Stocks & Equities

View the 145 stocks in Bill Gates portflio including latest addition and adjustments HERE

View the 145 stocks in Bill Gates portflio including latest addition and adjustments HERE

Last Update: 2013-11-14

Total Value: $19,466 Mil

Q/Q Turnover: 8%

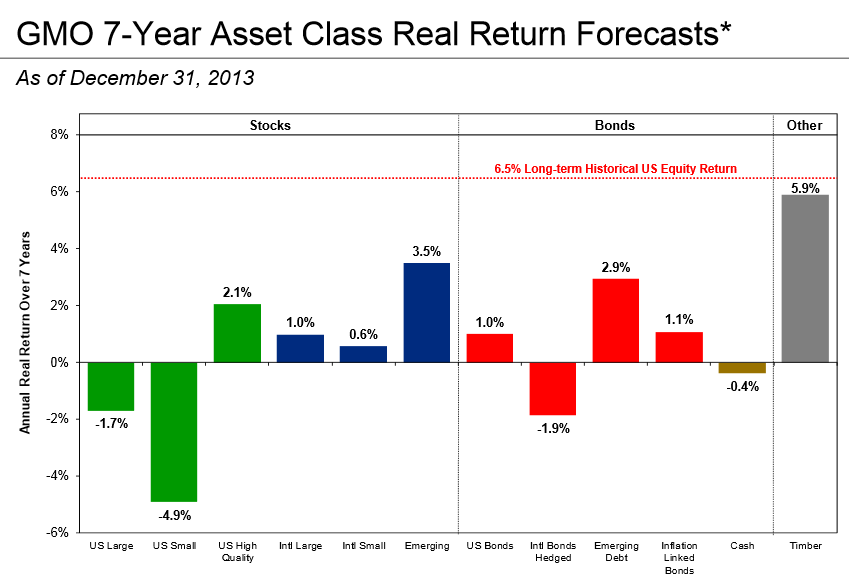

Value investor Grantham, Mayo, Van Otterloo (GMO) now estimates US stocks are poised for annualized losses for the next seven years. (click on image or HERE for larger view)

*The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements. US inflation is assumed to mean revert to long-term inflation of 2.2% over 15 year.

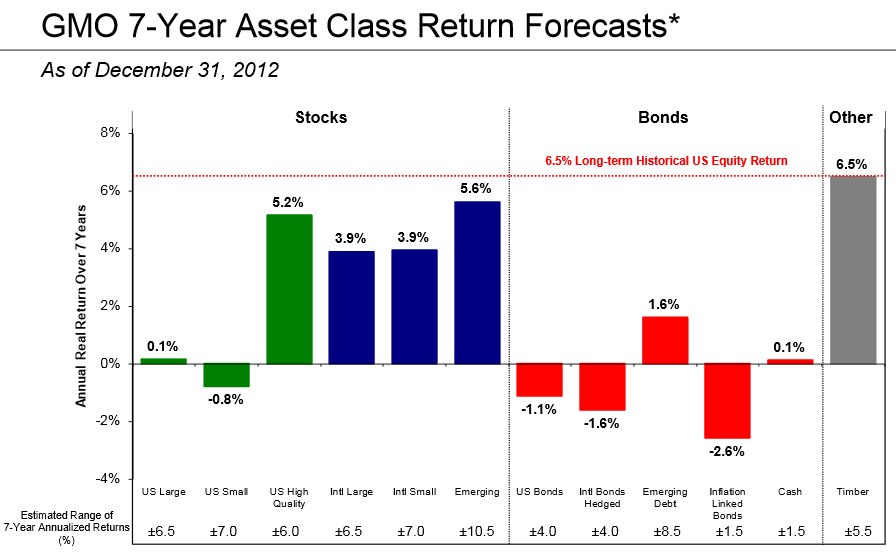

A year ago the chart looked like this. (Click HERE or on image for larger view)

Charts from GMO Asset Class Forecasts.

Reflections on Extreme Valuations

Was GMO wrong last year? Of course not. Expected returns are just that. Extreme valuations can always become even more extreme (and they did).

My Thoughts:

During periods of market excess, avoiding bubbles and instead investing in out of favor but attractive assets can be quite painful to live through in the short-term. But those who remain disciplined and on the right side of the somber judgment eventually get rewarded with significant gains amid widespread losses for those favoring that which has been working well during the period of excess.

GMO 10-Year History

Let’s step back a bit and look at GMO’s 10-Year history from 1999-2009. Please consider the chart below from What a Decade!

Highlighting in yellow is mine.

In December 1999, GMO thought the S&P 500 would deliver negative returns for a decade. In 2007 that prediction probably looked ridiculous. Yet, it happened.

When GMO predicts negative returns, it’s smart to pay attention.

Here are GMO’s “Lessons Learned in the Decade”.

Lessons Learned

- The Fed wields even more financial influence than we thought.

- Low rates have a more powerful effect on driving financial assets than on driving the economy.

- The Fed is capable of being extremely out of touch with the real world – “what housing bubble?” – plus more doctrinaire – “no, the low rates had no effect on housing” – than anyone could have imagined.

- Congress is nearly dysfunctional, primarily controlled by large corporations, and hamstrung by the supermajority now routinely required in the Senate.

- Government administrations can be incompetent for long periods.

- Poor leadership can really damage a country’s hard- won reputation in a mere 10 years.

- Obama is not a miracle worker!

- The two time-tested investment tools, value (P/E ratios and P/B ratios) and price momentum, are now much more heavily used and not so reliable as they once were, say from 1977 to 1997.

- Asset classes really are more inefficiently priced than individual stocks on average, and therefore offer greater opportunities for adding value and reducing risk.

- Developed countries, including the U.S., are past their prime compared with developing countries: it is indeed a new world order.

- Education and training are the keys to increasing wealth on a sustainable basis and the U.S. is in danger of losing its once large edge here.

- We all live on an island, which can be overexploited and turned into a barren Easter Island if we are not careful. Resources are finite and biodiversity is fragile, and both must be protected. Carbon emissions are the single greatest threat.

- Being a global policeman is expensive, and somewhere between difficult and impossible.

- The Fed learns no lessons!

Fed Uncertainty Principle Revisited

The only point I disagree with is number 12 “carbon emissions are the single greatest threat” to finite resources and biodiversity.

Arguably the most important points are 1-3 and 14 “The Fed learns no lessons“.

Readers will recognize those points as part of my Fed Uncertainty Principle, written April 3, 2008, before the big collapse.

Fed Uncertainty Principle:

The fed, by its very existence, has completely distorted the market via self reinforcing observer/participant feedback loops. Thus, it is fatally flawed logic to suggest the Fed is simply following the market, therefore the market is to blame for the Fed’s actions. There would not be a Fed in a free market, and by implication there would not be observer/participant feedback loops either.

Corollary Number One:

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

Corollary Number Two: The government/quasi-government body most responsible for creating this mess (the Fed), will attempt a big power grab, purportedly to fix whatever problems it creates. The bigger the mess it creates, the more power it will attempt to grab. Over time this leads to dangerously concentrated power into the hands of those who have already proven they do not know what they are doing.

Corollary Number Three:

Don’t expect the Fed to learn from past mistakes. Instead, expect the Fed to repeat them with bigger and bigger doses of exactly what created the initial problem.

Corollary Number Four:

The Fed simply does not care whether its actions are illegal or not. The Fed is operating under the principle that it’s easier to get forgiveness than permission. And forgiveness is just another means to the desired power grab it is seeking.

Bubble Valuation Blues

It’s not just GMO singing the bubble valuation blues. John Hussman has independently concluded the same thing.

On November 11, 2013 in Textbook Pre-Crash Bubble Hussman commented “The problem with bubbles is that they force one to decide whether to look like an idiot before the peak, or an idiot after the peak. There’s no calling the top, and most of the signals that have been most historically useful for that purpose have been blazing red since late-2011.“

Such is the nature of the game. Everyone thinks they can get out at the top. Few ever do.

Hovering With an Anvil

Please consider this snip from Hussman’s Hovering With an Anvil from January 13 (emphasis mine).

The ratio of nonfinancial equity market capitalization to GDP is about twice its pre-bubble norm, and is presently associated with an expectation of negative total returns for the S&P 500 over the coming decade. Measures based on properly normalized earnings are a little bit more favorable, with the overall outcome that we broadly expect nominal total returns for the S&P 500 of about 2.3% annually over the coming decade, with negative total returns on horizons of less than about 7 years.

Keep in mind that the 2000-2002 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to May 1996. The 2007-2009 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to June 1995. Our present expectations are rather conservative by comparison.

I side with GMO and Hussman.

Wine Country Conference II

I am pleased to again mention that John Hussman is a speaker and host of the second annual Wine Country Conference will be held May 1st & 2nd, 2014.

We have an exciting lineup of speakers for this year’s conference.

- John Hussman: Founder of Hussman Funds, Director of the John P. Hussman Foundation which is dedicated to providing life-changing assistance through medical research

- Steen Jakobsen: Chief Economist of Saxo Bank

- Stephanie Pomboy: Founder of MacroMavens macroeconomic research

- David Stockman: Ronald Reagan’s budget director, best-selling author, former Managing Director of The Blackstone Group

- Mebane Faber: Co-founder and the Chief Investment Officer of Cambria Investment Management

- Jim Bruce: Producer, Director, and Writer of Money For Nothing: Inside the Federal Reserve

- Chris Martenson: Reknown speaker and founder of Peak Prosperity

- Mike “Mish” Shedlock: Investment advisor for Sitka Pacific and Founder of Mish’s Global Economic Trend Analysis

In addition, we expect confirmation from a number of other highly respected fund managers and speakers. This year’s event is two days and will include additional “break-out” groups.

For speaker bios, please check out Wine Country Conference Speakers.

This Year’s Cause: Autism

$100,000 of the money raised last year came from a generous matching grant from the John P. Hussman Foundation.

Some of us in the industry who have done well are making an effort to give something back. John Hussman is at the very top of that list.

One of John’s kids has severe autism. This year, all net proceeds will go to support autism programs.

Conference Details

For further details about the 2014 conference, please see Wine Country Conference May 1st & 2nd, 2014

Nothing Like It!

This event is not just another “come and hear someone talk” kind of thing. Attendees and their significant others can expect an educational, fun, and relaxed time.

Last conference, we arranged wine tours. They were a big hit. We will do so again. One of the wine estates we visited had a Bocce Ball court. On a couple of miracle shots, I won both games I played.

Stay an extra day and golf or travel. I did. The conference hotel is a fun place in and of itself.

Unlike many other conferences, you will have easy access to speakers.

Want to chat with me, Steen, John, or anyone else at the conference? You will have an easy chance.

Not only do we have an excellent lineup of speakers, you will have an opportunity to meet with them, have intimate discussions on important investment topics, with a lot of fun on the side, including wine tours and great wine.

There’s nothing like it in the investment business. And your money goes to a great cause! What can be better?

Quantitative Easing has helped to expand global stock market capitalization by a staggering $36 trillion over the last five years. As the accompanying chart indicates, the only intermissions were after each dose of Quantitative Easing (QE1 & QE2).

What is truly astounding is the minimal impact all of this has made with respect to economic growth and employment (some argue that the global economy would have collapsed without QE – but that argument only resonates with the first emergency dose in 2008-2009 – the following applications were more about engineering a recovery in the job market).

All this highlights the risk presented by a full “Tapering” of QE3. There may be some central bank optimism that the recent increase in economic growth might be enough to weather the headwind that a Taper will create. However, history shows us that things almost immediately slowdown after the foot is taken off the QE gas pedal. With this in mind, it may be just too difficult for the current dovish regime of central bankers to maintain their pledge of ending QE3 by the end of this year. Who knows, come 2015 we might be at new records for global stock market capitalization … if things really get bad, that is.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

The S&P 500 futures have rallied back 29 points from the big sell off on Friday to be green on the year at 1838.25. The next target will be the All Time High made at the end of last year at 1846.50.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

In the low-interest-rate environment of recent years, investors have had to exercise patience when waiting for attractive fixed-income opportunities to arise. I often write about specific opportunities worth exploring and attempt to provide a variety of fixed-income ideas so that all the various types of income-focused investors have some food for thought.

Last month, I was interviewed for Seeking Alpha’s “Positioning for 2014” Series. The focus of the interview was fixed income, with an emphasis on bonds. One of the many questions I was asked had to do with broadly identifying where in the world of fixed income investors could find the best yields relative to the risk of acquiring those securities. Part of my response included the following:

So many preferred stocks and exchange-traded debt are currently trading at moderate-to-large discounts to their liquidation preference/call price/maturity price with yields in the 6% to 8% range. I think it is time to begin building an allocation to those securities.

Toward the end of last year, I was of the opinion that a significant amount of window dressing and tax-loss selling was negatively affecting the price of various fixed-income securities, with preferred stocks in particular being pressured. Given my outlook for at best moderate GDP growth and inflation that is nothing to worry about over the coming years (health care being the one exception), 6% to 8% yields from preferred stocks and exchange-traded debt make a lot of sense for an income-focused investor. I don’t think investors should load up a portfolio with those securities. But a modest allocation is worth considering.

As I mentioned in the opening paragraph, exercising patience is a must when searching for attractive income opportunities in today’s generally low-interest-rate environment. On the other hand, when those opportunities arise, investors should act quickly. As 2014 has already taught preferred stock investors, if you don’t act quickly, the best opportunities can disappear.

Since bottoming on December 30, the iShares U.S. Preferred Stock ETF (PFF) is up 3.22%. That’s a nice gain for just two weeks of trading but certainly nothing to write home about. When looking at my favorite preferreds, equity-REIT preferreds, the returns are much more striking. Below is a table outlining the performance since their lows on either December 30 or December 31 of the seven equity REITs with risk-reward profiles I found compelling enough to buy in 2013.

To illustrate, in yield terms, just how large the moves have been in the aforementioned REIT preferreds, let me start with Vornado Realty Trust, a REIT with a portfolio of over 100 million square feet of commercial real estate. The move from $18.63 to $20.29 was the equivalent of a drop of 59.2 basis points in yield, from 7.246% to 6.654%. In comparison, the 30-year Treasury bond (TLT) is trading roughly 17 basis points lower than its high on December 31. Even the two worst performers of the group, Digital Realty’s Series G preferred and Realty Income’s Class F preferred have fallen 29.4 and 29.7 basis points respectively in just over two weeks.

Despite the recent steep drop in yields, the lowest yielder of the bunch still offers a respectable 6.529% (Public Storage – Series W preferred). If you find the credit risk appropriate, the preferreds mentioned above still provide real yields that many investors will find attractive. This is especially true for those who see, at worst, only moderate upside in benchmark yields over the coming years.

Investors wishing to conduct research on the companies mentioned in this article may be interested in the following two sources: (1) Some of the commentaries I have written on these companies can be found here, and (2) Brad Thomas, a Seeking Alpha contributor who regularly writes about REITs, may have detailed articles regarding the seven aforementioned companies. His articles can be found here.

Other articles via The Financial Lexicon:

- 3 Things Every Stock Market Investor Should Consider

- The Financial Lexicon Positions For 2014: Individual Bonds Are The Way To Go

- Toll Brothers Bonds: Is 5.51% An Attractive Yield?

- The Case For A 0% Bond Allocation Is Weak

I am an investor/trader with more than a decade of experience in the financial world. I have experience investing in and trading equities, options, and a variety of fixed income and alternative investment products.

I also write for LearnBonds.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair