Daily Updates

This brief comment below from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail: dennis@thegartmanletter.com or HERE to subscribe at his website

SHARE PRICES ARE REBOUNDING with sanity returning here just as sanity has returned to the forex markets following the beating administered by the Obama Administration’s naïve decision to release the Goldman suit information Friday morning. Saner minds are prevailing and wisdom is trumping naiveté once again. Our Int’l Index has risen 0.3%, much of which is from Asia this morning and part from N. American share dealing yesterday. Earnings season is now hard upon us, and we are expecting Apple’s earnings today, with the Street’s consensus running to or near $2.43 for the quarter compared to $1.33 a year ago. Bank of New York, State Street Bank and Mellon’s earnings top the financial services today, while J&J and Coca-Cola are the consumer products earnings reports of the greatest interest. After the close last evening, IBM reported, and although it “beat” Street estimates, it apparently did not “beat” sufficiently, with shares falling in the aftermarket.

What has our eye this morning is the overt weakness in steel shares in the past several weeks. It makes little difference what steel company one looks at, all are down and all are down materially… but importantly back to what we consider to be support. If “risk” is going back on the table we’d be reasonably intent upon taking that risk in the form of steel. Perhaps we should cast about looking for metals and basic materials ETFs. That may be the better choice rather than be open to the vagaries of individual companies and earnings “hits or misses:”

Chart posted by Money Talks

Back on Feb 10th, I picked ten stocks that could double in the next 12 months. The list is up an average 17%. With a little more than two months gone by, here’s a follow-up to those picks (Model portfolio has been updated).

Anooraq Resources Up 36% – The PGMs continue to perform well and it appears the investment world sees ANO as a true emerging major PGMs producer. Rating raised to outperform from market perform at Raymond James today.

Continental Minerals Up 12% – See past comment Unusual to see First Boston as an aggressive buyer of late-hmm…?

Crocodile Gold Down 17% – Firing on all cylinders corporate-wise. Weakness is an opportunity to put an aggressive emerging producer in most gold portfolios (keep in mind I’m very biased).

Donner Metals Nil – Drilling success continues. Further update hopeful soon.

Evolving Gold Nil – In several decades in and around the junior resource sector, I can’t recall a situation quite like this. Most juniors never even come close to having one world-class deposit let alone two. EVG is IMHO in possession of two yet many speculators and professional investors don’t have any real love for EVG’s management as a whole. This lack of love shows up in the share price as I believe it would be much higher if not for this supposed bad taste in many mouths.

Management has stated to me they are well aware of this and are addressing it. I suspect any such “mouthwash” should be applied before the drilling kicks off at the Rattlesnake project. Stay tuned.

Heatherdale Resources Down 18% – A lack of major promotion and analyst coverage at the moment has impacted the share price. We’re not even in the third inning yet but because the second inning of drill results weren’t as strong at the first inning out-of-the-box shot, some holders have thrown in the towel already. This is premature at the very least and quite possibly a gift to those who take their place now. A more detailed commentary can be anticipated from me in the not-too-distant future.

Nevsun Resources Up 21% – As it moves closer to commercial production, the share price can follow.

Rodinia Minerals Down 16% – Lack of fresh news and an overall quiet to down rare metals market in general, has led to RM’s share price overall weakness. I continue to believe RM can be more than just a player in this sector play.

Silver Quest Resources Up 115% – As good as it has performed, relative to where it’s many projects are versus where they were a few months ago, the stock appears still quite cheap. Its drill season window is only first opening now so we should have lots of news in the coming months.

Taseko Mines Up 43% – News on Prosperity is likely the next potential catalyst for the share price. Stay tuned.

On Major Moves, Peter Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website

To HERE Peter speak and others speak on Trading go HERE:

Market Summaries

S&P/TSX Composite down 0.09% to 12071 (up 2.80% year-to-date)

S&P/TSX Venture Composite down 0.08% to 1666 (up 14.28% ytd)

Dow Jones Industrial Avg up 0.20% to 11019 (up 5.70% ytd)

Nasdaq Composite up 1.10% to 2481 (up 9.30% ytd)

Oil (West Texas Intermediate) down $1.68 to $83.24 (up $3.88 ytd)

Gold (Spot USD/oz) down $24.60 to $1137.40 (up $40.45 ytd)

Commentary

Goldman Sachs Big Bet Against The U.S. Subprime-Mortgage Market – In a bluntly worded civil lawsuit, the US Securities and Exchange Commission alleges that Goldman Sachs and one of its vice-presidents, Fabrice Tourre, defrauded investors by misstating and omitting key facts about an investment instrument it developed that was tied to subprime mortgages. The allegations against Goldman Sachs Group Inc centre on the creation of a single security called Abacus 2007-AC1. Goldman has often been criticized for selling billions of dollars of debt securities, called credit default obligations (CDOs), filled with mortgages that the bank itself allegedly thought were overvalued. But like many controversies in the financial services industry, it’s not about what you know, or what you do, it’s about whether you tell anyone. That’s what makes Abacus 2007-AC1 special in the SEC’s eyes. It alleges that for this security, Goldman hired Paulson & Co to come up with a number of the mortgage-based contents. Two things about Paulson & Co: Firstly, Paulson had perhaps the biggest bet on a US housing market collapse and part of that bet was through shorting Abacus 2007-AC1. Secondly, Goldman allegedly didn’t tell anyone that Paulson helped build the same security the hedge fund was betting would fail. According to the New York Times, Goldman took most of its short positions on the Abacus securities before 2007. Goldman’s bets against the performances of the Abacus CDO’s were not worth much in 2005 and 2006, but they soared in value in 2007 and 2008 when the mortgage market collapsed. This glaring conflict of interest is at the centre of the SEC’s charges. The involvement of Mr Paulson and his company was “undisclosed in the marketing materials and unbeknownst to investors” the SEC said. Instead the SEC alleges Mr Tourre led investors to believe that an impartial firm, ACA Management LLC, selected all of the mortgage-backed securities in Abacus 2007-AC1. Essentially, Tourre designed the security to fail, while telling investors it was designed to succeed. Paulson’s timing couldn’t have been better, getting in just before the US housing market started its collapse. Beyond the headline, the thing that makes this situation even more stressful is the fact that Goldman Sachs is Wall Street’s most dominant investment bank, employing some of the industry’s smartest. Ordinarily, firms caught in the crosshairs of the SEC jump through hoops to avoid publication of charges that can cause significant damage to their reputation, which is why more often than not they opt for a settlement. However, it appears that SEC, with its newly invigorated Obama appointees is on a mission to distance itself from the previous regime and isn’t willing to play by the old rules. Any question about the impact of the charges were answered when Goldman’s stock price tanked more than 10% within an hour of the stunning charges becoming public, despite the firm’s insistence of its innocence and pledges to vigorously defend itself.

– excerpts from the Financial Post

Soundbites

- Here are a few “warm and fuzzy” stats surrounding Greece and parallels to the US: Greece has been in default 50% of the time since 1800. Aren’t they overdue for some carnage? The London Financial Times says Greece’s debt is 120% of GDP. The US government debt is 63% of GDP, according to Monday’s Wall Street Journal, and rising. It will reach 90% by 2020, says the non-partisan Congressional Budget Office, assuming the end of the Bush tax cuts don’t impede growth rates. Higher taxes – whether needed or not – do slow growth. Federal spending is almost 25% of GDP versus the longer-term average of 21%. The budget deficit as a percent of GDP is almost 10%. The US finds itself in a very tangled web and the problems are escalating.

- BC’s real estate market started and finished the first quarter strongly, cooling off through the Olympic stretch. According to MLS, the 7110 sales in March were 43% higher than a year earlier when the market was only beginning to pull out of the downturn. Through the entire three-month stretch, the province saw 18,284 sales, representing a 64% jump from 2009 stats. “Since the beginning of the year, we’ve seen home sales moderate,” said Cameron Muir, the BC Real Estate Association’s chief economist. “That is largely the result of pent-up demand that has already been expended in the marketplace as well as eroded affordability as higher home prices and more recently, higher mortgage interest rates are certainly squeezing some low-equity buyers out of the marketplace.”

- Russia and Argentina have ended years of ignoring one another and are now exploring numerous avenues to combine their resources. When Russian President Dmitry Medvedev stepped off his plane in Buenos Aires, it marked the first visit by a Russian head of state in 125 years to the Latin American country. Following successful talks with Argentine President Cristina Kirchner, the two signed numerous deals which will expand their economic ties. Trade between the two stood at just $2 billion in 2008 and was mostly comprised of meat, fruit and mineral fertilizers. The new deals will focus on oil & gas, ship building and possibly even arms trading.

- The Canadian Pension Plan Investment Board has announced plans to make significant investments in India. In what will be the first India-focused fund for the CPPIB, the board announced intentions to initially invest $100 million and ultimately grow the fund to approximately $450 million. The fund, to be named the Multiple Alternate Asset Management Fund, will invest in mid-sized Indian companies, management-led buyouts, and spin-offs of divisions from larger groups. The Toronto-based CPPIB currently manages $123.9 billion in assets, making it one of the country’s largest pension fund administrators. The profile of CPPIB is growing with the entity participating in three of the top five global private equity deals in 2009.

Marketwatch – A Look at the Week’s Newsmakers

Canadian Oilsands Trust (COS.UN) – shares shot up in Monday’s session after Houston-based ConcocoPhillips confirmed the sale of its stake in Syncrude Canada to Chinese refining giant Sinopec for $4.65 billion USD. Many believed that Canadian Oilsands would step up and buy this stake and this announcement now paves the way for a much-desired distribution increase. Syncrude Canada is now made up of the following consortium: Canadian Oilsands Trust (36.74%), Imperial Oil (25%), Suncor (12%), Sinopec (9.03%), Nexen (7.23%), Murphy Oil (5%), and Mocal (5%).

Apple Inc (APPL) – facing very high demand in the US market, Apple is about to disappoint Canadian fans with a reported one-month delay of the tablet device’s overseas launch. In a news release from the company’s Cupertino, California headquarters Apple claims to have sold more than 500,000 iPads, and taken “a large number of pre-orders for iPad 3G models for delivery by the end of April.” It expects sales will “likely continue to exceed our supply over the next several weeks.” Calling it a “difficult” decision, Apple will only begin taking online international pre-orders on May 10 (announcing at the same time the international price), with delivery delayed until the end of May. This is the second delay for customers living outside the US. In January, Apple said the iPad would be sold worldwide in late March. It started selling them in the US on April 3, but delayed the international launch until later this month. “We know that many international customers waiting to buy an iPad will be disappointed by this news, but we hope they will be pleased to learn the reason—the iPad is a runaway success in the US thus far.”

Khan Resources Inc (KRI) – after beginning the trading week at 83 cents, shares plummeted Tuesday on word that Khan’s takeover by China National Nuclear Corp (CNNC) may have hit some resistance. Shares in Tuesday’s session fell as low as 51 cents, far below the proposed buyout price of $0.96. Last year, Khan ran into trouble with Mongolian authorities and had a license suspended, which was followed shortly after by a lowball offer from a state-owned Russian company that Khan rejected. The company worked hard to get the suspension lifted and worked out the aforementioned deal with CNNC this past February. But according to Khan’s CEO Martin Quick, Russia has been working behind the scenes to squeeze Khan out of the Mongolian operations, despite the bid from the Chinese. This mess is far from over.

Canadian Pacific Railway Ltd (CP) – there is no clearer sign of an improving economy than measuring rail volumes and if the latest data is a signal, we are in the midst of a significant rebound. Canadian railroads reported 74,686 carloads last week (up 31% from the previous year) and 44,046 trailers or containers (up 17.4% form 2009). While these results are indicative of how bad 2009 was, it is still extremely encouraging to see so much product being shipped. Year to date, overall rail volume is up 16.9% from the first 14 weeks of 2009 and the percentages continue to expand.

“Quote of the Day”

“Sometimes I lie awake at night, and I ask, “Where have I gone wrong?” Then a voice says to me, “This is going to take more than one night.” – Charles M. Schulz (1922 – 2000), Charlie Brown in “Peanuts”

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

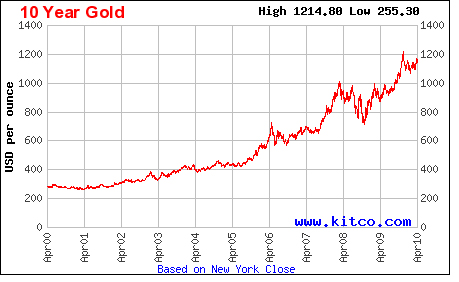

Gold $1,130 – Since just above $300, gold has climbed a wall of worry and denial. You wouldn’t need more than your hands and maybe a few toes to count the number of “experts” who have stayed the bullish course along the way. The road is littered with former gold bulls and perma-bears, all of whom predicted gold’s demise (many more than once).

Once again we find ourselves at one of those speed bumps…only this time the supposed land mine is one of those claims that just makes you laugh at the extent some go to in futile hopes of stopping the mother of all secular gold bull markets. The latest charade is the fear Paulson will have to sell his gold holdings because of the Goldman charges. While I would expect such nonsense from the “Senior Analyst” (he ran out of legitimate excuses hundreds of dollars lower ago), I find it amusing (but not surprising) that this lame excuse has caused some real grief.

Hello? Do you honestly think the rise in gold has been thanks even in part to Paulson? Sure, he has purchased some credible positions in it, but I highly doubt without him having done so we wouldn’t be at this point anyway. Oh, and by the way, even if his fund was somehow force to sell (the chances of which I believe are slim and none), it’s my understanding that there’s a three-year freeze on redemptions.

If I told you once I told you a thousand times, the financial world and the media that covers it hate gold. It will never be widely accepted because ownership of it flies in the face of what makes their world go around – stocks and bonds. This secular gold bull market takes no prisoners and this time will be no exception. I believe the latest naysayers (not the permanent ones like you know who) will end up joining an ever-increasing list of bears who end up mauled by the big and bad gold bull.

On Major Moves, Peter Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website

To HERE Peter speak and others speak on Trading go HERE:

The Bottom Line:

Now is the time to START taking at least partial profits in a wide variety of seasonal trades that reach the end of their period of seasonal strength in May including seasonal trades in the market and in sectors (including seasonal trades in platinum, silver, mines & metals, energy, oil services, consumer discretionary and materials). Profit taking on strength is preferred.

U.S. equity index futures are lower this morning. S&P 500 futures are down 5 points in pre-opening comments. Equity markets around the world are responding to continuing concerns on several issues including the SEC charge against Goldman Sachs, continuing concerns about Greece’s sovereign debt and fallout from the volcano eruption in Iceland. Weakest international equity index overnight was the Shanghai Composite Index, down 4.8%. And now the latest news! This morning, the United Kingdom and Germany opened investigations on Goldman Sach’s corporate finance activities. In addition, negotiations with Greece on a possible bailout have been delayed due to travel disruptions related to the volcano eruption in Iceland.

European based airline stocks are down sharply this morning. Commercial flights throughout northern Europe no longer are flying due to concerns about possible damage to aircraft if they fly through volcanic ash.

Goldman Sachs slipped another 2% in overnight trading.

The U.S. Dollar strengthened and the Euro weakened on overnight events. Commodities priced in U.S. Dollars including crude oil, gold, silver and copper traded lower.

Index futures moved lower despite better than expected first quarter earnings released this morning by Halliburton, M&T Bank, Hasbro, Eli Lilly and Citigroup. Only Citigroup moved higher on the news.

Cenovus fell 2% after BMO Capital downgraded the stock from Outperform to Market Perform.

Economic News This Week

Economic news is positive again this week.

March Leading Economic Indicators to be released at 10:00 AM EDT on Monday is expected to improve 1.0% versus a gain of 0.1% in February.

March Producer Prices to be released at 8:30 AM EDT on Thursday is expected to increase 0.5% versus a decline of 0.6% in February. Core PPI is expected to increase 0.1% versus a 0.1% increase in February.

March Existing Home Sales to be released at 10:00 AM EDT on Thursday are expected to increase to 5.30 million units from 5.02 million units in February.

March Durable Goods Orders to be released at 8:30 AM EDT on Friday are expected to remain unchanged versus a 0.9% gain in February. Excluding transportation, Orders are expected to increase 0.8% versus a gain of 1.4% in February.

March New Home Sales to be released at 10:00 AM EDT on Friday are expected to increase to 320,000 from 308,000 in February.

Earnings Reports This Week

Expect lots of good news!

Monday sees Citigroup, Eli Lilly, Halliburton and IBM.

Tuesday sees AK Steel, Apple, Coca Cola, Goldman Sachs, Johnson & Johnson, State Street, Teck Resources and Yahoo.

Wednesday sees Abbott Labs, Amgen, AT&T, Boeing, EBay, Encana, Freeport McMoran Copper & Gold, McDonald’s, Morgan Stanley and Wells Fargo.

Thursday sees Amazon.com, Capital One, Celestica, Microsoft, Pepsico, Philip Morris, Union Pacific and Verizon.

Friday sees Honeywell and Travelers.

Equity Index Trends

The ratio of S&P 500 stocks in an uptrend to a downtrend increased last week from 7.22 to (410/54=) 7.59. However, it deteriorated slightly on Friday. The ratio remains intermediate overbought.

Bullish Percent Index for S&P 500 stocks increased from 86.00% to 87.00% last week and remained above its 15 day moving average. The Index remains intermediate overbought, but continues to trend higher.

Ed Note: 5 of the 46 Charts Don Vialoux analyzes below. Go HERE to view them all.

The Dow Jones Industrial Average improved 21.31 points (0.19%) last week. It reached an 18 month high on Thursday. Intermediate trend is up. Short term momentum indicators are overbought and showing signs of rolling over. Seasonal influences are positive, but approaching the end of their period of seasonal strength in May. Strength relative to the S&P 500 Index remains negative. Intermediate downside risk is to its 50 day moving average currently at 10,598.20.

The TSX Composite Index fell 106.18 points (0.87%) last week. The Index reached an 18 month high on Thursday. Intermediate trend is up. Short term momentum indicators are overbought and have rolled over. Seasonal influences remain positive. Strength relative to the S&P 500 Index remains negative. Intermediate downside risk is to its 50 day moving average currently at 11,847.41.

The U.S. Dollar slipped 0.15 last week and tested support at 79.51. Resistance has formed at 82.24. Short term momentum indicators continue to trend lower. ‘Tis the season for the U.S. Dollar to move lower.

Gold has a brief period of seasonal strength in the month of May. However, its best seasonal sweet spot is from August to December.

Silver’s seasonal strength is approaching an end in May.SI) Seasonal Chart

Go HERE to view all 46 Charts and Commentary

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Don earned his Chartered Market Technician (CMT) designation from the Market Technician Association in 1995. His CMT paper entitled “Seasonality in Canadian Equity Markets” was published in the Spring-Summer 1996 edition of the MTA Journal. Don also has extensive experience with Exchange Traded Funds (also know as Index Participation Units) as well as conservative option strategies. In 1990 he wrote a report that was released in the International Federation of Technical Analyst Journal entitled “Profiting from a Combination of Technical and Fundamental Analysis”. The report introduced ” The Eight Phases of the Stock Market Cycle”, an investment concept that continues to identify profitable entry and exit points for North American equity markets. He is currently a member of the Toronto Society of Fundamental Analyst’s Derivatives Committee. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair