Gold & Precious Metals

Gold forecasts split at $10,000 & $1000 as ETFs sell, central banks buy, Indian dealers cleaned out

Gold forecasts split at $10,000 & $1000 as ETFs sell, central banks buy, Indian dealers cleaned out

Wholesale gold rose to an eight-session high just shy of $1450 per ounce in London trade Thursday morning, recovering 45% of this month’s near-record slump.

Asian stock markets also ticked higher, but European shares were flat while commodities extended their rally.

Silver prices were unchanged for the week so far at $23.30 per ounce.

Gold priced in sterling fell £10 per ounce from an eight-session high of £946 as the pound jump on news that the U.K. avoided recession – growing just 0.3% – in the first quarter of 2013.

“Gold is continuing [its] recovery,” says the daily comment from the commodities team at Germany’s Commerzbank.

“Rate-cut speculation ahead of next week’s [Eurozone central bank] meeting – and the prospect of continued ultra-loose U.S. monetary policy following more weak economic figures – are lending buoyancy to the gold price.”

Investors who buy gold,” writes Société Générale’s global strategist Albert Edwards in a new report, are making “a bet against central banks’ competency.”

Given central banks’ track record, he adds – repeating his team’s forecast of $10,000 gold – “that’s certainly a bet I’d be happy to still take.”

Money-creation leading to a surge in inflation is also the forecast from billionaire hedge-fund manager John Paulson, who reportedly told clients on a webinar Wednesday that he and his chief precious metals strategist – the highly respected former UBS analyst John Reade – are also “holding course” despite last week’s price crash.

Dutch bank ABN Amro however – which this month said “the demise of gold [was] still at an early stage” – today revised its $1000 gold forecast from end-2015 to the end of 2014.

“ETF [trust funds] still see sellers, but physical demand remains very strong,” says Moudi Raad at Swiss refining and finance group MKS.

New York’s giant SPDR Gold Trust yesterday shed another 4 tonnes of gold, taking the bullion held to back its shares down to the lowest level since the start of September 2009 at 1093 tonnes.

Over in India however – the world’s heaviest gold-buying nation – “We are unable to get supply,” Reuters quotes a state-bank dealer.

“Refiners have sold out till second or third week of May. Gold for immediate delivery is quoted at $10 on London prices.”

Latest data from the International Monetary Fund meantime show that emerging-market central banks again chose to buy gold for their reserves in March.

Russia led central-bank gold buying, adding 4.7 tonnes to reach 981 tonnes, while Turkey continued to pull in metal from its commercial banks, adding a further 33 tonnes to reach 409.

“I think physical and central banks…those buyers are supporting the market,” Reuters quotes Yuichi Ikemizu at Standard Bank in Tokyo.

“With this sharp decline in the price,” he adds, “I think South Korea is buying gold too. [It] always buys gold when the price comes off.”

About the Author

About the Author

Related Articles:

- Stocks higher, U.K. looking better, gold has glimmer

- Physical gold vs. paper gold: waiting for the dam to break

- Portfolio manager Greg Orrell: ‘my belief in gold has not wavered’

- Gold lifted by physical bar demand but silver relatively weak

- U.S. Mint suspends sales of small gold coins

We don’t like the looks of it…

Advisors are too bullish. Investors are too complacent. The financial authorities are too confident.

All up and down Wall Street… in central banks and in Washington… the stuff that goeth before the fall is thick, sticky and stinky.

The economy is recovering, they say. The Fed has the situation in hand, they add. Don’t worry… we know what we’re doing, they assure us.

Barron’s magazine says the Dow is going to 16,000, illustrated with a picture of a bull on a pogo stick.

Barron’s magazine says the Dow is going to 16,000, illustrated with a picture of a bull on a pogo stick.

Prime Minister Abe says he’ll revive the Japanese economy by printing yen to buy Japanese bonds. And speculators take each hint from the Fed as though it were a whisper from God Himself.

And all around them, the real economy struggles to stay even. Here’s David Rosenberg of Gluskin Sheff with 12 signs that the economy is weaker than we think:

-

Household employment (-206,000 in March, the steepest decline in well over a year).

-

Real retail sales (-0.3% in March, down for the second time in three months).

-

Manufacturing production (-0.1% and also down in two of the past three months).

-

Core capex orders (-3.2% in February and, again, down in two of the past three months).

-

Single-family housing starts (-4.8% in March and negative for two of the past three months, as well).

-

New home sales (-4.6% in February).

-

Philly Fed for April down to 1.3 from 2 .

-

NY Fed Empire manufacturing index down to 3.05 from 9.24.

-

NAHB Housing Market I ndex down to a six-month low of 42 in April from 44.

-

Conference Board C onsumer C onfidence I ndex down to 59.7 in March from 68.

-

University of Michigan consumer sentiment down to 72.3 for April from 78.6, the lowest in over a year.

-

Conference Board leading indicators down 0.1% in March, first decline in seven months.

Markets Make Opinions

Facts, figures, statistics…

Do you believe them, dear reader? We don’t. We’re just giving the dreamers a little taste of their own medicine.

“Markets make the opinions,” say the old timers. When prices are up, people share the opinion that they are going up. When prices go down, opinions change with falling prices.

And when prices rise, the opinion mongers look for reasons to explain why they have become so bullish. They find indexes, statistics, numbers – all the “facts” confirm their opinion. When prices fall, their opinions grow dark and they need to find new facts that they can use to justify a counter view.

Get a feeling. Form an opinion. Find a fact and pretend that you are a rational, reasonable investor. That’s the name of the game.

But are we any different?

Not at all. We’re just crankier. More cynical. And less impressed by authority in all its forms. Besides, we’ve been living in Argentina.

If a Nobel Prize-winning economist tells us that the economy is improving, what do we really know? We know he can talk!

If the president tells us that he and his friends are making the world a better place, what do we do? We laugh!

If a leading financial magazine tells us that the “Big Money” firmly believes the Dow is headed higher, what do we do?

We seriously consider selling!

From bearish fund manager John Hussman: “Rule o’ Thumb: When the cover of a major financial magazine features a cartoon of a bull leaping through the air on a pogo stick, it’s probably about time to cash in the chips.”

Regards,

![]()

Bill

“The Dollar and Oil May be Telling Us Gold is Toast”

Quotable

“Speaking the Truth in times of universal deceit is a revolutionary act.”

George Orwell

Commentary & Analysis

The Dollar and Oil May be Telling Us Gold is Toast

I’ve been surmising/guessing and attempting to validate a thematic JR and I developed about three or four months ago, initially shared with our Global Investor subscribers—the commodities super cycle is over. Is gold validating that view? I tend to think so.

My bias is leaking in here. We have been short gold for many months. Our initial target was 1,400. Now the question is: Will gold fall further? I say yes. Why? The US dollar is one reason.

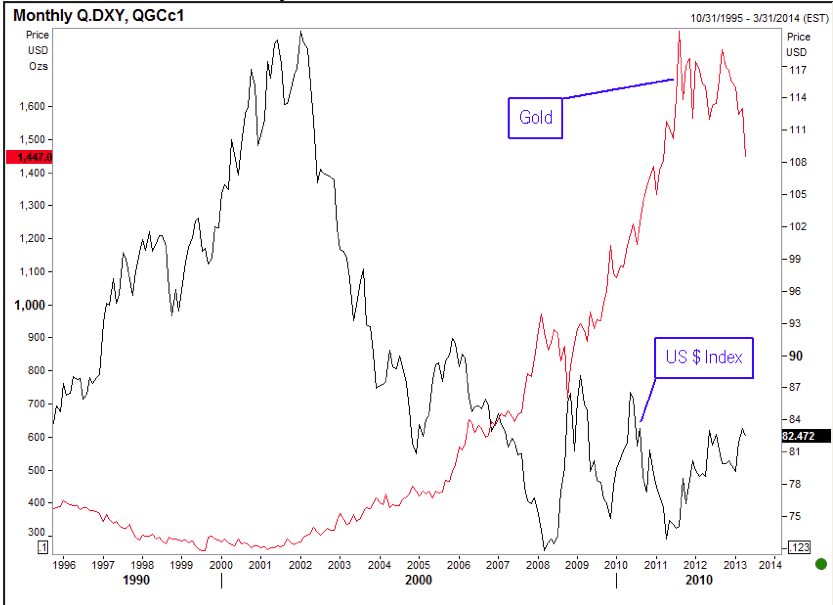

Long-time readers of Currency Currents might remember that back in mid-2008 I said I expected the US dollar had bottomed thanks to the credit crunch, and said crunch was a sea change in the global macro environment–the catalyst for new multi-year bull market in the US dollar. I have a seven to ten year time frame when I say multi-year bull market. If I am right about that, the gold bull market may be toast for a while, and has the potential to go much lower from here based solely on the correlation below:

US Dollar Index versus Gold Monthly

But there is more evidence staking up.

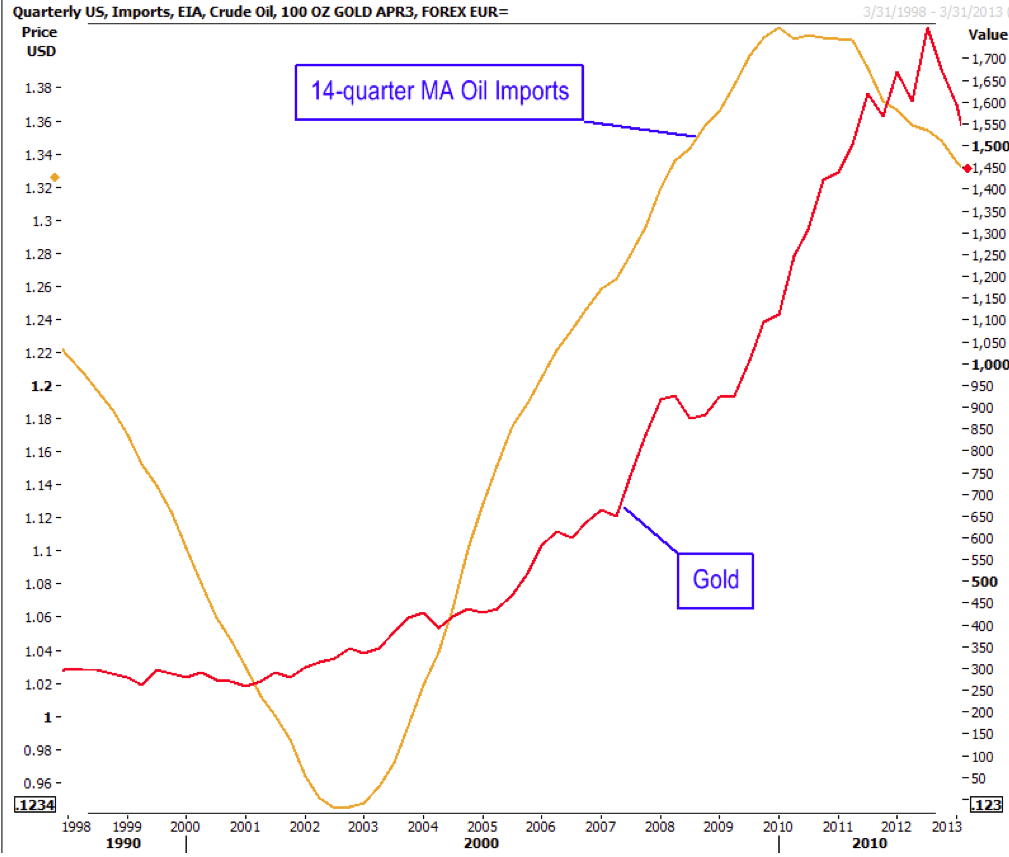

As you might know, one of my fundamental rationales for a bull market in the dollar has to do with rising US energy production, or the flip side, i.e. falling oil imports. If the oil analysts are correct, then increasing energy independence for the US economy will lead to lower cost energy. That may have a powerful positive self-feeding impact for the US economy for three reasons:

1. It will likely reduce the US current account deficit, thus reducing the need for international funding of said gap; and

2. If energy prices do in fact fall, given the rising local supply, this should put a major dent in inflation expectations (a big driver for gold). Is there a more powerful real economy price driver than energy?

3. Foreign direct investment will flow into the US as international companies set up manufacturing bases so they can take advantage of cheaper energy.

And if we go to the chart we see something very interesting, at least it is interesting to me, and maybe to you.

Summary: What is the validation to my guess gold may be toast for a while and goes a lot lower: 1) A stronger US dollar 2) Increasing US energy independence

Together they will help reduce inflation expectations in a self-reinforcing manner.

I am sure this isn’t something you are going to hear on your local irritating “buy gold” radio advertisement. But I do think it makes a whole lot of sense.

Jack Crooks Black Swan Capital

I grew up relatively poor, the second of eight children. My father earned $12,000 a year as a college professor. As a teenager, I was ashamed of our small house, my hand-me-down clothes, and my peanut-butter-and-jelly sandwiches.

I dreamed, literally dreamed, of living like a rich man.

And so, when I got my first job at age nine as a paperboy – and then at 12 as a lackey at the local carwash – I would spend my money on luxuries, like a pair of brand-new Thom McAn shoes.

I worked every chance I got through high school, and then worked two or three jobs during college and graduate school. I spent 80% of my money on necessities: food, clothes, and tuition. But I always spent a bit on little niceties. Even back then, I had the notion that I didn’t need to deprive myself now for some better life later.

I tell you this to emphasize a key part of the simple money-management system I’ve used to generate more than $50 million in wealth…

I don’t believe in scrimping severely to optimize savings. I believe you can live a rich life while you grow rich, so long as you are willing to work hard and you are smart about your spending.

I don’t believe in scrimping severely to optimize savings. I believe you can live a rich life while you grow rich, so long as you are willing to work hard and you are smart about your spending.

Think of the typical earning/spending/saving pattern of most wealth-seekers…

During their 20s, they spend every nickel of their modest income to make ends meet. At that age, it is nearly impossible to put aside money for the future.

During their 30s, their income increases. But this is also when they start a family. Expenses soar. There are more mouths to feed, a “family” car to buy, and the dreaded down-payment on a first house. They manage to save a little during these years, but not nearly as much as they thought they would.

If they work hard and make good career decisions, their income climbs much higher in their 40s and early 50s. They have more money to put aside for the future, but they are also tempted into buying newer cars, nicer clothes, more exotic vacations, and – the biggest wealth-stealer of them all – that dream house.

In their later 50s and 60s, their income plateaus or even dips… and they may have to start shelling out for college tuition. Aware that their retirement funds are being depleted rather than enhanced, they invest aggressively to try to make up the difference.

Finally, sometime in their mid- to late-60s, they realize that they don’t have enough money to retire. They have spent almost 40 years working hard and chasing wealth, but they never managed to attain it.

It’s sad, but it’s the reality for most people. And it is just as true for high-income earners (doctors, lawyers, etc.) as it is for working-class folks.

There are two lessons to be drawn from this:

First, it is very difficult to acquire wealth if you increase your spending every time your income goes up.

Second, setting unrealistic investing goals means taking greater risks. And taking more risks, contrary to what many pundits say, will almost always make you poorer… not richer.

The truth is, there is only a marginal relationship between how much you spend on housing, transportation, vacations, and toys, and the enjoyment you can derive from them.

My spending strategy is simple: Discover your own, less expensive way to live a rich life. By a “rich life,” I mean a life free from financial stress, but also filled with things that give you pleasure.

For example, good, restful sleep is essential for a happy life. Ideally, you’re going to spend around one-third of your life sleeping. So rather than “pay up” for an expensive car or an expensive necklace, buy a great mattress. By getting a great mattress (which can be had for less than $2,000), you’ll sleep as well as any billionaire… and be just as happy.

Your family can be just as happy in a house that costs $100,000 or $200,000 as opposed to one that costs $10 million or $20 million. Likewise, a $25,000 car will get you where you want to go just as well as a car that costs 10 times that amount. There are dozens of ways to live like a millionaire on a modest budget. If you learn those ways, you will have a tremendous advantage over everyone else at your income level.

Make smart spending decisions. Stop thinking that because you’re earning more money, you should be spending more. Your future wealth is determined by how much you save and invest, not by how much you spend.

So here’s what I’d like you to do: Figure out how much you need to spend every year to live your own personal version of a “rich” life. It might help to spend a few minutes thinking about all the things you truly enjoyed last year. If you are like me, you’ll find that almost all the things you enjoy require very little in the way of money. (Those are the true luxuries.)

Keep the biggest wealth-stealing expenses – like your house, your cars, and entertainment – to a necessary minimum. And eschew any expenditure that has a brand name attached to it. Brand names are parasites that gobble up wealth.

Don’t nod your head and promise to get to it sometime in the future. Do it today. Estimate, as well as you can, what you need to spend each year to have the life you want.

This is a number you must have firmly in your mind if you intend to be a serious wealth-builder.

This simple system for managing money can work for you if you commit yourself to it. As I said, it’s part of the system I used to build a net worth of more than $50 million – and it’s still working for me and everyone else I know who has tried it.

So today, spend the time it takes to establish your own approach to “living rich” now… and in the future.

Regards,

Mark Ford

Editor’s note: Last year, Mark formed a small group at The Palm Beach Letter to teach subscribers how to live rich while building wealth. The results have surpassed all expectations… Shaun Hansen wrote in to say he made $20,000 in less than 60 days – from home – with Mark’s techniques.

Mark has agreed – for a limited time – to open his complete “playbook” to DailyWealth readers at a generous discount. To review the full details and access this “life-changing material,” click here.

Further Reading:

Find more of Mark’s strategies for growing your wealth here…

A Three-Year Plan to Achieve Financial Independence

“Becoming a multimillionaire takes years. But breaking the chains of financial slavery can be done relatively quickly.”

How to Get a Little Bit Richer Every Day

“By following one simple rule of getting richer every day, I was able to do better than I ever expected… without a single day of feeling poorer than I was the day before.”

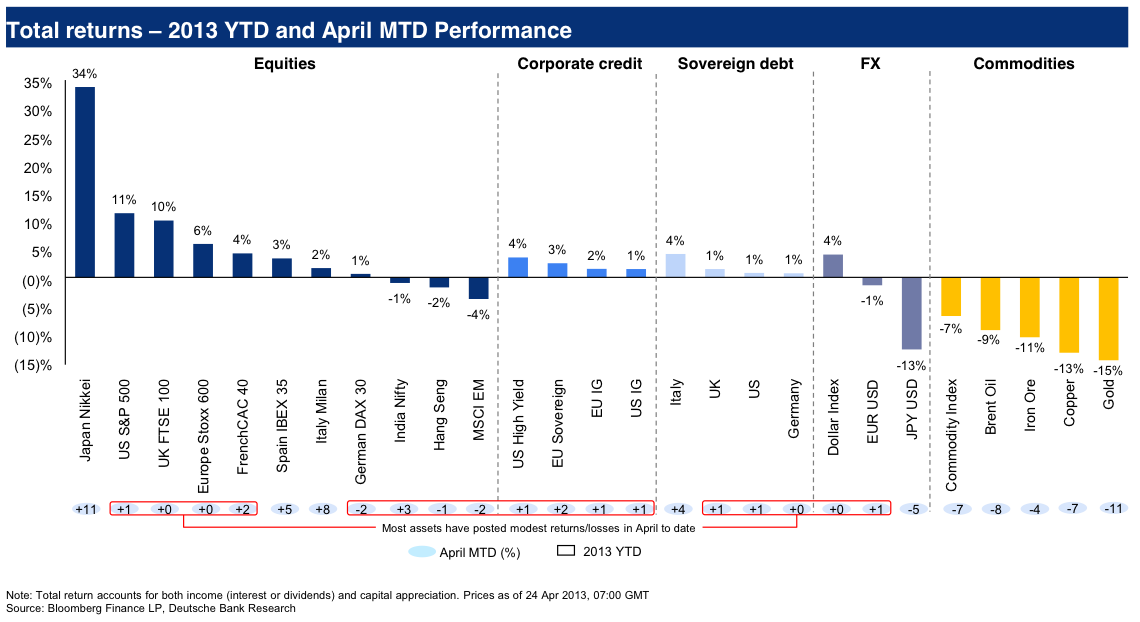

Gold is the biggest loser in this snapshot of the financial markets since the beginning of the year (and the beginning of the month) via Deutsche Bank‘s “Equity House View” report.

Thanks to Japanese Prime Minister Shinzo “Abenomics” Abe, the Nikkei is the top performer and the yen is a major loser.

Click HERE or on the Chart for a Larger View

ALBERT EDWARDS: Stocks Will Crash, Hyperinflation Will Come, And Gold Will Go Above $10,000

This is always reassuring. SocGen strategist Albert Edwards remains an ultra-bear, and predicts everything will go to hell.

In his new note he writes:

We still forecast 450 S&P, sub-1% US 10y yields, and gold above $10,000

My working experience of the last 30 years has convinced me that policymakers’ efforts to manage the economic cycle have actually made things far more volatile. Their repeated interventions have, much to their surprise, blown up in their faces a few years later. The current round of QE will be no different. We have written previously, quotingMarc Faber, that “The Fed Will Destroy the World” through their money printing. Rapid inflation surely beckons. But that will not occur without firstly a Japanese-style loss of confidence in policymakers as we dive back into recession and produce dislocative market moves.

So yeah, it goes on from there. Lots of doom. This is why everyone loves Albert Edwards.

Marc Andreessen Is Blown Away By Google Glass: ‘Oh My God, I Have The Entire Internet In My Vision”

Marc Andreessen Is Blown Away By Google Glass: ‘Oh My God, I Have The Entire Internet In My Vision”

….read about them HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair