Timing & trends

U.S. Stock Market – I have constantly resisted the cries from bears to come back ever since leaving the bearish camp in March 2009. It’s been my opinion that the least resistance was up, not down and the surprises shall be to the upside.

It would come as no surprise that last Friday ends up marking an important low and in this seasonally favorable week of trading, the “Don’t Worry, Be Happy’ crowd ramp up their yearly “Santa Claus Rally” talk (It helps that Santa Claus will be in the White House for four more years).

No Bah-Humbug from me!

Gold – For the umpteen time, the bloodied perma-bears have tried to break the back of the “Mother” of all gold bull markets and failed. Look for $1.745 to be taken out on a closing basis and then yet another challenge of key resistance around $1,800.

Mining and Exploration Shares – I think last week was an important low up and down the food chain. While it won’t be straight up from here, I do think we can say good riddance (fingers, toes and all other body parts crossed) to the horrific bear market of 2012

The comments above by Peter Grandich @ Grandich.com

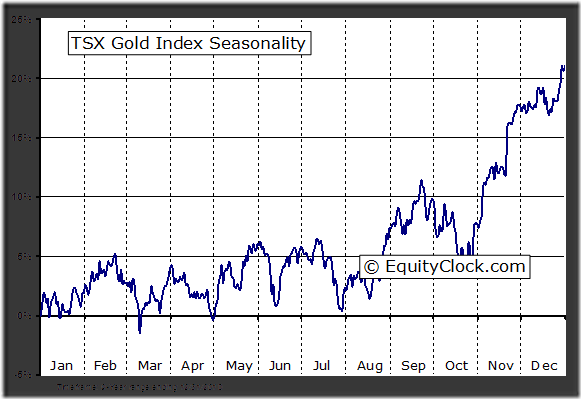

Ed Note: The following comments and the short term chartwork on mining shares is from Don Vialoux’s monday report:

The TSX Metals & Mining Index dropped 44.47 points (4.66%) last week. Intermediate trend is neutral following a break below support at 910.32. The Index fell below its 20 and 50 day moving averages. Short term momentum indicators are trending down. Strength relative to the S&P 500 Index remains positive despite the loss last week. Seasonal influences start to become positive at this time of year.

The AMEX Gold Bug Index dropped 40.36 points (8.84%) last week. Intermediate trend is down. The Index remains below its 20 and 50 day moving averages and fell below its 200 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming. Strength relative to gold bullion remains negative.

“I consider it so important that I want everyone to read the following adapted from the main article of my November Real Wealth Report, which published last Friday”. – Larry Edelson

It’s not kind to President Obama, but whether you agree with my views or not, it’s an important read …

The Sovereign-Debt Crisis Coming Our Country’s Way Will Be a Category 5 Financial Storm

And Obama’s Second Term is Entirely Consistent With it

Obama’s policies of class warfare and fat tax increases on the job-producers and risk-takers in our country will tear our society apart by the seams.

It will deepen the looming sovereign-debt crisis, and eventually destroy the U.S. dollar.

The next eight months – before the crisis fully hits our economy – will be your very last chance to get your financial house in order.

Fact is, I didn’t like either presidential candidate all that much. But Obama’s policy of instigating and escalating class warfare in our country, further dividing our society and blaming almost everything on the rich is just about the worst platform any leader can have.

Just consider the history of class struggles and you will see what I mean. They almost never solve any of those problems. Instead, they often lead to terrible consequences.

Nearly every one of the revolutions in our history was largely triggered by class warfare – blaming the rich, targeting them for higher taxes and, in many cases, literally chasing them out of their country.

And what happened as a result? In the majority of cases, the revolutions turned bloody, the existing government collapsed, the underlying economy was destroyed and society crumbled to its very core.

In some cases, class warfare led to genocide, civil war and even armed international conflict and world wars.

Class warfare almost always becomes the No. 1 enemy of economic growth. That’s especially true, according to the historical record, when a mature economy experiences class warfare.

Consider the U.S. economy right now. It’s lousy; the number of people in the labor force is the lowest it’s been in 31 years. We’ve had 43 months where unemployment has exceeded 8%.

You would think President Obama would want all the help he could get to boost employment. He would want those with money and credit to take risks to stimulate job growth, new industries, new technologies, entrepreneurship and more.

But instead, Obama has made class warfare his biggest priority. That’s why he’s even insanely claimed that those with money never would have made it “without government help.”

And why he has labeled small business and job-creators as “millionaires and billionaires” — targeting them instead for higher taxes.

It’s all allegedly in the name of “fairness” and supposedly aimed at closing the budget deficit.

Yet according to the Internal Revenue Service, the top 1% of U.S. taxpayers pay about 36% of all federal income taxes, while 47% of Americans don’t pay a single dime.

It’s why President Obama will stick to his guns on the upcoming fiscal cliff negotiations, keeping tax hikes in place for the wealthy at all costs, while conceding on other measures such as spending cuts.

Mind you, President Obama defines the “rich” — those he is targeting for higher taxes — as individuals earning $200,000 a year or more, and $250,000 a year for those married filing jointly.

That’s hardly “rich” by any measure. Not in today’s world of generally rising living costs and declining real incomes, net of inflation.

Is it any wonder that …

- President Obama, in his first term, signed more than 923 Executive Orders — almost 15 times more than former President George W. Bush signed during his two terms while fighting the war on terror?

- You now have to report every penny of financial assets you own overseas?

- If you owe taxes to the IRS, they can confiscate your passport, without a court order?

- The reporting requirement for sending money overseas has dropped from $10,000 to $3,000?

It’s hardly surprising to me. Many of the Executive Orders Obama has signed have been entirely consistent with his attacks on the rich all along …

Turning the “Patriot Act” into something it was never intended to be — a scheme to systematically deny American citizens, especially those with wealth, one liberty after another.

No, it’s not likely that Obama’s policies will lead to massive bloodshed in our country or to a world war, as many other cases of class warfare have done.

But targeting the “rich” simply isn’t going to cure our country’s problems.

President Obama could confiscate 100% of their estimated $6.4 trillion in wealth and it would hardly make a dent in the $222 trillion Washington owes us, its foreign creditors, Social Security, Medicare and more.

Quite to the contrary, it will aggravate our federal deficit and our national debt by systematically robbing our country of economic growth that’s largely propelled by entrepreneurs and risk-takers, by job-creators.

Again, just take a look at the history books. During the French Revolution, class warfare leader Maximilien Robespierre enforced confiscatory taxes on the rich with the guillotine. Those that could get out of the country, left as fast as they could.

In 1290, King Edward I issued an edict expelling all money-lenders (predominately the wealthy Jews) from England. And as we all know, Hitler went after them too.

During the Bolshevik Revolution, Vladimir Lenin declared class war against capitalists, confiscating their privately owned land, banks and businesses. It destroyed the productive capacity of Russia and set off a famine that killed an estimated 5 million Russians.

In 1929, Joseph Stalin pursued a class war as well, seizing the assets of Russia’s rich farmers, causing yet another famine where an estimated 7 million people subsequently starved to death.

Mao Tse-tung attacked China’s wealthy capitalists, promoting the Cultural Revolution which resulted in an estimated 45 million Chinese people starved or beaten to death between 1958 and 1962.

More recently, in Argentina, President Cristina Kirchner seized private pensions supposedly to help cover government budget deficits. Yet government spending subsequently soared 40% as Argentines fled the country, taking their cash and wealth with them.

In Europe, France is hollowing out its economy, raising taxes

on the wealthy (those earning more than $1.2 million to a 75% tax and for those earning over $186,000, a 45% tax) — and raising taxes on assets, inheritance and dividends.

Already, many big French names are leaving France. PPR, the luxury-goods group controlling Gucci and Yves Saint Laurent, is said to be relocating executives to London. Private-equity executives Bertrand Meunier and Christophe Florin have left for jobs in Switzerland and Abu Dhabi.

Entrepreneur Pierre Chappaz, founder of websites Kelkoo and Wikio Ebuzzing, has moved to Switzerland. Marc Simoncini, one of France’s most famous dot-com investors, is threatening to move to Belgium.

French magnate Bernard Arnault – Europe’s richest man, head of the LVMH fashion and Luxury Empire, and owner of iconic brands like Louis Vuitton, Moet and Chandon, Hublot and Bulgari – recently announced he had applied for Belgian citizenship in what may be an initial move toward acquiring tax-free status in Monaco.

Here in the U.S., wealthy Americans renouncing their U.S. citizenship is exploding higher, up sevenfold since 2008.

A record 1,781 U.S. citizens gave up their citizenship last year, compared to 231 in 2008.

I expect that trend to accelerate in the months and years ahead. Obama’s class warfare strategy virtually guarantees it.

Capital will flee the U.S. like never before. It will deepen the sovereign-debt crisis by reducing federal tax receipts, making it nearly impossible to shrink the federal deficit, not to mention our country’s $222 trillion of national debts and IOUs.

In the end, by the time the U.S. sovereign-debt crisis reaches full-tilt, it will also hollow out the U.S. dollar – making it virtually impossible for the greenback to remain the world’s single reserve currency.

I wish things were different. We all do. But I am afraid they are not, and I’m convinced that President Obama will soon come to regret a second term.

His policies virtually ensure that the sovereign-debt crisis will become a full Category 5 storm when it does hit the U.S., in the middle of next year.

How to Prepare … and Why 2013

Will be Your Very Last Chance to Do So!

Based on my timing models, I believe the U.S. will become fully infected with a sovereign-debt crisis around the middle of 2013.

That means that the eight months between now and the middle of next year represent your last window of opportunity to fully prepare for the mother of all financial storms.

The good news is that you have time. You also have the markets on your side, provided you understand the forces at work.

The majority of investors won’t see the storm coming. Even fewer will be prepared. Fewer still will understand how it will pan out.

My Real Wealth Report subscribers are in a unique position — well-ahead of the game, with a deep understanding of when, why and how the storm will hit … and what its consequences will be.

We’re in the first phase now. Europe is still going down the tubes.

There’s a worldwide contraction of credit happening right now that’s overpowering most markets and central bank money-printing. This first phase is largely disinflationary, precisely as I have been warning you.

And it will remain disinflationary, until the U.S. is fully engulfed by the sovereign-debt crisis around the middle of next year.

Between now and then, you can expect more downside action in commodities and stocks, setting up buying opportunities of a lifetime …

Don’t be fooled by the declines. Take advantage of them with speculative funds using bearish vehicles that profit from declining markets.

And then, when everyone else is panicking and selling, get ready to buy virtually everything under the sun. More money can be made in the markets over the next few years than in a lifetime of work, provided you know how the sovereign-debt crisis is going to unfold.

Best wishes,

Larry

P.S. Real Wealth Report is a no-brainer for any investor who wants a different, independent point of view. That alone is worth the cost of a membership, at just $89 a year.

Add in all my recommendations — in precious metals, in natural resource-based income stocks, in currencies, in Asian investment plays and more — and the $89 membership fee is an outrageous bargain! Click here to join now.

The Bottom Line

Most equity markets around the world and most sectors remain under significant technical pressure and signs of a bottom are tentative at best. Meanwhile, most equity markets and sectors are substantially oversold and set up for a strong recovery rally triggered partially by short covering. Favourable seasonal influences in selected sectors are apparent despite the decline by broadly based equity indices. Equity markets are setting up for a recovery rally on a Fiscal Cliff agreement that likely will last until at least Inauguration Day in the third week in January.

Other Factors

Volume in equity markets is expected to be significantly lower than average this week as the U.S. Thanksgiving holiday on Thursday approaches.

Historically, the strongest two consecutive days for stock market performance during the year are the day before U.S. Thanksgiving and a day after U.S. Thanksgiving. Average return per period for the S&P 500 Index during the past 61 years is 0.80%

Earnings reports and economic news this week are not expected to have a significant impact on equity markets.

Political focus is on the Fiscal Cliff. A meeting with the President and Congressional leaders on Friday concluded with encouraging comments about a possible agreement. However, no agreement will be reached this week. The President is in Asia and Congress is closed for the Thanksgiving holiday. The media’s count-down to the Fiscal Cliff is 43 days. However, with Congress on holidays today and on holidays in the last two weeks in December and with any agreement required to be scored by the OBC (Office of the Budget Committee), actual number of days available for negotiation is closer to 21 days.

Short term momentum indicators are deeply oversold and showed encouraging signs on Friday of bottoming.

Macro events outside of North America will impact North American equity markets. The escalating conflict between Israel and Gaza has grabbed the world’s attention. The Eurozone group of 17 nations is meeting today. The Euro summit of 27 nations will meet on Thursday and Friday.

The spending of large cash positions held by corporations on both sides of the border have started to move in a small way (e.g. Sherwin Williams purchasing a Mexican companies, several companies announcing fourth quarter ex dividend dates before the end of the year instead or early next year, share buy backs). However, most corporations are waiting for results of negotiations on the Fiscal Cliff before making major changes.

Long term seasonal influences on equity markets are positive from October 28th to May 5th.

Equity markets in the month of November have been strongest in the second half of the month.

Despite weakness in broadly based U.S. equity indices, favourable seasonal influences continue to show through (but in an unfavourable way). Sectors such as agriculture, forest products, transportation, industrials, home builders, semiconductors, China, Europe and the TSX Composite continue to outperform the S&P 500 on an intermediate basis (but by declining less than the S&P 500).

Key Indexes/Markets

The S&P 500 Index dropped 19.97 points (1.45%) last week. Intermediate trend is down. The Index remains below its 20 and 50 day moving averages and fell below its 200 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming.

The TSX Composite Index fell 319.08 points (2.62%) last week. Intermediate trend changed from neutral to down on a break below support at 12,137.18. The Index remains below its 20 and 50 day moving averages and fell below its 200 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming. Strength relative to the S&P 500 Index remains positive.

The U.S. Dollar gained another 0.23 (0.28%) last week. Intermediate trend is up. The Index remains above its 20, 50 and 200 day moving averages. Short term momentum indicators are overbought, but have yet to show signs of peaking.

Crude Oil added $1.01 per barrel (1.17%) last week. Intermediate trend is down. Support is forming at $84.05 per barrel. Crude oil moved above its 20 day moving average on Friday, but remains below its 50 and 200 day moving averages. Short term momentum indicators are recovering from oversold levels. Strength relative to the S&P 500 Index has turned positive.

Gold slipped $17.10 per ounce (0.99%) last week, triggered by continuing strength in the U.S. Dollar Index. Intermediate trend is neutral. Support is at $1,672.50 and resistance is forming at $1,739.40. Gold remains below its 50 day moving average and fell below its 20 day moving average on Friday. Short term momentum indicators are neutral. Strength relative to the S&P 500 Index remains positive.

Silver slipped $0.18 (0.55%) last week. Intermediate trend is neutral. Support is at $30.66 and resistance is forming at $32.93. Silver trades above its 20 and 200 day moving averages and below its 50 day moving average. Short term momentum indicators are trending up. Strength relative to gold has turned positive.

The AMEX Gold Bug Index dropped 40.36 points (8.84%) last week. Intermediate trend is down. The Index remains below its 20 and 50 day moving averages and fell below its 200 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming. Strength relative to gold bullion remains negative.

The TSX Metals & Mining Index dropped 44.47 points (4.66%) last week. Intermediate trend is neutral following a break below support at 910.32. The Index fell below its 20 and 50 day moving averages. Short term momentum indicators are trending down. Strength relative to the S&P 500 Index remains positive despite the loss last week. Seasonal influences start to become positive at this time of year.

…..many more charts & comments HERE on Don’s Great Monday Report

Do not let anyone tell you a savvy investor cannot make money in this market.

While it is true North American markets sold off significantly in the seven sessions directly following the U.S. election as investors again focus on the “fiscal cliff” — a series of tax hikes and spending cuts set to take effect at the start of 2013. It is our belief that the recession in Europe and slowing in China present more real challenges, but investors tend to be myopic these days and the cliff is staring them in the face.

Attention Money Talks Listeners – Exclusive Offer (Save $200-$600)

Or combine the services and save over $600!

So the Dow has fallen 5% as investors worry about higher dividend and capital gains taxes. And the TSX is off 3.9% since the election as worries about a sudden slowing of economic growth would be bad news for a resource heavy market like Toronto’s, since a lessening of demand for oil and metals would put pressure on mining and energy stocks.

But there are individual stock specific situations making us great money even with these concerns.

We are happy to report this Monday morning we awoke to excellent news from our Top Small-Cap Pick from March of this year. The Brick Ltd. (BRK:TSX), a stock we recommended in the $3.50 range just 8 short months ago, announced that they had entered into a definitive agreement to be purchased by Leon’s Furniture Limited (LNF:TSX) by way of plan of arrangement for $5.40 per share. The total consideration payable to The Brick shareholders and warrantholders is approximately $700 million.

Our return was approximately 55% in 8 months in a market (the TSX) that is down just under 3% on the year.

The lesson – the broader markets have been fairly valued for some time and are not the place to be. There is value out there and the smart money is uncovering it and we are recognizing tremendous gains in overlooked stocks. The key is to be very stock specific, patience, and very selective.

In the case of The Brick, the story was one of a significant restructuring and turnaround. At the time of our recommendation, the company was generating in the range of $100 million in cash flow with a strong balance sheet. From a valuation perspective, The Brick was trading at around 4 times cash flow a discount to its peers and appeared ready to introduce a dividend (catalyst), which it did, and appeared like a potential takeover candidate (ultimate catalyst).

The Brick is not the first company directly from our recommendation list that has been taken over and produced strong gains in our portfolios. In fact, it is just one of 7 companies from active BUY list in the past 18 months. Additionally, we have seen 7 more premium takeovers in 2012 from our 2012 Cash Rich, Profitable Small-Cap Stock Report – which we are updating with new stocks for 2013, slated for upcoming release.

While the ‘fiscal cliff’ is a worry, and the state of government and debt in Europe and North America are without doubt worrisome, this ‘fear’ has consistently created opportunities. We continue to selectively seek these types of companies and present them to our loyal client’s overtime.

Congratulation to all who purchased The Brick – this was a significant win in what has been a poor broader market in 2012.

KeyStone’s Latest Reports Section

11/14/2012

PLEASE NOTE: SIGNIFICANT PROJECT DELAY FOR JUNIOR COPPER PRODUCER PROMPTS DOWNGRADE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair