Stocks & Equities

Most Asian stocks fell, dragging the regional benchmark index lower for a second day, after U.S. consumer confidence unexpectedly dropped this month.

Industrial Bank of Korea sank 4.6 percent as South Korea government sells 13.2 million of shares in the lender. BHP Billiton Ltd. lost 0.9 percent in Sydney after copper prices fell for the first time in more than a week. Rakuten Inc. surged 10 percent after the website operator said it will increase its dividend following a plan to move its listing to the First Section of the TokyoStock Exchange.

The MSCI Asia Pacific Index declined 0.1 percent to 141.46 as of 9:32 a.m. in Tokyo, as two shares fell for each that rose. The gauge gained 9.5 percent this year through yesterday as central banks around the world pledged to leave interest rates near record lows for a prolonged period. Futures on the Standard & Poor’s 500 Index were little changed.

“Data on balance still looks murky,” Matthew Sherwood, head of investment markets research in Sydney at Perpetual Ltd., which manages about $25 billion, said by e-mail. “Most importantly, there was a surprise decline in the Conference Board’s measure of consumer confidence.”

The MSCI Asia Pacific Index yesterday traded at 13.9 times estimated earnings, close to the multiple of 14 reached on Nov. 18, which was the highest since May, according to data compiled by Bloomberg. That compares to a current multiple of 16.3 on the S&P 500 and 15.1 for the Stoxx Europe 600 Index.

Regional Gauges

Japan’s Topix index fell 0.4 percent. Australia’s S&P/ASX 200 Index was little changed and New Zealand’s NZX 50 Index added 0.1 percent. South Korea’s Kospi index lost 0.2 percent. Markets are yet to open in China and Hong Kong.

More than $8 trillion has been added to the value of global equities this year, the biggest increase since 2009, as central banks took steps to shore up economies worldwide. The S&P 500 is poised for its best annual performance since 1998, with an increase of 26.4 percent through yesterday. Three rounds of Fed bond purchase programs have helped push the S&P 500 up 166 percent from a bear-market low reached in 2009.

The Conference Board’s consumer confidence index fell to 70.4 in November from a revised 72.4 in October, which was stronger than initially estimated, the New York-based private research group said yesterday. The median forecast in a Bloomberg survey of 78 economists called for a November reading of 72.6.

Hong Kong

Contracts on Hong Kong’s Hang Seng Index dropped 0.4 percent in the most recent trading session, while Hang Seng China Enterprises Index futures declined 0.5 percent. The Bloomberg China-US Equity Index of the most-traded Chinese stocks in New York climbed 0.8 percent yesterday.

Sayuri Shirai, a Bank of Japan board member who voted against a report at the bank’s Oct. 31 meeting, speaks to reporters today in Tokushima.

Bank of Japan Governor Haruhiko Kuroda helped drive a 46 percent surge in Japan’s Topix this year by maintaining monetary easing as he and Prime Minister Shinzo Abe sought to jolt the nation out of 15 years of deflation. The Topix is the best performing of 24 developed markets tracked by Bloomberg, on course for its biggest annual advance since 1999.

U.S. stocks pared gains in the final minutes of trading yesterday before changes in MSCI Inc. indexes, offsetting a rally among homebuilders and technology shares. The Nasdaq Composite Index topped 4,000 for first time in 13 years. The S&P 500 added less than 0.1 percent to 1,802.75, after earlier rising as much as 0.3 percent.

The U.S. flew two unarmed B-52 bombers into a disputed air-defense zone claimed by China, the first test of China’s response amid escalating tensions in the region that have implications for international air travel.

The flight of bombers into China’s newly claimed zone occurred without incident, according to a U.S. defense official. The area includes three islands in the East China Sea that are owned by Japan, a major U.S. ally, and have been at the center of a dispute between Asia’s two biggest economies.

To contact the reporter on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net

To contact the editor responsible for this story: Sarah McDonald atsmcdonald23@bloomberg.net

“Those of us who have been in combat during any war know the idiocy and tragedy of a world where man is pitted against man. My feeling is that at some future time, we will look back at the current age and shake our heads at its savagery and stupidity … The changes coming, I am convinced, will be harsh. And in the end, for the better of mankind.

The Godfather of newsletter writers, 89 yr old Richard Russell who has never taken a day off since he began writing in 1958 went on:

A few thoughts about gold. Never buy gold for a profit, gold is a measure of wealth. Count your gold holdings in the number of ounces, not the current worth in dollars. You don’t price the home you live in every day, or with each passing week. Nor should you price your gold holdings in dollars with each passing day. Gold is a timeless wealth asset; an asset that will have a value with the passing of time.

Remember this: Of the original issues that made up the Industrial Average, only one remains. And that stock is General Electric. And what happened to all the rest? In investing, nothing is permanent except gold. But remember, do not buy gold with the idea of making a profit. Buy gold because it is pure wealth, and may be the last man standing.

Late Notes — With gold down 3 points today, the gold mining stocks were all down. This is tax loss selling. Keep your eye on the bullion price. The Dow continues to push up as expected, although warnings are coming out of the woodwork from every direction. Money managers are afraid to leave the festivities so they will stay with the market until the bitter end.

Remember that megaphone pattern in the Dow? We’re now at the upper trendline. This could take the Dow as high as 17,000 to complete the pattern.

Between the technical position of the market and the uncertain position of the fed, we can expect erratic and hard to analyze action in the coming weeks.

At such a crucial area, I expect the market to be irregular and unstable. Also, the Dow has just closed above 16,000 and this can act like a high wire. The main trend continues higher and the melt-up that I expect still lies ahead. Speculative positions in the DIAs can be held.

………………………………….

Russell added: “The watch on watches. The ads are loaded with announcements for expensive watches. It seems that every big designer has his own brand of watch for sale. Why? The mark-up on watches is absolutely huge. They can be made in Switzerland, Japan or China.

Only two brands are worth anything — Rolex or Patek Philippe.

Do yourself a favor — send for the Stauer catalogue and look it over. I’ve bought dozens of watches (gifts) from this outfit, and they are eye-openers. They sell for around $200 and they compete with the multi-thousand dollar watches that you see advertised everywhere. A designer can order 500 watches and mark them up hugely. Then if they don’t sell, he can dump his unsold inventory and recoup his losses. Buying expensive designer watches is a sucker’s game.”

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE.

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

“In investing, what is comfortable is rarely profitable.” — Robert Arnott

Valuations still matter.

Assuming that one is investing as opposed to speculating, initial valuation (i.e. the price you pay for the investment) remains the single most important characteristic of whatever one elects to buy.

And at the risk of sounding like a broken record, “initial valuation” in the US stock market is at a level consistent with very disappointing subsequent returns, if the history of the last 130 years is any guide.

Without fail, every time the US market has traded on a cyclically-adjusted P/E (CAPE) ratio of 24 or higher over the past 130 years, it has been followed by a roughly 20 year bear market.

The evidence for the prosecution is clear, especially for the peak years 1901, 1929, 1966 and 2000. And 2013? The CAPE ratio is more than 25 today.

But there is the stock market, and then there are individual stocks. We have no interest in the former, but plenty of interest in the opportunity set of the latter.

We’re just not that interested in the US market, given general valuation concerns, and the malign role of Fed policy in distorting the prices of everything. As purists and unashamed value investors, we have plenty of other fish to fry.

Probably the biggest of those fish is that giant part of the world economy known as Asia. The chart below shows the anticipated growth in numbers of the middle class throughout the world over the next two decades.

The solid green circle is the current middle class population (or as at 2009 to be precise); the wider blue-fringed circle represents the forecast size of this population in 20 years’ time.

The OECD definition of middle class is those households with daily per capita expenditures of between $10 and $100 in purchasing power parity terms.

Note that in the US and Europe, the size of the middle class is barely expected to change over the next two decades. The stand-out area is obvious: the emerging middle class in Asia is forecast to explode, from roughly 500 million to some 3 billion people.

In equity investing, the combination of a compelling secular growth story and compellingly attractive valuations is a very rare thing, the sort of investment opportunity that one might only see once or twice in a generation, if that.

But it exists, here in Asia, today. Once again, however, we have to abandon conventional financial thinking in order to exploit it.

Asian personal consumption between 2007 and 2012 – while the West was suffering from a little localised financial crisis – grew by 5% to 10% per annum. Industries likely to benefit from sustained growth in domestic consumption include food and beverages, clothes, cars, and insurance.

But the index composition of Asian equity index benchmarks leaves much to be desired.

Of the 10 largest companies in the MSCI Asia ex-Japan index, three are low margin exporters in Korea and Taiwan, one is a low margin Chinese telecoms business, three are state-run Chinese banks, one is an inefficient Chinese oil and gas producer, and one is an expensive Chinese internet business.

That doesn’t leave much for value investors to go on.

Asian equity funds more generally, tending to be index-trackers, are heavy in Chinese stocks of indeterminate value and clunky ‘old Asia’ exporters with far too much research coverage.

Or one can ignore index composition (‘yesterday’s winners’) entirely and focus instead on ‘best in breed’ businesses throughout the region on an unconstrained basis– especially those with favorable returns on equity, strong balance sheets, and low valuations.

As Greg Fisher of Adepa Asset Management wrote, amid a world of worries, “keeping the discipline of holding lowly valued, under-owned and unleveraged companies is likely to continue to protect our capital and earn us both income and capital appreciation over the longer term.”

Or to put it more plainly, and in the words of Warren Buffett, “price is what you pay; value is what you get.”

US stocks may be expensive, but you can get better economic fundamentals and cheaper valuations selectively throughout Asia.

And as insurance against the sort of disorderly currency moves that seem to be almost inevitable courtesy of so many central banks behaving badly, we still maintain you can’t do better over the medium term than gold.

Japanese stocks fell on Tuesday, failing to hit a new high for the year, while the Australian dollar picked up after the Reserve Bank of Australia dampened speculation that it’s close to intervening in the currency markets.

After bumping up 1.6% over the previous three sessions, the dollar retreated from the recent highs against the yen USDJPY -0.11% . Having climbed as high as ¥101.92 on Monday — its highest level since May — the greenback eased to ¥101.52 after a strong run that had seen it gain for 9 of the past 12 sessions.

That weakening trend for the yen resulted in substantial gains for Japanese stocks, which also suffered a setback on Tuesday, with the Nikkei Average JP:NIK -0.67% down 0.5%. The market closed on Monday just a slither away from a new high for the year, but remains up 8.4% month-to-date. – Full Article

QUESTION: From reading your blog, my understanding of your view is that all relationships are in flux with respect to markets and market drivers, except for confidence. For example, the stock/bond relationship can change over time, so stocks do not ultimately go up or down based on what bonds do but based on where confidence stands. If that is correct, then I would submit that both stocks and bonds globally reflect a high degree of confidence in the authorities to “manage” the situation without an accident. European bond market yields reflect complete confidence in the EU and ECB. The US stock market is exactly positively correlated to the belief that the Fed has things under control (see Wednesday’s reaction). Logically, loss in that confidence would obliterate stocks. Yet you suggest we are on the verge of a massive collapse in confidence in government and its agencies and that stocks will double. How do I reconcile?

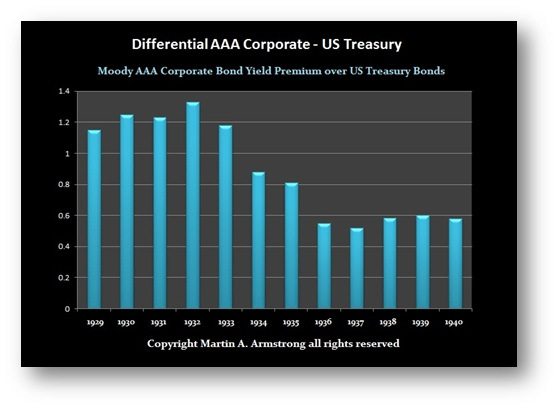

ANSWER: I am finishing up a new book on the global economy. The interpretation ofCONFIDENCE you assume is actually post Great Depression. This relationship between bonds and stock did not exist previously. Even when the Federal Reserve was formed and people argue that was a Jekyll Island Conspiracy, they too judge the past by the present. When the Fed began it had a direct tool to manage the economy. To stimulate it would buy corporate paper stepping in when banks would not lend. That made PERFECTeconomic sense. However, that was 1913. When World War I erupted and government needed to borrow, they instructed the Fed to buy their debt and not corporate. As always, they never returned the Fed to its original intent – a quasi-FDIC for banks.

The rates today no longer reflect CONFIDENCE in the state – only manipulation by the state. You will see divergences emerge between state bond rates and private. This took place even during the Great Depression. What will emerge is capital will migrate to stocks and private sector bonds at first for yield. This will cause the central banks to eventually have to buy government debt themselves (monetize) or allow rates to rise. This is what the Fed Tapering is all about. I have already reported that the Fed was going around and informing the banks to re-calibrate their models. They have been warning behind the curtain that they DO NOT SEE a flight to quality for the next decline. This is part of the negative nonsense coming from Summers.

There will be a split with this post-Great Depression thinking that government debt is best. This is the change on the horizon and the Fed even knows this. So open your mind and observe the subtle movements that are revealing the change in trend on the threshold of this chaos. Our sources are real. I do not bullshit with my “opinion” for like assholes, everyone has one. I report facts. That is what my clients expect. I am neither Republican nor Democrat. I am for practical economics.

Tax Revolts and that 309 Year Cycle – read it all HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair