Real Estate

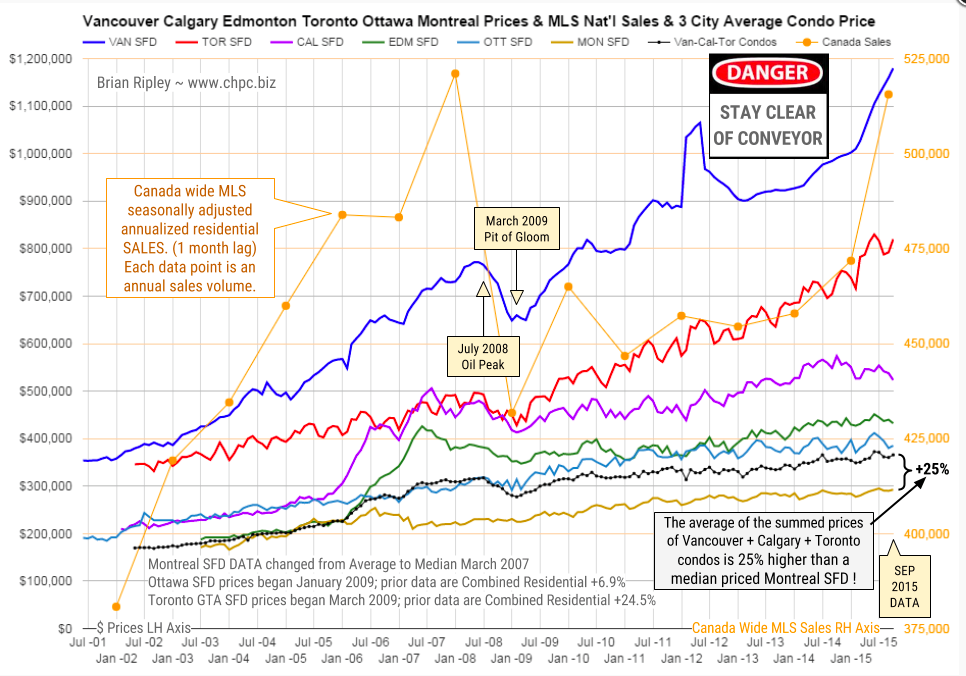

The indomitable Vancouver and Toronto markets continue to drive housing price gains, evidence of inventory challenges that continue to plague key markets.

The indomitable Vancouver and Toronto markets continue to drive housing price gains, evidence of inventory challenges that continue to plague key markets.

The chart above shows the average detached housing prices for Vancouver, Calgary, Edmonton, Toronto*, Ottawa* and Montréal* (the six Canadian cities with over a million people) as well as the average of the sum of Vancouver, Calgary and Toronto condo (apartment) prices on the left axis. On the right axis is the seasonally adjusted annualized rate (SAAR) of MLS® Residential Sales across Canada (one month lag).

Go HERE for analysis and a larger chart

Go HERE for the the PLUNGE-O-METER, which tracks the dollar and percentage losses from the peak and projects when prices might find support.

The Chinese rush to buy U.S. Real Estate is probably a sign of a top in that market.

The Chinese rush to buy U.S. Real Estate is probably a sign of a top in that market.

…..listen to Jim’s podcast HERE

also from Rogers:

China Will Not Save Us Like They Did In 2008-09

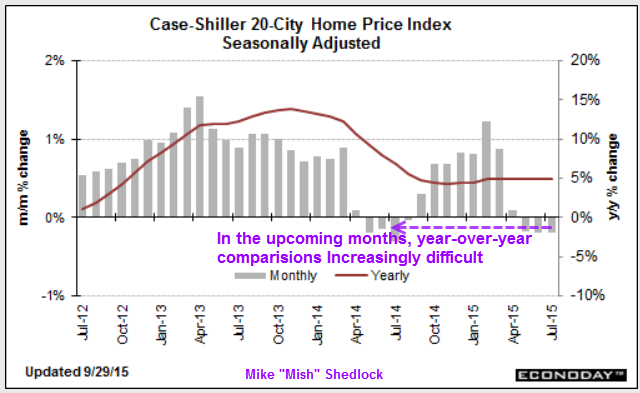

For the third month in a row, the Case-Shiller 20-city seasonally adjusted home price index declined. Last month was revised lower. Economists were surprised.

The Bloomberg Econoday Consensus was for a month-over-month rise of 0.1%, instead prices declined by -0.2%.

Case-Shiller is reporting what is becoming striking weakness in home prices, at -0.2 percent in July for the adjusted 20-city index which, after a downward revision to June, is the third straight 2 tenths decline. Twelve of 20 cities show contraction in the month with the deepest for a third straight month in a row coming from Chicago at minus 1.2 percent. Year-on-year readings are all still positive led by San Francisco at plus 10.4 percent with Washington DC at the bottom at 1.7 percent.

Year-on-year, the 20-city index, whether adjusted or unadjusted, is at plus 5.0 percent vs 4.9 percent in July. The unadjusted month-to-month index, reflecting summer strength in home sales, was up 0.6 percent in August for however the weakest reading since the winter weather of February.

This report is very closely watched and offsets last week’s gain for FHFA prices which are trending slightly higher than Case-Shiller. Home sales have been mixed this year with existing homes showing strength through most of the year but weakness in the latest report and vice versa for new homes which had been weak but have since popped higher. Lack of home-price appreciation is a negative for household wealth and spending and may be another symptom of general price weakness.

Case Shiller 20-City Index

Year-over-year comparisons have held stable at 5% in spite of month-over-month declining prices because of easy comparisons. Year-over-year comparisons will be increasingly difficult in the upcoming months.

Mike “Mish” Shedlock

With thin margins in the mortgage business, lenders are always looking for ways to offer lower mortgage rates but still maintain profitability. The latest of these low-rate mortgage trends has been deeply discounted rates but with limited pre-payment privileges. One of these products may offer rates as low as 1.95% for a 5 year variable or 5 year fixed of 2.39%, but with a 2.75% administration penalty if you break the mortgage early.

With thin margins in the mortgage business, lenders are always looking for ways to offer lower mortgage rates but still maintain profitability. The latest of these low-rate mortgage trends has been deeply discounted rates but with limited pre-payment privileges. One of these products may offer rates as low as 1.95% for a 5 year variable or 5 year fixed of 2.39%, but with a 2.75% administration penalty if you break the mortgage early.

On a $300,000 mortgage, a typical variable rate penalty would be about $1,600 (penalty for a variable rate mortgage is 3 months interest). If you ever had to break up your mortgage for any reason and you chose the lower rate option, your penalty could be around $8,250. The savings over the 5 year period would only be about $3,000 so that’s a big price tag to pay for lack of pre-payment privileges, lack of lock-in privileges, etc.

Many of these low rate products are with “non-bank” lenders, not major banks. In most cases, major banks’ products are usually fairly standard, and they don’t usually offer a normal full service product alongside a no frills product, with the exception of BMO. Only mortgage brokers have access to these non-bank lenders who have these no frill, low rate products, so if you think you are in the market for a product like this and are ok with some of the downsides, make sure to talk to your broker to learn more about the product.

Here is a list of important items you should ask about your broker or bank when negotiating your next mortgage:

- How much can I prepay per year with no penalty? (Standard is 15% – 20%)

- When can I make these payments? (most allow anytime during the year but some require only one payment annually on the anniversary date)

- How much can I increase my payments per year? (Standard is 10% – 100%)

- What is the penalty to break my mortgage? (most are 3 month penalty, with fixed terms having a potential Interest Rate Differential Penalty)

- How is my IRD penalty calculated? (Major banks have a really nasty calculation for their penalties that could cost you 2.5 times more than a “non-bank” lender)

- Under what circumstances can I refinance? (many of the low rate offers restrict this option)

- Can I lock into a fixed rate at any time? (some low rate mortgages don’t allow lock-ins)

- Am I guaranteed your best rate when I lock in? (most major banks don’t offer a guarantee)

- Are there any other bells and whistles that I get with this product?

Getting the best mortgage isn’t always about rate – it’s about value and about choosing the right term. A good broker will ask what your goals and intentions are to ensure your mortgage is properly set up for your short term goals but also for your long term goals.

Kyle Green

Mortgage Alliance Meridian Mortgage Services Inc. – www.GreenMortgageTeam.ca

Office: 778-373-5441

#2000 – 1066 W Hastings, Vancouver, BC V6E 3X2

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair