Personal Finance

25 years ago, on another Monday in late October, the financial world seemed to disintegrate in a heartbeat. Though the 205 point drop in the Dow last Friday (the technical anniversary of the ’87 Crash) was somewhat reminiscent of its 108-point drop on Friday, October 16, 1987, the real action in ’87 was on the Monday that followed. And while this Monday is not nearly as black, it is important that we use the opportunity to recall the circumstances that nearly sent the stock market into cardiac arrest.

While there were technical reasons that allowed the snowball to gather so much mass, it was major economic problems that started it rolling. Those issues remain to this day, but have grown much, much larger. But while they terrified the market 25 years ago, they don’t rate a second look today. Whether investors have gotten wise, or merely oblivious, is the question we should be asking.

Though most simply remember the 1987 Crash as one panicked selling day, Black Monday was just the largest drop in a string of bad days. On the Wednesday before, the Dow sold off 95 points (then a record) and dropped another 58 points on the Thursday. On Friday the selling got worse, with the Dow setting another record with a 108 point drop. After thinking about it over the weekend, investors decided to preserve what remained of their gains by selling on Monday. Unfortunately, everyone got the same idea at the same time.

It is true that the Crash was in some ways a technical phenomenon. As of August of 1987, stocks had surged 75% from January 1986, and 40% from January 1987. After such an upswing, it was inevitable that investors were on edge. Rather than taking profits, many on Wall Street instead hedged their positions using the new, and largely untested, trading programs that were designed to put a floor under losses if the markets turned south. But when the selling came in waves, the machines went into overdrive. Selling begat selling and an automated rout ensued. When the dust settled, the Dow was down 22% in a single day.

If that was all there was to the story, we would be left with a neat cautionary tale about the folly of placing too much faith in machines. But that is a distracting sideshow. In truth, the market was spooked by concerns over international trade and government debt, which then became known as the “twin deficits.” After widening earlier in the 80’s, investors had hoped that these gaps would come under control. But as Ronald Reagan’s second term wore on, those hopes faded.

From 1982 to 1986, the U.S. trade deficit had expanded 475%from $24 billion to $138 billion. Most economists blamed the trend on the dollar gains in the early 1980’s, which had apparently made U.S. products uncompetitive. As it was assumed that a weakened dollar would solve the problem, in 1985 the leading western democracies and Japan announced the Plaza Accords to systematically push down the dollar against the Japanese yen and the Deutsche mark. By 1987, the plan had “succeeded” devaluing the dollar 51% against the yen. But by the second half of that year it became apparent that the Plaza Accord had failed in its real mission to cut down on the U.S. trade deficit. Despite the plunging dollar, the deficit expanded that year by another 10% to $152 billion.

At around that time, the U.S. government budget deficits also became a major concern. Everyone remembers Ronald Reagan as a small government champion, but many conveniently forget that he presided over a significant expansion in government spending. Federal deficits rose 199% from 1980 ($74 billion) to 1986 ($221 billion). Although the deficit came down to $150 billion in 1987, many were frustrated that it remained stubbornly high by historic standards.

As early as August of 1987, concern over the twin deficits, which together accounted for 6.4% of the nation’s $4.76 trillion GDP became critical. Given the prior run up in stocks, this was enough to convince many investors to head towards the exits. Before Black Monday (October 19), the Dow had already declined 18% from its August peak.

When we look back at those events from the current perspective, it almost seems comical. Government deficits now approach $1.5 trillion annually and annual trade deficits exceed $500 billion. Today’s twin deficits now add up to more than 13% of current GDP (twice the level of 1987). But today’s investors are largely untroubled. Oftentimes news of a falling dollar and wider deficits will spark a stock rally, and the issues barely rate a mention in a presidential debate.

Are investors today simply more sophisticated than they were then? Have they lost an irrational fear of deficits? To the contrary, I believe that we have arrived at a point where money printing and government stimulus has replaced manufacturing and private sector productivity as the foundation of our economy (see my lead commentary in the October 2012 edition of theEuro Pacific Global Investor Newsletter for more on this). As a result, most investors are now blind to the dangers of deficits. But that does not mean that they don’t exist.

When America’s creditors wake up, particularly those foreign governments now shouldering the lion’s share of the burden, concerns over our twin deficits will return with a vengeance. As the problems now loom larger than ever, so too will the economic and market implications when the issues come to a head. Interest rates will surge and the dollar will fall. But the U.S. economy is not nearly as well equipped as in 1987 to withstand the stresses. Given the relative size of our imbalances, the manner in which they are being financed, and the diminished state of our manufacturing sector, higher interest rates and a weaker dollar will exact a much greater toll.

Despite this, I do not believe that the stock market is as vulnerable to another Black Monday. With the Federal Reserve so committed to its current course of quantitative easing, it seems to me unlikely that they will allow such a steep one-day drop. Also, with bond yields so low, domestic investors are currently presented with fewer attractive options. If anything, the next Black Monday is more likely to occur in the currency and/or bond markets, with safe haven flows moving into gold not treasuries.

Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital, best-selling author and host of syndicated Peter Schiff Show.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

And be sure to order a copy of Peter Schiff’s recently released NY Times Best Seller, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country.

Euro Pacific Capital, Inc.

10 Corbin Drive, Suite B

Darien, Ct. 06840

800-727-7922

www.europac.net

schiff@europac.net

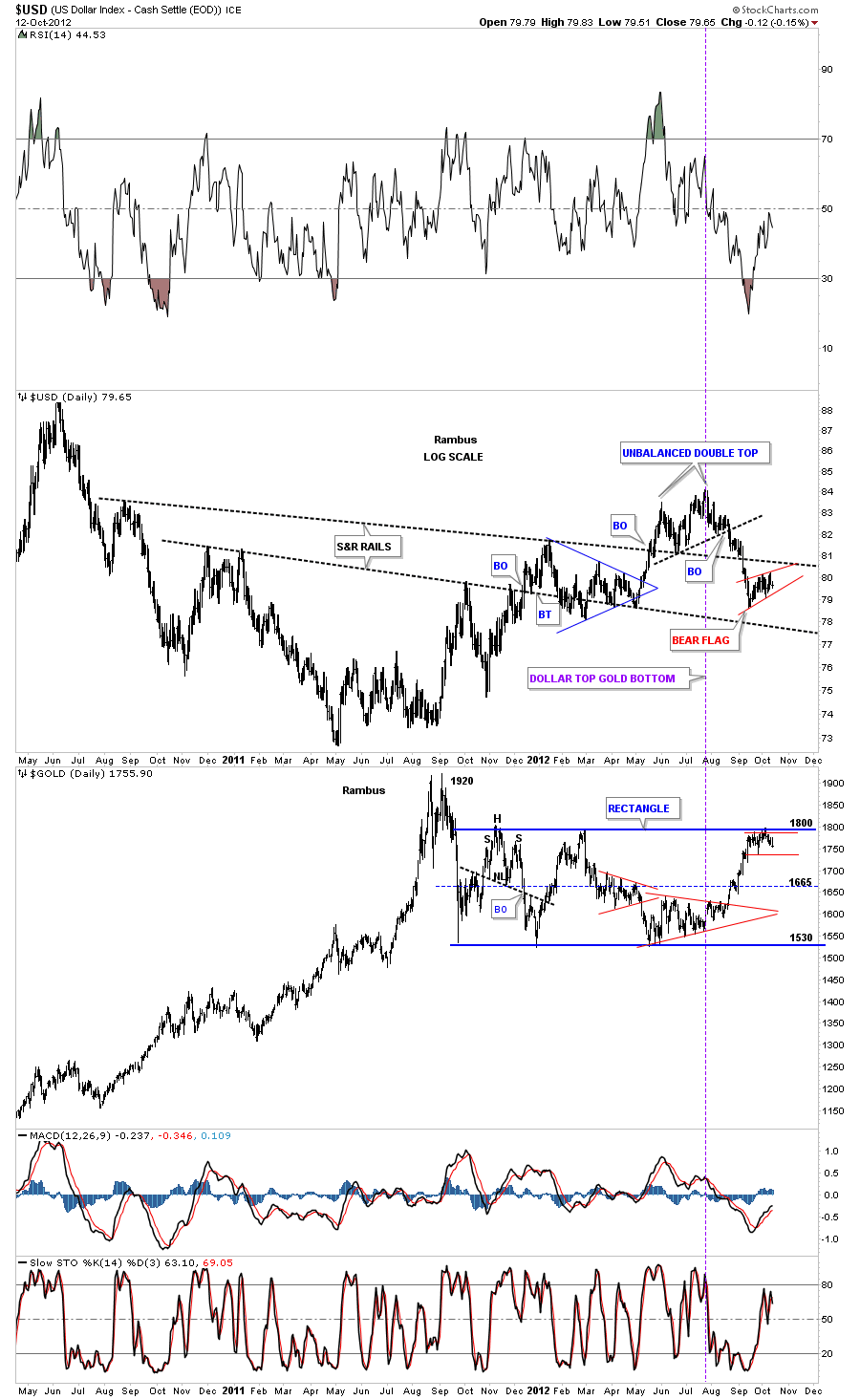

In this report I want to get everyone up to speed on the US Dollar and Gold. This week will mark the 6th week of consolodation time for the precious metals complex.

![]()

Strategy of the Week & 3 Stocks that meet that Strategy

I hope those of you near Vancouver or Calgary will join Michael Campbell, host of MoneyTalks, and I for an evening discussion of the market and how I approach it. For those who are not familiar with MoneyTalks, it is an excellent financial radio show that is broadcast in most markets in Canada. If it is not broadcast in your city it is available for free download from iTunes as a podcast.

Past MoneyTalks events have been sell outs and we expect this one to be no different, don’t wait too long to purchase tickets.

The following link has some great information on what the night will include:

Evening with Michael Campbell and Tyler Bollhorn, Calgary Oct 29 and Vancouver Oct 30

When do you buy an ugly market? I discuss in this week’s Market Minutes video. You can watch this week’s video on Youtube by clicking here. To receive email alerts any time I upload a new video, subscribe to the Stockscores channel at www.youtube.com/stockscoresdotcom.

Here is an excerpt from my upcoming book, The Mindless Investor, How to Make Money in the Market by Overcoming Your Common Sense. This piece is from the chapter, Trade Less:

Be Selective

It’s better to miss a good trade than to take a bad one. Missing a good trade doesn’t deplete your capital-it only fails to add to it. A bad trade will not only reduce the size of your trading account, it will eat up emotional capital and your confidence. A losing trade is not a bad trade, it is one that doesn’t meet your requirements. Bad trades come from working hard to see something that’s not there, guided by your need to trade rather than the market offering a good opportunity.

I have read very few books about the stock market, but one that I’ve read more than once and that I think is a must-read for every investor is Reminiscences of a Stock Operator by Edwin Lefevre. Here is a wonderful quote from that book that captures the essence of what this chapter is about:

What beat me was not having brains enough to stick to my own game-that is, to play the market only when I was satisfied that precedents favored my play. There is the plain fool, who does the wrong thing at all times everywhere, but there is also the Wall Street fool, who thinks he must trade all the time. No man can have adequate reasons for buying or selling stocks daily-or sufficient knowledge to make his play an intelligent play.

-Reminiscences of a Stock Operator

I advise all my students that they will make more money by trading less, at least so long as trading less is the result of having a high standard for what they trade. If you tell yourself you’re limited to only making 20 trades a year, you’re probably going to be very fussy about what trades you take. With less than two trades to be made each month, only the very best opportunities will pass your analysis. All of the “maybes” or “pretty goods” will get thrown out.

We take the pretty good trades because we’re afraid of missing out. It’s painful to watch a stock you considered buying but passed on go up. You remember this pain and the next time you see something that looks pretty good, you take it with little regard for the expected value of trading pretty good opportunities. Pretty good means the trade will make money some of the time and lose some of the time, and the average over a large number of trades may be close to breaking even. The fact that one pretty good trade did well is reasonable and expected. In the context of expected value, taking those pretty good trades many times will lead to less than stellar results when the losers offset the winners.

You shouldn’t judge your trading success one trade at a time. You must look at your results over a large number of trades. To maximize overall profitability requires you to have a high standard for what trades you make. Maintaining that standard will be easier if you take the trades that stand out as an ideal fit to your strategy, not by taking those that are marginal and require a lot of hard work to uncover.

![]()

The US is printing money and China’s economy appears to be stable and improving. Combined, these point to an improving commodity market which will benefit the Canadian stock market. With that idea in mind, I set out to find some Canadian dividend paying stocks with a good potential to move higher. I did so by filtering the market with the Stockscores Market Scan using the following filters:

Exchange = All Canadian

Yield > 4%

Pays Dividends

Sentiment Stockscore >= 60

Number of Trades > 500

This found 29 stocks, here are a few that have decent charts and good historic yields. I recommend verifying that dividends will continue at the same rate as what has been paid recently.

![]()

1. T.VSN

T.VSN has paid dividends to give it an historic yield of 7.59%. The stock has been slowly building optimism and looks like it can continue the long term upward trend that began in 2009.

2. T.ERF

T.ERF was punished by the market because of its emphasis on natural gas. Its historic yield is 6.49% and the stock has an improving chart as natural gas prices improve. Appears like it has more upside in the months ahead.

3. T.HSE

T.HSE has been paying out 4.39% but the stock has not done well over the past number of years. It is up for 2012 and starting to show some optimism. Has good potential to move to $30 where it will find some resistance.

If my evening with Michael Campbell is not broadcast in your city, it is available for free download from iTunes as a podcast.

In these evenings I plan to highlight some of the lessons from my new book, The Mindless Investor. This book is not yet available (it is being printed right now) and those who attend this event will be the first to receive one of the first 1000 copies of the book. Attendees will also receive:

– Attendance at the event

– Two months of my daily newsletter (value $118, new subscribers only)

– One month access to Stockscores.com (value $29, new subscribers only)

Some of the important lessons from my book:

– You must think like a trader to invest in the stock market today

– Diversification is a dangerous way to manage risk

– The stock market is not fair

– You can analyze any stock or market in 10 seconds (I will show you how)

Past MoneyTalks events have been sell outs and we expect this one to be no different, don’t wait too long to purchase tickets.

For more information, click on the appropriate link below:

Evening with Michael Campbell and Tyler Bollhorn, Calgary Oct 29 and Vancouver Oct 30

To get 20% off of the ticket price, use the special offer code SSTB2013 at checkout.

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

Singularity was originally a mathematical term for a point at which an equation has no solution. In physics, it was proven that a large enough collapsing star would eventually become a black hole so dense that its own gravity would cause a singularity in the fabric of spacetime, a point where many standard physics equations suddenly have no solution.

Beyond the “event horizon” of the black hole, the models no longer work. In general relativity, an event horizon is the boundary in spacetime beyond which events cannot affect an outside observer. In a black hole it is “the point of no return,” i.e., the point at which the gravitational pull becomes so great that nothing can escape.

Beyond the “event horizon” of the black hole, the models no longer work. In general relativity, an event horizon is the boundary in spacetime beyond which events cannot affect an outside observer. In a black hole it is “the point of no return,” i.e., the point at which the gravitational pull becomes so great that nothing can escape.

This theme is an old friend to readers of science fiction. Everyone knows that you can’t get too close to a black hole or you will get sucked in; but if you can get just close enough, you can use the powerful and deadly gravity to slingshot you across the vast reaches of spacetime.

One way that a black hole can (theoretically) be created is for a star to collapse in upon itself. The larger the mass of the star, the greater the gravity of the black hole and the more surrounding space-stuff that will get sucked down its gravity well. The center of our galaxy is thought to be a black hole with the mass of 4.3 million suns.

I think we can draw a rough parallel between a black hole and our current global economic situation. (For physicists this will be a very rough parallel indeed, but work with me, please.) An economic bubble of any type, but especially a debt bubble, can be thought of as an incipient black hole. When the bubble collapses in upon itself, it creates its own black hole with an event horizon beyond which all traditional economic modeling breaks down. Any economic theory that does not attempt to transcend the event horizon associated with excessive debt will be incapable of offering a viable solution to an economic crisis. Even worse, it is likely that any proposed solution will make the crisis more severe.

The Minsky Moment

Debt (leverage) can be a very good thing when used properly. For instance, if debt is used to purchase an income-producing asset, whether a new machine tool for a factory or a bridge to increase commerce, then debt can be net-productive.

Hyman Minsky, one of the greatest economists of the last century, saw debt in three forms: hedge, speculative, and Ponzi. Roughly speaking, to Minsky, hedge financing occurred when the profits from purchased assets were used to pay back the loan, speculative finance occurred when profits from the asset simply maintained the debt service and the loan had to be rolled over, and Ponzi finance required the selling of the asset at an ever higher price in order to make a profit.

Minsky maintained that if hedge financing dominated, then the economy might well be an equilibrium-seeking, well-contained system. On the other hand, the greater the weight of speculative and Ponzi finance, the greater the likelihood that the economy would be what he called a deviation-amplifying system. Thus, Minsky’s Financial Instability Hypothesis suggests that over periods of prolonged prosperity, capitalist economies tend to move from a financial structure dominated by (stable) hedge finance to a structure that increasingly emphasizes (unstable) speculative and Ponzi finance.

Minsky proposed theories linking financial market fragility, in the normal life cycle of an economy, with speculative investment bubbles endogenous to financial markets. He claimed that in prosperous times, when corporate cash flow rises beyond what is needed to pay off debt, a speculative euphoria develops; and soon thereafter debts exceed what borrowers can pay off from their incoming revenues, which in turn produces a financial crisis. As the climax of such a speculative borrowing bubble nears, banks and other lenders tighten credit availability, even to companies that can afford loans, and the economy then contracts.

“A fundamental characteristic of our economy,” Minsky wrote in 1974, “is that the financial system swings between robustness and fragility and these swings are an integral part of the process that generates business cycles.” (Wikipedia)

But a business-cycle recession is a fundamentally different thing than the end of a Debt Supercycle, such as much of Europe is tangling with, Japan will soon face, and the US can only avoid with concerted action in the first part of the next year.

A business-cycle recession can respond to monetary and fiscal policy in a more or less normal fashion; but if you are at the event horizon of a collapsing debt black hole, monetary and fiscal policy will no longer work the way they have in the past or in a manner that the models would predict.

There are two contradictory forces battling in a debt black hole: expanding debt and collapsing growth. Without treading again on ground covered in many past letters, let’s take it as a given that if you either cut government spending or raise taxes you are going to reduce GDP over the short run (academic studies suggest the short run is 4-5 quarters). To argue that raising taxes or cutting spending has no immediate effect on the economy flies in the face of mathematical reality. Note that I’m not arguing for one approach or the other, just simply stating that there will be consequences, either way. The country might be better off with higher taxes and/or more spending, or the opposite. But those choices are going to have consequences in both the short and long term.

Second, there is a limit to how much money a government can borrow. That limit clearly varies from country to country, but to suggest there is no limit puts you clearly in the camp of the delusional.

Regards,

John Mauldin

for Investors Insight

Editor’s Note:

Go HERE for more from John Mauldin. Specifically

The Event Horizon

The Glide Path

Speaking on Alternatives

I Was So Much Older Then, I’m Younger Than That Now

John Mauldin is the creative force behind the Millennium Wave investment theory. He is a New York Times bestselling author with a unique ability to present complex financial topics and make them understandable to the lay reader. One great example of this ability can be found in John’s “Yield Shark” investment service, which shows you how to protect and even boost your investment income…in any market. Click here to find out how.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair