Gold & Precious Metals

One way to rise above the day-to-day noise in markets and get the longer view right is to adopt an investment sage, somebody older, wiser and considerably richer due to their past good judgement. Many in the gold market turn to Jim Sinclair, adviser to the Hunt Brothers in the 70s and a veteran market trader of considerable net worth.

One way to rise above the day-to-day noise in markets and get the longer view right is to adopt an investment sage, somebody older, wiser and considerably richer due to their past good judgement. Many in the gold market turn to Jim Sinclair, adviser to the Hunt Brothers in the 70s and a veteran market trader of considerable net worth.

Now in his eight decade Mr. Sinclair publishes a website with a mission to explain what he knows to be the truth about the gold market. Sometimes it is difficult for the uninitiated to understand the language of traders but he tries to make the message as clear as possible. Here’s what he is saying now…

……read it all HERE

Another Jim Sinclair interview:

Jim Sinclair – Paper Markets To Disappear As Gold War Rages

Today legendary trader Jim Sinclair predicted the paper markets would disappear as the gold war intensifies. Sinclair also spoke with King World News about the “end game,” how various countries are positioning themselves, and how this will impact the gold market. Below is what Sinclair, who has been actively trading the markets for over half a century and whose father was business partners with legendary trader Jesse Livermore, had to say about what is now taking place as the gold war continues to rage.

…..full interview HERE

As bad as it has been for me in the junior resource market the last year or two, being on the right side (or at least avoiding being on the wrong side) of the U.S. stock market for almost my entire 30 year career in and around Wall Street has been a good thing.

From several thousand DJIA points lower, I spoke about a new, all-time high to come. Knowing you’re only as good as your last call (and some on Wall Street have milked that for years), where do we go from here?

The chart above was from an excellent article from Safehaven.com that I used in my January 3, 2013 edition. It fits well into my long-standing belief that this rally would not only take us to a new high, but after running some after that, would then crater into the worse bear market of the modern era. I don’t know the exact number or date but I do believe the best strategy is to begin a scale-up sell program and what monies need to be in general equities be allocated to areas of the world more likely to prosper versus the U.S.

I continue to find equity portfolios in North America seriously overloaded with public companies that derived the majority of their business in North America. Like it or not, the United States is no longer the economic engine that pulls the world’s economy anymore.

Investors should tap market segments most geared to faster global growth and less exposed to US consumption. This belief suggests lowering exposure to small and mid-caps and favoring large and mega-cap companies, which benefit the most when global growth accelerates and are the least sensitive to a slower domestic economy.

To benefit from global growth even more directly, investors can reduce their overall US allocation. For most of the past three years, the US has been a safe port in the storm. Part of the reason is an incredibly resilient corporate sector, which until recently has effectively delivered double-digit earnings from low single-digit economic growth. But US competitiveness was not the only factor. On a relative basis, the US has been the unintended beneficiary of an unexpected slowdown in emerging markets, Europe’s fiscal crisis, and an over aggressive out of control Federal Reserve.

Today, while US companies are still reasonably priced, they are relatively expensive compared with the rest of the world (the S&P 500 trades at a 40 per cent premium to international markets based on price-to-book). Given the near-term outlook for slower growth, more volatility, and a debt-ceiling showdown, that premium may no longer be justified. At the same time, the rest of the world is in marginally better shape. Given the shift in relative fundamentals, investors should consider reallocating much of their holdings out of the US and into emerging markets, smaller developed markets and European exporters.

For example, many smaller developed markets – Australia, Singapore, Hong Kong, Switzerland, and Canada – came out of the financial crisis much better positioned than the larger, developed countries. Generally, their labor markets were less impacted and their fiscal situation looks credible and, in some cases, quite good. While these nations have their own challenges, valuations are generally more forgiving and growth estimates may be less prone to disappointment. At the minimum, they appear to be the lesser of two evils.

The 21st century economic engine is now China. It has surpassed the U.S. to become the world’s biggest trading nation last year as measured by the sum of exports and imports of goods. China’s growing influence in global commerce threatens to disrupt regional trading blocs as it becomes the most important commercial partner for some countries. Germany may export twice as much to China by the end of the decade as it does to France

For so many countries around the world, China is becoming rapidly the most important bilateral trade partner by the end of the decade many European countries will be doing more individual trade with China than with bilateral partners in Europe.

Missed China boom? India is the next china.

From 1990 to 2010, growth in both countries’ labor forces was comfortably above 200 million people. Over the next 20 years, India is forecast to add another 200 million to its workforce. China just 3 mil. China’s labor force will turn negative in 2016 or 2017. These aren’t guesses. These people are already alive. It will create huge wage pressures. After years of intense investment, China will have enormous installed capacity but a shortage of labor. India will have a shortage of installed capacity and excess labor.

So where will we see the next construction boom? India. China will supply the cement, steel and capital to India as it has tried to do to Africa. But only India has the size and potential scale to absorb it. India needs hundreds of billions to be spent on infrastructure and China can supply much of the materials needed.

India, moreover, is still urbanizing. Brazil and China are a long way down the urbanization path. In India, 70 per cent of the population is stull rural.

The risk in this?

The problem is that India does not have the regulatory framework to permit large scale infrastructure projects. It needs a central agency to provide the “comfort and guarantees” to make investment possible. How likely is that? India embarked on reform in the 1990s but the process has been stalled for years. As the need to resume it has become more urgent, the government has only become more ineffective. On present form, India faces a descent into social unrest before its politicians rediscover a sense of urgency. I believe it will eventually enact reform, after time.

Bottomline – It’s not if the United States implodes, but when. Bernanke’s Ponzi finance is self-sabotaging. Endless cheap money upsets the balance between credit expansion and real economic growth, resulting in diminishing returns. Each additional dollar of credit seems to create less and less results. In the 1980s, it took four dollars of new credit to generate $1 of real GDP. Over the last decade, it has taken $10, and since 2006, $20 to produce the same result. With debt now heading over 100% of GDP, history shows any and all economies that go into triple digits are hindered. The U.S. shall be no exception.

Unlike so many who remained bearish on U.S. equity market from the lows in 2009, I not only didn’t stand in its way and get run over, but a new, all-time high I spoke of has arrived.

Seeing them high-fiving again on Tout-TV and much of the media (that makes their monies following the pied pipers of the “Don’t Worry, Be Happy” camp that fills the boardrooms and sales floors of the financial industry at-large) writing about “Happy Days Are Here Again”, the ingredients of that ultimate top are now brewing. Exactly when it all comes together I don’t know but as it has been for almost my entire 30-year career in and around the financial arena, you can feel it in your bones (the only difference now is there’s a lot more fat around those bones).

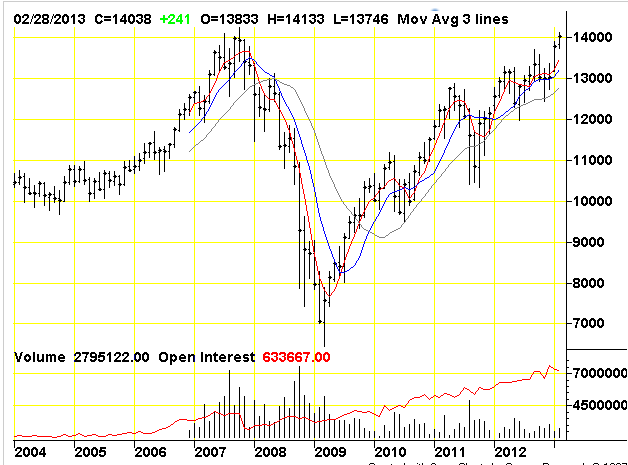

Five and a half years ago, the Dow Jones Industrial Average set an all-time record high of 14,165 points before sliding into the second-worst bear market in its history. Yesterday, the Dow broke its record, nearly four years to the day from the start of its rebound. Memories of that long fall still linger, staining the perception of those who endured it and tempering the optimism of all but the most fervent bull. Doomsayers are to be expected this far into a sustained rally — which, at more than 1,000 trading days with no real correction, has now run well ahead of both the median and average length of all bull markets since the Dow’s creation. But does this market really deserve the distrust, fear, and outright anger many investors have shown toward it as it continues to defy calls for another crash?

Five and a half years ago, the Dow Jones Industrial Average set an all-time record high of 14,165 points before sliding into the second-worst bear market in its history. Yesterday, the Dow broke its record, nearly four years to the day from the start of its rebound. Memories of that long fall still linger, staining the perception of those who endured it and tempering the optimism of all but the most fervent bull. Doomsayers are to be expected this far into a sustained rally — which, at more than 1,000 trading days with no real correction, has now run well ahead of both the median and average length of all bull markets since the Dow’s creation. But does this market really deserve the distrust, fear, and outright anger many investors have shown toward it as it continues to defy calls for another crash?

It’s important to have a little perspective.

…..read it all HERE

Dow up 125 points yesterday, to a new all-time record.

Why? What’s behind it? The economy is not so hot. Why the red-hot stock market?

China is back in the news. A new report from CBS’s “60 Minutes” documents the extent of the ghost cities in China — miles and miles of empty highway, office towers, apartments and malls. Analysts are talking about the biggest real estate bubble in history!

Is China a bubble? We don’t know.

Does it matter? Well… yes… maybe. If China melts down or blows up the demand for oil and other resources goes down. The Chinese have pumped vast sums of money into development projects. That money helped to keep people on the job… and also kept the ships full of stuff, going back and forth across the world’s oceans.

Trouble in China is trouble everywhere — particularly in Australia (which has been selling itself by the ton to the Chinese) and in Europe (which sells its precious, high-touch products by the boatload). Drive around Beijing and you see German autos, Italian shoes, Swiss watches and French perfumes.

But why worry? The Chinese can print money too! When China does something, it tends to do it to excess. That’s why there are so many empty buildings in the Middle Kingdom and why it might have created the biggest real estate bubble in history.

China overdoes it when it comes to central bank stimulus measures too. Arguably, no central bank has done more than the People’s Bank of China when it comes to pumping up the economy.

M2 money supply in China is roughly twice GDP. In developed economies the ratio between M2 and GDP is usually below one. In emerging market countries, M2 is usually 1 to 1.5 times GPD.

That’s why bad news for China… like bad news for the U.S. economy… could be good news for the stocks. The Chinese feds will pump more money. Stocks will go up!

The New York Times reports:

The Dow Jones industrial average, which measures the performance of 30 blue-chip companies, closed with a gain of more than 125 points Tuesday, surpassing its previous record close of 14,164.53, which it achieved nearly five and a half years ago, as well as its record intraday high, set around the same time, of 14,198.10.

Of course, a few things have happened since October 2007. The housing market collapsed, the financial system went into meltdown, the European Union started to fray and politicians dragged the United States through an on-off-on-again fiscal imbroglio.

But stocks managed to move beyond all that.

Since a low point in March 2009, the Dow Jones index has more than doubled, stunning even the most seasoned stock market watchers. It closed at 14,253.77 Tuesday.

“What’s amazing about this bull market is that people still don’t think it’s real,” said Richard Bernstein, chief executive of Richard Bernstein Advisors, a money management firm. “We think this could be the biggest bull market of our careers.”

The Aristotelian Error

Yeah — you can count us among those who don’t think it’s real. We think it’s what happens when all the world’s central banks are evaporating yields on bonds and corralling investors into stocks.

If China goes into a serious correction, how will its leaders overreact? With even more funny money and EZ credit?

We don’t know enough about the Chinese situation to make an educated guess. So we’ll make an uneducated one. Whether they live in Beijing or Washington, economists tend to have the same dumb ideas.

They are heirs to the Aristotelian error: the belief that without them the whole world will fall to pieces. They believe they must set the price of the economy’s most essential ingredient: credit. And if the economy fails to do their bidding, they will give it more money too.

All major central banks are in agreement about this. All believe they can see, in their mind’s eye today, a picture of the world as it will be tomorrow. And they further believe that they can Photoshop it to make it better.

They improve the future by making credit cheaper or dearer, as the occasion requires.

But how is it possible, you might wonder, that these few homo sapiens can do something so remarkable?

How do they know precisely how much new money to create and how to price it? What kind of bread do they eat? What kind of liquor do they drink? Surely, they do not eat and drink the same things we do; for they must sup at the gods’ table to be able to do such things.

In their naïve and simpleminded way, the planners believe that a slack economy calls for overtime work at the central bank. That which the private sector taketh away, they say, is what we will put back — and more!

So stocks go up. That’s our best explanation.

Regards,

![]()

Bill

Bill Bonner started Diary of a Rogue Economist to share his over 30 years of economics and market experience with as many interested readers as possible.

Diary of a Rogue Economist is always free, and it’s delivered to your email each business day.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair