Gold & Precious Metals

For those that view gold as a poor investment or hedge against currency devaluation need to consider the charts illustrated below. The first chart was produced by Thomas Gresham of Gresham’s Law. “When a government compulsorily overvalues one type of money and undervalues another, the undervalued money will leave the country or disappear from circulation into hoards, while the overvalued money will flood into circulation.”[1] It is commonly stated as: “Bad money drives out good”, but is more accurately stated: “Bad money drives out good if their exchange rate is set by law.”

The Long-Term Fundamental Case for Gold

“No State shall enter into any Treaty, Alliance, or Confederation; grant Letters of Marque and Reprisal; coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts; pass any Bill of Attainder, ex post facto Law, or Law impairing the Obligation of Contracts, or grant any Title of Nobility.”

~ United States Constitution, Excerpt from Article 1, Section 10 ~

A quick glance at most of the headlines over the weekend and the primary focus seemed to be either calling a near term top in domestic equity indices or a focus on the Greek debt situation. Why is anyone even paying attention to what is going on over there? Until the ISDA declares a default where the underlying Credit Default Swaps (CDS) are triggered, it is all just noise.

The ECB has broken the rule of law by placing itself as the senior creditor ahead of private creditors, the Greek government is trying to pass retroactive legislation to trap private sector creditors holding out of the PSI, and the leader of Greece was not even elected by the people of Greece – how much more manipulation and insanity do we need to monitor?

Similar to the price action since 2008, central banks around the world control everything from financial markets to the ascent of political leaders. These same political leaders help central bankers and planners control policy and decision making at the highest government levels in Europe and around the world. It would seem that the United States should change the motto from “We the People” to “We the Bankers.”

However, there is one particular asset class that even the central bankers have a hard time controlling. While they can impact short term price action through direct currency manipulation initiatives, in the longer-term gold is likely to move in only one direction – higher.

The price action on Tuesday reminded market participants that actions such as the Greek bailout come at a cost. Quantitative easing and/or printing money (depending on what one wishes to call the practice of producing fiat currency out of thin air) has a direct impact on the price of gold.

Many financial pundits argue that gold has no utility, but what they fail to recognize is that gold is the senior currency to all other fiat currencies. Silver is also a form of currency and is senior to all other fiat currencies as well. While one can draw the utility of gold into question, the idea that gold is the senior most currency to all other fiat currencies is not new.

The Constitution of the United States of America, which is over 200 years old, refers to gold and silver as forms of payment. Looking back thousands of years the Romans used gold coins as a form of currency. The idea that gold and silver are currencies is certainly not a grandiose thought or a stretch of historical concept. Trying to depict gold as a worthless asset depends on your view and consideration of fiat currency.

There are those that would argue that the Federal Reserve of the United States is not actively manipulating economic conditions domestically or abroad. For those that view gold as a poor investment or hedge against currency devaluation need to consider the charts illustrated below. The chart below was produced by Thomas Gresham of Gresham’s Law.

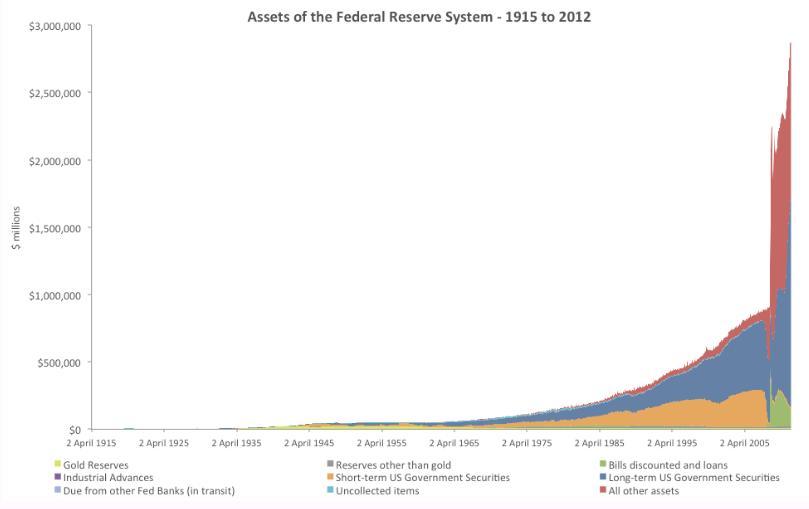

Total Asset Growth of the Federal Reserve System – 1915 – 2012

It is rather obvious by looking at this chart that the Federal Reserve has actively sought to enter domestic and foreign financial markets. The surge in balance sheet assets serves to prove how far the Federal Reserve Bank is willing to go to maintain markets which seemingly are only allowed to move higher over time.

This chart is bearish for nearly any form of paper backed assets. The above referenced chart is long-term bearish for the Dollar and Treasuries and long-term bullish for physical gold and silver. As the Federal Reserve continues to debase the U.S. Dollar in concert with other central banks’ monetary easing programs, gold and silver prices over time are destined to move higher in virtually every form of fiat currency.

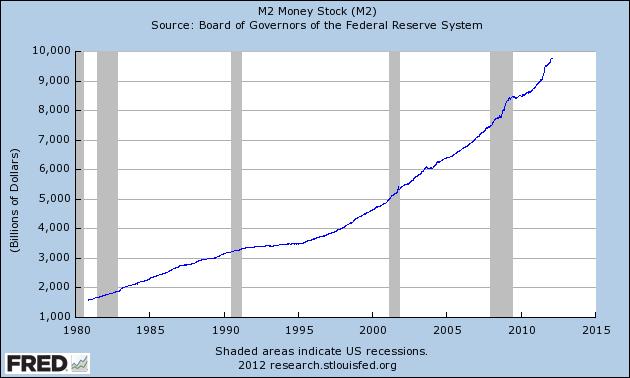

During the same time frame that the Federal Reserve has seen its balance sheet grow exponentially, the rapid rise of M2 money supply is staggering. The long term chart of M2 is compared to gold futures in the charts presented below.

M2 Money Stock

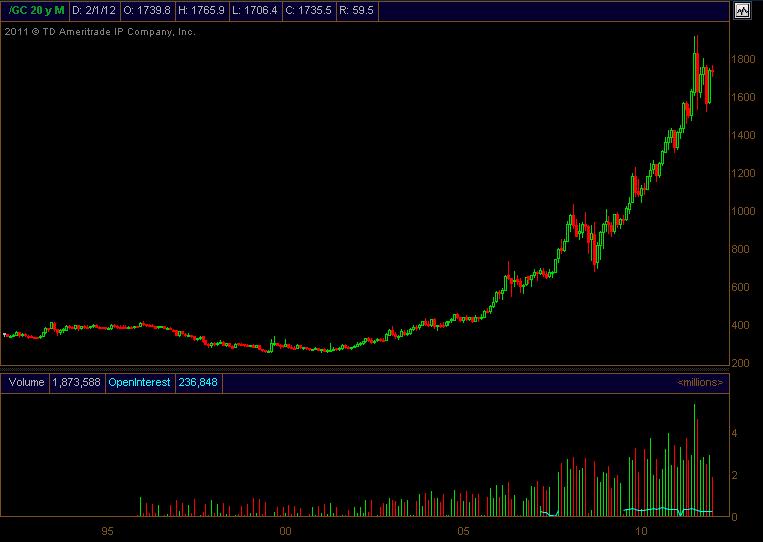

Gold Futures Monthly Chart

It is rather obvious what has happened to the price of gold as the M2 money supply has grown. The idea that the Federal Reserve has not already destroyed a significant amount of the purchasing power of the Dollar can easily be refuted by the two charts shown above.

In the short-term, gold and silver could suffer from a pullback, but in the intermediate to longer term it is unlikely that we have seen the highs of this bull market for either metal. As long as central banks around the world continue to print money and expand their balance sheets gold and silver will remain in a long-term bull market. The daily chart of gold futures is presented below.

Gold Futures Daily Chart

As can be seen above, it is not out of the question that we could see gold pullback to test one of the key moving averages in coming days/weeks. However, I expect the key support area to hold in the event of a sharp selloff. Ultimately, I expect to see a breakout over the resistance zone in the days/weeks ahead. However, I would not be surprised to see gold consolidate or work marginally lower from current prices before breaking out to the upside. Right now the primary threat in this fledgling gold rally is a short-term spike higher in the U.S. Dollar. The primary catalyst which could drive a flight to the Dollar involves the sovereign debt situation in Greece and the Eurozone as a whole.

While the short-term price action may be bearish, the intermediate to longer term time frames are quite bullish for metals as central banks will continue to race to debase their currencies. Quantitative easing in the U.S. and around the world will become pervasive and gold prices could potentially soar in value. The data from the Federal Reserve Bank itself suggests that they are indeed increasing the money supply. As time has passed, the money supply and gold have seemingly grown in lockstep with one another. Surely inquiring minds do not consider this mutual relationship between gold and the money supply to be purely coincidental.

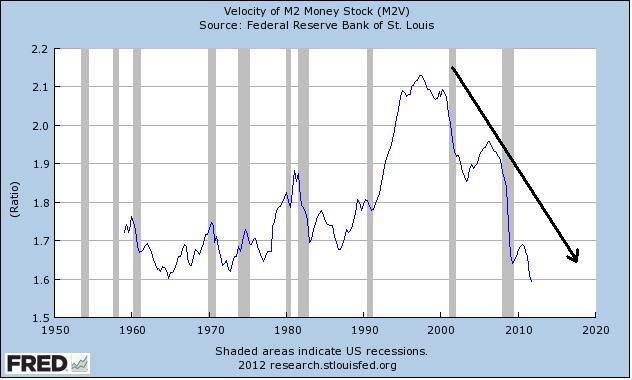

As further evidence that the Federal Reserve continues to use quantitative easing to manipulate asset prices through direct entry into financial markets, a chart of the velocity of M2 clearly depicts that the velocity of money is declining. I am not an expert regarding macroeconomic data, but if the velocity of money is declining to 1960’s levels would it be a stretch to say that we may be going through a period of stagflation? The chart below illustrates the Velocity of M2 Money Stock courtesy of the St. Louis Federal Reserve Bank.

Velocity of M2 Money Stock

For those unfamiliar with the term velocity of money, it is simply the rate of turnover in the overall money supply. The velocity of M2 is expressed as the number of times that a Dollar is used to purchase final goods or services which are included in the total gross domestic product.

Conclusion

The short term technical picture in gold is a bit suspect due to overhead resistance and recent U.S. Dollar strength. However, the longer term macro factors that impact the value of the U.S. Dollar and precious metals are all telling us the same thing.

As time wears on and central banks do even more to prop up the broader economy and failing financial institutions, it is without question in my mind that gold and silver will both benefit handsomely from these decisions being made by central bankers from around the world.

Ultimately, I am very bullish of gold and silver in the intermediate to longer-term, but in the immediate short-term frame gold could consolidate or pullback before breaking out to the upside.

By: Chris Vermeulen – Free Weekly ETF Reports & Analysis: www.GoldAndOilGuy.com

Co-Author: JW Jones – Free Weekly Options Reports & Analysis: www.Optionnacci.com

This material should not be considered investment advice. J.W. Jones is not a registered investment advisor. Under no circumstances should any content from this article or the OptionsTradingSignals.com website be used or interpreted as a recommendation to buy or sell any type of security or commodity contract. This material is not a solicitation for a trading approach to financial markets. Any investment decisions must in all cases be made by the reader or by his or her registered investment advisor. This information is for educational purposes only.

Dustan Woodhouse was one of the six Personal Finance workshop presenters at this year’s World Outlook Financial Conference. As the world markets reel from one debt disaster story to another Dustan discussed the practical realities, pitfalls and opportunities of personal debt in the days ahead.

To see Dustan’s complete PowerPoint presentation – CLICK HERE

For more information contact him at www.ourmortgageexpert.com .

Sometimes the most exciting investment opportunities fly under the radar. James Passin of Firebird Management LLC combs the world for emerging opportunities in often overlooked areas. In this exclusive interview with The Critical Metals Report, he discusses companies producing critical materials that could revolutionize defense and aviation technology and make nuclear power safer and more efficient. He also shares some commodities growth stories currently unfolding in Mongolia and East Africa.

The Critical Metals Report: It’s been over two years since you last spoke with us. How have macroeconomic events affected your investment strategy?

James Passin: I am not going to discuss specific investment strategies. But it’s interesting to take a careful look at the current environment, in which there remains a huge amount of fear regarding the solvency of the world financial system. At the same time, there’s clear evidence of growth returning to the USA and certain other regions, although interest rates are near zero and central banks continue to print money. So, I see a situation in which powerful opposing forces at are work, a situation which may continue to manifest itself in violent, short-term fluctuations in asset prices.

I think that the global risk appetite is in a recovery process and that this will gradually lead to more stable capital markets, which should, generally, be positive for equity valuations. But the fear of black swans has kept a lot of cash in the sidelines. There is a danger in remaining out of the market in the current negative interest rate environment.

TCMR: What are you expecting with commodity prices in the next year or so? Will China’s growth continue, or is the country in a bubble?

JP: China has attempted to engineer what the media is calling a “soft landing,” to try to weaken real estate prices and restrain inflation. To some extent, it seems that its policies have been successful. If inflationary pressures in China continue to moderate, then the central bank should have room to loosen credit conditions. This should help to offset economic weakness.

When you look at the strength in copper, the Australian dollar and other leading or coincident indicators of Chinese economic activity, it’s very hard to take a bearish outlook on China. Major Chinese stock indexes have held at support levels and are starting to bounce. So, overall, I expect China’s economy to be somewhat constructive for commodity prices.

TCMR: Do you anticipate any significant potential disruptions to the global economy?

JP: I think we are going to see mergers and acquisitions in the commodity space following the recent high-profile merger of two very large affiliated companies, Glencore International plc (GLEN:LSE) andXstrata PLC (XTA:LSE). Companies that work closely with governments are in a position to implement strategic industrial policy, which may trigger a wave of consolidation in the commodity space and a struggle for control of a limited universe of valuable mineral assets. That environment would create a very positive scenario for the prices of mining companies’ securities in general.

TCMR: Would you say the giant majors and governments of developing nations are competing for assets at the lower end of the food chain?

JP: There’s a lot of evidence to support this view. Indian companies now seem to be on the hunt and there are a lot of buyers for world-class resources. A number of companies that control world-class resource projects seem to have very compelling valuations, following the horrendous equity market in fourth quarter of 2011. I suspect we are going to see a huge number of merger deals, hostile takeovers and various forms of consolidation, reducing the supply of commodity shares.

TCMR: You are invested in critical and strategic metals. What looks attractive to you in those investment areas?

JP: One area we’re focused on is fluorspar, which is an important mineral used in a number of metallurgical processes, such as aluminum production. It’s also the raw material necessary for the production of hydrofluoric acid, which is the precursor to all hydrofluoric chemicals and a number of products containing fluorine or made through the process of fluorination. It’s an obscure commodity, but it is critical to modern life and to the world economy. In fact, it’s so strategic that the EU put it on the list of critical commodities. There has been a lot of government angst about the availability of fluorspar because China controls approximately 50% of world fluorspar production. China was once a fluorspar exporter, but the country is moving more toward exporting value-added chemicals and consuming the raw chemicals itself. That means the rest of the world has to look for non-Chinese sources for fluorspar. There are very few sources of fluorspar from operating mines and not many deposits can be brought into production in the near future either.

TCMR: What are some companies focusing on fluorspar production?

JP: I would suggest taking a look at Fluormin Plc (FLOR:AIM), listed on the AIM Market of the London Stock Exchange. Fluormin owns the producing Witkop fluorspar mine in South Africa as well as 20% of a producing Kenyan fluorspar company. It has other fluorspar exploration projects in various African countries and a joint venture with a fluorspar trading company. Fluormin is a significant producer and trader in the global fluorspar industry. The company is controlled by Firebird and I serve with another colleague on the board of directors.

TCMR: Last time we met, you discussed IBC Advanced Alloys Corp. (IB:TSX.V; AALF:OTCQX). What’s going on with that company?

JP: The stock has been somewhat stagnant, but IBC Advanced Alloys has been growing its revenue. We’re intrigued by the company’s Beralcast business, which involves an aluminum-beryllium composite material with unique characteristics that make it attractive in defense aviation platforms and, potentially, in various commercial aviation applications. It could be a game-changer when you look at the market for beryllium-aluminum composite materials. The company is also exploring for beryllium in Utah, with some promising recent results. I should note that IBC was co-founded by Firebird and Firebird remains a significant shareholder in the company.

TCMR: You cover a wide range of investment arenas both geographically and in terms of commodity type. What looks promising in the energy arena?

JP: Since we started following East African oil in 2003, there have been a number of very large, important discoveries, the most famous of which was Heritage Oil Corp. (HOC:TSX; HOIL:LSE) discovery in Uganda, which proved the existence of world-class oil basins in the Great Rift Valley, precipitating a wave of strategic interest in East Africa. At the same time, evolving geopolitical dynamics are now supportive to East African oil development. For example, South Sudan’s independence created momentum for a new pipeline that can potentially link offshore East African oil fields to export markets, creating a platform for monetization of otherwise stranded oil deposits.

TCMR: What companies in this space are you considering?

JP: I am the Chairman and Interim CEO of Vanoil Energy Ltd. (VEL:TSX.V), which has two blocks in Kenya. Given the amount of interest in Kenya now and the number of deals that we can point to in East Africa, I think it’s worth considering independent companies with acreage in Kenya and the surrounding countries. Vanoil has had some encouraging results from its seismic program and we look forward to advancing further work on our Kenyan properties under the terms of our Production Sharing Contracts. Firebird’s East African holdings include Africa Oil Corp. (AOI:TSX.V), a Lundin company. It has a number of interesting oil exploration projects in East Africa, and the company is currently drilling on two properties, one in Kenya and one in the Puntland Province of Somalia. I’ve been to the Somalian oil concession—it has the potential to prove the existence of Yemen-size oil basins in the Horn of East Africa.

TCMR: You also mentioned Mongolian coal. What’s going on there?

JP: Mongolia has a host of remnants of the sea that vanished when the Indian and Asian subcontinents collided a long time ago. Those remnants formed a vast sedimentary basin that has been transformed into one of the world’s largest undeveloped coal provinces, with both thermal and coking coal. Mongolia’s thermal coal story is quite interesting. China is now the world’s largest importer of thermal coal, while India has very limited supplies of thermal coal. Mongolia will inevitably emerge, in my view, as an important regional thermal coal supplier.

Also, Mongolia is the world’s fastest-growing economy. This is creating a growing need for new electricity generation capacity. The country’s large thermal coal deposits have an important role to play in providing domestic energy. There’s a wave of new interest in Mongolia from strategic and financial investors. We think that the country’s real 2011 gross domestic product (GDP) is probably going to end up 18% higher than the prior year. We believe this GDP is going to keep compounding at a very high rate over the next 10–20 years.

TCMR: How can investors participate in the market in Mongolia? There is a stock exchange there, but not many companies, and liquidity is low. What’s the story there?

JP: We’re very active investors in the Mongolian Stock Exchange (MSE). Certainly the market is not liquid, but there are no restrictions on foreign ownership of shares, and the currency is freely exchangeable. It is very easy to open and fund a brokerage account. The hard part is sourcing shares. The London Stock Exchange (LSE) is now managing the MSE under a three-year contract. We’re quite optimistic about the potential for liquidity on the MSE to increase in the future. Some thermal coal stocks are listed on the MSE, such as Sharyn Gol JSC (SHG:MSE), a coal producer controlled by Firebird. There are other coal companies with assets in Mongolia that are listed on other major exchanges, although we don’t have a particular view on those companies.

TCMR: Let’s switch to nuclear. The U.S. Nuclear Regulatory Commission (NRC) granted some licenses in the last few weeks—the first ones in nearly 35 years. What effect is that going to have on the nuclear fuels and related industries and equipment suppliers?

JP: Although I’ve generally reduced my focus on the nuclear industry following our broad exit from the space during the uranium bubble in 2006, we remain long-term bulls on nuclear power. It is the only economic means of producing electricity without producing vast amounts of carbon. Many government policies will most likely continue to provide at least some economic inducement for nuclear power generation. China will continue to build new nuclear reactors irrespective of the changing political sentiment in some countries following the Fukushima disaster. My focus is mainly in companies that are providing essential services to the nuclear industry and are positioned to benefit from the continued long-term growth in nuclear power generation capacity.

TCMR: What service companies appeal to you?

JP: A U.S. company, International Isotopes Inc. (INIS:OTCBB), is seeking a Nuclear Regulatory Commission (NRC) permit to build the first and only uranium de-conversion and fluorine extraction plant in the world. This plant will take depleted uranium hexafluoride, the toxic waste byproduct of uranium enrichment, and convert it into a stable form of depleted uranium, while extracting the commercially valuable fluorine content. The resulting waste material is far safer and cheaper to store and transport than depleted uranium hexafluoride. If this plant is financed and built and operates successfully, it should significantly reduce the environmental impact of the nuclear fuel cycle.

TCMR: How much commercial value is there in the fluorine? Will the company see substantial profits from producing safer uranium?

JP: I expect the company to have two major revenue streams. The first would be the payment it receives for de-converting uranium hexafluoride, as this provides a direct benefit to the producers of depleted uranium hexafluoride. The second revenue stream will come from extracting the fluorine content and producing fluorine gases and other fluorine products, which it can sell commercially.

TCMR: How large is the fluorine gas market and what kind of sales could International Isotopes expect?

JP: I don’t want to get into financial projections, but the fluorine market is quite large. If you look at all of the fluoride chemical products, especially fluorine gases and products made through the process of fluorination, it is an immense market. I would note that Firebird is a significant shareholder in International Isotopes.

TCMR: We appreciate your time and thoughts today.

JP: My pleasure.

James Passin joined Firebird in 1999. James is a graduate of St. John’s College, where he majored in philosophy and classical literature. James serves on the board of directors of several Mongolian and Canadian companies, including Sharyn Gol JSC, Baganuur JSC, BDSec JSC, National Investment Bank of Mongolia, Vanoil Energy Ltd., Undur Tolgoi Minerals Inc. and Fluormin PLC, a UK fluorspar mining company.

Want to read more exclusive Critical Metals Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about critical metals companies, visit our Critical Metals Report page.

DISCLOSURE:

1) Zig Lambo of The Critical Metals Report conducted this interview. He personally and/or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Critical Metals Report: IBC Advanced Alloy Corporation. Streetwise Reports does not accept stock in exchange for services.

3) James Passin: I personally and/or my family own shares of the following the following companies, either directly or through indirect ownership through funds and related business entities, mentioned in this interview: Vanoil Energy, Ltd., Fluormin PLC, Sharyn Gol JSC, International Isotopes Inc., IBC Advanced Alloy Corporation and Africa Oil Inc. I personally and/or my family am paid by the following companies mentioned in this interview: none. I was not paid by Streetwise for participating in this story.

“So what?” he asked. “Things will only get worse. We have reached a point where we’re trying to figure out how to survive just the next day, let alone the next 10 days, the next month, the next year.”

-Anastasis Chrisopoulos, Athens taxi driver (from Reuters)

130-billion-euro here, 130-billion-euro there, and pretty soon you have to start finding some growth!

One adage that seems to work as much as anything else, and why it is an adage I guess, is “buy the rumor and sell the news.” I won’t bore you with the behavioral aspects of why this works, I think you know. We are seeing it a bit this morning on display on news a Greek default has been averted: the euro is lower, and ditto for most Eurozone bonds since the announcement of a deal that gives Greece another 130-billion-euro it can pour down the rabbit hole with the rest of the money funneled in by Eurozone taxpayers.

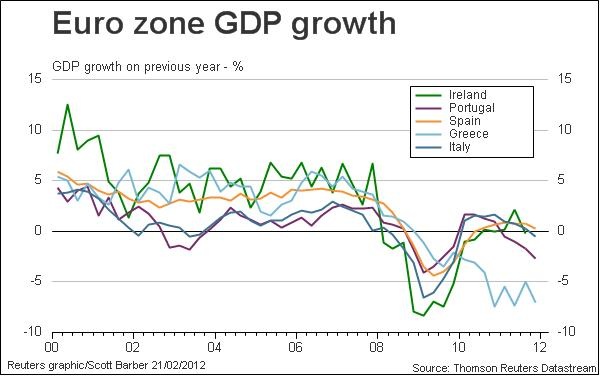

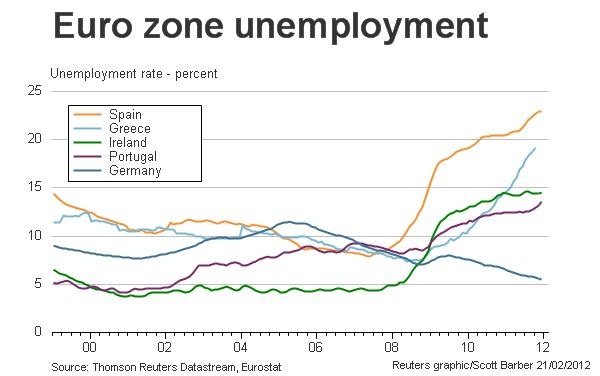

Of course, sooner or later financial engineering reaches the limits of its public relations effect and there must be some underlying payoff from said engineering besides getting funds to follow banks chasing into periphery debt for a trade. It’s not that rising periphery bond prices, i.e. lower yields, isn’t helpful; it is. But even at current rate levels, it will be mighty hard for many countries to maintain austerity pledges; all attempts to do so will likely accentuate the trend we see in the chart below:

And of course, this chart is the mirror image of the domestic adjustments periphery countries have to make because they do not have a free-floating currency available to help them make these adjustments:

Thus, periphery economies desperately need some growth. Rising unemployment and tighter budgets will not produce revenues needed to pay debt; instead it produces a self-feeing vicious spiral downward. This view seems completely at odds with the Troika program even though the Greek economy provides them with live test case of abject failure stemming directly from the implementation of their own flawed theories.

And here is why it will likely get worse for Greece and other periphery countries whose growth is heading lower—the real economy will be starved.

We have already witnessed this economic/money/manipulation phenomenon in the US, from the WSJ this morning:

“The eight giant European banks that have disclosed their annual results in recent weeks reported holding a total of about $816 billion in cash and deposits at central banks as of Dec. 31. That is up 50% from a year earlier, when the same banks were holding roughly $543 billion.”

Does any of this sound familiar? You can lead a horse to water, in fact you can force-feed said horse with massive amounts of reserves, but you can’t make him lend any of it to the real economy where real people build real businesses and hire other real people who need real jobs.

Just in case you forgot just how tightly US banks have held on to their Fed sponsored reserves via the massively steep yield curve that impoverishes savers to subsidize bank healing, here is a look. This chart shows reserves in the US banking system … hmmm … three years and counting so far since Bernanke and Company decided this is the only viable strategy for the economy. Viable for financial assets, but the other side of the economy is still starved …

The point is, despite the new Greek rescue (I am losing count how many we have had so far), it appears the Eurozone, now clearly a two-track world with Germany bathing in credit and low rates and low unemployment (which adds to more angst and animosity toward Germans amongst the PIIGS), appears collectively heading into deeper recession.

One wonders if now, finally, EU leaders have run out of rabbits of financial engineering to pull from their hats. Financial engineering is a lot easier than real growth. If you don’t believe me, go ask Goldman; after all it is their fun and games that caused much of this Greek problem in the first place.

Hmmm …

Downside risk in equity markets and most sectors exceeds short term upside potential. Short term weakness will provide an opportunity to enter into seasonal plays this spring including Energy, Mines & Metals, Chemicals and Auto sectors. Energy already is showing early signs of seasonal strength.

Equity Trends

The S&P 500 Index added 18.59 points (1.38%) last week. Intermediate trend is up. The Index remains well above its 50 and 200 day moving averages. Short term momentum indicators are overbought and showing early signs of peaking.

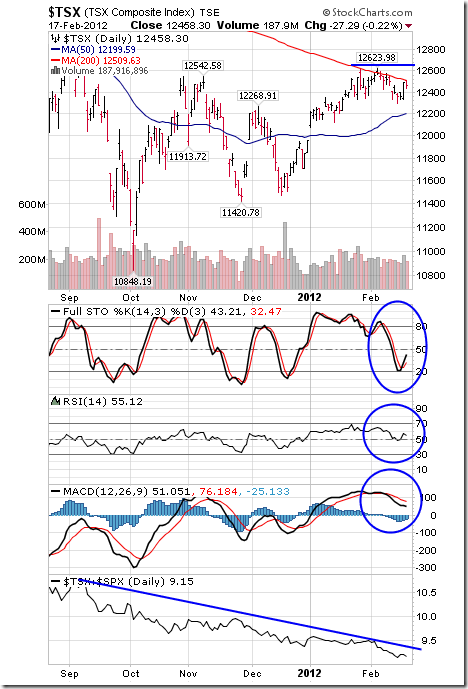

The TSX Composite Index added 68.88 points (0.56%) last week. Intermediate trend is up. Support is at 11,420.78. Resistance has formed at 12,623.98. The Index trades above its 50 day moving average, but recently has found resistance near its 200 day moving average currently at 12,509.63. Short term momentum indicators are trending down. Stochastics already are oversold and showing early signs of trying to bottom. Strength relative to the S&P 500 Index remains negative.

Gold fell $4.20 per ounce (0.24%) last week. Support is at $1,765.90 and resistance is at $1765.90. Gold is close to completing a so called “Death Cross” when its 50 day moving average moves below its 200 day moving average (Tech Talk is not a believer in “Death Crosses, but the media will talk about it). Short term momentum indicators have rolled over from overbought levels and are trending down. Strength relative to the S&P 500 Index remains mildly positive. Seasonal influences tend to peak near the end of February.

Silver slipped $0.41 per ounce (1.22%) last week. Support is at $26.15 and resistance is forming at $34.52 and near its 200 day moving average at $34.96. Short term momentum indicators have rolled over from an overbought level and are trending down. Strength relative to gold remains positive. Seasonal influences are positive until May.

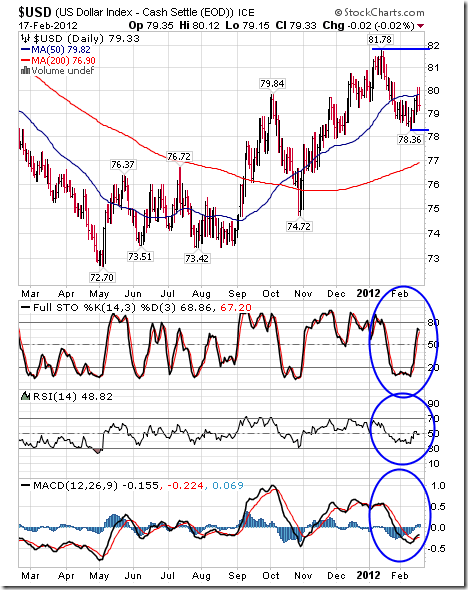

The U.S. Dollar added 0.22 last week. Intermediate trend is up. Support is forming at 78.36 and resistance is at 81.78. The Dollar remains above its 200 day moving average and below its 50 day moving average. Short term momentum indicators are recovering from oversold levels.

The Canadian Dollar added 0.46 cents U.S. last week. Intermediate trend is down. Support is at 95.03 cents and resistance is at 101.10 cents. The Canuck Buck trades above its 50 day moving average, but has found resistance near its 200 day moving average at 100.39. Short term momentum indicators have rolled over from an overbought level and are trending down.

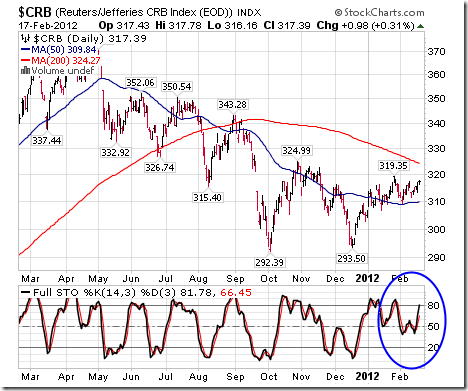

The CRB Index added 3.17 points (1.01%) last week thanks mainly to strength in the energy complex. Intermediate trend is down. Support is at 292.39 and resistance is at 324.99. Short term momentum indicators are trending higher.

Crude Oil gained $6.51 per barrel (6.66%) last week. Intermediate trend is up. Crude broke above resistance at $103.74 on Friday implying intermediate upside potential to $112.75. Short term momentum indicators are overbought, but have yet to show signs of peaking. News over the weekend that Iran has halted exports of oil by French and United Kingdom companies adds to a bullish stance. Seasonal influences remain positive.

Don Vialoux has another 30+ charts, analysis and guest contributors HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair