Gold & Precious Metals

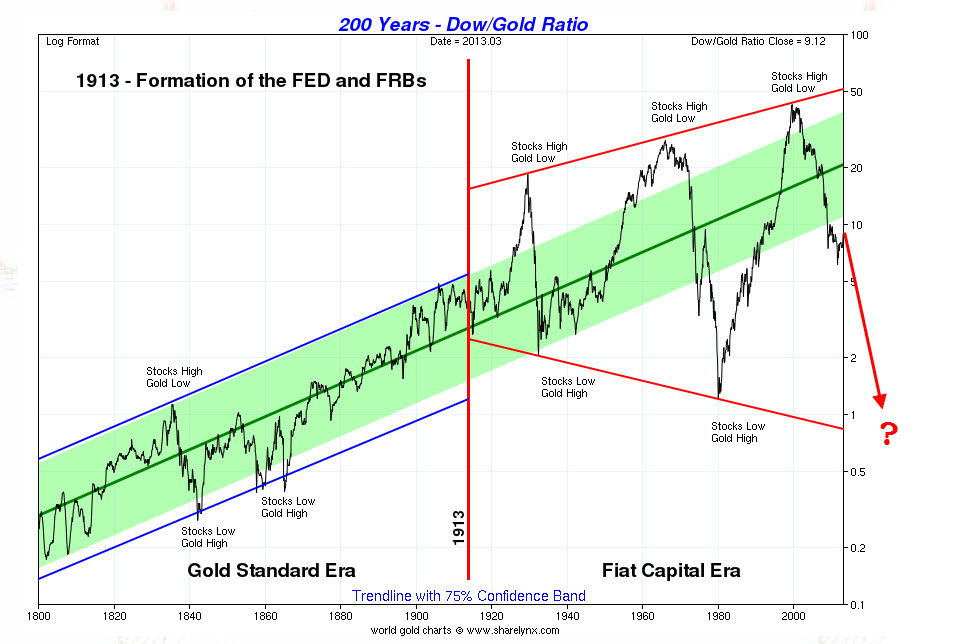

One of the more fascinating reminders of what may be to come for the remainder of this gold bull market, is the charted history of the dow/gold ratio. Below are two charts illustrating the upward potential in gold which remains for the duration of this market.

Here is the second and more alarming dow/gold ratio chart, illustrated with a “confidence trend band”:

…..read more HERE

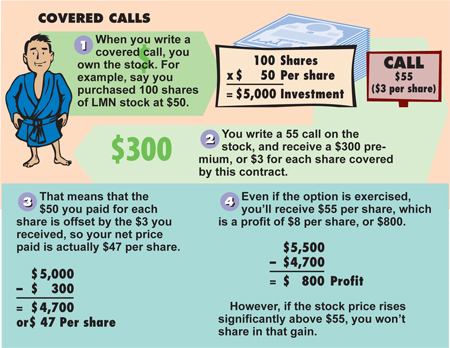

One of Michael Campbell’s favorite investment strategies is to sell options against his investments. Selling options can be an ideal way to add income to your account. There might be no guarantees in the stock market, but that doesn’t mean you can’t minimize risk, and generate income.

Here’s an example of Selling Call Options:

You have 500 shares of XYZ stock trading $20 a share and valued at $1,500.

You sell (writes) 5 call option contracts (1 option contract covers 100 shares) @ $300 x 5 and receive $1500. This premium of $1500 covers a certain amount of decrease in the price of XYZ stock (i.e. only after your initial $10,000 stock position has declined by more than $1500 at the time of the option expiry would you lose money overall).

Let’s look at the possible scenarios…

1) The Covered Call Option expires worthless. This happens if the current market price of XYZ is below the strike price ($20) of the call option on its expiration date. This is fantastic because you were paid income up front and now that the time of the option is over, you are no longer obligated to anything. You can forget all about the option and continue to hold the stock, or you can repeat and sell another covered call option.

2) The Covered Call Option is exercised. In this case, you were paid money up front and then you were obligated to sell the stock at the agreed upon price ($20) on the expiration date of the call option. This is still profitable news because you owned XYZ at $20, took in the $1,500 you were paid to sell the Call Option, your profit from the date you made the decision to sell the call option is $1,500 / $10,000 or 15%.

The point is that you are increasing your guaranteed income by being willing to trade away some of your upside profit potential.

Here’s another example in a visual form:

There are other option strategies, for example to learn how to protect yourself from losing money by buying insurance in the form of a put option, go HERE

You’d think that with all this practice, politicians would know how to handle a banking crisis by now. Most especially in the Eurozone.

But no. Five years since Bear Stearns hit the skids (the anniversary was Monday) the Cypriot mess is such a mess that people elsewhere feel the urge to say that “it couldn’t happen here.”

Portugal’s finance minister said it Tuesday afternoon. Italy’s La Stampanewspaper said it Tuesday morning. Yet a raid on banking deposits already happened in Italy, a mere 21 years ago with a 0.6% hit across all bank accounts. Italy applied a hit of 4% or so in 1920 as well, back when the Czech government, Austria, Germany and Hungary all tried the same move too. Norway made a grab for savers’ cash in 1936. Brazil and Argentina used the gambit — raiding savers’ accounts for emergency cash — a little over a decade ago.

Still, it could never happen, right?

Protect the small savers” — barring the more recent examples above, that has been the mantra of policy wonks and politicians dealing with bank failures since the Great Depression 80 years ago.

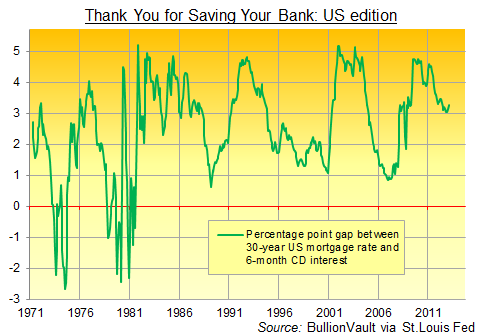

Customers of Bear Stearns barely noticed the change, for instance, when it collapsed into the warm, taxpayer-funded embrace of JPMorgan for just $2 per share on March 18, 2008. Because amongst major-currency nations, the preferred route to whacking the little guy — and getting him to pay for the banks’ excesses — has been via interest rates, as our chart above shows.

Get borrowers to pay way more than depositors earn, and post the difference straight to your bottom line. Throw in negative real rates on bank savings and government bonds — courtesy of central banks squishing rates below the pace of inflation — and the same scam can help entire economies chip away at the real value of their public debt, too.

But this rule — the rule of hiding the theft from savers — finally broke Saturday morning. To get a bail-out from the rest of Europe, the government of Eurozone-member Cyprus agreed to a 9.9% levy on anyone with €100,000 in a Cypriot bank. Most amazing, small savers are no longer sacred. They would be hit for 6.75% on deposits below €100,000.

The FT called this a stupid idea whose time has come. Paul Krugman writing in the NY Times said “It’s as if the Europeans are holding up a neon sign, written in Greek and Italian, saying ‘Time to stage a run on your banks!‘” The U.K. government, ever eager to pretend that we Brits are immune to bank-account losses, is shipping out €1 million in cash to help pay our armed forces stationed there, and it has also promised U.K. tax-payers will make good any loss the troops might suffer on their Cypriot deposits in just the way that we all shared the £100m cost of making U.K. users of high-yielding Icelandic banks whole in 2008.

Heaven forbid anyone should say that such high-paying bank accounts should have been warning enough. Like Felix Salmon says, a promise is a promise, and Cypriot savers had bank-account insurance up to €100,000. It’s just not fair!

A few other talking-heads meantime guess — as we do — that the initial “levy” was a dummy, intended to make the real savings tax look much less drastic. But lots of people also note that Russian mafia money, a huge part of Cypriot banking, will see its 9.9% levy as just a cost of doing business. The island’s reputation as a money-laundering center will be intact, at the cost of hurting the little guy.

Cyprus accounts for just 0.5% of the 17-nation Eurozone economy. The proposed levy will raise perhaps €5.8 billion, just $7.5bn. Yet the Eurogroup’s action has already seen stock markets sink, along with the euro. The gold price in euros jumped 2.3% at the start of Asian trade Monday morning, and has since jumped again as the chaos in Cyprus’s rescue gets worse.

Now, this is very much a crisis in motion. The Cypriot finance minister, for example, may or may not have resigned Tuesday whilst visiting Moscow to discuss Russian aid and bank savings. And as we say, odds are that the levy on small savers will yet be cut, altering the terms to make whatever deposit-grab is left more acceptable. But either way, the big lie behind the financial crisis so far — that bank savings are safe — has blown up again.

Putting cash on deposit makes you a creditor. And in financial crises, the creditor always pays in the end, whether through inflation, default or a “levy.” Yes, you are supposed to be safe from immediate loss, thanks to the charade of deposit insurance. But the cost of getting off price risk is credit risk lying unseen and unstated until the day that it matters.

Holding a little physical property, in contrast, exposes you to price movements. But it gets a chunk of your savings away from the myth of bank-account security. Hence the jump already this week in gold.

Even without that price move, gold still makes sense as a physical escape from all-too transient banking. Of which in Nicosia and all points west there remains way too much. The Cypriot solution is at least one way of shrinking the finance sector overnight.

About the Author

Adrian Ash runs the research desk at BullionVault. Formerly head of editorial at Fleet Street Publications – London’s top publisher of financial advice for private investors – he was City correspondent for The Daily Reckoning from 2003 to 2008, and is now a regular contributor to a number of investment websites.

They did it!

Last week something major happened off the coast of Japan…

Nearly 1,000 feet below the seabed, Japanese engineers successfully accomplished something that has the potential to turn this resource-poor island nation into a world leader in fossil fuel production.

After hundreds of millions of dollars and more than a decade of research and testing, Japan has officially extracted natural gas from underwater deposits of methane hydrate.

After hundreds of millions of dollars and more than a decade of research and testing, Japan has officially extracted natural gas from underwater deposits of methane hydrate.

I know that doesn’t sound very exciting — but bear with me, because this event has officially marked the beginning of a new energy revolution that could actually be bigger than fracking!

Let me repeat that: bigger than fracking.

Flammable Ice

According to a 2010 International Energy Agency report, it’s estimated methane hydrates — also known as “flammable ice,” because it’s essentially a frozen gas — contain almost twice as much energy as all the world’s resources of gas, oil, and coal combined.

Let that sink in for a moment…

…..read more HERE

With these words, the 89 year old Godfather of Newsletter writers, Richard Russell went Bullish the Dow on March 11th.

“Yes, I know that this market is uncorrected during its long rise from the 2009 low, and I know that there are risks in buying an uncorrected advance that is becoming uncomfortably long in the tooth, but my suggestion is that my subscribers should take a chance (after all, Columbus took a chance) and take a position in the DIAs.”

“My intuition tells me that there will be an early period [around now] of erratic and uneven scary advance, this to occur while formerly battered investors work up the nerve to enter this market,” Russell predicted.

“Then the action will smooth out as the crowd gathers courage and confidence.Finally, in the last stage of this advance we might see the stock averages rise in parabolic fashion.This will be the time to pack our bags and get out.”

One of the toughest things to do is buy when it is the ideal time to do so. When it is terrifying. For most people that would have been at Dow 6,547 after the shocking 2007-2009 collapse,

For old experienced market hounds like Richard Russell, buying stocks right here at Dow 14,455, up 7,908 points or more than double from the 6,547 low in 2009 must be about as terrifying as it gets! Thats probably why Ben Gersten, Editor for Money Morning, has probably written the article below questioning Russell’s conversion.

The writer of Dow Theory Letters, clearly one reason for Russell’s change of mind was his use of the 100 year old Dow Theory. A theory that is said to have formed the basis for all modern technical analysis through its definition of a trend and its reliance on studying price action.

You can read Ben’s analysis of Russell’s decision HERE, or click on the link below:

Should Investors Still Trust the Dow Theory as a “Buy” Signal?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair