Daily Updates

Greece’s crisis at critical phase, likelihood of a disorderly outcome has risen dramatically in the last 48 hours.

Which New Technologies Will Increase Oil Recovery Margins?

The Energy Report: When you were speaking with your friends and clients at the Small Explorers and Producers Association of Canada (SEPAC) Showcase a few weeks ago, what were the issues they wanted to discuss?

Bruce Edgelow: In most cases, the comments centered on the encouraging application of new technologies that have transformed the resources-versus-reserves landscape. The revised view reflects the idea that broader oil and gas (O&G) resources may be available for extraction over time, if enough capital is available. We can now go into a reservoir and apply different completion processes to take advantage of a whole new technology frontier. That would be one thing.

Attendees were also interested in hearing more about the service industry’s capacity going forward. How would we manage if both commodities, natural gas and oil, experienced an uptick in prices? Could we actually fund growth through the use of services? There’s growing concern that the industry doesn’t have enough human capital to deploy on equipment. The services industry is starting to be really pressured with respect to having the right people and talent with the right supervisory skills on the drill rigs.

Merger opportunities have also been a hot topic. One of the notations I made in the presentation was about the size of asset the equity investor is seeking. In the past, we often talked about 1,000 barrels per day (bpd) in order to be a starting junior; but now investors probably need 5,000 bpd with a good management team that has run both oil-weighted and gas-reserve opportunities.

The other general conversation is the need to grow. We are a fast-depleting resource industry. On average, we are depleting our resources at 15%–20% standing still—even if we don’t show up. Whether we’re public or private, there’s a desire to be able to grow incrementally versus the depletion rate that’s taking place. How do you then grow yourself over and above that and provide attractive returns to investors? So, some of these are new discussions, but a lot of them are ones that we have every year because they are ongoing strategic issues.

TER: Bruce, the large gas producers can make about a buck per thousand cubic feet (Tcf) of natural gas in the $4–$5/Tcf range. But, as you told the group at SEPAC, summer’s going to be a very tough time for juniors. What are you telling the smaller guys? How do they survive such low natural gas prices?

BE: We’ve been in this price regime for the last 18 months, and the reality is that those discussions have been going on for quite some time. It’s not a change. In this community, there’s a lot of patience in terms of not forcing assets up for sale. By doing so, we would just drag the whole marketplace down. Collectively, the view is that we are closer to a recovery; however, we may still have a long way to go. So, we have been hard at work reducing general and administrative (G&A) expenses at stranded companies in the natural gas-producer community to attract expansion investment, even if it’s at the margin.

But it’s very difficult. Entrenchment creeps in to executive mindsets, which limits the willingness to sell at a reduced price, thereby eliminating their jobs at a time when it might be difficult to raise funds and start again. While we may be closer to natural gas-price recovery, we can’t avoid the reality of a low summer gas environment.

We’re touching base with a few of these entities on a quarterly basis just to make sure that the strategy we outlined 12 or 18 months ago is still underway. To be honest, it’s just a continuation of something that we’ve been at for the last two summers.

TER: Are you open to carrying or helping a client through these low points?

BE: Absolutely, and this is shared across the broader lending community. I could point to a variety of files, public or private, where we’ve hung in there and demonstrated phenomenal support. This is driven by the reality that you have to put out an inordinate amount of new capital to offset losses. We can never charge enough to recover an absolute loss on the debt portfolio.

By cashing-in on a low-price environment, you just create a new bottom or new low watermark for the price of the reserves. So, if you can provide a sense of reasonableness to the broader community of being able to work with the companies through this process, you will forestall any scavenger attempts by the stronger entities. With a growing sense that we’ll start to come out the other side on natural gas in the next 12–18 months, there’s no incentive for us to create a new bottom.

TER: That brings to mind a question. Does ATB ever take an equity position in companies, or would that be totally outside your business model?

BE: We have provided a significant amount of patience and support to a stalled, public nat gas junior over the past two years. We recognized that cash was dear to the company and instrumental to growing its reserve base, so we took equity back in payment of fees that were due to us. In the first case, it was warrants to purchase shares. In the second case, it was straight out issuance of shares. This structure gave the company time to develop an oil story. We were cognizant of where cash was needed, and we took some equity back. That was a new one for us. When I was at another financial institution, those situations were more common.

TER: The energy-lending business in Canada reached $25 billion by the end of October 2010. That’s up from $14B in 2005—a near 80% increase. Your firm, ATB, has a $5.3B portfolio, which works out to a significant chunk of the Canadian energy debt. What accounts for this increase in leverage?

BE: There’s probably been twice the amount of equity support over and above what the debt support has been. First, the balance sheets have been cleaned up and improved with merger and acquisition (M&A) activity and equity coming in. So, we’ve really cleaned up the over-leveraged situation weighing on the industry prior to 2006/2007 period. That meant the balance sheets were capable of taking on more debt if it was required for growth. The fact that we’re in a historically low interest-rate environment makes leverage economical. You can raise debt capital at rates that are less than what your capital expectations are on the shareholders’ side. The cash flow being generated from the oil regimes has allowed the leverage factors to come up. So, we’re still in a good healthy debt-to-equity relationship. Again, it’s new equity coming into the business that has reduced leverage, allowing clients to go back into their lines of credit when appropriate.

TER: As a banker, do you think of the juniors and the mid caps as being in nearly separate industries? How does the due diligence process for lending vary between these two groups?

BE: To be fair, the only piece that does creep into the smaller ones is the question of whether the company is concentrated into a single resource type that provides less flexibility than a larger-cap, mid-cap or senior producer would have. What running room is in front of them? If they’re going to tap out that resource potential, where might they grow to from there? So, that would be one piece that we’d pay particular attention to in smaller entities.

TER: Could rising debt in small- and mid-cap companies be indicative of a bubble?

BE: No, I wouldn’t suggest that. If we have a rising debt capacity, it’s because the resource type is in fact capable of managing it. When clients get to 40,000–50,000 bpd, they have a capacity, they have a balance sheet and they have an asset base that’s considerably varied and diverse. From that point in time, the leverage is managed through a financial covenant regime, which historically, would be a debt:cash flow ratio of 3x. That’s the rule of thumb. Junior companies’ reserves are expected to support their lines of credit via a borrowing base covenant. The lender takes a forward view of production, commodity prices and burdens, such as royalties and G&A, and lends on a margin of the net present value (NPV) of this calculation. The larger, more-senior companies’ historical cash flow serves that purpose. So, it’s not a bubble, per se. The reserve-exploitation strategy is being deployed prudently, and the companies are capable of being lent more money.

TER: Asian demand for oil, primarily from China, is expected to continue growing at more than 6% per year, and you are forecasting that crude will remain above $100/barrel (bbl), but choppy over the next few years. Given that 6% growth in Asia, that sounds conservative.

BE: I would agree. It is very conservative. The reality is that we have a lot of unknowns. For the first time in a long time, the OPEC group sitting around the table on June 8, 2011 couldn’t come to a consensus on output. I also question whether China will be the real demand driver. What about the other regions—India or Japan, as it rebuilds? I think there’s real reason to be conservative in the approach. Some of us have learned from the past, and we don’t want to race ahead and provide a more opportunistic, or for that matter, negative view of things.

TER: For the sake of this discussion, assume that crude oil hits $150/bbl over the next five years. Are you and your group positioned to fund renewable or alternative energy production?

BE: We are constantly on the lookout in these areas as energy prices move outside economic boundaries and where, from an economic perspective, alternative energy would be required. Our organization, in particular, has a real penchant for staying on top of these opportunities. We attend most of the alternative energy conferences to find technology that has been proven and has enough equity support to get through testing and the buildout phases. We want to provide whatever support is needed to birth these new industries. It’s critical. The changes come quickly, and they are not without risk, but we are excited about the variety of opportunities. So, yes, $150/bbl oil will accelerate this process, but these advancements are coming regardless. So, it’s incumbent upon anyone in this business to stay on top of emerging industries in order to participate at the earliest possible opportunity.

TER: The geothermal industry, in some ways, is technologically similar to your current industry segments.

BE: Yes, they’re significant. If you look at the geothermal technology being applied, it’s been there for quite some time; so, it’s not new science. It’s a great time to be optimistic for this business.

TER: I notice that 30% of your debt portfolio is utilities and service providers. Just from what you said at SEPAC, it sounds like you’re thinking about working with some of these engineering firms to potentially clean out tailing ponds. This could be very important for the development of oil sands.

BE: It’s critical. That technology has already been tested and is available to us, but may not be scaled up to total oil sands application today. There’s a great expectation that in three to five years, the tailings ponds will be a thing of the past and new technology will enable safe delivery of the waste to a landfill. So, we’re paying close attention to those service providers with respect to the new technology. At $60/bbl oil, these weren’t economical; but at $90–$110/bbl, these are very economical and are being developed. There is a lot of equity support behind it. We like to be green, we like to be energy efficient and we’d like to get rid of the whole tarnish of dirty oil.

TER: Sticking with the technology theme here for a moment and going back to traditional O&G production, which companies are some of the shining examples of using technology in an innovative and productive way now?

BE: We’ve seen a real consolidation in the services business to allow for economies of scale. I’d be remiss to point out anyone in particular; but, from a Canadian lens, you could look at the likes of Trican Well Service Ltd. (TSX:TCW), Schlumberger Ltd. (NYSE:SLB) or Calfrac Well Services Ltd. (TSX:CFW) on the oil field-services side.

TER: Great. Do you have any thoughts to leave with our readers?

BE: We think the technology’s here to stay. We spend a lot of time dealing with independent, third-party engineering reports to gather expertise. The encouragement we’re seeing is based on the new methods of additional recovery—miscible floods or more waterflood work, for example—that allow us either to continue to work on fields or go back into wells that have been suspended, and then apply the new technology. We’ve seen companies go back downhole and go from a 20% to a 30% recovery stage.

When you look at the total reserves in place across the basin of the North American marketplace, with our newer abilities to manage depletion or do a better job of recovery, it is phenomenally encouraging. These secondary and tertiary recovery methods are being applied today across more of the resource types than we’ve ever seen before. Think about the past, when we pulled some 15% of reserves out of the ground. Now, move that number to 20% based on new technology. There’s phenomenal impact to the entire basin with no drilling or exploration costs associated. There are no above-hole costs. It’s simply a downhole application. So, there’s less capital expenditure and the impact is significant.

TER: So, if you get an additional 5%, that increases the margin dramatically?

BE: Yes, just phenomenally.

TER: This has been very educational. Thank you very much, Bruce.

BE: Thank you.

Bruce Edgelow is responsible for the leadership and growth of ATB Financial’s energy business and capabilities. Before joining ATB, he was a senior Royal banker and has more than 39 years of experience with a focus on the oil and gas industry. Bruce is a Fellow of the Institute of Canadian Bankers, a member of the Calgary Petroleum Club and is a very active participant in community and church activities. Bruce leads a team of over 30 energy-industry professionals making ATB’s energy group one of the largest units in Canada. His team specializes in all aspects of the energy market, including oil and gas exploration and production, drilling and oilfield services, pipeline and utilities and midstream. Over the past several years, ATB’s energy group has grown to become a significant leader in Alberta, largely due to its focus on developing highly responsive relationships.

Small Explorers and Producers Association of Canada (SEPAC) Showcase Sponsors

Argosy Energy Inc. (TSX:GSY)

“GSY’s strategic land in the emerging Alberta Bakken play provides investors with some of the best leverage to a new Bakken discovery area.” Stacey McDonald, GMP Securities (4/12/11)

Bellamont Exploration Ltd. (TSX:BMX.A)

“. . .our target price already infers one of the hightest expected returns in our coverage universe.” Dan Payne, National Bank Financial (6/2/11)

Birchcliff Energy Ltd. (TSX:BIR)

“Volumes bested our forecast, with Birchcliff exhibiting 19% production growth year-over-year.” Robert J. Fitzmartyn, First Energy Capital (5/20/11)

Canada Energy Partners Inc. (TSX.V:CE)

“. . .encouraged with the retest results from the original Portage well and believe that there may be additional upside in the three untested formations.” Peter Doig, GMP Securities (3/16/11)

Cequence Energy Ltd. (TSX:CQE)

“Further expansions are certainly likely as the Company begins to define the resource footprint of its Montney and Wilrich (and exploration) prospects.” Robert J. Fitzmartyn, First Energy Capital (5/13/11)

Galleon Energy Inc. (TSX:GO)

“. . .cash flow is expected to grow.” Jason Bouvier, Scotia Capital (5/26/11)

Palliser Oil & Gas Corp. (TSX.V:PXL)

“. . .development will be ramping up, including 15 wells to be drilled.” Tim Murray, Jennings Capital (5/19/11)

Open Range Energy Corp. (TSX:ONR)

“The upstream business continues to realize a top-tier cost structure.” Dan Payne, National Bank Financial (6/2/11)

Paramount Resources Ltd. (TSX:POU)

“. . .numerous positive catalysts on the horizon.” Cody Kwong, First Energy Capital (6/2/11)

Strategic Oil & Gas Ltd. (TSX:SOG)

“. . .well positioned to keep this momentum going.” Alistair Toward, PI Financial (6/3/11)

Sure Energy Inc. (TSX:SHR)

“. . .second half of the year to be extremely active.” Aaron Swanson, Dundee Capital Markets (5/26/11)

Trilogy Energy Corp. (TSX:TET)

“. . .exceeded our production and cash flow forecasts for the quarter.” Roger Serin, TD Newcrest (5/24/11)

Yoho Resources Inc. (TSX.V:YO)

“. . .virtually unrivaled leverage to resource capture.” Robert Cooper, Mackie Research (5/26/11)

Primary Petroleum (TSX.V:PIE)— is focused on the acquisition of prospective oil and gas acreage in Montana. Currently Primary holds more than 170,000 net acres (266 sections) in Bakken prospective areas.

Richard Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe.

Brief Excerpt from Richard Russell:

Where, oh where is the stock market going? Today’s site could be a shocker. The pros follow the S&P so lets do like the pros. The chart below is a daily of the widely-followed S&P. First, we see a head-and-shoulders top delineated with three red arrows. Support was broken when the S&P fell below the upper blue support line.

The next and critical question is: “Will the S&P break below its March low,” which we see as the second (lower) support line. We’ve seen the S&P sink on seven consecutive weeks, which should mean that it is severely oversold. I’m guessing that the March low will hold.

Now –The case for a reversal and a bullish rally. The Dow has fallen on six consecutive weeks. This is highly unusual, and the odds for a seventh weekly decline in the series are slim.

During the past seven weeks my PTI has finally issued a sell signal, but after dropping for 27 points, my PTI is oversold.

Recently we have experienced two 90% panic-type down days (June 1st and 6th) on the NYSE which served to reduce a lot of the overhanging supply.

With three 90% panic-type down days in June, the overhanging supply of stocks has contracted. The decline in the Transports today adds mystery to the picture of the free-falling Dow.

The latest issue of Time magazine flashes on the cover, WHAT RECOVERY? There is an accompanying picture of the dollar falling apart. By the time one of the national magazines puts its opinion on the cover, the move or the trend referred to is usually over.

When what’s happening is not clear, best to stay clear of the stock market. Gold holds stubbornly well above 1500.

Is the Market Set for a Replay of 2008?

Eerily, the crash in 2008 began from the same levels as the S&P is at currently.

Technically, the crash was triggered by a false breakout over a short-term declining trendline which mirrors the May 31 false breakout and ensuing accelerated downside momentum that began on the Solar Eclipse on June 1. False signals are more powerful than true signals.

See the daily chart of S&P from 2008 here and the daily chart S&P from May 2 below.

….view the chart and read more HERE

Click on Chart for Larger image:

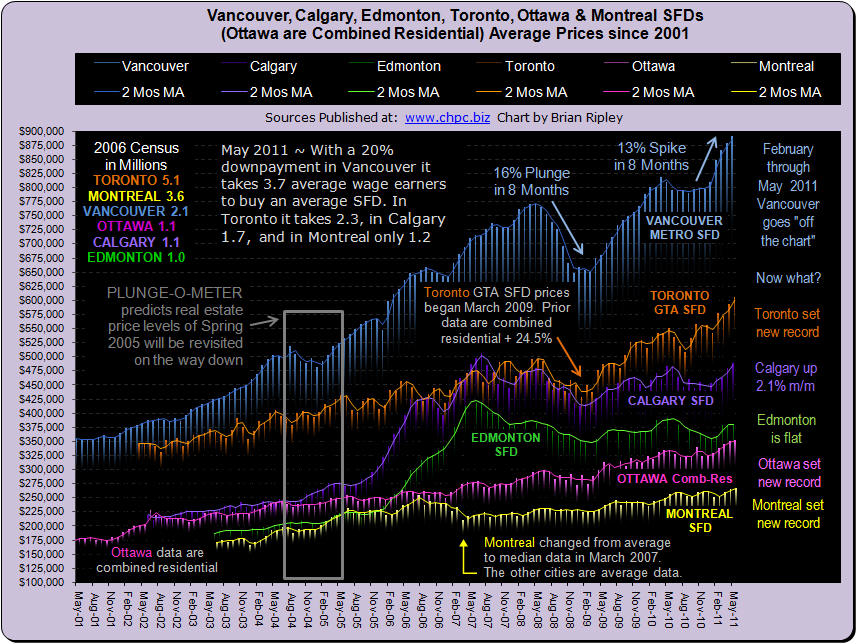

Bank of Canada Mark Carney in a speech to the Vancouver Board of Trade issued a sharp warning that the Canadian Housing Market is extremely vulnerable to a decline, a decline which will put the financial system at risk. Even as growth in mortgage credit has started to slow and prices are expected to moderate, investment in residential properties nationwide is now near “peak levels”, the Governor said.

“The risk is that expectations become extrapolative, prompting the classic market emotions of fear and greed – greed among speculators and investors, and fear among households that getting a foot on the property ladder is a now-or-never proposition.”

Recent data from the Canadian Real Estate Association report shows that Vancouver, where the average selling price is now 11 times higher than the average household income, isn’t the only market that’s overvalued. Housing is also at All-Time Highs in Toronto and Montreal with gains of 8.7 per cent in Toronto and 6 per cent in Montreal. Ottawa is also at all-time highs. Nationally prices rose 8.6 per cent in May to $376,820 from $346,950 compared to a year ago

Carney came as close as any central banker ever could on Wednesday to saying some parts of the Canadian housing market are in a bubble with some cities prices now 13 per cent above their pre-recession peaks, He also basically said there’s not much the Bank of Canada can do to stop the frenzy. Without saying the Bank of Canada will take specific measures to tame the sector, Mr. Carney left little doubt that he is concerned.

“Some excesses may exist in certain areas and market segments.” “Do we obsess about specific real estate markets in Canada? No, Our job is to manage policy for the country as a whole.”

Regarding Stimulus: “some (of the stimulus will ) eventually (be) withdrawn.”

Households “highly vulnerable to an adverse economic shock” have risen to the highest in 9 years.

Banks are also highly vulnerable, with real estate loans now making up more than 40 per cent of Canadian banks’ assets, compared with 30 per cent a decade ago, a situation he called “unprecedented exposure.” “Housing excesses could generate important vulnerabilities in the financial system,”

“One cannot totally discount the possibility that some pockets of the Canadian housing market are taking on characteristics of financial asset markets, where expectations can dominate underlying forces of supply and demand,” Mr. Carney said.

No market goes up forever. Every market is subject to bull and bear phases, even Canadian Housing.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair