Personal Finance

U.S. Stock Market – With 5% or so upside and multiple times that to the downside, risk/reward doesn’t favor being long. (Ed Note: All charts were chosen by Money Talks Editor)

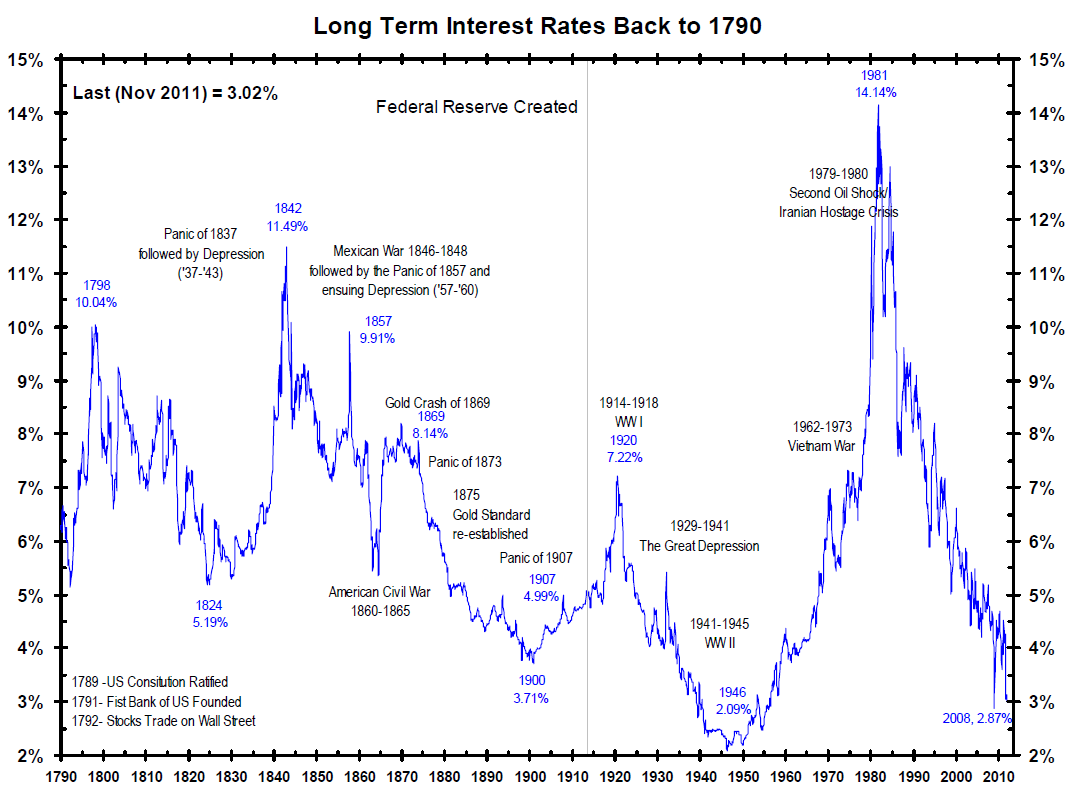

U.S. Bonds – Avoid!

U.S. Dollar – Despite numerous reasons to push it higher, it still can’t get above the selling area of 84-85 area on the U.S. Dollar Index.

Canadian Dollar: Would love to buy more Canadian Dollars around .95

Gold and Silver – Some very bullish technical patterns regarding momentum are starting to form, but I suspect we first need to get pass options expiration next week before any real bottom can be cemented.

Mining and Exploration Shares – Here too some bullish momentum indicators are turning positive; but an unbelievable amount of resistance awaits any significant rallies – especially as one goes down the food chain into juniors.

Richard Russell is bullish. While there’s more money sloshing about than he has ever seen in his 88 years of living on this planet and the treasury market has evolved into the biggest bubble in the history of the world, his studies are bullish and the Fed seems to have the Treasury Market well in hand. Despite all this he is still a chronic worrier which is probably a good thing for the rest of us.

Here is one of the latest clips from one of his letters that makes a pretty interesting read:

To be honest, I’m outright bullish on the market myself. Strange, I woke up Sunday morning with this dream. Bear markets are meant to clean out the financial garbage, and put the fear of God into investors and politicians. The crash of 2008-09 failed to do that, mainly because the Fed stepped in and reputedly saved the US and the world from disaster.

Furthermore, bear markets are supposed to put the fear of God into just about everyone. The crash of 2008-09 failed to dampen the speculative ardor of a good many investors. Here we are, about 5 years after the 2008-09 crash, and speculative juices are back again.

Here’s my fantasy — the stock market opens one morning, and there are absolutely no bids. Unexplainably, everyone is frightened at the same time, and everyone decides to wait to see how the market opens. Finally, a few bids come in, and the Dow opens down 400 points. There is a minute of shocked indecision, and suddenly the NYSE is flooded with sell orders.

What happened to the people who had fat paper profits? They were going to sell if the market backed off maybe 50 or 60 points from its record highs. Their strategy didn’t work, not with a market where the Dow opened down 400 points. And that’s where my absurd fantasy ended.

But the reality is that my studies continue to look OK. I’m bullish, although I’m still an incurable worrier. One more thing. The Treasury bond market has evolved into the biggest financial bubble in history. But the Fed has the Treasury market well in hand. So why worry about bonds?

Ed Note: Richard didn’t enclose this Bond Chart, but it is pretty clear where yields were in of 2010 and that they have been improving since then.

Yesterday’s NY Times featured a page 1 story on the incredible luxury-building boom in the City. Evidently, super-luxury housing in NYC is less expensive than it is in London or Hong Kong.

The new 432 Park Avenue super-luxury building will be the tallest residential building in the Western hemisphere. Already the penthouse has been sold for a cool $95 million. Who’s buying these insanely priced apartments? Mostly foreigners who want to establish “getaway” residences, “just in case.”

Other super-luxury buildings are springing up all over NYC. Said one real estate agent, “It’s not location that is so important, it’s all about bigness and pure luxury.” A builder states, “It’s all about helicopter views.” When a person puts $95 million into a New York penthouse, he’s putting his money into an object of tangible value.

But what happens if times get tough? The cost of carrying that penthouse becomes prohibitive. The penthouse is not moveable. Thus paying $95 million for a penthouse is a risky play, and you have to hope that underlying conditions don’t change. Ironically, the same article in the Times states that the median family income in NYC has fallen 8% since 2008.

In the same issue of the Times there appears an ad for two vintage Patek Philippe wrist watches. One is offered for $250,000, the other is priced at $1,200,000.

Russell comment — I’ve never seen so much money being sloshed about. Nor have I ever seen so much news of corruption and criminal activity. Maybe the media is just doing a more thorough reporting job than ever before.

I must admit that I am fascinated with the current stock market. I feel that I am almost daring the market to push higher. And yet, with it all, I don’t see any indications of danger in my studies. If this market does top out, it will top out without any of the usual signs of trouble. Until then, I remain bullish. After all, I’ve never seen a market turn down on its own with no signs of danger prior to the top-out.

“I think the gold miners will fly once gold gets over 1500. This crunch job on gold is the crudest manipulation job I’ve ever seen.

The Fed wants to kill all signs of inflation to hide the damage they’re doing to the middle class. First the Fed leaves food and energy out of the CPI, and then they get the Labor Department to lie about the figures. Their last trick — smash the price of gold and silver. What are they going to do when the bond market (fearful of inflation) collapses? You can’t fool all of the people all of the time.”

To subscribe to Richard Russell’s Daily written Dow Theory Letters CLICK HERE.

As a general rule, the most successful man in life is the man who has the best information

My last article, ‘Give It A Doubt’ was about population growth, urbanization in developing countries and the one billion people predicted to join the consuming classes by 2025.

“One billion people will enter the global consuming class by 2025. They will have incomes high enough to classify them as significant consumers of goods and services…” McKinsey Global Institute, Urban world: Cities and the rise of the consuming class

Some of these new consumers are going to be Americans but the majority are in developing countries, they might not want to be Americans but they do want at least a modest piece of what we’ll call the American lifestyle, the cell phones, flat screen TV’s, a nicer apartment, a car or maybe a motorcycle, washer/dryer, a fridge, AC – the amenities of a modern society and all the necessary infrastructure that goes with a well functioning competitive modern economy.

But what if all these new one billion consumers were to start consuming, over the next 12 years, just like an American? What’s going to happen to the world’s mineral resources if one billion more ‘Americans’ are added to the consuming class? Here’s what each of them would need to consume, per year, to live the American lifestyle…

In 2010, more than 38,000 pounds (19 tons) of minerals and fuels were needed per person to maintain the American lifestyle.

Out of the 38,000 total pounds needed, 21,675 pounds were energy fuels – the coal, petroleum, natural gas, uranium – required for transportation and to heat, cool and light homes and businesses.

One billion new consumers by 2025. Can everyone who wants to, live an American lifestyle? Can everyone everywhere else have everything we in North America have?

The answer is a resounding NO!

“The data also show that nations such as South Africa and China will need to increase their average urban per-capita copper stock-in-use by seven or eight times to achieve the same level of services as the developed countries if they use existing technology.

Is there enough copper to meet this potential requirement?

Concern about the extent of mineral resources arises when the stock of metal needed to provide the services enjoyed by the highly developed nations is compared with that needed to provide comparable services with existing technology to a large part of the world’s population. Our stock data demonstrate that current technologies would require the entire copper and zinc ore resource in the lithosphere and perhaps that of platinum as well. Even a lower level of services could not be sustained worldwidebecause a continuing supply of new metal is needed to make up for inevitable losses in the recycling of the metal stock-in-use.

Substitution has the potential to ameliorate this situation, but one should not automatically assume that technology will produce a satisfactory substitute for every service at an affordable price and precisely when needed.

…anthropogenic and lithospheric stocks of at least some metals are becoming equivalent in magnitude, that world-wide demand continues to increase, and that the virgin stocks of several metals appear inadequate to sustain the modern ‘‘developed world’’ quality of life for all Earth’s peoples under contemporary technology…Do we really envision a developed world quality of life for all of the people of the planet…?” R. B. Gordon, M. Bertram, and T. E. Graedel, Metal Stocks and Sustainability

Copper ETF

The U.S. Securities Exchange Commission (SEC) approved the first copper exchange traded funds (ETF) to actually hold the physical metal. J.P. Morgan and Blackrock received approval to each start copper ETF’s that will allow speculators to buy and hold copper in warehouses – up to 183,000 tons – the more shares investors buy, the more copper is taken off the market.

JPMorgan’s fund would store LME copper valued at up to $499,761,150. BlackRock’s iShares Copper Trust – Goldman Sachs owns the warehousing company Metro BlackRock intends to use to store its copper – would use up to 121,200 tonnes of copper as guarantee against shares in its fund.

As of writing the two funds would equate to 30 percent of current copper stocks in LME-bonded warehouses.

Credit Suisse/Glencore, Deutsche Bank and Citigroup are also looking at physical copper ETFs. Goldman Sachs signed a copper off-take agreement with Spanish miner Emed in 2012.

“ETFs…can immediately take metal out of the market, potentially leading to physical scarcity. If investment in ETFs proves to be highly responsive to news, such as an earthquake in Chile for example, a relatively modest supply disruption could turn into a much larger one, directly impacting on the ability of consumers to buy the red metal.” Bloomsbury Minerals Economics’ Copper Briefing Service

Future Production

Some of the major copper projects either going into production or continuing to ramp up are:

- Buenavista, Mexico

- Antapaccay, Peru

- Los Bronces, Caserones and Esperanza, Chile

- Salobo, Brazil

- Konkola Deep, Zambia

- Morenci, U.S.

- KOV and Tenke Fungurume, Democratic Republic of Congo (DRC)

- Oyu Tolgoi, Mongolia

Two of the world’s largest existing mines – Escondida in Chile and Grasberg in Indonesia – should start seeing higher output again.

In April of 2013 the Chilean Copper Commission (Chile is the world’s largest producer of copper) predicted global demand for copper will rise by 1.4 percent this year to 20.829 million mt. Global mine production will rise 3 percent to 17.526 million mt to create an estimated world surplus of 68,000 mt, rising to 89,000 mt in 2014.

There are many reasons to be bullish on copper

Global surpluses of 68,000 mt in 2013 and 89,000 mt in 2014, are, in the world of copper supply, fairly tight conditions. Perhaps even more significant, no one is calling for much in the way of a price decrease.

Why are analysts not calling for much of a price decrease? Well, many mines do not come online on time and the disruption rate, the amount of promised copper that fails to materialize is now as high as 8 percent – operating mines can suffer production stoppages/slowdowns or move into lower grade ore.

A long term structural trend became evident in the industry in 2012 – shortfalls in targeted production were characterized by a fall in grades and recoveries rather than unexpected disruptions.

Chile produces a third of the world’s copper and has seen a seven fold increase in energy costs over the last ten years, also because of a severe water shortage in the high desert, where most of the country’s major copper mines are located, water must be pumped from the ocean to almost 800 meters above sea level and then pumped hundreds of kilometers to the mines, of course the seawater must also be desalinated.

CRU estimates Chile’s copper production costs have risen 60 percent over the last seven years compared to a world average of 30 percent. Chile’s state copper giant, Codelco, has seen a 57 percent cash cost increase between 2010 and 2012.

Chinese end demand is growing and consumer destocking has ended.

Many of the world’s largest mining companies have delayed or outright halted expansion plans – BHP Billiton, the world’s largest miner, has said it will not spend the $80 billion slated for expansion by 2015.

There is a lack of good substitutes, plastic piping replaces copper piping but this has been going on for years, aluminum can replace copper in electrical cables but more is necessary for the same effect and connections are poor which can cause fires, this has lead to municipal building codes actually banning aluminum from being used for residential wiring.

There has been a recent surge in warehoused copper stocks, the increases reflect incentives offered to store metal in those locations. Glencore owned Pacorini has been offering incentives of more than $100 to deliver copper to their warehouses. These incentives have drawn usually unseen stocks into the public’s eye perhaps distorting impressions.

Perhaps the biggest reason to get bullish on copper are the massive costs and risks involved in finding and opening new mines in often geo-political risky countries where a miners social license to operate is shaky at best.

Copper prices need to be significantly above marginal cost, in other words, prices need to stay high enough to provide miners with an adequate return on their investment for building today’s much more expensive and riskier new mines. There is also a significant additional cost in keeping production constant year over year.

If copper does not stay well above miners marginal costs the much needed new mines will not be build.

Conclusion

Global growth is on the path for continued improvement in 2013 – metal consumption will expand. Excess copper stocks are being taken up by traders, warehousing companies and soon ETF’s.

Copper, one billion new consumers, over 800 million people to be born between now and 2025 and a massive current, and future, infrastructure deficit should all be on our radar screens.

Is an investment opportunity in copper on your radar screen?

If not, maybe one should be.

Richard (Rick) Mills

Richard is the owner of Aheadoftheherd.com and invests in the junior resource/bio-tech sectors. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, ninemsn, ibtimes, businessweek.com and the Association of Mining Analysts.

If you’re interested in learning more about the junior resource and bio-med sectors, and quality individual company’s within these sectors, please come and visit us atwww.aheadoftheherd.com

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

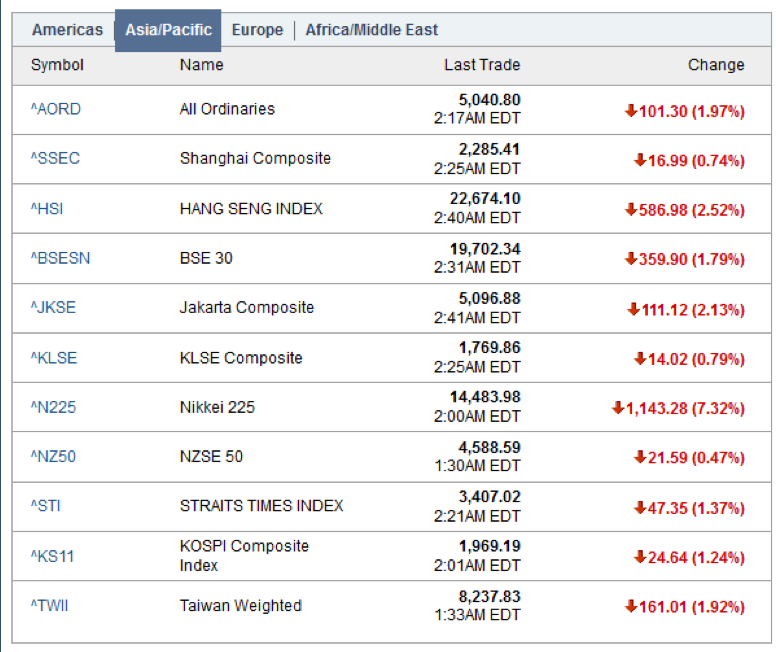

The Nikkei plunged a whopping 1,143 points as the chart shows;

Global Equities Hammered

Global Equities Hammered

It’s not just the Nikkei that’s being hammered. Asia-Pacific is in a rout as well.

Start of Reflation Bubble Bust?

Is this the start of the great reflation unwind? I don’t know, but we should all hope so.

The bigger the bubble the bigger the crash, and this Fed (central bank in general) sponsored equity and corporate bond bubble is enormous.

Ed Note: The critical point Martin Armstrong’s makes on a Flash Crash like the one described above is to focus on the crashes aftermath to determine its validity:

“The validity of any Flash Crash is determined by the aftermath. You simply cannot manipulate any market defined as changing the trend. So any attempt to impact prices is a short-term manipulation is short-lived. Take the May 6, 2010 Flash Crash in the US share market also known as The Crash of 2:45. The US stock market crash came on Thursday May 6, 2010 in which the Dow Jones Industrial Average plunged about 1000 points (about 9%). Regardless if it was an error or a deliberate attempt to push the market down, it takes place because there is a lack of bid. However, if the move is false, the the market will rapidly recover those losses within minutes or a couple of days. In that case, it was the second largest point swing in history, 1,010.14 points, and the biggest one-day point decline, 998.5 points, on an intraday basis in Dow Jones Industrial Average history. It is the LACK OF BIDS in the market that allows that downdraft to take place. Everyone made excuses from sticky fingers to it wasn’t real. The market failed to generate any sustainable rally. It rebounded rapidly closing at 10520.32 that day, but the next day it closed lower 10380.43. The market then rallied ONLY for 3 days (3 day reaction rule) reaching the highest closing at 10896.91 failing to even close above the high of the day of the crash 10925.86. The 3 day reaction rule worked and the market fell to new lows bottoming at .9596.04 on July 1, 2010The market is NEVER wrong. It does not matter if it was thin or robust trading. All the excuses in the world are still excuses. It is what it is. The Dow elected a Daily Bearish 04/27 1 day after the high. The trend was headed lower.

During a Flash Crash, (1) there is a lack of bids underlying the market, and (2) typically what happens is market-makers withdraw out of UNCERTAINTY. The very day of the low in the 1987 Crash, I looked at the screen and saw a 240 call option was $300 in the S&P when it fell to 180. I picked up the phone and tried to buy. The market-makers withdrew. ONLY my experienced saved me. I would have said buy at the market. I hesitated and put in a limit order. The next trade was 3000. With no market makers I would have been filled on that limit offer.

It is what it is. Excuses are simply the way to say you were not wrong, it was fake. But the truth is always revealed by the price. It is what it is.” – Martin Armstrong

Martin Armstrong’s perspective fascinated so many at last night’s Emergency Gold Summit, as you can tell from this email sent to Martin:

Thank you. Your insight into how everything is connected has saved me a fortune. I cannot tell you how many people showed up tonight simply to hear you. As the moderator said, you have the best track record of anyone. Your insight into the world is amazing. I understand what you said tonight as so many were talking about your speech walking out. It will be the markets that force political change. You have thousands of followers here in Vancouver. You should know that.

Thanks for everything you are doing.

R…S,,,

The entire Emergency Gold Summit Video presentation in which David Bensimon, Mark Leibovit and Martin Armstrong’s presentation and specifics about how everything is connected can be found HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair