Personal Finance

In Vancouver and Toronto a Dramatic Sentiment Shift is Manifesting. Calgary shares a bearish view with Toronto and Vancouver voters that prices will be down 20% next year, but their vote tallies suggest prices may be flat or only 5% down.

The Canadian Real Estate Plunge-O-Meter…

…tracks the dollar and percentage losses from the peak and projects when prices might find support.

The Toronto view is for a definite price break but the depth of plunge is still debatable. In Vancouver, the bears rule. RESULTS HERE

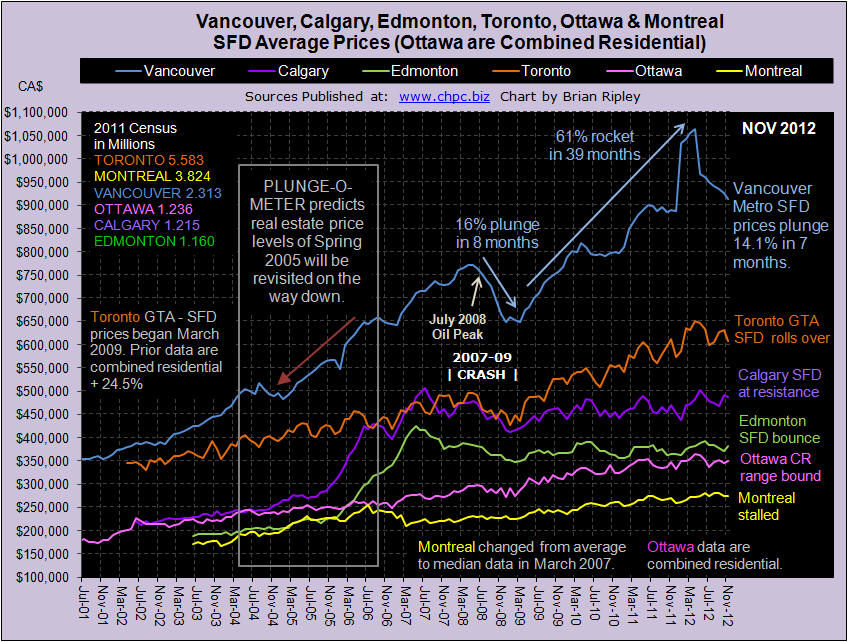

Vancouver average single family detached prices in November 2012 dropped again for a seven month plunge of 14.1% and a loss of $150,300 which is greater by 22% than the 2007-09 crash amount and the current plunge is an 85% retracement of the $177,329 gain since the beginning of the year (Vancouver Chart). At the “low end” strata prices slipped again and townhouses are 13.5% below their July 2011 peak and condos are down 9.9% below their April 2011 peak (Scorecard). Vancouver strata units are trading at 3Q & 4Q 2007 price levels and the Plunge-O-Meter predicts 2005 price levels will be seen again.

Earnings in BC held steady just 0.7% below their July 2012 peak, but remain 3.5% below Canada, 4.2% below Ontario and 19.8% below Alberta. BC earnings failed to follow Alberta’s big move up in early 2010 and has lagged average Canadian earnings since then by 3-5%.

…..for details on Calgary, Edmonton, Toronto, Ottawa, Montreal go HERE

The US is the place to be. That’s what everybody says. America has all the advantages: a stronger economy, a younger population, cheaper energy, and a central bank more ready to print money as necessary.

Look for US manufacturing to get a boost, especially in industries such as chemicals, from new energy discoveries. Households should benefit from lower energy prices too. And the dollar should go up as foreigners move their money to America in search of safety and higher returns.

Here’s Business Insider:

We are seeing calls that, thanks to shale drilling, the U.S. is poised to become the world leader in oil production, leading some to begin invoking “Saudi America.”

… Goldman Sachs analyst Kamakshya Trivedi, weighed in on the global macro implications of this phenomenon in a note titled: The shale revolution is changing the global energy landscape.

The note actually goes further, talking about how the entire economic landscape could potentially change.

The main impact, they write, is that oil prices will no longer prove a brake on growth:

…shifts in production are gradually loosening the oil price constraint that has been a persistent feature of the global economy. If global demand growth can recover, the risks that it will be choked off by rising oil prices are receding.

This will produce a knock-on effect for household incomes in the West, while blindsiding petro-states:

The drag on household incomes in the developed world from this source should end.

Meanwhile, central banks will be able to shift their focus from containing headline inflation:

Rising energy prices have affected core inflation measures to a degree, influencing the inflation outlook even for central banks, like the Federal Reserve, that have focused more on underlying inflation measures. As a result, lower ongoing energy inflation means that monetary policy may be easier on average than it otherwise would have been.

What? Fighting inflation? What central bank is worried about fighting inflation? They’ve got ZIRP and QE…they seem to be trying to cause inflation, not fight it. These guys aren’t firefighters, trying to put out the flames of inflation. No, they’re pyromaniacs. As Tony Boechk puts it:

The magnitude of reflation efforts is without precedent.

Meanwhile, here’s Philip Stephens, writing in the Financial Times:

It’s time to buy America.

America’s military reach will be unrivalled for decades. It has a stable political system. The country’s demographic profile is significantly better than that of any potential rivals. …The US has huge advantage in technological prowess and intellectual resources. …

How about that, dear reader? Is it time to buy America?

Maybe not. The real effect of cheaper energy in the US, will be to allow policymakers to make a bigger mess of things. They’ll shift more of America’s real wealth to the zombies. They’ll go deeper into debt. They’ll print more money.

The US got lucky. Its energy entrepreneurs found ways to squeeze oil and gas out of stone. Pretty nice trick. But sometimes good luck is the worst kind of luck. Atlanta would have been better off if the South had lost the war before Sherman approached…George A. Custer would have been better off if he’d gotten fired before taking his troops to the Little Big Horn…and the whole world would have been better off if Gavrilo Princip had not had the good luck to have a revolver in his hand when he accidentally ran into the Archduke Ferdinand.

Putting that aside, one thing we notice immediately: Mr. Stephens seems to have no idea how markets work. Reading his description of America’s pluses, it looks like a time to sell the country, not buy it.

He says the US is leading in several important ways. But so what? What America is today must already be reflected in the prices of her stocks, bonds and real estate. Today determines current prices; future prices are tomorrow’s business. If the US could surprise on the upside, it might be a good time to buy. If the surprise is more likely to come on the downside, it is better to sell.

It is like betting at a race track. The previous winner may hold his head high and prance around. He may be the favorite to win again. He may be at the very peak of his career. But that is not usually a good time to bet on him. Investors tend to over-value the recent past and forget the distant past. They like betting on yesterday’s winners. They run the odds up on the favorite until the payout for winning is small and the risk of loss is huge.

That is why the 10-year note yields so little – less that 1.6% last week. And that is why US stocks are so expensive – well above average on a P/E basis. Stocks and bonds have been in bull markets for the last 30 years. A whole generation of investors has grown up with no experience of anything else. As far as they know, stocks only go up. And on the rare occasions when they go down, the feds come in to push them back up again.

As for bonds, they’re a one-way bet too. Ben Bernanke has pledged to keep bond prices high for years into the future. If prices begin to fall (pushing up bond yields) he’ll come into the market to shore them up.

Of course, it’s been many years since we thought we could predict the future. A full head of hair and soothsaying both went away at about the same time. What we try to do now is to wait for things to get so far out of whack that even a Fed governor has to work hard not to notice. Then, we bet that they will get back into whack.

When? How? We don’t know. But right now, we see US debt at levels that look out of whack to us. The feds are running real, unfunded deficits equal to 21 times GDP increases.

Where this will lead, we don’t know. But probably not to higher prices for America’s stocks and bonds.

Bill Bonner for The Daily Reckoning

Bill Bonner Is the President & Founder of Agora Inc, an international publisher of financial and special interest books and newsletters.

Since founding Agora Inc. in 1979, Bill Bonner has found success and garnered camaraderie in numerous communities and industries. A man of many talents, his entrepreneurial savvy, unique writings, philanthropic undertakings, and preservationist activities have all been recognized and awarded by some of America’s most respected authorities. Along with Addison Wiggin, his friend and colleague, Bill has written two New York Times best-selling books, Financial Reckoning Day and Empire of Debt. Both works have been critically acclaimed internationally. With political journalist Lila Rajiva, he wrote his third New York Times best-selling book, Mobs, Messiahs and Markets, which offers concrete advice on how to avoid the public spectacle of modern finance. Since 1999, Bill has been a daily contributor and the driving force behind The Daily Reckoning. Dice Have No Memory: Big Bets & Bad Economics from Paris to the Pampas, the newest book from Bill Bonner, is the definitive compendium of Bill’s daily reckonings from more than a decade: 1999-2010.

Looking for direction – I’ll start this week’s blog by commenting on a few short-term charts…trying to make some sense out of the recent choppy price action…and then give you my brief cynical assessment of the Great Socialist Demand for anything that’s not nailed down…as they try to buy time…try to escape the inevitable consequences that come from the deleveraging of a broken consumption-driven, credit-drunk society in a post credit bubble collapse.

Charts:

The S+P had a Key Turn Date on Sept 14 and traded down until Nov 16 when a few (optimistic?) words from Boehner turned the market higher. I’ve thought that the rally from the Nov 16 lows was a correction to the downtrend that began at the Sept highs…but a break above 1425 – 1432 (perhaps on some more optimism about the fiscal cliff) would likely lead to a challenge of the Sept highs…at least. If the market advance stalls below 1425 and then drops back below 1383 my guess is that we’re probably headed for 1300 or lower by early 2013.

The bond market didn’t like today’s (Dec 7th) employment report…and a failure here…below the Nov highs…would look bearish…especially if we take out the recent lows around 14810.

Gold had a tough week last week…on Nov 28 it broke hard on record high volume…I thought taking out 1700 might lead to some downside momentum…but prices have held…a break below 1675 might ignite downside momentum.

The Euro rally from the Nov lows was astonishing in the face of the European news…but a dismal forecast from the ECB and a triple top on the charts turned the market lower this week…we are going into year-end…FX volumes get thin and weird things happen…as implausible as it seems, if this market rallies and takes out the triple top it could run higher…I’m inclined to think that the more likely course is that the Euro will fall and the USD will rise…but I try to remember to trade what the market is doing…rather than what I think it should be doing!

The CAD also rallied from the Nov lows (Boehner’s comments) so maybe it was just a case of a weak USD…CAD traded up on today’s Canadian UE report…but not much given how strong the report looked at first blush…so maybe the prospect of a weak US economy due to the fiscal cliff impasse is holding CAD back…or maybe the market is waiting on the imminent gov’t decision of foreign take-overs of Canadian energy companies…

Crude has been turned back by resistance around $89..a break below $85 sets up a challenge of the $80 level (seek weekly chart) and below $80 it’s a long way down to the next support levels…(weak global economies Demand less oil while North American Supplies grow?)

The Rising Tide of Socialist Demands on the “Rich” to pay for Entitlement Promises – it’s Class Warfare

Right after the Obama win I wrote that the “Rich” must now feel as though they have a target on their back…since then we’ve seen Obama declare that he has won a “mandate” to increase taxes on the “Rich.” I’ve maintained for the past few years that, “Way More Promises Have Been Made Than Will Ever Be Kept” and I believe that as the bills for the Entitlement Promises grow larger and larger that Socialists everywhere will grab for anything they can get from the “Rich” as they vainly try to deliver on those impossible promises…which will ultimately have to be broken. As my good friend Dennis Gartman wrote this week, “The President is, if nothing else, a very cool, and some might say a very cold…calculating political animal and he knows all too well the familiar political refrain that he who robs Peter to pay Paul has the everlasting support of Paul….President Obama (is) a champion of class warfare…Paul is delighted at Peter’s impending tax problems…Paul is delighted that someone else shall be forced to pay for (his) entitlement programs…Paul, sadly to say, is more than willing to have Peter fleeced. The President knows this; the President believes this and the President, as a leftist, is ready, quite willing and very able to press ahead.”

Of course, as Margaret Thatcher famously declared, “The problem with socialism is that you eventually run out of other people’s money.” So soak the “Rich” all you want…and then what will you do?

We are living in The Age of Deleveraging (thank you Gary Shilling) and the over-indulgences of the credit boom era will be painfully restructured…which means that some debts will not be fairly repaid…some promises will not be kept….specifically some pension promises. Central bankers and governments around the world hope to “kick-start” economic growth with easy money and stimulative programs (except where selective “austerity” is prescribed) but isn’t it obvious that going deeper into debt to pay off previous debts isn’t working? Isn’t it obvious that write-offs or bankruptcies are inevitable?

The times they are a-changing…big-time…and change brings great trading opportunities…keep your eyes open…and your powder dry.

Victor

Most equity markets in the world and major sectors are recovering from oversold lows set on November 16th. Sectors with favourable seasonality are responding, but currently are overbought. Preferred strategy is to accumulate favoured sectors on weakness for a recovery rally that is likely to last at least until Inauguration Day.

Equity Trends

The TSX Composite Index slipped 79.59 points (0.65%) last week. Intermediate trend is down. Support is at 11,761.34. The Index remains above its 20 and 200 day moving averages and below its 50 day moving average. Short term momentum indicators are trending up. Stochastics already are over bought, but have yet to show significant signs of peaking. Strength relative to the S&P 500 Index remains negative.

The S&P 500 Index added 1.89 points (0.13%) last week. Intermediate trend is down. Support is at 1,343.35. The Index remains above its 20 and 200 day moving averages and moved above its 50 day moving average on Friday. Short term momentum indicators are trending up. Stochastics already are overbought, but have yet to show significant signs of peaking.

The Dow Jones Industrial Average gained 129.55 points (0.99%) last week. Intermediate trend is down. Support is at 12,471.49. The Average remains above its 20 and 200 day moving averages and below its 50 day moving average. Strength relative to the S&P 500 Index has changed from negative to at least neutral.

Sectors with positive seasonality at this time of year continue to outperform the S&P 500 Index including Agriculture, forest products, industrials, technology, semiconductors, biotech, Europe, base metals, silver, platinum, lumber and copper.

Silver gained $0.88 per ounce (2.73%) last week. Intermediate trend is neutral. Support is at $30.66 and resistance is forming at $34.49. Silver remains above its 200 day moving average and below its 20 day moving average, but moved above its 50 day moving average on Friday. Short term momentum indicators are trending down. Strength relative to gold remains positive.

Platinum added $0.40 per ounce (0.02%) last week. Intermediate trend is up. The Index remains above its 20 and 200 day moving averages and below its 50 day moving average. Strength relative to gold remains positive.

Copper added $0.01 per lb. (0.27%) last week. Intermediate trend is up. Support is at $3.403. Copper remains above its 20, 50 and 200 day moving averages. Short term momentum indicators are overbought, but have yet to show signs of peaking. Strength relative to the S&P 500 Index remains positive.

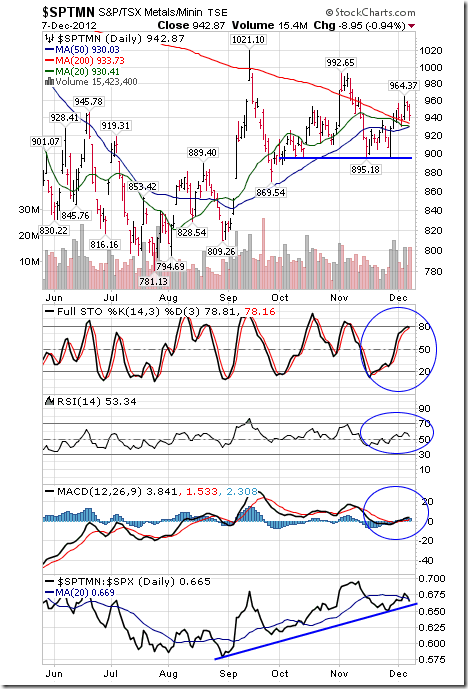

The TSX Metals & Mining Index slipped 1.95 points (0.21%) last week mainly on weakness in Freeport McMoran Copper & Gold following acquisitions of non-mining operations. Intermediate trend is neutral. Support is at 895.18 and resistance is at 1021.10. Short term momentum indicators are trending up. Stochastics already are overbought, but have yet to show signs of rolling over. Strength relative to the S&P 500 Index remains positive.

Other Issues

The VIX Index added 0.03 (0.02%) last week. It continues to hold above long term support near 14%.

Earnings news this week is not expected to have a significant impact on equity markets.

Short term momentum indicators for most equity markets and sectors are overbought, but have yet to show signs of rolling over.

Generally, U.S. economic news this week is expected to have a positive impact on equity markets. Positive events include the FOMC meeting release, retail sales, PPI, CPI, Industrial Production and Capacity Utilization. Greatest focus is on the FOMC meeting when information about extension of Operation Twist is expected to be released.

News outside of North America can have an impact on equity markets. Events in Syria have escalated to a level where news on a possible attack using biological weapons could shift focus. In Europe, Eurozone finance ministers meet on Wednesday ahead of the European Summit in Brussels this Thursday and Friday. Several economic data points were released by China last night, more are scheduled today and the next HSBC Flash PMI report is released on Friday. India’s Industrial Production report on Wednesday could provide a pleasant surprise.

On average, North American stock market performance in the second week in December has been neutral to slightly negative. The strongest period is the second half of the month when the Santa Claus rally usually occurs (particularly during U.S. Presidential election years). The rally normally continues until the first week in January.

…..much more (46 charts and analysis) HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair