Personal Finance

INSTITUTIONAL ADVISORS

THURSDAY, MARCH 21, 2013

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The following is part of Pivotal Events that was published for our subscribers March 14, 2013.

Signs Of The Times

“I view the balance of risk as still calling for a highly accommodative monetary policy to support a stronger recovery.”

“I view the balance of risk as still calling for a highly accommodative monetary policy to support a stronger recovery.”

– Janet Yellen, the Fed’s # 2 official, Bloomberg, March 4

She added that there was no “persuasive evidence” of financial instability. Clearly, Yellen is reading too many internal reports and has never spent any time as a margin clerk.

However, on the same day, March 4th, Bloomberg reported:

“Former Fed chairman, Paul Volker, said U.S. central bank officials may find it difficult to rein in their historical stimulus at the appropriate time– ‘because there is a lot of liquor out there’.”

“Disposable income, or the money left over after taxes, plunged 4 percent, the biggest plunge since monthly records began in 1959.”

– Bloomberg, March 1

“The riskiest U.S. companies are tapping institutional investors at the fastest pace ever.”

– Bloomberg, March 1

“U.K. Manufacturing unexpectedly shrank in February as new orders plunged.”

– Bloomberg, March 1

“German factory orders unexpectedly fell in January as the sovereign debt crisis curbed demand in the euro area.”

– Bloomberg, March 7

Unexpected plunges in economic numbers provide an interesting contrast against reckless behaviour by investors and central bankers.

“Private equity firms have lost no time taking advantage of record low yields in global leveraged loan markets. And like a school of piranhas sensing blood, they have thrown themselves into the fray with gusto. The frenzy of activity comes as institutional investors…demand assets that carry a higher yield.”

– Financial Times, March 7

“Collateralized loan obligations paying the lowest rates in five years are being snapped up by investors, providing fuel that’s contributing to the biggest surge in corporate buy outs since before the financial crisis.”

– Bloomberg, March 8

Stock Markets

High sentiment and momentum readings clocked in January were followed by five weeks of consolidation. This month’s rise includes 10 consecutive trading days up for the Dow, including today. It’s a sign of enthusiasm.

Weekly RSI momentum is up to 74, which seems to be a spike. This compares to the 73 reached a couple of times with the “rounding” top of 2007. Higher readings of 76 and 78 were only accomplished on the power rallies out of the 2002 and 2009 crashes.

The sharp plunge in U.S. disposable income could be mainly due to radical policies. But “unexpected” bad numbers in England and Europe are telling a sad story that not much of their “stimulus” is going into GDP, which Janet Yellen may be focusing on. Perhaps Volker has a broader perspective on financial conditions.

While the incoming tide of “liquor” seems not to be lifting the GDP and employment boats in the harbor, it has been lifting financial instruments.

This shows up in the Broker-Dealer Index (XBD), which soared to a Daily RSI of 85 through most of the first two weeks in February. The Weekly got to 73. Both momentums reached the highest in years. And the latest rally has made it to 110 on the index, which is a big test of the 110 reached in February. Momentum then was at 65, now it’s at 73, which suggests the test will fail.

Of interest, is that in 2007 and in 2011, Broker-Dealers led the high in the S&P.

Another topping indicator is the Percent Bulls on the NYSE Composite and it is showing negative divergence.

There are now more indicators registering conditions for a reversal than in late January. We would continue to sell the rallies.

Currencies

The US dollar continues to rise against the euro, C$, yen and sterling. The DX did trade at the 82 level, but for only two days. Then, yesterday’s action accomplished an Outside Reversal, to the Upside that took it up to 83.

As noted a few weeks ago, the Daily RSI became overbought at the first of the month. As mentioned last week, the Weekly RSI is a neutral momentum, which suggested, eventually, the rise had further to go.

Obviously, the 84 level reached in last summer’s concerns about Euro debt default represents considerable resistance. In looking at the chart back to 1980 there has been a tendency to respect resistance levels. Other support levels, such as at 71.33 in 2008 (just before the stock market began its crash) and the big test at 72.70 in 2011.

Before that the big high with the Telecom Crash was at 121 in 2001-2002.

On the near-term, the dollar’s advance could pause. Rising above 84 would indicate that the karma of the marketplace is beginning to overwhelm the dogma of policymakers.

The Canadian dollar suffered its sharpest sell-off since commodities tanked in 2011. But, on this move the CRB only declined a little. The weekly RSI is down to a level that could limit the decline.

Commodities

Copper declined to 3.47 which is the support level. At 30, the Daily RSI was also at “support”. Often copper can rally into March, but the spring “seasonal” could be deferred to next month.

Much the same holds for the base metals index (GYX). A rebound seems possible. However, real copper prices have been unusually high and have yet to correct.

A recent Bloomberg report about the governing classes in egalitarian China is fascinating:

“Ninety members of the National People’s Congress are on the list of China’s 1,000 richest people.”

Beyond China’s industrial demand for copper, there has been China’s investment demand for copper. This reminds of 1996 when “Mr. Copper” in Japan had run up a huge position beyond economic demand. Herbert Black, a wealthy metals trader in Montreal, was instrumental in bringing the scam down. It cost Sumitomo $2.6 billion.

Much has been written about the uniqueness of the great change in China: The turn to industrialization, accompanied by migration from rural to cities.

Much the same happened in North America during the last half of the 1800s. Economist W.W. Rostow determined that in the late 1840s the US had 5 percent of global industrial production. By the 1880s this had increased to an impressive 29 percent. A long economic expansion segued into an era of inflation in tangible and financial assets. This ended in 1873 as a classic bubble climaxed. That marked the beginning of a Great Depression that ended in 1895. The “unique” transformation of the US economy and massive migrations from rural to urban life had little influence on that great and global contraction.

China’s “uniqueness” is in the market, but its unusual position in base metals has yet to be resolved. Mining and smelting stocks were outstanding performers into the 1873 mania. The index reached over 500 and slumped to around 20 before the depression was over.

This time around, base metal miners (SPTMN) soared from 105 in 2002 to 958 in 2007. After plunging to 177 in 2008, the index “flew” to 1600 in 1Q2011, when our Momentum Peak Forecaster kicked in. The next key low was at 781 last summer. The high in January was 1050 and last week’s low of 875 took out the November low of 895.

The present rebound could gain a little more over the next few weeks. To be wary, taking out the 781 low of last summer would be very negative to the sector. And that means the global economy!

There has been little change in agricultural prices over the past week.

Crude oil sold off to 89.33 with an RSI at 30 a couple weeks ago. The rebound has made it to 92.50. There is resistance at the 94 level.

Credit Markets

Government compulsion to buy bonds of doubtful returns continues, accompanied by complacency on the buy and hold side. All participants have a “tiger by the tail” and dare not let go. For fear of being mauled.

This has been the case with every inflation, and all have been deliberate and not accidental. But due to exhaustion, all have ended. Recently the street is again in the mode that “printing” over the past few years will suddenly erupt in a massive surge in the CPI. On March 7th a letter-writer headlined:

“Are You Prepared For Hyperinflation?”

Our point has been is that the “inflation” has been in financial assets – particularly in lower-grade bonds. And without speculator’s compulsion to get leveraged the Fed’s portion of credit creation would not happen.

Actually, inflation in financial assets has been “on” since inflation in consumer prices blew out in 1980.

More recently, Our February 14th edition reviewed the sequence of speculative highs set in different classes of bonds.

The first was in long-treasuries reaching 153 with last summer’s European crisis. Then Munis accomplished the big surge with the MUB reaching 113.5 at the end of November. The initial plunge was to 108.43 in mid-December and the rebound made it to 112.15 in January. The price traded down and up to the key high at 111.86 at the first of the month. The drop to 109.67 is significant. Taking out the 109 level would be concerning.

The next support level is at 104. Another crisis would take it down to 90.

Emerging Market Bonds (EMB) became the next favourite on the run to 122.46 at the first of the year. Today’s trade is at the 118 support level. Taking it out seems inevitable. The next level is at 105 and in the last crisis the market cleared at 60.

With some zest, Junk (JNK) is testing the momentum high set at 141. Taking out 40 turns the action down. In which case the next level is 36. In the crash it plunged to 18.

We look at this as a sequence of speculative surges and Junk is the last horse to run and it is getting tired.

On the bigger picture, our Gold/Commodities Index turned up in May 2007 a few weeks before all credit markets turned down. To the worst financial calamity since the 1930s.

It could take a few weeks to confirm the uptrend and that could be the “Death Cross” for orthodox investments in stocks, junk bonds and commodities. Not to overlook subscriptions in “hyper-inflation” letters.

Link to the March 15, 2013 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2013/03/dream-team-ii/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

He earned $12.6 billion in today’s dollars in the 1929 Crash.

The stock market has certainly produced its share of heroes and villains over the years. And while villains have been many, the heroes have been few.

The stock market has certainly produced its share of heroes and villains over the years. And while villains have been many, the heroes have been few.

One of the good guys (for me, at least) has always been Jesse L. Livermore. He’s considered by many of today’s top Wall Street traders to be the greatest trader who ever lived.

Leaving home at age 14 with no more than five bucks in his pocket, Livermore went on to earn millions on Wall Street back in the days when they still literally read the tape.

Long or short, it didn’t matter to Jesse.

Instead, he was happy to take whatever the markets gave him because he knew what every good trader knows: Markets never go straight up or straight down.

In one of Livermore’s more famous moves, he made a massive fortune betting against the markets in 1929, earning $100 million in short-selling profits during the crash. In today’s dollars, that would be a cool $12.6 billion.

That’s part of the reason why an earlier biography of his life, entitled Reminiscences of a Stock Operator, has been a must-read for experienced traders and beginners alike.

A gambler and speculator to the core, his insights into human nature and the markets have been widely quoted ever since.

Here are just a few of his market beating lessons:

On the school of hard knocks:

The game taught me the game. And it didn’t spare me rod while teaching. It took me five years to learn to play the game intelligently enough to make big money when I was right.

On losing trades:

Losing money is the least of my troubles. A loss never troubles me after I take it. I forget it overnight. But being wrong – not taking the loss – that is what does the damage to the pocket book and to the soul.

On trading the trends:

Disregarding the big swing and trying to jump in and out was fatal to me. Nobody can catch all the fluctuations. In a bull market the game is to buy and hold until you believe the bull market is near its end.

….read the other 6 market lessons HERE

You’d think that with all this practice, politicians would know how to handle a banking crisis by now. Most especially in the Eurozone.

But no. Five years since Bear Stearns hit the skids (the anniversary was Monday) the Cypriot mess is such a mess that people elsewhere feel the urge to say that “it couldn’t happen here.”

Portugal’s finance minister said it Tuesday afternoon. Italy’s La Stampanewspaper said it Tuesday morning. Yet a raid on banking deposits already happened in Italy, a mere 21 years ago with a 0.6% hit across all bank accounts. Italy applied a hit of 4% or so in 1920 as well, back when the Czech government, Austria, Germany and Hungary all tried the same move too. Norway made a grab for savers’ cash in 1936. Brazil and Argentina used the gambit — raiding savers’ accounts for emergency cash — a little over a decade ago.

Still, it could never happen, right?

Protect the small savers” — barring the more recent examples above, that has been the mantra of policy wonks and politicians dealing with bank failures since the Great Depression 80 years ago.

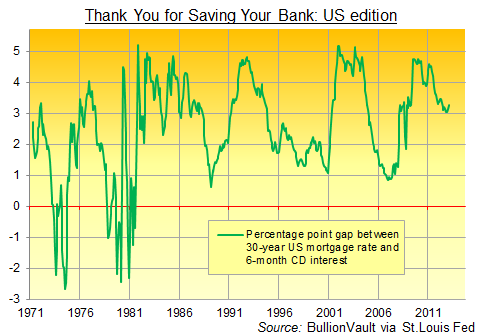

Customers of Bear Stearns barely noticed the change, for instance, when it collapsed into the warm, taxpayer-funded embrace of JPMorgan for just $2 per share on March 18, 2008. Because amongst major-currency nations, the preferred route to whacking the little guy — and getting him to pay for the banks’ excesses — has been via interest rates, as our chart above shows.

Get borrowers to pay way more than depositors earn, and post the difference straight to your bottom line. Throw in negative real rates on bank savings and government bonds — courtesy of central banks squishing rates below the pace of inflation — and the same scam can help entire economies chip away at the real value of their public debt, too.

But this rule — the rule of hiding the theft from savers — finally broke Saturday morning. To get a bail-out from the rest of Europe, the government of Eurozone-member Cyprus agreed to a 9.9% levy on anyone with €100,000 in a Cypriot bank. Most amazing, small savers are no longer sacred. They would be hit for 6.75% on deposits below €100,000.

The FT called this a stupid idea whose time has come. Paul Krugman writing in the NY Times said “It’s as if the Europeans are holding up a neon sign, written in Greek and Italian, saying ‘Time to stage a run on your banks!‘” The U.K. government, ever eager to pretend that we Brits are immune to bank-account losses, is shipping out €1 million in cash to help pay our armed forces stationed there, and it has also promised U.K. tax-payers will make good any loss the troops might suffer on their Cypriot deposits in just the way that we all shared the £100m cost of making U.K. users of high-yielding Icelandic banks whole in 2008.

Heaven forbid anyone should say that such high-paying bank accounts should have been warning enough. Like Felix Salmon says, a promise is a promise, and Cypriot savers had bank-account insurance up to €100,000. It’s just not fair!

A few other talking-heads meantime guess — as we do — that the initial “levy” was a dummy, intended to make the real savings tax look much less drastic. But lots of people also note that Russian mafia money, a huge part of Cypriot banking, will see its 9.9% levy as just a cost of doing business. The island’s reputation as a money-laundering center will be intact, at the cost of hurting the little guy.

Cyprus accounts for just 0.5% of the 17-nation Eurozone economy. The proposed levy will raise perhaps €5.8 billion, just $7.5bn. Yet the Eurogroup’s action has already seen stock markets sink, along with the euro. The gold price in euros jumped 2.3% at the start of Asian trade Monday morning, and has since jumped again as the chaos in Cyprus’s rescue gets worse.

Now, this is very much a crisis in motion. The Cypriot finance minister, for example, may or may not have resigned Tuesday whilst visiting Moscow to discuss Russian aid and bank savings. And as we say, odds are that the levy on small savers will yet be cut, altering the terms to make whatever deposit-grab is left more acceptable. But either way, the big lie behind the financial crisis so far — that bank savings are safe — has blown up again.

Putting cash on deposit makes you a creditor. And in financial crises, the creditor always pays in the end, whether through inflation, default or a “levy.” Yes, you are supposed to be safe from immediate loss, thanks to the charade of deposit insurance. But the cost of getting off price risk is credit risk lying unseen and unstated until the day that it matters.

Holding a little physical property, in contrast, exposes you to price movements. But it gets a chunk of your savings away from the myth of bank-account security. Hence the jump already this week in gold.

Even without that price move, gold still makes sense as a physical escape from all-too transient banking. Of which in Nicosia and all points west there remains way too much. The Cypriot solution is at least one way of shrinking the finance sector overnight.

About the Author

Adrian Ash runs the research desk at BullionVault. Formerly head of editorial at Fleet Street Publications – London’s top publisher of financial advice for private investors – he was City correspondent for The Daily Reckoning from 2003 to 2008, and is now a regular contributor to a number of investment websites.

It’s easy enough to focus on the smoldering ashes of the politically and economically insane move in Cyprus by the heavy-handed bureaucrats in Brussels and Germany.

It’s easy enough to focus on the smoldering ashes of the politically and economically insane move in Cyprus by the heavy-handed bureaucrats in Brussels and Germany.

Instead, I suggest we focus on the bright side, and there is plenty to be found.

- The nannycrats have been permanently exposed as liars

- Trust is gone

- Everyone can now clearly see that deposit guarantees were a lie

- Realization has set in that in spite of nannycrat denial, this will happen again

- The move in Cyprus will strengthen the Five Star Movement in Italy

- The move in Cyprus will embolden the separatists in Spain

- The move in Cyprus will strengthen UKIP in Great Britain

- The move in Cyprus is even likely to strengthen Alternative für Deutschland (AfD)

- Eurobonds and joint budgets are exposed as dead

- In Germany, Merkel is likely to have won a Pyrrhic victory (if indeed she won anything at all)

- Sensible people now realize all this talk of European solidarity is a gigantic lie

- Even ardent supporters of the eurozone are now starting to question its existence

That is one heck of a lot of good things for the bargain basement price of a mere €5.8 billion.

If Europe could not come together to scrape up a mere €5.8 billion to rescue tiny Cyprus, what exactly can they come up with? The answer of course is nothing.

Philosophically speaking, Northern and Southern Europe could not possibly be wider apart.

No Union, Only Dreams

There is no union, only foolish dreams of one. There is no solidarity, only talk.

Yet the talk has changed. I was wondering exactly what it would take to light a fire in Telegraphcolumnist Ambrose-Evans Pritchard and we now have the answer.

Pritchard says Daylight robbery in Cyprus will come to haunt EMU. But so have two-dozen others. What struck me was these paragraphs.

They [EU creditor States] have demonstrated that the rhetoric of EMU solidarity is just hot air, that they will not force their own taxpayers to share a single cent of clean-up costs for the great joint venture of monetary union.

The sooner this is made clear, the better. The sooner they take the proper course of withdrawing from EMU and organise the break-up the euro in the least disruptive way, the sooner Europe can recover.

America and China must crush Germany into submission

Please compare the above paragraphs with an article Pritchard wrote on November 9, 2011: America and China must crush Germany into submission

As we watch Italy’s 10-year bond yields near 7.5pc and threaten to detonate the explosive charge on €1.9 trillion of debt, it is time for the world to reimpose order.

Yes, this means mobilizing the full-firepower of the ECB – with a pledge to change EU Treaty law and the bank’s mandate – and perhaps some form of quantum leap towards a fiscal and debt union.

The EU Project has become both dangerous and insane.

Two days later, on November 11, 2011, I wrote a rebuttal: We Must Crush Ambrose Evans-Pritchard, Nouriel Roubini, Martin Wolf, the Army of Krugmanites into Submission; Reflections on “Dangerous and Insane”

Reflections on “Dangerous and Insane”

- What’s dangerous and insane is economists like Prichard demanding treaties be tossed to the wind to test poorly thought out economic ideas.

- What’s dangerous and insane is economic theory that says printing presses are the answer. It has never worked in history and will not work now.

- What’s dangerous and insane is more leverage. Didn’t Lehman and LTCM prove that? How many more times do we have to prove that before it sinks in?

- What’s dangerous and insane is the idea is that central banks can impose their will on the world.

- What’s dangerous and insane is doing the same damn thing over and over and over again hoping for a different result

- What’s dangerous and insane is the moral hazard policy of time-and-time-again forcing the 99% to bail out the 1%.

The world will not end if banks fail. Forcing the 1% (banks and bank bondholders) to take a hit will not cause the world to end either, nor will it cause lending to cease.

In my rebuttal, I also wrote “Widespread debt restructuring and partial break-up of the eurozone is where we are headed, and the debate ought to be how to do that correctly instead of how to achieve the impossible.”

As you can see, Pritchard finally has it correct. Given that he was one of the original eurosceptics, I knew he would eventually come around.

It’s one thing for eurosceptics to finally get back on the right track, but it’s another thing indeed for dyed in the wool euro supporters to begin questioning the euro itself.

Wolfgang Münchau, founder of Eurointelligence and columnist on the Financial Times is one such euro supporter.

The Failure of the Euro-Politicians

Please consider Münchau’s recent column on Der Spiegel Expropriation in Cyprus: The Failure of the Euro-politicians.

The euro finance ministers will partially expropriate bank customers in Cyprus. This decision is the worst accident in the monetary union. Anyone now trusting his savings to a southern-European bank must be pretty naive.

It was by far the most stupid and dangerous decision the politicians in the euro zone have made. Europe’s finance ministers have knitted the Cyprus package with hot needle – and triggered a fire storm.

The fatal mistake was to try to overturn deposit insurance for savers. What’s important is not the formal legal nature of the guarantee but its credibility in Cyprus and elsewhere. In the euro zone deposits are insured up to 100,000 euros. If now the government comes and says: we’ll take money by a property tax, then the trust is gone. This action constitutes theft.

When Tanks Are Needed

Reader Bernd translated the final two paragraphs as follows …

“Readers of my column know, that I have always defended the Euro, including the instruments (tools) needed to make it a success. However, there comes a point when it is no longer morally acceptable to uphold a currency if Governments and Parliaments do not have the will and the insight to manage it properly.

The day approaches when the Euro can only be defended with tanks. When that happens, the Euro will no longer be worth defending”

And so here we are, at long last, with ardent supporters finally questioning whether this experiment can work. The answer should now be obvious to all: it can’t.

So we finally need to do what I suggested long ago, start frank discussions on how to break up the eurozone in the least disruptive manner.

Wine Country Conference

I am hosting an economic conference on April 5 in Sonoma, California. Proceeds go to the Les Turner ALS Foundation (Lou Gehrig’s Disease).

Please see My Wife Joanne Has Passed Away; Stop and Smell the Lilacs for my association with the disease.

To learn about the economic conference with world-class speakers including John Hussman, Michael Pettis, Jim Chanos, John Mauldin, Mike “Mish” Shedlock, Chris Martenson with guest moderator Lauren Lyster and other Special Guests, please visit Wine Country Conference April 5, 2013

Bank run in New York in 1933.

You can be forgiven for thinking that you don’t need to give a hoot about what’s going on in Cyprus this weekend.

After all, it’s just a little island somewhere in the Mediterranean.

But what’s going on in Cyprus could actually matter — not just to the rest of Europe, but to the rest of the world.

Here’s the short version of what’s happening:

Cyprus’s banks, like many banks in Europe, are bankrupt.

Cyprus went to the Eurozone to get a bailout, the same way Ireland, Greece, and other European countries have.

The Eurozone powers-that-be gave Cyprus a bailout — but with a startling condition that has never before been imposed on any major banking system since the start of the global financial crisis in 2008.

The Eurozone powers-that-be (mainly, Germany) insisted that the depositors in Cyprus’s banks pay part of the tab.

Not the bondholders.

The depositors. The folks who had their money in the banks for safe-keeping.

…….much more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair