Daily Updates

Discovery

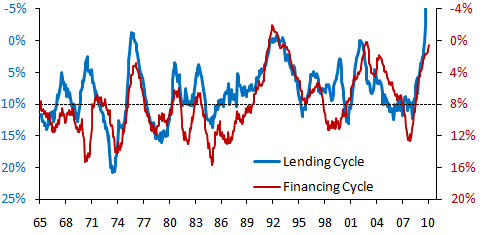

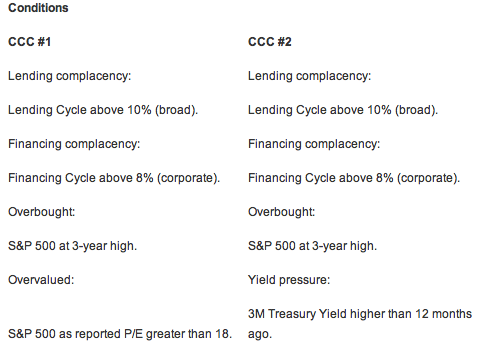

We unexpectedly discovered two sets of conditions preceding every major S&P 500 peak since 1965! We coined this signal the imminent Credit Complacency Crash – CCC. When these two sets occur, they have always (so far) indicated imminent major stock market crashes. We define a crash as a decline of more than -15%.

We believe our CCC model could have direct applications mostly in tactical asset allocation and risk management for institutional clients. How did we discover this innovative model? This time, we had the intuition of back testing both our Lending Cycle and Financing Cycle anticipatory indicators.

Both of these anticipatory indicators lead CB LEI Y/Y [Conference Board Leading Economic Indicator] by at least 12 months. Given the S&P 500 Y/Y lead Real GDP Y/Y by 3-6 months and CB LEI Y/Y had a consistent lead of 3 months over Real GDP Y/Y, we can estimate having between 6-9 months of lead on the S&P 500 when we combine both these indicators.

Note: Scales are inverted Source: EMphase Finance

Before we display our results, take note we observed these two sets of conditions on a monthly closing basis. We used S&P 500 data as reference. We trailed all these signals for six months except for the P/E in order to match sub-signals. We also eliminated multiple signals by only taking the first signal given.

Results

Take a look at the chart below. And no… We didn’t cheat by manually pinpointing S&P 500 peaks on an Excel spreadsheet. These are the actual and concise results from rules explained earlier. We believe these two sets of rules do make sense and respect our K.I.S.S. (Keep It Simple & Sweet) philosophy.

Source: EMphase Finance

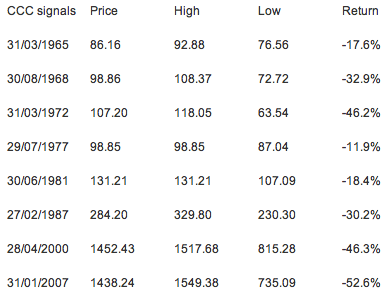

See below the summary of all CCC signals. First column is date of occurrence, second column is monthly closing price at signal, third column highest monthly closing seen following signal, fourth column is lowest monthly closing seen following signal and fourth column is the awful S&P 500 return seen:

The average decline following our CCC signal is -32.0%. Note the loss in 1977 is more than -11.9% and below -15.0% if we are taking daily data instead. Moreover, S&P 500 declined more than -15.0% in 1998 and we didn’t get a CCC signal but it is not an issue and debatable considering equity peaked in 2000.

Conclusion

How to exploit a CCC signal? When it happens, we suggest to closely monitor S&P 500 price movements with various tools for an imminent reversal. For example, simple technical indicators or sentiment indicators may help on a short-term horizon identify the right moment to adopt a more bearish stance.

Our CCC signal is probably one of the best indicators of S&P 500 peaks available and is yet undefeated with no false signal. Based on this model only, there is no equity meltdown in sight. This corroborates our view the U.S. economy recovered from the latest recession and is now back in expansion mode.

This article is part of our research U.S. Economics Monthly.

Disclosure: None

About the author: Francois Soto

Francois Soto is the President of EMphase Finance. EMphase Finance strives to become one of the most important websites in North America concerning quantitative analysis using traditional economic, fundamental and technical analysis.

Quotable

“No folly is more costly than the folly of intolerant idealism” – Winston Churchill

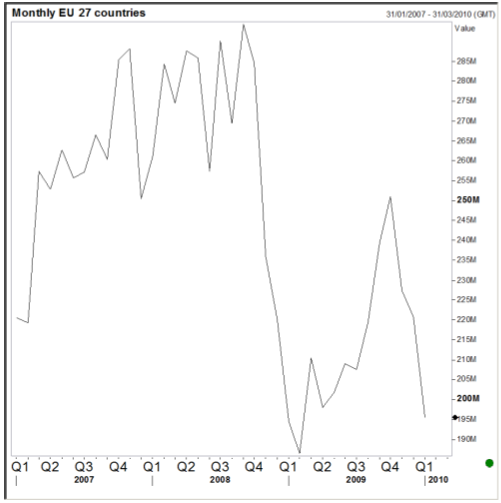

FX Trading – Can you say “contagion” boys and girls? Sure, I knew you could!

Okay, this morning I am going to present a series of charts. Let’s play: Guess that country? Here is a hint: It is not China.

Exports EU 27 Countries: Tank!

…..read more HERE

“Investors need to understand the long-term trends in stock valuations,” writes Dan Amoss. Starting valuation is crucial to your investing results. Overpaying for stocks near the peak of bull markets is a surefire way to lose money.

“One of the best methods of stock market valuation is based on the work of Yale professor Robert Shiller and his now-famous “Shiller P/E ratio.” The Shiller P/E ratio is calculated as follows: Divide the S&P 500 by the average inflation-adjusted earnings from the previous 10 years. Here is a chart of the Shiller P/E going all the way back to 1880:

“This is the best P/E ratio to use over long stretches of history, because it smoothes out the extreme peaks and valleys in earnings, giving a better framework for thinking about future S&P earnings power. The mean and median Shiller P/E since 1880 are both about 16. Today, it’s about 22. At the last four major bear market bottoms, in 1921, 1932, 1949 and 1982, the Shiller P/E fell all the way into the range of 5-10. This is a far cry from bouncing sharply off of 15 — which we saw at the March 2009 bottom.

“Valuation is the main reason why I expect the bear market to last several more years into the future — probably somewhere in the 2015-2020 time frame. I think we’ll get there through some combination of falling stock prices and modest earnings growth. Rising Treasury yields should drive stock valuations lower.”

If you’re worried about the next market correction, Dan’s your man. His Strategic Short Report readers are well prepared for the next leg down. Join his ranks HERE — for a limited time — for just $1.

…..read the topics below HERE

- How Greece has pushed gold to a new record high

- Congress quietly passes capital control laws… government tightens grip on money leaving I.O.U.S.A.

- Alan Knuckman on what’s really driven oil to $86 a barrel

- Dan Amoss offers “one of the best methods of stock market valuation”

- Plus, one step closer to war with Iran (or North Korea)… America’s latest nuclear declaration

U.S. Stock Market – My long standing belief we shall see DJIA 11,000+ is upon us. Any weakness in the market is likely to be short-lived as the “Don’t Worry, Be Happy” crowd knows how much they can milk such a feat.

As you know, I continue to look for economic growth at least through June/July and that should put a floor under any stock market correction. The “fantasy” in all this is to see several more hundred points added on into summer and then put on my growling bear suit again (which by then may may need to be taken in a little please God).

U.S. Interest Rates – Going substantially higher over time. I continue to suggest avoidance of any bond maturities over two years.

Gold and Silver – Going substantially higher over time (where have we heard that before?). Love them!

U.S. Dollar – The feeble countertrend rally continues and my target remains 83-84 on the U.S. Dollar Index. Anyone notice the Loonie at parity? From below 80, I’ve said it’s by far my favorite currency. Now will the Canucks have me eating crow this summer? Stay tuned.

Oil and Gas – At $90+, oil could become a tempting short but for now I remain on the sidelines. Natural gas could see below $3 this summer so continue to avoid.

Model Portfolio Thoughts

Fingers and toes crossed that Northern Dynasty Minerals *can finally make the $10 area a bottom versus a top. No news is good news on Continental Minerals*. Why? Because IMHO if there weren’t anybody knocking on their door, it would be in their best interest to do all they could to promote the further development of KMK. The fact HD remains deadly silent is to me good enough for my belief KMK is a takeover target.

After being in the doghouse, Nevsun has come roaring back and could make a new 52-week high in this move. Evolving Gold has put in a major bottom in my highly biased opinion. Stay tuned. East Asia Minerals appears to be on automatic pilot and is a prime takeover target. Be a strong holder.

*Were originally model portfolio selections but became clients of mine afterwards.

Client Thoughts

I had a lengthy discussion with Scott Cousens of Heatherdale Resources yesterday and he remains very optimistic on the company’s future. He believes the market read much too much into the last few drill holes and reminded me that we’re only in the first or second inning of a nine inning game. I think the current price gives those not yet shareholders a chance I honestly thought would never present itself again. To me, I wouldn’t look a gift horse in the mouth but I’m highly biased here.

Silver Quest Resources is consolidating after more than doubling in price on big volume. The Hard Rock Analyst came out with a write-up this morning on the company. In my mind, HRA is the #1 newsletter for junior resource companies. I continue to wait for data from Spanish Mountain Gold before doing a write-up. Sunridge Gold had great news recently and in my heart of hearts would be much higher if not for where it’s located. I believe it won’t end up mattering if results continue to be so good. Taseko Mines is firing on all cylinders and I highly anticipate new 52- week highs shortly. Finally, Timmins Gold is cheaper now relative to where it is on the corporate development ladder than any time since I first became involved with it.

On Major Moves, Peter Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website

To HERE Peter speak and others speak on Trading go HERE:

Gold — The large symmetrical triangle in gold that I’ve been focusing on is breaking out, and it’s breaking out to the upside. This is particularly bullish action, since gold is breaking out in the face of a strengthening dollar. Ordinarily, with the euro weak (Greece) and the dollar stronger, you’d think gold would be getting whacked. Not so, and that’s a huge plus factor for gold. – Richard Russell

John Licata: Gold Stands Its Ground

Tim McLaughlin and Karen Roche of The Gold Report

Gold prices continue to climb and John Licata, chief commodity strategist at Blue Phoenix Inc., says he sees reason to be optimistic about gold’s future. In this exclusive interview with The Gold Report, John says that as inflationary pressures present themselves, gold prices will continue their upward move. He also sees silver, platinum and palladium as interesting plays for investors.

The Gold Report: The price of gold is around $1,100. Last year you were saying the best buying opportunities were in the $850 range. Are you still recommending gold to investors?

John Licata: Yes I am. Wall Street has thrown the kitchen sink at gold, and for all intents and purposes gold could have fallen below $800 per troy ounce with the rally in the U.S. dollar and overall stock market. Yet gold maintained its resiliency and showed it can act independently of foreign exchange movements. That has me very constructive on the outlook for the yellow metal. We’re still holding on to $1,100—and I continue to maintain $1,375 as my target on gold for the rest of the year. Gold can benefit from increased geopolitical risk. Also inflationary pressures will start to reveal themselves later in the year. That will continue, especially in 2011 from various stimulus packages being unveiled or implemented over the next few quarters.

More and more, gold prices will be considered a currency in its own right. With that said, I think it’s going to replace the U.S. dollar as the ultimate hedge in terms of risk. Gold prices can continue to move higher, and $1,375 is just another stop on a train that I’ve been looking at for many years. That train has a long way to travel, but $1,375 is a level I’m very comfortable sticking with through this year.

TGR: If gold should really be trading at $800, why are you putting a $1,375 target on it?

JL: I don’t think it should be $800, but that’s what the market was suggesting. The market threw everything at gold. The price of the euro-dollar cross deteriorated, and yet gold held its ground. You heard about less risk of inflation, and yet gold held its ground. Nothing that the marketplace has thrown at it, including the stock rally, has taken gold prices down. If you were a seller of gold, you had your chances to take gold back down to $800 and now those chances are gone, in my view.

The fact that gold held its ground makes me think that, when the economy starts to show signs of life again—and I do see signs of inflation contrary to many indicators out there—gold prices will actually see a much bigger rise. Geopolitical factors will play a role, as well. Some nations don’t view the dollar as that global safe haven. A lot foreign exchange companies that have predominantly jumped on the dollar bandwagon think that the Fed is not going to raise rates anytime soon. If that’s the case, then maybe gold is more attractive; and I firmly believe that gold is.

TGR: You’ve said you expect to see a market rally in Q310 or Q410 as the unemployment rate potentially goes down. If there is a market rally and unemployment goes down, are you inferring that gold will go up because we’ll start to see inflation or because we have a market rally? In other words, what’s going to cause gold to rise?

JL: Gold will rise as more inflationary pressures present themselves. Only 40% of the stimulus package has actually been allocated. There will be a lot more government money allocated to various economies in the middle, and toward the end, of the year. We can see a lot of inflation—and not only here in the United States. Globally, we’re still trying to figure out what’s happening from the sovereign debt perspective. If we keep throwing so much stimulus into reviving economies around the world, then “hyperinflation” is a term that we’ll be really comfortable using in 2011.

Because I mentioned sovereign debt, we have to talk about Greece and how that situation could spill over into Portugal, or perhaps even Italy. Yet we have our own problems here in the U.S., with California perhaps coming up with a default of $20 billion. That’s another catalyst for gold—the fact that sovereign debt issues are being magnified right before our eyes even here at home.

TGR: Some analysts who recommend precious metals have actually talked about a complete collapse of the dollar. Do you see anything like that happening?

JL: I don’t know about a total collapse of the U.S. dollar. Look at the action we’ve seen in the dollar over the past year. If anything, I was concerned with a total collapse of the euro. There were some conversations about perhaps buying the euro on eBay someday. I don’t think that’ll ever happen; but, if there was a total collapse, it would happen to a non-U.S. dollar-denominated asset.

I don’t think the dollar is going to completely collapse. We still have a very resilient economy. Look at where we’ve been in the stock market just in the last year. I definitely want to point out that I don’t mean the stock market is a sole pointer of confidence, but I do think the stock market is forward-thinking.

What we’ve seen in the U.S. has definitely been more proactive than what we’ve seen in many other countries. The length of time it’s taken Europe to hash out a plan to save Greece has been a confidence deterrent—and the potential fallout from that is still unknown. That said, I don’t see the USD being the currency to get kicked out of any basket. A basket of currencies is something that could be discussed in the future. OPEC has actually talked about a basket of currencies for years so crude oil doesn’t have to be tied to the USD.

TGR: You’ve recommended investors hold physical gold rather than equities, as the latter tends to underperform the underlying commodity. Do you still prefer physical gold to equities?

JL: I do. There are some opportunities within the gold space that are intriguing still. A name that comes to mind that we’ve talked about in the past, and that I continue to be enthusiastic about, is NovaGold (NYSE.A:NG;TSX.V:NG). Just recently, they secured funding by Soros, as well as Paulson & Co. That’s a testament to the management and what they’re doing up north in Canada. Some of their individual assets are fantastic in their own right; but collectively they represent a very bright future for this company. For investors looking to play junior companies that have extremely bright futures, NovaGold might be the name to play.

TGR: Any other gold equities that you find attractive right now?

JL: Goldcorp (TSX:G;NYSE:GG) is still very interesting, as is Yamana (TSX:YRI;NYSE:AUY;LSE:YAU). And I do like other metals, such as platinum and palladium. Some of those names we’ve mentioned in the past, such as Stillwater Mining (NYSE:SWC), still has a lot of leg.

TGR: When you look at gold equities—or any other metals companies—what sorts of things do you look for specifically? Is management a big thing? Do you look at whether these companies do a lot of exploration? What are your criteria for choosing such companies?

JL: No matter what area, management credibility is definitely at the top of the list. Geography is also a major consideration. Investors shouldn’t jump into areas that might be politically unstable. Government friendliness toward foreign companies mining their land for economic gain is extremely important, as well. Companies that have great relationships with foreign governments are definitely high on my list. Low debt is something that isn’t often discussed when considering metals companies; so when you find those companies, you kind of embrace them because they’d have an easier time raising capital if they did find something.

Those are the main areas to look at—that and a breakdown of what they’re actually finding. Are they simply a gold player? Or are they a gold player that is a silver story? Sometimes investors get confused by the company names; they think that the word “gold” in a company’s name implies that it mines only gold.

TGR: Back in February you were optimistic about a metal called indium (see Blue Phoenix posting). Can you tell our readers about this metal and your take on the indium market?

JL: Indium is a fascinating under-the-radar minor metal that, in my opinion, could be major. Its uses are completely varied. It’s used in flat panel LCD screens, plasma TVs, cell phones, computer monitors, cameras, touch screens and new tablets like the new Apple iPad. It could be used in leading-edge thin-film solar PV cell technology.

The price of the indium recently traded a little closer to $600 per kilogram. That’s the highest level since October 2008. And there’s been speculation that China’s been building the reserves of strategically important minor metals such as indium. So I do believe that indium can be a major metal to be on the watch list.

Paul Otellini, the CEO of Intel (NASDAQ:INTC), has been quoted saying that, by 2017, the silicone processor will be replaced by possibly an indium-based compound that is actually faster than silicone. It uses less power than silicone. It’s much more efficient at processing 3D graphics, which many electronic devices are moving toward. Indium is going to be a great story in the future.

TGR: Are there specific indium companies that you’re watching right now?

JL: Unlike many other metals in the marketplace, there aren’t many companies that are specifically indium-focused. It’s usually something that develops when they’re looking for gold or silver, or they just happen to come across indium. It kind of resembles zinc. It’s a metal that could become a scarce resource over the next decade due to increased usage.

I typically don’t write about micro caps, but there’s a small company called Argentex Mining (TSX.V:ATX:OTCBB:AGXM) that has some really interesting properties in the southern Argentine province of Santa Cruz. It’s a very interesting play but, other than Argentex, there aren’t many indium-specific companies in the marketplace—at least not yet.

TGR: Where is indium being found? In specific geographic areas or worldwide?

JL: It’s not worldwide. There is some indium in Argentina, as I mentioned. China has one of the largest indium resources; Russia has some, too. Those are the biggest sources. The U.S. does not produce any indium whatsoever.

TGR: In the past, you’ve been bullish on platinum and palladium. Do you still think those are good plays for investors?

JL: I am and, being that I am so bullish on gold, I think that platinum and palladium are platinum group metals (PGMs) that will not only ride the coattails of the gold market strength but also establish themselves as unique metal plays. Recent launches of ETFs on those metals show that investors are gaining more confidence in them as individual metals—rather than metals used solely by automakers for catalytic converters. Both metals are also starting to see more use in jewelry, especially in Asia. Palladium is so much cheaper than gold. You can imagine that’s definitely resonating with the youth in Asia. They can get something that looks like platinum but is actually much cheaper.

TGR: What about platinum and palladium companies?

JL: I’m still a very big fan of Anglo American PLC (OTCBB:AAUKY). I like Lonmin (OTCBB:LNMIY). And, as I mentioned earlier, Stillwater Mining is a company I’ve mentioned in the past and still feel enthusiastic about.

One thing investors should keep in mind is that Stillwater’s contract with Ford Motor Company (NYSE:F) will expire at the end of 2010. There’s been some talk that the floor prices they have in those contracts are going to go away. Even if Ford does renew the contracts, it has no floor prices. That has helped the stock in the past because it’s made Wall Street much more comfortable with revenue targets. If those floor prices do go away, investors may look to ring the register on that name.

Regardless, I like the company longer term and believe there could be many buyers looking for the company’s platinum and palladium sources in the open marketplace.

TGR: You said that geographic factors were very important in choosing gold equities. Do you feel the same way about companies in the platinum and palladium sectors?

JL: If you’re looking at commodities, you have to. That concept goes across the entire spectrum.

TGR: Regardless of what business they’re in?

JL: It doesn’t matter if it’s energy, metals or bottling Coca-Cola. If a company’s not in a geographically and politically sound area, investors should think twice about investing in it.

TGR: You mentioned platinum and palladium were going to increase as gold takes off. What do you think about silver?

JL: In my opinion, silver has been gold’s evil stepchild for years. And I continue to view silver as an overlooked commodity. Uses of silver continue to increase, and I like the prospects of the metal very much. Right now, platinum and palladium are the sexy metals, so to speak, because the ETF is new. However, I think silver prices will surge above $20 by year’s end or in 2011.

TGR: Are you following any silver juniors?

JL: Sure. I have been keeping tabs on silver-focused names such as Hecla Mining (NYSE:HL), Ivanhoe Mines Ltd. (TSX:IVN) or Pan American Silver Corp. (NASDAQ:PAAS;TSX:PAA).

The volatility created by these ETFs is historically known to take the price of futures higher. You can apply that to crude oil, natural gas, gold or silver. Platinum and palladium are the new kids on the block that will benefit from the same concept. One of the reasons the Commodity Futures Trading Commission (CFTC) is looking to curb speculation is because it is a major driver of commodities these days.

Recently, a trader told me that if the CFTC puts regulations in place and limits the amount of contracts individual firms can trade, it might actually do more harm than good. That’s because more violent price swings can actually take place if there’s less volume. It was interesting to hear a trader say that. It makes me think that, as much as these ETFs seem like a blessing from above, they’re probably one of the worst things to happen to the commodities market.

TGR: Given what you’ve said, do you anticipate government regulations on these ETFs; and, if so, in what timeframe?

JL: Government has too much on its plate right now to handle everything at once. In a month’s time, we’ll be talking about the CFTC regulations on energy and metals. So I don’t necessarily think ETFs are right at the forefront of new legislation, but I do think it’s something we’ll hear about in the near future. There’s so much happening on the regulatory side in terms of energy prices and metals; concentration needs to be focused. As we saw with the healthcare plan, you can only do one thing at a time.

TGR: Of course. Thanks so much for your time, John.

John J. Licata is chief commodity strategist at Blue Phoenix, Inc., an energy/metals independent research and consulting firm based in New York City. He has appeared regularly in the media (CNBC, Bloomberg TV/Radio, Business News Network, Barron’s, etc.) over the years for his insights/forecasts in the commodity spectrum.

After studying economics and graduating from Saint Peter’s College (where he received the Wall Street Journal Award for economic excellence), Licata set his sights on Wall Street. During his more than 14-year career, John has held both trading and research positions on the NYMEX, Dow Jones, Smith Barney and Brokerage America. Early in 2005, he founded Blue Phoenix. John is presently in the EMBA program at New York University’s Stern School of Business. You can follow John on Twitter and LinkedIn.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair