U.S. Silver does have more shares outstanding then I would like to see, but this is one silver junior that I think will do well as the precious metals bull market continues to unfold.

Greg McCoach is an entrepreneur who has successfully started and run several businesses the past 23 years. For the last nine of these years he has been involved with the precious metals industry as a bullion dealer, investor, and newsletter writer (Mining Speculator) and The Insider Alert. Greg is also the President of AmeriGold, a gold bullion dealer. Greg’s years of business experience and extensive personal contacts in the mining industry provide unique insights that have generated an impressive track record for The Mining Speculator since its inception in 2001. He also writes a weekly column for Gold World.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

Bried Excerpt from Richard Russell’s Dow Theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe. Amongst his achievements Richard was in cash before the 2008/2009 Crash and he has been Bullish Gold since below $300 Ed Note: Richard Russell is bullish Silver and holds one of the largest single positions he has held since the 1950’s in the precious metals.

As subscribers know, I’ve been keeping an eagle eye on the daily chart of the 30-year Treasury bond. As of yesterday, the “long bond” had sunk exactly to its support at around 114. If support breaks, interest rates will be heading dangerously higher. The chart shows a double top (first two red arrows). Then a break to the downside and a formation showing a triple top (second set of three red arrows). As of yesterday’s close, the 30-year T-bond was sitting exactly on critical support. If bonds are down today, it won’t be pretty. (This paragraph was written Thursday evening, and yes, I do work at nights.) Ed Note: Friday’s Bond Chart below show’s Bonds did not fall further

WHO WILL BUY U.S. BONDS?

by David Rosenberg

Sentiment is so negative on the U.S. Treasury market it’s not even funny. Everyone seems to focus strictly on supply without realizing that the only way to predict a price is by forecasting both supply and demand. On its own, supply looks worrisome given the Administration’s bent on running huge fiscal deficits (and it just unveiled a new set of initiatives to reverse the foreclosure crisis).

What is ignored in so much analysis is the demand side of the equation — boomer households, for example, have only 6% of their assets in bonds versus nearly 30% in real estate and equities. They have about $8 trillion that they can put to use towards income-oriented portfolio strategies and in fact this powerful demographic trend is already underway. The banking sector is sitting on $1.3 trillion in cash and if it ever decided to play the yield curve, as it did coming out of the credit crunch of the early 1990s, it too could provide up to a trillion dollars of support for the bond market (even if Bill Gross sits on the sidelines).

Finally, it may pay to have a look at what is happening at the State and local government level when it comes to unfunded pension liabilities and the modifications that are coming from the General Accounting Standards Board (GASB). The era of relying on 8% return assumptions are no longer tenable in a world of sub-4% nominal GDP growth. Looking at the latest Fed Flow of Funds report, State and local government pension funds are sitting on an equity allocation of nearly 60%, but only have 6.5% of their financial assets in treasury, notes and bonds.

From the mid-1960s up until the mid-1990s, the bond share was consistently between 20-30% and moving back into this range would involve roughly $500 billion of an allocation shift towards the fixed income market. I highly urge everyone to read the article on page A2 of today’s WSJ titled Showing the Woes in Public Pensions.

Ignoring the demand for fixed income product would have left you with a dramatically incorrect forecast of where JGB yields were headed in the aftermath of its credit collapse two-decades ago. There were at least seven spasms to the upside, but the primary trend in bond yields was down.

For more from David’s 17 page Market Musings and Data Deciphering go HERE to subscribe for his FREE Reports (He also publishes a summary of his full report)

Go HERE to subscribe for his FREE Reports

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair