Currency

Quotable

“Oft expectation fails, and most oft where most it promises; and oft it hits where hope is coldest; and despair most sits”

William Shakespeare

Commentary & Analysis

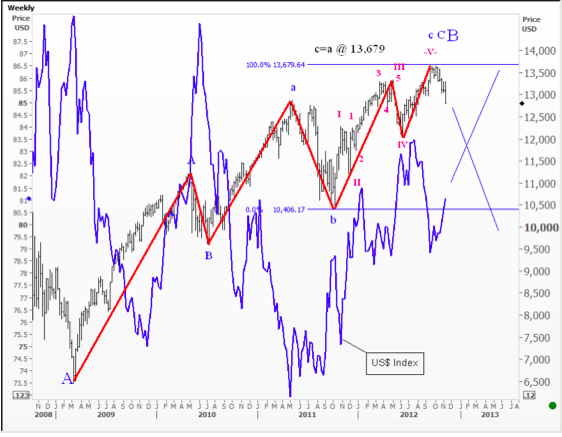

We Remain Long-term Bears on Stocks and Bulls on the Dollar

About six-weeks ago, our wave count suggested it was time to get short stocks. We shared the chart below with our Global Investor service Members at the time, suggesting they get short the Dow Jones Industrial Average. So far so good…

We noticed Marc Faber was at it again yesterday, suggesting US stocks should have fallen at least 50% now that the left’s hero is back in the White House.

From my partisan perch, I have seen what President Obama has done to us in four years, so was a bit surprised/shocked/stunned/angry/amazed (insert other words not appropriate for a family publication) he was rewarded with four more to completely finish the job of destroying the US economy. After some reflection yesterday (after I came in from the ledge), I thought about my wife’s grandfather, a real man and proud daily scotch drinker to boot; he used to say to me, “Jack, if the whole world is sane thank God I am crazy.” Now I get it.

On 24 September 2012 we said: Dow Jones Industrial Average Weekly: Symmetry and wave count suggest we may have seen a decent intermediate-term top here in the DJIA:

Same chart above, but fast forward to today:

We don’t believe it’s going too far out on a limb to suggest the US dollar gets a major risk bid should Farber’s view play out along with our chart analysis…

If our assessment about our President’s ability to further destroy real economic growth here is correct, it significantly increases the probability of another major global systemic event. Why? It’s because Europe and Asia need the US to grow, buying time for them to alter their economic models to the new reality of slower global demand. For Europe it is austerity and deflation in periphery country unit labor costs, and in China it is reduced reliance on exports and dangerously high levels of internal investment.

It’s interesting that both Europe and China were routing for President Obama, based on news reports, during the campaign. Well, you know the saying, “Be careful what you wish for it may come true.”

Jack Crooks

Black Swan www.blackswantrading.com

IMF Hypocrites Urge Permanent US Can Kicking, Fiscal Stimulus, and Enormous Deficits

One thing sure to raise my ire is a group of mindless hypocrites who say one thing and do another, while pretending they have a clue. In this case I am talking about the IMF.

One thing sure to raise my ire is a group of mindless hypocrites who say one thing and do another, while pretending they have a clue. In this case I am talking about the IMF.

As part of the Troika, the IMF helped ruin Greece. The country is now in a never ending depression with the youth jobless rate at 58 percent, and overall unemployment at 25.4%. Every step of the way the IMF demanded more austerity measures, as did the ECB, EU, and Germany.

And every step of the way Greece spiraled further and further behind. It’s not that austerity was unneeded, rather austerity could only really work in conjunction with a eurozone exit and work rule reform.

The IMF has lowered economic forecasts on Greece too many times to count. What was a €40 billion problem several years ago when I urged Greece to default is now a €240 billion problem.

Yes, the Troika threw €200 billion at a €40 billion problem. The reason is stubborn arrogance coupled with what amounts to religious fanaticism to save the euro project no matter who is destroyed in the process.

Eventually there is going to be a €240 billion haircut when Greece comes to its senses, tells the Troika to go to hell, and defaults on the entire mess.

IMF Hypocrites Urge Permanent US Can Kicking, Fiscal Stimulus, Enormous Deficits

……read much more HERE (including what the IMF urged the US to do).

As a result of a host of concerns (looming fiscal cliff, European debt crisis, slowing Chinese economy, geopolitical issues, etc.), the Dow has pulled back from its post-financial crisis high of one month ago. For some perspective, today’s chart illustrates the overall trend of the stock market (as measured by the Dow) since 2003. As today’s chart illustrates, the post-financial crisis rally was especially sharp during its first two years. Since then, the rally slowed but continued to trade above support (green line) — until now. The sharp selloff over the past two days has resulted in the Dow breaking below its 3.5-year, upward sloping support trendline.

Notes:

Where’s the Dow headed? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

<a href=”http://www.chartoftheday.com/”>Chart of the Day</a>

Quote of the Day

“Ride the horse in the direction it’s going.” – Werner Erhard

Stocks of the Day

Find out which stocks investors are focused on with the most active stocks today.

Which stocks are making big money? Find out with the biggest stock gainers today.

What are the largest companies? Find out with the largest companies by market cap.

Which stocks are the biggest dividend payers? Find out with the highest dividend paying stocks.

Author Peter Schiff has helped reassure me that I haven’t been taking crazy pills. President and chief global strategist of broker-dealer Euro Pacific Capital, Schiff is also the man who argued face-to-face with the Occupy Wall Street protestors in Manhattan’s Zuccotti Park, telling them — in part, at least — that they had a right to be angry.

Such perspectives help inform this wide-ranging and highly readable tome. For those who dismiss Schiff as an eccentric investor who “got lucky” with his now-famous prediction of the housing collapse, The Real Crash showcases a writer and analyst with a clear hold on sanity, who nonetheless has an unsettling message to convey.

“Whenever people credit me with calling the crash,” he declares at the outset, “it pains me to tell them that what they saw in 2008 and 2009 wasn’t the crash — that was a tremor before the earthquake. The real crash is still coming.”

Like many economists in the Austrian School — associated with thinkers like Ludwig von Mises and Nobel laureate F.A. Hayek — he author blames the housing bubble largely on the Federal Reserve. He acknowledges that government-sponsored agencies Fannie Mae and Freddie Mac and related interventions were contributing factors. But he thinks these alone can’t explain the size of the bubble.

…..click on the image or read more HERE

INSTITUTIONAL ADVISORS

THURSDAY, NOVEMBER 8, 2012

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The following is part of Pivotal Events that was

published for our subscribers November 2, 2012.

“MORE NEGATIVE SIGNALS”

SIGNS OF THE TIMES

“Chinese industrial company profits dropped 6.2 percent in August from a year ago, the largest decline this year and the fifth straight monthly deceleration.” – Bloomberg, October 22

“Bernanke: You can’t fire me – I’m going to quit in 2014” – Business Insider, October 23

Weird thinking – but, can that be made retroactive? To around now!

“It’s bad luck to kill wizards.” – Arnold Schwarzenegger, in Conan The Barbarian (1982)

“Rural Savings Threatened After Collapse” – Sydney Morning Herald, October 25

The article was about a non-bank lender that had been paying high interest on debentures and lending it out as mortgages or commercial property loans.

“Ford will shut three European plants, its first factory closings in the region in a decade.” – Bloomberg, October 25

* * * * *

CREDIT MARKETS

Ross noted in September that trends in money market stuff run “forever”. That’s the instruments with maturities of less than a year. Specifically, the Ted-Spread continues to narrow. At 0.581 as the mini-panic ended in late 2011, the spread-ratio has narrowed to 0.203 this week – clocking 19.4 on the Weekly RSI.

The chart begins in early 2008 and the previous most extreme was 23 in 2009. The trend change, and it is uncertain when it starts, will reflect a profound change in the main creditmarkets.

Within the Ted is the 3-month Libor and its Weekly RSI is down to 6.6. It was as low as 8 with the reversal in March 2008. The jump that began in that fateful September marked that disappearance of liquidity in the London Interbank Offered Rate. That was a shock to the current generation in the money markets, as well as in central banking.

Can this reverse?

Yes!

When?

????

What would be the mechanism?

The ability of governments to run increasingly reckless policy through their central banks has always depended upon the gullibility of the general public. Also prevalent has been the assumption of unlimited funding through confiscatory tax collections and unlimited abilities to issue credit/currency.

Obviously, taxpayer complacency is ending. Most taxpayers have had to tighten their belts and have been attempting to force thrift upon their extravagant governments. The more immediate effect has been upon local governments. State or provincial governments are one-step more remote, but will eventually be forced to be accountable.

In so many words, the “makers” have had it with the “takers”.

The paramount evil has been the federal level with not just the prerogative of issue, but increasingly evident lately, the ability to buy endless amounts of bonds out of the market.

Historically, practically and morally this has been absurd and will be overwhelmed by political and market forces.

The drive to today’s outbreak of bureaucratic despotism began around 1900 and where traditional means of US finance were limited by the constitution, the Federal Reserve System subverted this on the way to providing virtually unlimited finance.

As late as the mid-1960s the latter was considered impossible, but lately it has been widely accepted and widely discounted as “printing money”. The latest belief-surge maxed out on September 14th and a significant decline seems to have started.

This would mainly involve stocks and commodities and it is doubtful that even the most desperate of central bankers would be willing to add these to their buying mania. Stocksand commodities don’t have a maturity date.

Some may ask about the distress we expected “this fall” in most bond markets. In June-July the bond future soared up to a magnificent high that triggered our technical models. A significant price decline was possible. Maybe twenty points but the ten-point slump finished the move and stability is easing the overbought condition.

Similar strong overboughts were sequentially registered on corporates (LQD) and emerging debt (EMB). There are two ways of getting rid of an outstanding overbought condition. The one we prefer is the straight down; the other is a period of consolidation. The latter has prevailed and perhaps the continuous and big bid by central bankers is helping.

The long bond has been rallying with the setbacks in stocks and commodities. There is nothing new to this, and it could continue over the next number of weeks.

Treasury bill rates are at “Depression” lows but corporate bond yields are not at “Depression” highs. This “divergence” can’t last forever.

CURRENCIES

China’s announcement of massive stimulus prompted a review of their currency system, which used to have holes in each coin. Today’s coins no longer feature these, but their monetary theories are full of holes.

To be serious, the Dollar Index traded down to 79.1 on Wednesday, which level was support from early October. Today’s jump marks that as a successful test of the low and reaching 80.5 marks the break above 80.25 resistance.

Tuesday’s ChartWorks pointed out that with the break out the initial move could be to the 82 to 83 level. After consolidating the gain, the next target is around 90.

This could be considered as an involuntary trend towards “sound money”, that would be your basic central banker’s worst nightmare.

In time, this trend and widening popularity of “sound money” could fill the holes in Western monetary theories.

Link to November 3rd ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2012/11/this-week-in-money-56/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair