Timing & trends

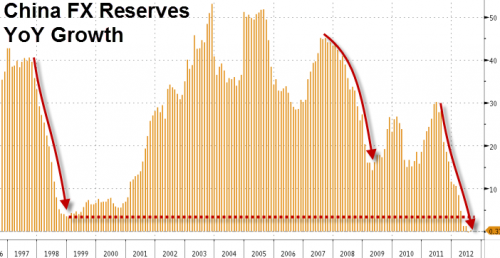

Hopes for an early recovery in the global economy may be overoptimistic, according to CLSA’s Russel Napier, as he notes the expansion of China’s reserves, which has been an engine of global economic growth, is about to come to a shuddering halt. As eFinancial News notes, Chinese reserves have decelerated dramatically over the last five years and are now close to zero. Napier said of the graph: “It is the most important chart in the world. The growth in Chinese reserves has determined all the key developments in financial markets in the last two decades. It printed lots of currency and artificially depressed the US yield curve. It has been the cornerstone of global growth, and now it’s over.”

Via eFinancial News:…

The last time the Chinese reserve growth rate was below 10% was at the end of the 1990s, just before the bursting of the technology stock market bubble and a recession. The recovery in the growth rate from 2001 onwards was followed by the economic boom of the last decade. The growth rate turned down decisively in 2007, just before the onset of the financial crisis.

China’s reserves have come from a trading surplus, and the Chinese authorities have used the money to buy US Treasury bonds. The finance that China supplied to the US helped fuel economic growth in that country and the rest of the world.

Ed Note: Perhaps that is why Marc Faber has this to say:

Investors should Buy themselves a machine gun in order to protect their assets

There will be Pain , very substantial Pain

“In the Western world, including Japan, the problem we have is one of too much debt and that debt now will have to be somewhere, somehow repaid or it will slow down economic growth,” stated Faber. “I think we lived beyond our means from 1980 to 2007, and now it’s payback period.” – in CNBC

“Credit is suspicion asleep”

SIGNS OF THE TIMES

“6,125 Proposed Regulations Posted in Last 90 Days – Average 68 Per Day”

– CNS News, November 8

Ironical, as the release came on the week when certain politicians were observing the deaths of so many soldiers – in the defense of freedom.

“Japan Plunges Into Deep Recession”

– Financial Times, November 12

“Bank of Canada warns that ‘vigilance by all parties’ is essential to contain the county’s household debt problem.”

– Financial Post, October 30

This seemed familiar so we checked our notes:

“The impact on the broader economy from sub-prime is likely to be contained.”

– Ben Bernanke, March 28, 2007

Using the typical timing on the end of boom, the yield curve was likely to reverse from inverted to steepening by as late as June 2007. The deadly reversal was completed by late in that fateful May.

* * * * *

CREDIT MARKETS

Representative sub-prime bonds soared to an outstanding high on September 14th. News that mortgage-backed securities were on the Fed’s shopping list was announced the day before. The chart shows the initial sell-off was followed by a trading range below the high. It broke down this week, suggesting no lack of supply for a foolhardy bid. At 57.4 now, taking out 56.6 would extend the downtrend. Taking out 55 would ring the alarm bells.

Contrary to official plans other bond sectors showed contempt for notions about “containment”.

US corporate high-yield (CYE) tested the late September high at 8.05 in late October and then plunged to 7.08. The low during the concerns of May was 6.86.

Junk (JNK) also tested its September high and has rolled over. The high was 40.53 and taking out 39.25 will set the downtrend. The low in May was 36.45.

Representing global markets, the Spanish Ten-Year reached 7.52% with concerns about default in July. Then the “risk-on” move dropped the yield to 5.34% in mid-October. The action has trended up and taking out 6.10% will start to get some attention.

As risk began to gain regard, the long bond has rallied from a key low of 144 and change on September 14th. Last week the high was 151.66 and the move is not overbought.

In shorter maturities, the Ted-Spread reached an exceptional degree of oversold at 0.203 on October 24th. It has set a brief and choppy uptrend to 0.240, which has been caused by the treasury bill rate plunging while Libor remained unchanged. It will become interesting when Libor starts to increase.

WRAP

This brief update will lead to a more extensive comment about government treasury departments issuing endless amounts of bonds as government central banks buy endless amounts of treasury issues. In case of the US it includes buying , shudder, the sub-prime.

Of course, outside investors have been playing the game, but overall it is institutionalized insanity. Where does the money come from to pay the interest? Well, it comes from issuance of yet more debt and it reminds of playing the popular game of Monopoly. Decades ago our family and friends decided to play the game with all of the money from another Monopoly set. It went on forever and there were no winners. Eventually, we quit and went back to only one set of money. Played by the rules it’s a good game.

Back in the 1970s as interest rates were soaring to unprecedented levels there were some articles about the costs of compounding interest. One concept was that within a speculative rise in price the compounding cost of interest eventually limits the ability of speculators to drive prices higher. This really took effect when surging prices faltered, which was the cue for Mister Margin to come onstage.

It makes sense that this would apply at any level of interest rates. Compounding doesn’t care what the rate is and even today’s low coupons must be paid.

Recently this seems to have been noticed by the UK government. The request for interest payments from the Bank of England is fascinating.

Halkin’s Weekly Letter includes a brief and amusing piece that starts with “Dear Mervyn”:

Link to November 17 ‘Bob and Phil Show’ where Bob makes some potent points on the Fiscal Cliff:

HYPERLINK “http://talkdigitalnetwork.com/2012/11/fiscal-cliff-with-a-creamy-filling/” http://talkdigitalnetwork.com/2012/11/fiscal-cliff-with-a-creamy-filling/

INSTITUTIONAL ADVISORS

THURSDAY, NOVEMBER 22, 2012

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The above is part of Pivotal Events that was

published for our subscribers November 18, 2012.

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL HYPERLINK “mailto:bhoye.institutionaladvisors@telus.net” bhoye.institutionaladvisors@telus.net

WEBSITE: HYPERLINK “http://www.institutionaladvisors.com” www.institutionaladvisors.com

PIVOTAL EVENTS – NOVEMBER 18, 2012 PAGE 2

PIVOTAL EVENTS – NOVEMBER 18, 2012 PAGE 1

“There’s never been a fiat currency in history that didn’t end in hyperinflation and complete collapse” says Asset manager Nick Barisheff . Barisheff thinks that Treasury Secretary Tim Geithner’s most recent call to have an “unlimited debt ceiling” for the U.S. was“just telling the truth.” That’s essentially what we have now with“open-ended” money printing by the Fed. Barisheff adds, “All it’s doing is postponing a problem . . . it makes it bigger and eventually it blows up.” Forget about remedies for the economy, it’s too late. Barisheff says, “We’ve passed the point of this getting fixed.” Barisheff thinks if the Fed’s gold holdings are ever audited, there will be a “gigantic short-covering rally . . . multiple bankruptcies . . . and a massive loss of confidence” in the dollar because much of the gold is gone or leased out. Barisheff thinks the gold price could be “easily double” right now. That’s because Barisheff believes, “What’s kept the price down is the artificial leased gold going onto the markets.” Join Greg Hunter as he goes One-on-One with Nick Barisheff, CEO of the $650 million Bullion Management Group.

Ed Note: Look at these staggering statistics that define the problem: The Joint Committee on Taxation found that raising the tax on millionaires to 30% federal (the so-called Buffet Rule) would raise a mere $5 billion a year.

Worse, if the Democrats passed all of their tax increase wish list – Congress’s Joint Committee on Taxation concluded the best case scenario (if no one changes their behaviour) – would raise $82 billion…..or just 7% of the current deficit!!!!

The two critical questions on this tour have been what about the Hong Kong-Dollar Peg and the Swiss-Euro Peg? The answer is simple. NEVER in history has there ever been any PEG or STANDARD that has ever survived. Why? Because “shit happens” meaning there is a business cycle that incorporates weather and climate changes as well as war.

Trying to hold even a gold standard cannot be accomplished because the economy is not a flat line. Attempts at creating a gold standard (fixing its value) have always collapsed as was the case with Bretton Woods in 1971. Napoleon’s gold standard failed. Britain tried to switch to a gold standard and was forced to leave several times. Its attempt to PEG the Pound to the Deutsche Mark collapsed in 1992.

WHY do all PEGS and STANDARDS simply collapse? Aside from trying to eliminate the business cycle, why communism also failed, it encourages speculation. PEGS are the greatest gift to traders in history – the illusive and fabled GUARANTEED TRADE. It is like going to the casino and you bet 100,000 on number 23 at roulette. If you win, you get your 35 to 1 return. If you lose, the house returns your 100,000. It is a no loss game.

Speculators can jump on the Hong Kong PEG as well as the Swiss PEG. When the timing is right, they will build up the position with no risk of loss. If they lose, the state held the peg and simply returns their bets; they win either way.

Some in the Goldbug Fanatic camp hate my guts because they paint me as some sort of traitor because I do not support their idea that returning to a gold standard will save the world. Their entire focus is money and nothing else. They refuse to consider history and ask the basic question if the gold standard is such a magic cure, why has it never lasted?

The Goldbugs confuse gold as a medium of exchange and an investment (as now), both having independent value (former by politicians latter by the free market), with the idea that only gold should be MONEY. They do not understand MONEY really can be anything because it is simply an economic language being the medium of exchange between two tangible objects. They are fixed on this idea that MONEY is of some standard value and thus becomes a savings. That was the entire basis of the Wizard of Oz – the political satire about maintaining a GOLD STANDARD that created austerity and depression. Sound familiar watching events in Greece? This same argument about fixing money has been going on for thousands of years. It has always collapse because there is such a thing as the Business Cycle that even Paul Volcker had to admit the Keynesian Economics completely failed to eliminate that in his Rediscovery of the Business Cycle.

The Goldbugs confuse gold as a medium of exchange and an investment (as now), both having independent value (former by politicians latter by the free market), with the idea that only gold should be MONEY. They do not understand MONEY really can be anything because it is simply an economic language being the medium of exchange between two tangible objects. They are fixed on this idea that MONEY is of some standard value and thus becomes a savings. That was the entire basis of the Wizard of Oz – the political satire about maintaining a GOLD STANDARD that created austerity and depression. Sound familiar watching events in Greece? This same argument about fixing money has been going on for thousands of years. It has always collapse because there is such a thing as the Business Cycle that even Paul Volcker had to admit the Keynesian Economics completely failed to eliminate that in his Rediscovery of the Business Cycle.

As soon as MONEY becomes a savings, you need a place to store it and you then create banks that lend the MONEY and you get leverage creating the VELOCITY of MONEY. Thus money is created by lending. Eliminate that to keep MONEY simply purely GOLD and then we are back to the Stone Age and you could only buy your house when you had cash since there would be no mortgages.

Why does MONEY have to have some fixed value when everything floats including your wages? Are you willing to work for a fixed sum for the rest of your life? Are you willing to sell the house for the same price you bought it at? Why invest if everything is a flat line and fixed? This debate has been going on for a long time but neither side listens to history.

The Fanatic Goldbugs further do not understand that to create a GOLD STANDARD is a derivative of Marxism – the idea of eliminating the fluctuations in the economy we call the Business Cycle. Just look at Southern Europe. Unemployment is off the charts. Social unrest is rising. The streets are often in flames. It is called austerity. This would be the same result introducing the GOLD STANDARD – the contraction of the money supply called DEFLATION. The Spanish youth have no future and a migrating to Brazil. Migration patterns such as this are common during economic crisis. A GOLD STANDARD would be more of the same.

The Fanatic Goldbugs’ superficial knowledge of monetary history serves only for slogans screamed from a tower with a loud speaker. Their logic is far from rational and amounts to basically if someone eats a carrot and died, gee, carrots must be dangerous. They childishly think money just has to be gold and all will be well. How does one create such a system without a Mad Max outcome? They have no idea.

This has been the debate even in the USA that has raged since the days of Andrew Jackson and the Bank War. Here is a picture of PUCK magazine from London showing America drowning in silver dollars which they valued more than Europe and led to massive gold migration from USA to Europe. That is why J.P. Morgan became famous lending the US Treasury gold in 1896 because politicians manipulated the gold-silver ratio and did not understand international capital flows. It has never been WHAT is money that is the core problem – but the complete lack of fiscal responsibility. Jefferson had it right – prohibit government from borrowing.

This has been the debate even in the USA that has raged since the days of Andrew Jackson and the Bank War. Here is a picture of PUCK magazine from London showing America drowning in silver dollars which they valued more than Europe and led to massive gold migration from USA to Europe. That is why J.P. Morgan became famous lending the US Treasury gold in 1896 because politicians manipulated the gold-silver ratio and did not understand international capital flows. It has never been WHAT is money that is the core problem – but the complete lack of fiscal responsibility. Jefferson had it right – prohibit government from borrowing.

Hamilton won the issue to create a national debt. Jefferson agreed on two terms. One it would be paid off, which it was. Secondly, the capital of the United States be moved next to Virginia becoming Washington, DC. Today, we have a national debt that is borrowing with no intention of paying it off. However, every pension fund is deeply invested in sovereign debt. It is the basis of reserve currencies for both local domestic banks as well as central banks. Going to a GOLD STANDARD would wipe out the world economy imposing major austerity

What do you do with the national debts? Do you now pay them off in gold? The bankers would love that and the treasury would be broke all over again. If we eliminate the level of debt, is new economic growth even possible? Just how can you pay down debt without creating money or restructuring the debt (devaluing it)? We only need to look at Greece to see what debt deflation creates. It is massively self-destructive to the brink of creating civil war.

On the other hand, not paying down debt but simply going bankrupt sets off a chain reaction where everyone’s pension funds vanish into the dark of the night. That too will lead to civil unrest and the Mad Max Effect – the total destruction of civilization. Perhaps it is just more practical to leave it alone and we simply inflate away. Society may hold together longer avoiding the civil unrest until they figure out they have less and less to show for their labor? But this lead government into authoritarian. They are already hunting down anyone with money. They create the Maximinus Effect – the hoarding of wealth and collapse of the economy as was the case with Rome.

So those proposing a simple return to the GOLD STANDARD cannot even begin to address these questions. This is not about what is MONEY, creating PEGS and STANDARDS that are simply derivatives of communism seeking to eliminate the business cycle. This is about trying to use history as a solution to save Western Civilization from the Debt Abyss not walking down the halls of Ivy.

This is the solution that will be presented at the Berlin Conference. This is the subject of the movie. This is not about me. This is about trying to come up with a solution reviewing history just for once to develop that solution. An alternative approach is the only answer. But it requires understanding the REAL role of the MEDIUM OF EXCHANGE since it has been everything from cowrie shells to paper.

How did Germany solve its hyperinflation? It replaced the Papiermark by the Rentenmark, which was an interim currency backed by the Deutsche Rentenbank, owning industrial and agricultural real estate assets – land. The French at one time also tried backing currency with land. Nonetheless, in 1924 the Rentenmark was replaced with the Reichsmark which was a permanent replacement. The Reichsmark was put on the gold standard at the rate previously used by the Goldmark, with the U.S. dollar worth 4.2RM. While the GOLD STANDARD was abandoned, during the Second World War, Germany established fixed exchange rates between the Reichsmark and the currencies of the occupied and allied countries, often set so as to give the Germans economic benefits.

These are just the real questions that have to be answered at the Berlin Conference(English: All-English / German All-German). Returning to a GOLD STANDARD because money should be REAL, is not practical, will lead to the Mad Max Effect, and accounts for nothing from history why all attempts to fix currency values have failed WITHOUT EXCEPTION since the legal code of Hammurabi who first attempted to fix the prices of everything in the first known STANDARDIZATION attempt in society of flat-lining the business cycle.

To the Goldbugs who demand a GOLD STANDARD so they can become rich, sorry. You are going to have to make money the old fashioned way – trade or work. This is not about saying gold is worthless. It is a object that retains value and is a recognized unit of value around the world. The only major commodity that is the same everywhere. It should remain as a hedge against government and should be a free market at all times.

The Buy-and-Hold Model for understanding stock investing is the dominant model of today.

The Buy-and-Hold Model for understanding stock investing is the dominant model of today.

It’s easy today to explain why Buy-and-Hold can never work. The root idea is preposterous (but not obviously so to those who have not yet seen through it — there are many smart and good people who possess a strong confidence in the concept). For Buy-and-Hold to work, valuations would have to have zero effect on long-term returns. Stocks would have to be the only asset class on the face of Planet Earth of which it could be said that the price paid for the asset has no effect on the value proposition provided. This cannot be. Price must matter. And if price matters, investors should not be going with the same stock allocation at times when valuations are insanely high as they do when stocks are fairly priced or low priced. Buy-and-Hold defies common sense.

Why, then, did so many experts come to believe?

The academics responsible for the Buy-and-Hold concept discovered something of critical importance in their studies of the historical data. They learned that short-term timing does not work. That is, those who predict where stock prices will be in a year or two are no more successful than what would be expected if their predictions were random rather than informed by intelligent study of the market. This was breakthrough stuff. This changed the history of stock investing. No longer was stock investing about bulls and bears making guesses as to when to buy or sell stocks. The science of investing showed that short-term forecasting does not work and that a long-term focus is needed. The science appeared at the time to suggest that a Buy-and-Hold strategy (sticking to the same stock allocation at all times) makes sense.

The science did not prove that Buy-and-Hold works. The Greatest Mistake in the History of Personal Finance took place when the academics jumped to the hasty conclusion that the fact that short-term timing does not work necessarily leads to a conclusion that Buy-and-Hold is the only rational strategy.

There is not one possible explanation for why short-term timing does not work. There are two. The explanation adopted by Fama and the other academics was that short-term timing does not work because the market always set prices properly and it is therefore impossible for even the smartest individual investor to do a better job than the market at determining the proper price for stocks. There is an alternate explanation that offers every bit as satisfactory an explanation. It could be that the market does such a poorjob of setting prices that there is no way for even the smartest investor to make sense of what the market is going to do. It could be that the reason why short-term timing does not work is not that the market is efficient but because it is wildly inefficient. It could be that stock prices do not reflect a rational collective assessment of the true value of stocks but an almost entirely emotional assessment that signifies just about nothing meaningful about the proper price of the stock market. Irrational markets cannot be timed because irrationality cannot be predicted.

There is a way to test which of the two explanations is the right one. If the market is efficient, the concept of overvaluation is silliness. An efficient market is a market that sets prices properly. But Shiller’s 1981 research (confirmed by a mountain of research done since then) shows that overvaluation is a meaningful concept. Shiller showed that stocks offer better long-term returns starting from times of fair or low prices than they do starting from times of insanely high prices. Even many Buy-and-Hold advocates acknowledge today that valuations matter. William Bernstein says that valuations affect long-term returns as a matter of “mathematical certitude.”

The further reality is that the market must in an ultimate sense be efficient. The purpose of a market is to set prices properly. If investor emotions were the sole influence on market prices, stock prices would go to the moon and stay there; what could ever persuade investors not to vote themselves raises by pushing stock prices higher and higher and higher yet? The market must ultimately be efficient, as the academics responsible for the Buy-and-Hold concept claimed. Yet the academic research of the past three decades shows conclusively that the market is not immediately efficient. What, then, is the full reality?

The full reality appears to be that the market is gradually efficient, not immediately efficient. It is investor emotions that determine market prices in the short term. But it is economic realities that determine stock prices in the long term (after the completion of 10 years of market gyrations or so). If the stock price rises too much higher than the price justified by the economic realities, opportunities open up for competing businesses to obtain the same assets on the cheap (relative to the market price assigned to them) and thereby to create a new business with the same profit potential as the overvalued one and thereby to pull the value assigned to it by the stock market down to reasonable levels. The market does indeed insure that stocks are priced properly. But it does not do this in an instant. The process can drag out for 10 years or even a bit longer.

….read The Dominant Model for Understanding How Stock Investing Works & Rational Investing Is The Answer (scroll down)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair