Energy & Commodities

Examining the macro-economic environment is how Jim Letourneau, publisher of the Big Picture Speculator, likes to begin his stock-picking process. However, his understanding goes beyond headline news to reveal surprising investment themes with profit potential. In this exclusive interview, Letourneau talks about the hype and commodity investment cycles and where to dig for blue-sky stocks.

COMPANIES MENTIONED: BIOASIS TECHNOLOGIES – DNI METALS INC. – ENERGY FUELS INC. – METHANEX CORP. – TALVIVAARA MINING CO. PLC. – UR-ENERGY INC. – URANERZ ENERGY CORP. – URANIUM ENERGY CORP. –

The Energy Report: You publish the Big Picture Speculator. What does that title imply?

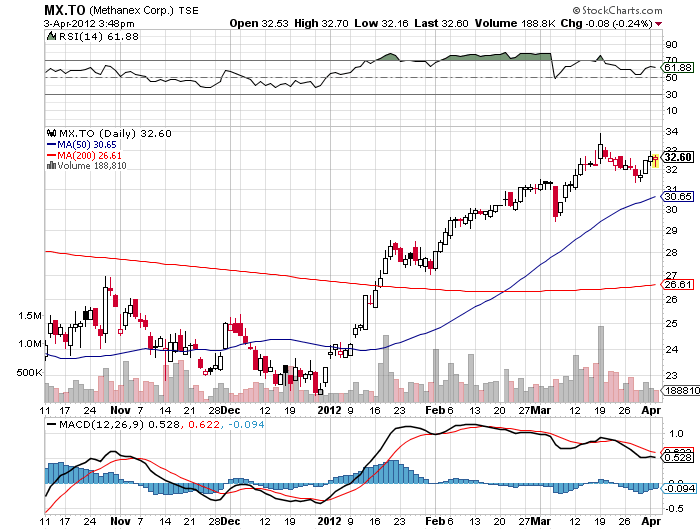

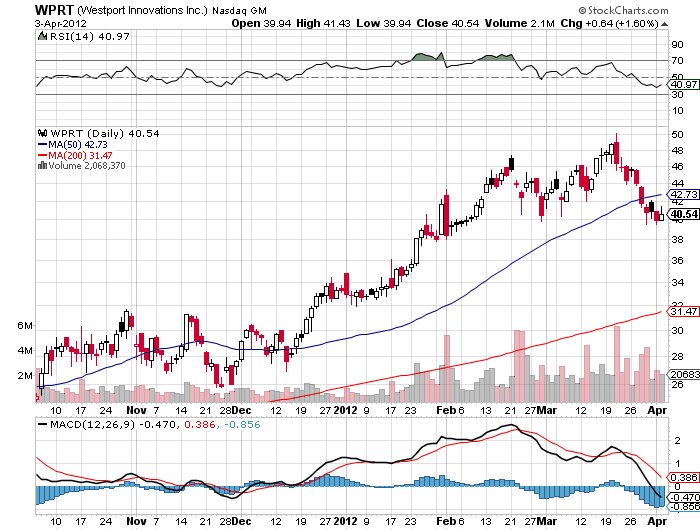

Jim Letourneau: I believe the macro context is often more important than the details about an individual company. I read a broad range of material every day that helps me form my views, and one of my best skills is putting together the big picture and connecting the dots for audiences. A recent example of my method is my coverage of the natural gas sector, which focused on how the abundant supply of natural gas has led to a complete shift in the types of companies that people should be following. Rather than natural gas producers, investors should find companies that are consuming natural gas, like Methanex Corp. (MEOH:NASDAQ; MX:TSX; METHANEX:SSE)

Westport Innovations Inc. (WPT:TSX)

or Energy Fuels Inc. (EFR:TSX). These companies are in great shape because their costs are significantly lower. That’s a huge big-picture shift, but people get bogged down in all of the debates about fracking and other controversies.

The bottom line is the U.S. now has the cheapest natural gas in the world, and that’s not a horrible problem to have. When I talk to technical people, we just look at each other and think this is a miracle. No one saw this coming.

TER: As a geologist, how does your technical knowledge shape your investment decisions? What do you look for in potential investment opportunities?

JL: Technical knowledge includes pluses and minuses. In general, the types of companies I look for are usually going to have a market cap of under $100 million (M) and for me to get excited about them, they have to have the potential to surmount that $1 billion (B) market cap. So there’s a potential tenbagger upside in them, if everything pans out. That potential could be in the form of a new technology backed by a critical management team or a higher-quality mineral property. Either way, management teams are critical for these types of things to play out.

TER: How far down in market cap do you go when considering investments?

JL: Sometimes I go down too far, but I think $50M is better than $5M. While you can argue that it’s easier for a $5M market-cap company to go to $50M, your odds start to dwindle. It’s a matter of finding that balance point. Obviously, it’s nicer to buy a company cheap and have it grow into something bigger, but the company is usually cheap for a reason. I don’t want to have to write about 50 companies a year that didn’t quite make it. I’d rather go up the food chain a little bit and follow ones that are going to survive, and whose progress we can track year by year.

TER: You spoke at the Cambridge House Energy and Resource Investment Conference in Calgary on March 30 and 31. What subjects did you cover?

JL: My keynote talk was called “Making Money Using Commodity and Hype Cycles.” I overlayed two kinds of cycles: The commodity cycle is a longer cycle that we’ve been in for over 10 years now. Hype cycles refer to heightened public awareness of a new technology or a particular element on the periodic table that hasn’t been speculated on yet. A recent example would be graphite. Uranium is another really good example of a hype cycle; there was a huge amount of interest about eight years ago and hundreds of companies were formed. Investors were making lots of money with uranium stocks. Then it all withered away. There is still opportunity because some of those companies are still around and advancing their businesses.

I also did a workshop called “How to Find Billion-Dollar Companies,” where I mentioned some of the companies I like that have market caps near $100M with the blue-sky potential to get up to the $1B level.

TER: What do you think the potential is on a percentage-wise basis of finding billion-dollar companies?

JL: The odds are challenging. This is more speculative and it’s much higher risk than a nice dividend-paying stock with cash flow. These companies have lower market caps for a reason; there is either skepticism about the technology or a lot of competition. We don’t need 100 new rare earth mines, but maybe we have 100 rare earth companies. So which companies are going to win that race? It’s a bit like horse racing; you pick your favorites. The odds are you’re not going to win on every one of them.

TER: For a company to get to a $1B market cap these days is probably going to involve some acquisitions and consolidations, unless it really has some amazing property or technology.

JL: That’s very true. Sometimes companies just lay it out and if you can see that it can get the sales and the trajectory, it is certainly possible, and it does happen. It’s a challenge, and that’s what we’re looking for.

The other important part of the stock-picking process is the timeframe. The commodity cycle has a long-term timeframe, whereas the hype cycles can be pretty brief. Eventually, the market turns and the interest goes away. The challenge for these companies, if they have something real, is to keep moving the project forward until the next hype cycle comes around, when people get really interested again. If you’re investing in equities related to commodities, you’re speculating both in the market and on commodities. Sometimes you can have the right commodity, but the company you pick doesn’t follow that commodity’s price performance very well.

TER: Can you point to any companies you’ve seen in the last few years that have turned out that way?

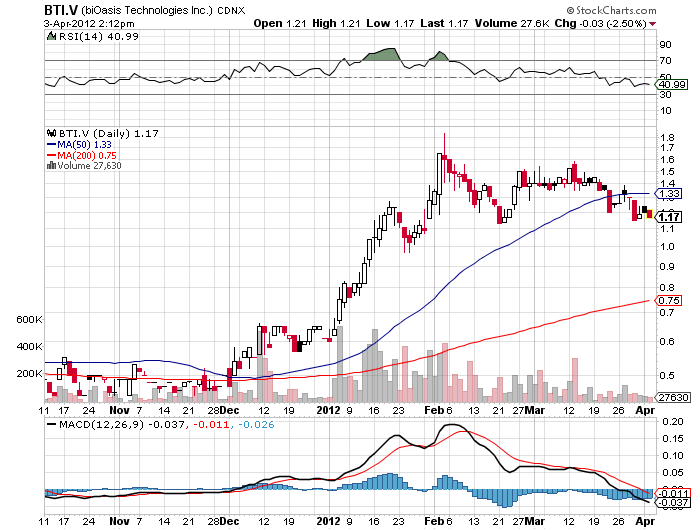

JL: There are a few. To be honest, the other part of this strategy is that for every company that I talk about and like, there are probably 100 that I don’t. There’s a lot of screening and filtering to get rid of the ones that don’t have the potential. One company that I like right now is a biotech that I think we’re at a triple on right now called biOasis Technologies Inc. (BTI:TSX.V). It has a protein that can cross the blood-brain barrier. Therapeutic molecules can be conjugated to this protein, allowing it to cross the blood-brain barrier. This can dramatically increase an existing drug’s effectiveness. That’s one. We found it under $0.50, and now it’s in the $1.40–1.50 range.

DNI Metals Inc. (DNI:TSX.V; DG7:FSE) has also performed really well. While it’s down now, it had gone from around $0.20 to more than $0.60. I like it because it’s pushing the frontiers a little bit. It has a very large, black shale metal deposit in northeastern Alberta, a bit north of the oil sands. Historically, very few geologists studied shales, but they’ve become more popular now because of shale oil and gas. The Alberta Geological Survey has done numerous studies going back to the early 1990s that mention an anomalous metal content in the Second White Speckled Shale. The grades are really low, but the deposits are very extensive. There are huge resources in place containing a whole cocktail of meterials, including rare earths, nickel, iron, vanadium, uranium, zinc, copper, cobalt and molybdenum. It’s almost a conceptual play in some ways. Although the grades are not stellar, they are a little bit higher than we’d expect anywhere else.

So it’s a resource-in-place story, but it’s also a technology story because we’ve seen other industries dealing with a low-grade resource that suddenly become economic plays because of technological breakthroughs. The best example of that is probably shale gas, where people knew for a long time that there was gas in these shales, but nobody was really making any money from them. New technology comes along, and suddenly these shale deposits are worth a lot of money.

For DNI Metals, the challenge is how to get the metals out and make money doing it. The best method to extract these metals is pointing to a technology called bioleaching, which is being used by a company called Talvivaara Mining Co. Plc. (TALV:LSE) in Finland. That’s the exciting part that’s pushing the frontiers.

TER: Are these metals pretty much disseminated throughout this whole deposit, or are certain metals concentrated in certain areas?

JL: The metals are widely disseminated within a fairly uniform and consistent material. That makes it similar to coal or potash mining, where the ore bodies are tabular in shape. They may not be exciting, but at least you know what to expect and you can plan very large operations around that.

TER: With bioleaching, is in situ recovery (ISR) an option?

JL: There may be some way to use ISR, but the bioleaching at Talvivaara involves actually digging it up, piling it onto pads and leaching it by letting the bugs do their work and make acid. But there may be a way to apply in-situ technology in the upper zone. Bioleaching in heaps seems to be the approach with the most potential at the moment.

The value of the minerals in this shale is probably $40 per ton (/t). Extracting the metals for less than $30/t is the challenge. No one’s done it before, so there’s a lot of skepticism. I think a really big mining company would eventually take interest in this because it’s the kind of project that, if it can get up and running, has a life-of-mine potential of over 100 years.

TER: You mentioned uranium earlier. Despite Fukushima, people are realizing that nuclear is here to stay and one of our best sources of energy generation for the foreseeable future. Is there still life after its hype cycle has ended?

JL: I think uranium’s future is very bright and it is a critical part of the world’s energy matrix. We can’t really afford to just turn it off. There actually are a lot of benefits to using it. In terms of the actual price of uranium, the market may not be as excited about it yet, but Russia said it will not renew its supply agreement with the U.S. so analysts are anticipating shortages starting in 2013, which isn’t that far away.

TER: What other companies would you like to comment on?

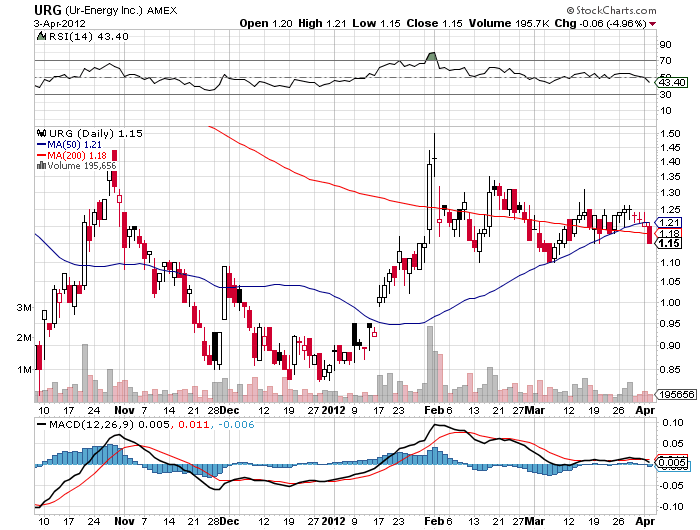

JL: I like the uranium companies that use ISR technology. The main plays I’ve been considering are either in Wyoming or Texas, where you don’t get the really high grades that you find in the Athabasca Basin. There were hundreds of uranium explorers in the Athabasca Basin and the only one that’s really been successful for investors was Hathor Exploration Ltd., which was recently acquired by Cameco Corp. (CCO:TSX; CCJ:NYSE). With an ISR uranium project, you have a degree of certainty that a company will actually be able to build the mine and get it into production.

There are three companies in that space that I like. Going from the smallest market cap to the biggest, there is Ur-Energy Inc. (URE:TSX; URG:NYSE.A), in Wyoming. It’s on track to be a producer very soon with expected permitting for its Lost Creek mine early this summer. Then it will be able to get its mine into production probably within six months.

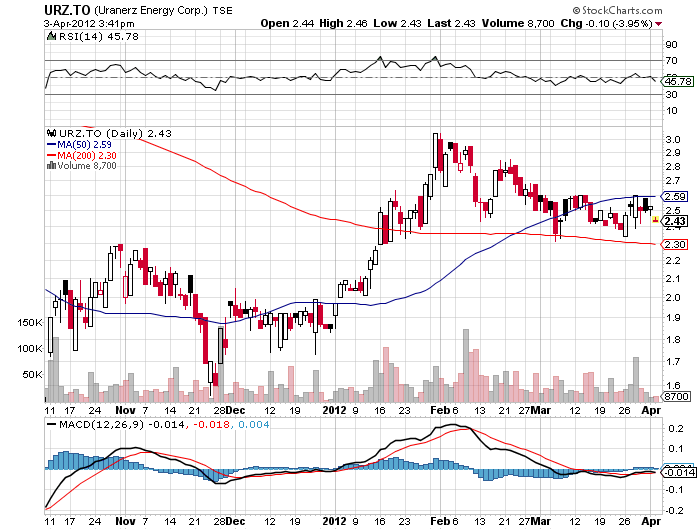

Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.A) is a similar company in Wyoming. It has actually started its mine construction and is looking to start producing 600–800 thousand pounds (Klb) uranium/year very shortly. Both are very near-term production stories.

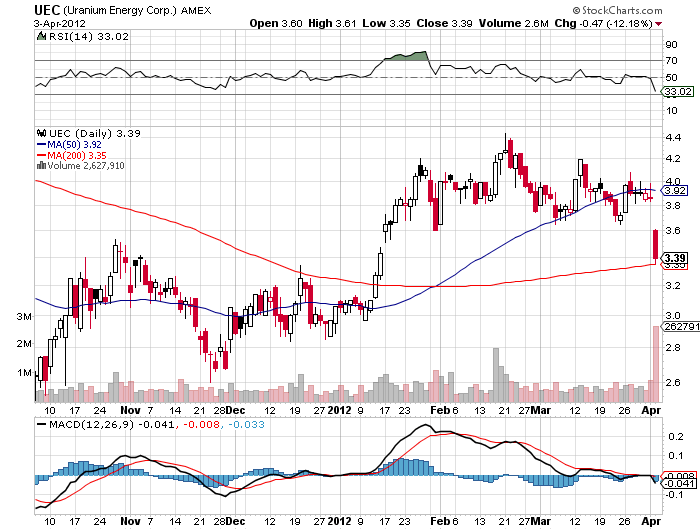

The last one, Uranium Energy Corp. (UEC:NYSE.A), is currently producing in Texas. It has an inventory of projects coming online and the company announced property acquisitions in Paraguay and Arizona earlier this year. These are all companies with uranium resources that, once their facilities are built, enable extremely long production runs. Typically, they’ll have a centralized uranium processing plant and all of the mines around it will be satellite projects.

The challenge for all of these companies has been permitting. The various U.S. government regulatory bodies didn’t really have anyone qualified to evaluate ISR projects because there haven’t been any new ones developed for decades. The absence of a competent regulatory structure has slowed down progress on getting these mines built. These companies have typically spent a year or two longer than they expected on the regulatory process; it’s not a reflection of any gaps in the quality of their projects.

TER: At least the regulators are willing to permit these operations, which apparently was quite a problem for a while.

JL: That’s a very good point. These are viable, useful industries with quite good safety records and low environmental impact. Again, I like to talk about the big picture.

TER: What sort of capital costs do these uranium ISR projects have?

JL: There’s a range, but the costs are usually $20–30/lb. But these companies are pretty comfortable that they can eke out a living at the current uranium price, which is not going to encourage a whole bunch of new projects to come along. They’re anticipating higher longer-term prices, which should make them quite profitable.

TER: Do you have any thoughts on the current gold market?

JL: I just tell people to look at a 12-year gold chart. Gold is probably the best-performing investment product over that timeframe. I personally don’t think gold has that critical a role in the monetary supply, but it is a place to preserve wealth and look for protection. This recent consolidation pullback is probably an opportunity, but people need to remember that bull markets don’t last forever. However, gold still has legs right now, and the trend is your friend.

TER: Looking at the “big picture,” what do you suggest people do to figure out how they should invest their money these days?

JL: Investors have to do their research and be informed. We are in dangerous times. A lot of assets are correlated so it’s hard to find safety. Sometimes maybe the best safety is not even being in the market, which I hate to say. I like finding good companies that are going to grow into viable businesses. But the markets are not kind, and we’ve seen what can happen when the flow of capital gets turned off. The valuations of publicly traded companies, big and small, in all sectors, tend to drop in unison, even precious metals prices. It’s important to be mindful of the downside. I look for upside opportunities because I’m an optimist and I assume that life will go on.

We do have some structural issues in the financial system. If that breaks down, you really don’t want to own anything that’s not tangible. That’s the strongest investment thesis for owning hard assets. That doesn’t mean owning shares in a hard asset company; that means owning the physical hard asset. If you own a car, a house or some gold, those things will still be around no matter what happens to the money supply and currency valuations. The monetary system is a wild card, and that’s the thing that keeps everybody nervous. We can make informed guesses, but nobody really knows how that’s going to play out.

TER: We appreciate your time and input today.

JL: My pleasure.

Jim Letourneau is the founder and editor of the Big Picture Speculator and is a professional registered geologist living in Calgary, Alberta. He has over 20 years of experience in the oil and gas sector.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

The markets, all of them literally, have been betwixt and between over the last couple of weeks. Chopping sideways. Looking at times like they are going to break out to the upside then failing. Moving lower, looking like they’re going to literally plunge at any minute. And then holding support and bouncing back.

This is very frustrating action for most traders and investors. However, I will tell you on a positive note that, when you see sideways action like you’ve seen in most of the markets, that of course is usually a prelude to a very big move.

And on another positive note, I do see this betwixt-and-between action — this sideways action — coming to an end very soon, probably by the end of this first week in April.

I want to go to the charts now. First, the gold chart. This is the gold chart that I’ve had up for the past month or so and been using to show you the action in gold. As you can see here, this is the rally that failed in February and failed to give a monthly buy signal.

Gold started to drift lower and is now pretty much in no-man’s land between support down here and resistance up here. I will tell you that the March closing for gold was not bullish, but it wasn’t very bearish either. So that’s indicative that gold is still in a sideways market, drifting lower.

I do expect as I just indicated that we will start to see some action soon in gold and all of my indicators point to a resolution of this sideways action to the downside.

Having said that, let’s now take a look at silver. Silver looks very similar to gold. The rally failed back here, which I showed you. Silver failed to give a monthly buy signal at the end of February. Since then, throughout March we’ve been drifting lower in a choppy, sideways slightly lower action.

It does look at times that silver’s going to collapse; yet it continues to hold support around the $32 level. Like gold, I expect a resolution to this sideways action in silver and very soon, probably by the end of this first week in April.

All of my indicators continue to suggest that another sharp decline in silver is the most likely outcome.

Now let’s move on to the U.S. Dollar Index. Again here, we’ve seen the dollar weaken to test support. But not a very impulsive decline here — rather, drifting lower. It looks kind of sharp on the chart, but it’s been a rather slow decline to support here.

I do believe we will hold this level of support and the next move in the dollar, which should come very soon, should be to the upside.

Now the Dow Industrials. The Dow Industrials are really holding support magnificently ever since we closed above the 12,849 level. The Dow being the only market that gave a monthly buy signal at the end of February, as I’ve indicated to you before, and now it’s consolidating.

Many of my indicators suggest the Dow and the broader stock markets in general are overbought and we should see some kind of correction. If you’re one of my trading subscribers who attended last week’s Resource Windfall Trader webinar, I did indicate to you that Dow 9,100 is now off the table.

I do expect some kind of shakeout in the Dow before the full force of the bull market of the Dow hits. So I wouldn’t be surprised to see a move down in the Dow. But it’s really quite fascinating how the Dow was holding this support area here and looking so rock-solid.

Even if we get a dip, a correction, in the Dow, there’s no question in my mind now that a new, long-term bull market in the Dow is forming. One that I’ve been talking about for some time now, and it will see the Dow and broader stock markets move substantially higher over the next few years as a result of the European sovereign debt crisis and the U.S. sovereign debt crisis.

The money that will be coming out of European bonds and U.S. government bonds has to go somewhere and it’s going to seek out safety, capital appreciation and income in the way of dividends and royalty in the stock market in addition to gold in a safe haven going forward. So keep that in mind.

Stay tuned to all my writings and have a good week.

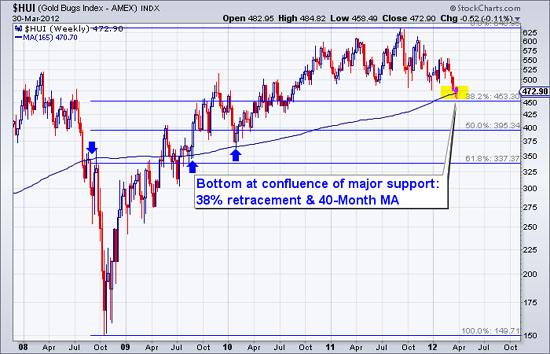

The gold stocks have frustrated investors for several reasons. First, the sector has had a general inability to keep pace with gold and that struggle has been particularly incensing over the last year in which gold has gained. Second, the substantial rebound in the equity market has provided no lift. We know that the gold stocks can be vulnerable when gold falls and when the stock market is plunging. Yet, the gold stocks did not respond as expected despite the reverse favorable conditions in the past year. In the words of a friend, these stocks couldn’t advance if a rocket ship landed up their ass! It is time to bail, right? Wrong! Considering the extreme negative sentiment and our technical work, we believe the market made an important long-term low last week.

First, let’s look at the large caps, which have really struggled over the past six months. Sure, the HUI broke to new 52-week lows but the market has been so oversold for so long that this breakdown didn’t initiate downside follow through. Veteran observers of the sector know that there are numerous false breakouts and breakdowns. Over the past two weeks, the HUI has formed bullish hammers, which is a sign of a reversal. More convincing is the fact that the market bottomed at the 38% retracement. Finally, consider the 40-month moving average. It provided key support at the 2007 bottom, resistance in 2008 and early 2009 and then support in early 2010.

Moving along, we show a daily chart of our proprietary gold stock index, which contains the 10 largest and strongest companies. This market was able to hold its December low after a pair of retests in the last two weeks. An advance above 75 and a weekly close above 75 this week should confirm the bottom.

If that is not enough evidence then consider the junior market. In reality, the companies that comprise the GDXJ and ZJG.to ETF’s are mid caps and small caps and not juniors. That being said, these ETF’s offer us insight into another important part of the sector. The weekly chart below shows both markets potentially completing important double bottoms. More important, while the HUI (large caps) made new lows GDXJ and ZJG.to did not. That is an important positive divergence.

The reality is that the gold stocks have been correcting what was a substantial two-year recovery. Pull out a historical chart of this sector and you will observe that it often is either in a state of a strong impulsive advance or a consolidation that lasts months and months. Remember, the 18-month consolidation from 2004-2005? Remember the consolidation from 2006 to 2007? Apparently, most gold bugs and gold investors do not remember how accustomed this sector is to significant drawdowns and persistent range-bound activity. We admit it is difficult to keep it all in perspective.

All one can do is maintain a level head and accumulate at times like this and take profits when the market and sentiment are extended. Now we see sentiment that echoes the 2008 crash. Anecdotally, there is talk on several gold-bug forums of throwing in the towel, giving up and considering other sectors. The more extreme gold bugs are out with their “only physical” mantra, which comes precisely at the wrong time. Through careful stock selection and basic market timing, an investor can utilize the equities to far outperform. That is what we focus on in our premium service. Consider learning more.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com“>Jordan@TheDailyGold.com

TheDailyGold

Those interested in doing some spring cleaning in their portfolios this month might be tempted to do the most radical spring cleaning of all: Sell everything and go to cash.

That’s because April represents the end of the seasonally favorable six-month period that began last Halloween, and the fast approach of the time when many will “Sell in May and Go Away.” Should you try to get a head start on those who mechanically wait until May Day to do their selling?

To read the full article click here

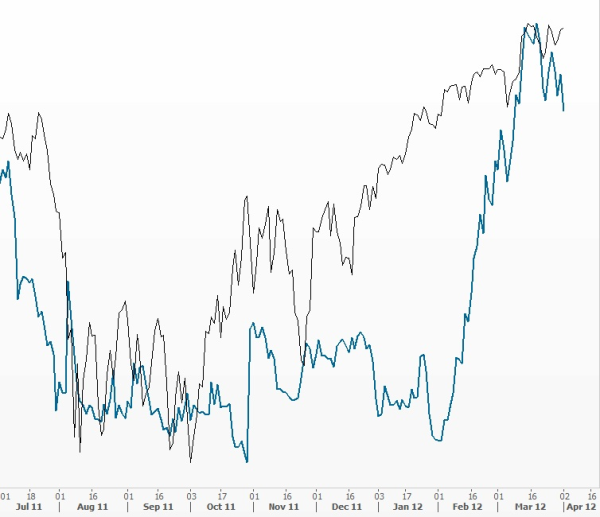

Interesting how tight this correlation has become lately. I have removed the labels to allow you to focus on the visual only at first look. Can you name these two price series?

If you said Dow Jones Industrial Average and Japanese yen, you nailed it! Below, DJIA is in black (right scale), the USD-Japanese yen in blue (left scale):

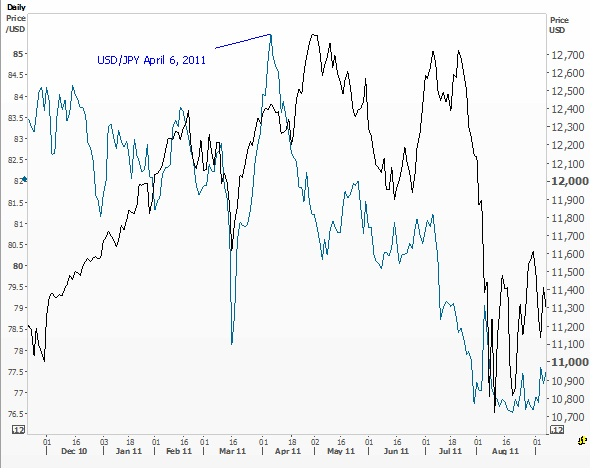

Now take a look at the same relationship, around the same time of year back in 2011. Back then, USD-JPY peaked in early April and led US stocks lower; eventually dragging the Dow down about 2000 points into September 2011 where it bottomed:

You may be asking: Well, what about 2010? Well, we saw a similar pattern back in 2010 also! USD/JPY topped in early May, the market topped in late April, both moved sharply lower together:

Just saying … stay tuned!

“I grieved to think how brief the dream of the human intellect had been. It had committed suicide. It had set itself steadfastly towards comfort and ease, a balanced society with security and permanency as its watchword, it had attained its hopesto come to this at last. Once, life and property must have reached almost absolute safety. The rich had been assured of his wealth and comfort, the toiler assured of his life and work. No doubt in that perfect world there had been no unemployed problem, no social question left unsolved. And a great quiet had followed. It is a law of nature we overlook, that intellectual versatility is the compensation for change, danger, and trouble. An animal perfectly in harmony with its environment is a perfect mechanism. Nature never appeals to intelligence until habit and instinct are useless. There is no intelligence where there is no change and no need of change. Only those animals partake of intelligence that have to meet a huge variety of needs and dangers.”

– H.G. Wells, The Time Machine (1895)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair