Real Estate

Sales of homes across Canada rallied by 2.2 per cent month-over-month in December after November transactions suffered some weakness in the wake of stricter mortgage rules, according to a new report from the Canadian Real Estate Association.

Sales of homes across Canada rallied by 2.2 per cent month-over-month in December after November transactions suffered some weakness in the wake of stricter mortgage rules, according to a new report from the Canadian Real Estate Association.

Home prices also went up by 3.5 per cent year-over-year in the same month, up to $470,661.

…related from Ozzie Jurock:

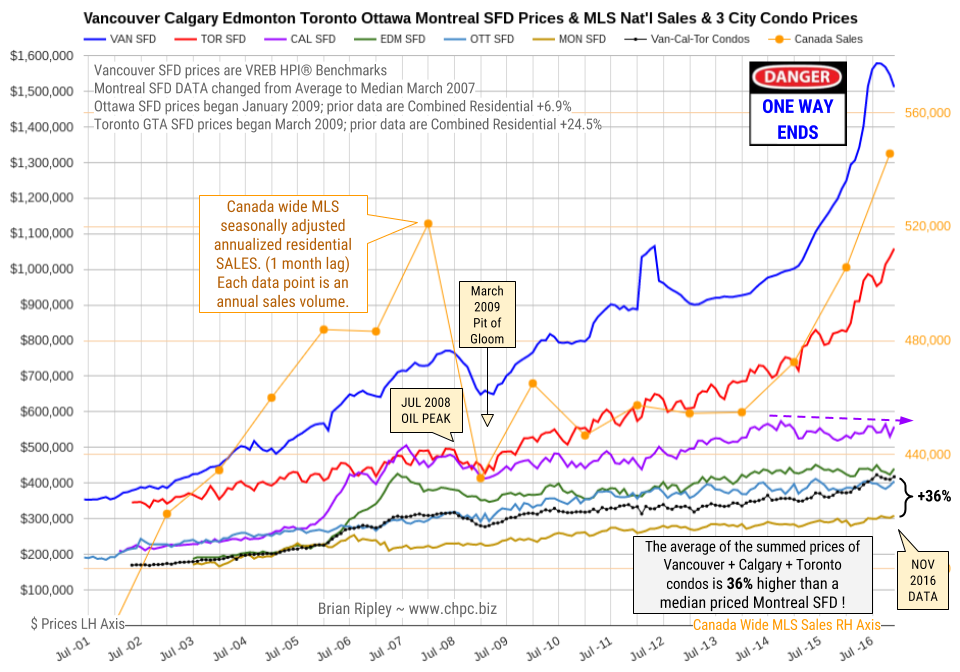

The chart above shows the average detached housing prices for Vancouver*, Calgary, Edmonton, Toronto*, Ottawa* and Montréal* (the six Canadian cities with over a million people each) as well as the average of the sum of Vancouver, Calgary and Toronto condo (apartment) prices on the left axis. On the right axis is the seasonally adjusted annualized rate (SAAR) of MLS® Residential Sales across Canada (one month lag).

….for larger chart and analysis go HERE

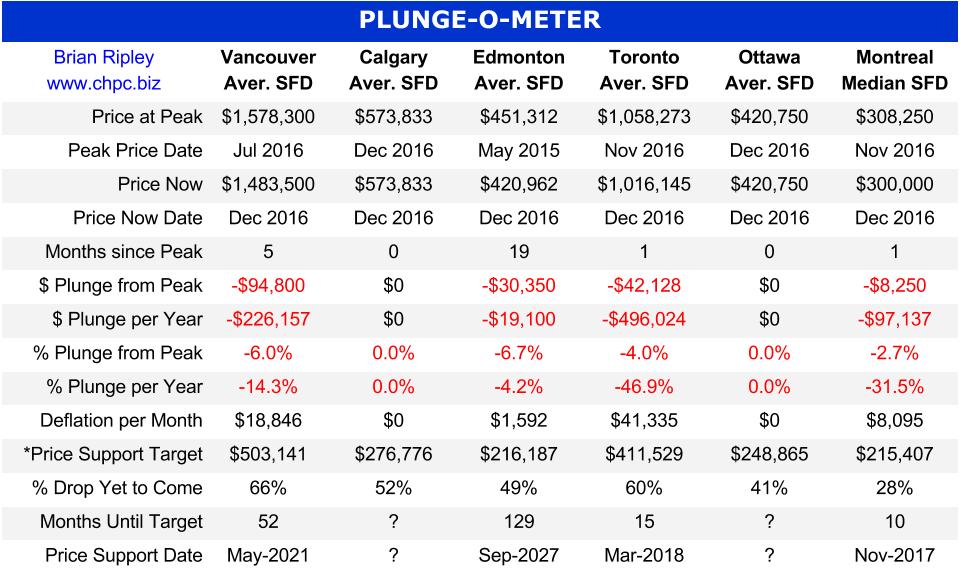

The Canadian Real Estate PLUNGE-O-METER

The Plunge-O-Meter tracks the dollar and percentage losses from the peak and projects when prices might find support. On the price chart in the spring of 2005 there was a 4-6 month plateau period while buyers and sellers twitched like a herd. When the credit spreads narrowed and the yield curve began its journey towards inversion, the commodity stampede began.

*The Price Support target represents prices at March 2005; the start of a 40 month period of ardent speculation in all commodities; then a full blown crash into the pit of gloom (March 2009); and then another 39 month rocket ship to the moon but then the crowd suddenly thinned out in April 2012. The revival of spirits erupted in 2013 as global money went short cash and long real estate on an inflation bet. Now we have a major sense of doubt about value in Vancouver and Toronto as sales and prices chill out as we move into 1Q 2017.

…for CDN Housing Priced in US Dollar go HERE

Ozzie Jurock first covers the 2016 year end real estate numbers, the big story being Toronto up powerfully. Victoria, Vancouver and other cities in BC have seen sharp decreases in single family homes, though increases in condo sales.

….related: Surprising New Forecast For Mortgages

Downsized condominium units are becoming increasingly popular option among Canada’s young buyers—an unavoidable development in a fiscal climate characterized by static income growth and ever-rising costs.

Downsized condominium units are becoming increasingly popular option among Canada’s young buyers—an unavoidable development in a fiscal climate characterized by static income growth and ever-rising costs.

….related:

CANADA’s 6 BIGGEST METROS Vancouver, Calgary, Edmonton, Toronto, Ottawa and Montréal Single Family Detached Housing as well as the National MLS Residential Annualized Sales and the Average Price of Vancouver, Calgary and Toronto Condos. Rental Offerings via Craigslist, Kijiji, and Airbnb Chart…..BELOW

…also: Affordability or Bust

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair