Bonds & Interest Rates

Up, down. Down, up.

Up, down. Down, up.

Yesterday, the Dow reversed recent declines. It rose 180 points. Gold, too, seems undecided as to what direction to take. It fell $14 an ounce.

We’ll carry on… trying to figure out what is really going on.

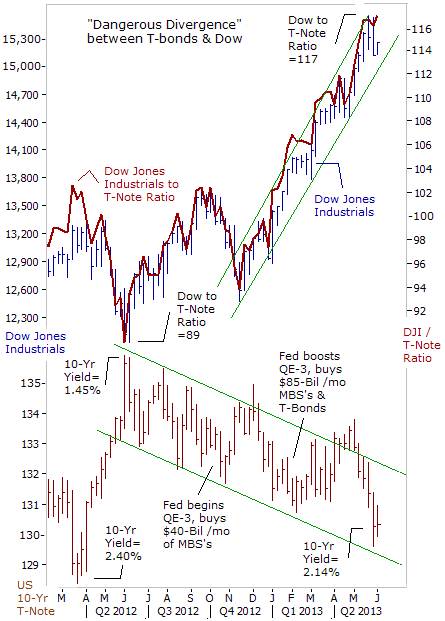

The typical post-war boomer has lived with just one complete interest rate cycle. Rates hit a low after the war… as the US faced the biggest fiscal cliff in its history.

The biggest stimulus program of all time – World War II – had come to an end. Millions of soldiers and defense industry employees were out on the streets looking for a job. Most economists and investors thought they’d never find one. They thought the war had pulled the economy out of the Great Depression. Now that the war was over, they expected it would fall back into its depressed state.

And they believed that interest rates – which had been falling for nearly a quarter of a century – were a forward indicator. Instead, they turned out to be nothing of the sort. The low interest rates of 1946-50 reflected the past, not the future.

The GIs went to work. They took out their wartime savings and started businesses… and families. Soon, the economy was booming.

And interest rates rose…

My Life in Bonds

In fact, interest rates in the US rose for the next quarter century… until the early 1980s.

And once again, investors who looked at interest rates for a hint of what lay ahead were misled. The high rates – the Fed funds rate was at 21% at one point – reflected the rising inflation rates of the 1960s and 1970s… not the lower inflation that lay ahead.

And here we are. Another quarter century has gone by – and more! Once again, interest rates are at record lows. In fact, they are now close to where they were when we were born.

That’s a complete roundtrip!

And once again, they tell us more about the past than the future. They are rising. From theNew York Times:

It has been a reliable fact of life for investors, corporations and ordinary borrowers: interest rates, for the most part, keep heading lower.

But all of that may be about to change. For prospective homeowners, the cost of mortgages has been going up in recent weeks. Governments are also facing the prospect of higher borrowing costs down the road, and they are projecting increases to their debt burdens. Savers with money in bank accounts, on the other hand, have the prospect of finally earning more than a pittance on their deposits. […]

Over the last few months […] investors and banks have been demanding higher payments for their loans, pushing up interest rates and bond yields.

“I think you all should be ready, because rates are going to go up,” Jamie Dimon, the chief executive of JPMorgan Chase, told a financial industry conference at the Waldorf-Astoria Hotel in Manhattan on Tuesday.

As investors brace themselves for a new era of higher interest rates, global markets in bonds, currencies and stocks have experienced spasms of turmoil. On Tuesday, the catalyst for the market’s volatility was disappointment over the Bank of Japan’s decision not to take new steps to address rising bond yields. That heightened worries that other central banks – the Federal Reserve in particular – will soon pull back on pumping money into the financial system.

We have been witnessing a fight between Mr. Bernanke and Mr. Market. We know who will win it. Mr. Market always wins in the long run. But we have no idea when… or how… he will win.

The latest news from the bond market suggests he is hitting Mr. Bernanke right where it hurts. Bond yields will go up. Mr. Bernanke will go down.

But watch out. Mr. Market is a wily and cunning fighter. He never likes to win his battles in a straightforward way. Instead, he dodges. He feints.

He fools us all…

Regards,

![]()

About Bill Bonner

Bill Bonner founded Agora Inc. in 1978. It has grown into one of the largest independent newsletter publishing companies in the world. In 1999, along with Addison Wiggin, Bill foundedThe Daily Reckoning. Today, this daily e-letter reaches over 500,000 readers around the globe.

Bill has also co-written two New York Times bestselling books, Financial Reckoning Day and Empire of Debt. He has written or co-written other widely read books as well, and has penned a daily column at The Daily Reckoning for over 12 years. Recently, Bill decided to “retire” from his role at The Daily Reckoning and begin writing his Diary of a Rogue Economist.

Bill Bonner’s Diary of a Rogue Economist is your gateway to Bill’s decades of accrued knowledge about history, politics, society, finance and economics. Sometimes funny, sometimes frightening – but always entertaining and packed with useful insight, Diary of a Rogue Economist can help you make sense of the complex world we live in today.

As a general rule, the most successful man in life is the man who has the best information

Most of the world’s cobalt is mined in Africa and the majority of Africa’s cobalt comes from the Democratic Republic of Congo. The DRC represented about 55 percent of global mine supply in 2012 and the country contains almost 50 percent of known worldwide cobalt reserves.

Most of the world’s cobalt is mined in Africa and the majority of Africa’s cobalt comes from the Democratic Republic of Congo. The DRC represented about 55 percent of global mine supply in 2012 and the country contains almost 50 percent of known worldwide cobalt reserves.

The DRC wants miners to process all their mined ore in the country to encourage more value-added production. On April 5th 2013, the government gave companies 90 days to clear stocks and halt exports of unrefined copper and cobalt – export streams are to be switched from ores and concentrates to refined products.

“It (the export ban – editor) will be fully enforced by July or August in order to allow mining operators to re-adjust themselves. The government is fully aware that mining operators have electricity problems.” DRC Mines Minister Martin Kabwelulu speaking to Reuters

The DRC has tried to impose such an export ban twice (in 2007 and again in 2010), imposition failed on both counts because of a lack of power in the country – the DRC suffers from acute electricity shortages despite a vast network of rivers.

Existing hydro plants, Inga I and Inga II, only produce about a quarter of their joint capacity of 1,700 MW because of low Congo River water levels and poor maintenance. Inga 3 wasn’t built because of concerns over the business climate in Congo. If the first phase, called Inga 3 Low Head does get built, South Africa will receive just over 50 percent of planned power output. The government actually expects power shortages to worsen in the coming years and that by 2020/21 there will be a power shortage of some 5,000 MW.

The country’s frequent brownouts and blackouts, and an expected increase in electricity shortages, do not bode well for an increase in refining capacity. Already less than 10 per cent of the DRC’s 70 million people have access to power, and mining companies are scaling back production and expansion plans because of power shortages.

The news of the DRC’s impending export ban comes as the country is reviewing its mining code – the government is going to overhaul mining laws with an eye to boosting state revenues by increasing tax rates and raising the government’s minimum automatic stake in mining projects, proposals include:

- Enlarge governments stake from five percent to 35 percent in projects, the 35 percent would be “free and non dilutable”

- Increase royalties to gain greater state revenues from the sector

- Introduce a 50 percent levy, a windfall-profit tax, on miners’ “super profits” – when a commodity’s price rises over 25 percent compared with its level at the time of the project’s feasibility study

- Scale back the length of exploration permits to three years, from the four and five year permits available under the current code

- Exploitation phase of mining licenses to be reduced to 25 years from 30 years

- Companies be required to sign written commitments to protect the environment and help local communities

- Pay a capital-gains tax in the event of a takeover

- Projects, after production start, may no longer benefit from preferential customs rates on imports destined for use in mining

According to an Internal Displacement Monitoring Centre (IDMC) report from May 2013. “There were more highly violent conflicts in Africa in 2012 than at any time since 1945.”

The Democratic Republic of the Congo (DRC) – previously known as Zaire – is no exception to the violence flaring in many parts of Africa.

According to IDMC’s report, armed conflict in the eastern part of the Congo intensified “dramatically” during 2012. The increase in fighting drove up the number of displaced people to record levels – there are more than 2.6 million internally displaced people (IDPs) in the country.

Traditionally the DRC’s North and South Kivu regions have been the main areas of extreme turbulence over the past decades. The mineral resources contained in these provinces have provided a steady source of wealth/funding for the various factions claiming its mines.

The hugely mineral rich copper belt region of the DRC, the Congo’s Katanga Province, has also been producing industrial metals such as copper and cobalt for decades, historically the region has been very quiet and not been caught up in the vicious conflicts in Congo’s North and South Kivu.

Unfortunately conditions have deteriorated sharply in the eastern provinces, including Katanga. Very recently, hundreds of insurgents belonging to the Mai Mai Kata Katanga (“cut out Katanga” in Swahili) militia – one of several local militias operating in the province – clashed with security forces in the streets of Katanga’s capital city Lubumbashi. According to the United Nations at least 35 people were killed. The attack was the largest in the province of Katanga in more than a decade. The transport of minerals was interrupted and authorities imposed a nighttime curfew in Lubumbashi.

The DRC holds two major distinctions:

- It is the richest country in the world in terms of mineral wealth, at an estimated $24 trillion.

- It is the country in which the highest number of people – estimates go as high as ten million – have died due to war since World War II.

Cobalt is a strategic and critical metal used in many diverse industrial and military applications.

The growing political risk and socio-economic dissension within the DRC are creating mounting concern for the security of cobalt’s global supply chain.

“The Democratic Republic of Congo faces what is probably the most daunting infrastructure challenge on the African continent”. World Bank report on DRC Infrastructure

Jim Rogers is well known as ‘The Commodities King’, he co-founded the legendary Quantum Fund with George Soros and authored two highly respected investing books – Investment Biker& Adventure Capitalist. Mr. Rogers is very bullish on investing in Russia having been quoted in numerous publications as saying Russia’s leader, president Vladimir Putin, wants to shake his thug KGB image and Russia stacks up as a good contrarian play.

Well I’m not in the habit of investing on anybody’s say so. I do my own due diligence, make my own decisions and take full responsibility for being right AND wrong.

BUT

I have to agree with Mr. Rogers in that I believe Russia has at least one good investment, one for strategic and critical metals (including cobalt) hungry resource junior investors.

The company’s name is Global Cobalt Corp. TSX.V: GCO and it has recently started trading after a considerable halt, amazing project acquisitions, and a name change from Puget Ventures.

Global Cobalt is going to fast-track development of its world-class Karakul Cobalt Project in the Altai Republic of Russia’s southern Siberia. Having historic Soviet C1+C2 resources estimated at 14.98 million tonnes of 0.28% cobalt equivalent Co eq. (0.21% cobalt Co; 0.09% bismuth Bi, 0.44% copper Cu and 0.11% tungsten WO2) with additional P1 resources of 46 million tonnes containing 82,800 tonnes of cobalt – all non NI 43-101 compliant – the Karakul Project has the potential of being the largest known primary cobalt asset outside of Africa.

Global Cobalt also plans to bring on stream a solid pipeline of other strategic and critical metal projects creating a mining district with enormous potential.

Four additional assets, collectively known as the Altai Sister Properties (cobalt-tungsten), have been optioned for acquisition by Global Cobalt. The proximity of the Sister properties to the Karakul Cobalt Deposit adds the possibility of an extension to the main ore bodies providing significant upside to the creation of a new mining jurisdiction in Altai.

Global Cobalt Corp., with its highly qualified management team has the exploration, development and production expertise to enable timely, skilled development of their impressive asset portfolio.

Global Cobalt is the first mover into a new mining region, the mineral rich, pro-mining Altai Republic of Russia’s southern Siberia. GCO is the pioneer, the first foreign, investable, publicly traded mining company to advance the mineral resources in the entire region.

And that’s the investment opportunity, investors get to position themselves at the forefront of a move into an immense, resource rich untapped region, much like what happened with early movers into Mongolia and Kazakhstan.

Global Cobalt Corp. TSX.V: GCO should be on all our radar screens. It’s definitely on mine, is it on yours?

If not, it should be.

Richard (Rick) Mills

Richard is the owner of Aheadoftheherd.com and invests in the junior resource/bio-tech sectors. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, ninemsn, ibtimes, businessweek.com and the Association of Mining Analysts.

If you’re interested in learning more about the junior resource and bio-med sectors, and quality individual company’s within these sectors, please come and visit us atwww.aheadoftheherd.com

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard does not own shares of Global Cobalt Corp. TSX.V: GCO

Global Cobalt is a paid advertiser on Richard’s site, aheadoftheherd.com

The markets in the US have entered a mania in which investors look for any and all excuses to push the markets higher.

Case in point, yesterday Japan’s Nikkei fell 6%. This happened in spite of the fact the Bank of Japan is currently engaged in a QE policy equal to over 25% of Japan’s economy.

And yet, despite this collapse (and the obvious implications for other markets that are being juiced by QE… namely the US), traders pushed stocks higher because once again, the Fed’s mouthpiece at the Wall Street Journal, Jon Hilsenrath, published a story about the Fed not wanting higher rates (which they took to mean the Fed willnot taper QE).

As a result, the S&P 500 bounced off its 50-day exponential moving average, which has become the line to defend for the bulls (see the chart below). When we break this line, the dam breaks…

The key question here is: what exactly is the Fed planning on doing?

Earlier this year, rumors abounded that Hilsenrath might publish an article on the Fed tapering QE. Stocks tanked. Now we get another article from Hilsenrath that the Fed probably won’t taper QE, and stocks rally.

This is the markets we are dealing with: one in which any article published by a man who traders believe is speaking for the Fed will drive the entire market one way or the other. One wonders what would happen if investors ever realized that the Fed actually is just making its policies up on the fly and doesn’t have an exit strategy or worse, could never actually engage in an exit strategy without kicking off another Crash.

For more market insights and investment ideas, visit us at: www.gainspainscapital.com

Best Regards,

Graham Summers

I’ve been warning subscribers of my Private Wealth Advisory newsletter that we were heading for a dark period in the stock market. We’ve since taken action to insure that when the market falls, we make money.

Indeed, in the last month alone we’ve seen gains of 8%, 12%, 21%, and 28%… all from basic stocks and bonds. And we’re now preparing with six carefully targeted investments that will pay out when the market falls.

To find out what they are, all you need to do is take out a trial subscription to Private Wealth Advisory. You’ll immediately be given access to the Private Wealth Advisory archives outlining our investment strategies.

You’ll also be given access to FIVE Special Reports (an $800 value) outlining the biggest risks to the financial system as well as the best means of protecting yourself and your loved ones from them.

To take out a trial subscription to Private Wealth Advisory and take action to make sure the coming months are a time of profit, not pain.

Best Regards,

Graham Summers

Nikkei Drops Fast After Bank Of Japan Minutes

After Nikkei futures rose as high as 13,225 earlier (up 6.3% from Thursday’s close), they have taken a sharp turn lower following the release of the minutes from the Bank of Japan’s May 21-22 policy meeting.

Right now, the Nikkei is trading around 12,995, up *only* 4.4%.

….read more HERE including the key paragraphs from the minutes:

Gold cannot be printed or manufactured in contrast to paper currency. That’s why it has kept its value as the ultimate currency over the long term. There can be no “gold war.” However, we often hear about a “currency war.” Sounds familiar — where did we hear this before?

The phrase “currency war” was coined by Brazilian Finance Minister Guido Mantega after the financial crisis of 2008. The idea is that highly indebted nations weaken the value of their currency by cutting interest rates down to zero and printing fiat currency in order to gain trade advantages (cheaper products to export) and to pay lessdebt service on their bonds. Countries compete against each other to achieve a relatively low exchange rate for their own currency. The policy can trigger retaliatory action by other countries that in turn can lead to a general decline in international trade, harming all countries.

Concerns over a currency war prompted the Group of Seven and Group of 20 economies recently to formulize what constitutes appropriate behavior by central banks in influencing currency exchange rates.

Let’s look at some numbers. Global currency reserves have swelled from $1.9 trillion in the year 2000 to a whopping $11.2 trillion by the third quarter of 2012. But most of that gain took place during the past six years with global currency reserves doubling to the current levels from $5.6 trillion at the beginning of 2007. If that is not evidence of the global currency war, then what is? There are two different examples to consider. The first is undeniable evidence of aggressive money printing. The second is an indication of determined stockpiling of the currencies of other countries in order to weaken your own currency.

For a widespread currency war to occur, a large proportion of significant economies must wish to devalue their currencies at once. This has so far only happened during a global economic downturn.

Under normal economic conditions, countries tend to overlook a small rise in the value of their own currency. However, during a time of recession, nations can take umbrage at other countries’ devaluations.

Let’s begin this week’s technical part with the analysis of the US dollar’s long-term chart. (Charts courtesy of http://stockcharts.com.)

When we take a look at the above chart, we can see that the USD Index declined once again this week. Despite that fact, the January breakout was not invalidated. As we see, the index is still above the declining support line, and thus the medium-term outlook remains bullish.

Let’s take a look at the medium-term situation. Has it changed since last week?

Here we can see that the USD Index moved to its medium-term support line (marked with the thin black line), which is currently close to 80.4. It is very possible that this line will pause the decline, at least for a while, and it’s quite possible that it will actually stop it.

The situation remains bullish for the USD Index in the long term and medium term, so let’s check to see if the short-time outlook is the same.

During the last several days, the USD Index declined and moved slightly below the short-term support line. There is a medium-term support line visible on the previous chart that is much more important so the above is actually not a big deal.

The most important factor on the above chart supporting the bullish case is the cyclical turning point, which is very close – about a week away. It is possible that we will see its impact on the dollar next week and this can lead to a bigger pullback or – more likely – the end of the current decline. If we move back in time a bit, we will see similar situation in August and September 2012, which is when the cyclical turning point worked very well after a significant decline.

Additionally, please note that the RSI Indicator is now at the 30 level, which is a classic buying opportunity.

Let’s find out what impact has this decline had on the two most popular precious metals. (click on image or HERE for larger version)

Click to enlarge

In this week’s very long-term gold chart, comments I made last week remain up-to-date:

We are still likely to see declines after the cyclical turning point from this long-term perspective. The turning point should work on a “near to” basis, and declines will likely be seen sooner rather than later (and the bottom is likely weeks away, not months away).

Now let’s take a look at the white metal. (click on image or HERE for larger version)

Click to enlarge

In this week’s very long-term silver chart, not much really happened as prices declined slightly, less than half of 1% overall. The intraday high for the week was lower than last week once again; from this perspective, the declines clearly go on.

No confirmed move has been seen below the level of the 2008 highs, but silver’s price is only slightly above it at this time. It seems that we’ll have another sharp decline once the breakdown below this support level is seen and confirmed.

Summing up, the most important event in the currency market was the further decline of the dollar. Although the decline visible on the USD Index chart has been quite heavy, we have not seen a rally in gold and silver so far this week; they moved lower. Gold’s underperformance has become even more significant this week and I think that this makes the outlook even more bearish for the short term. Although recent declines in silver have been small, the downtrend remains in place. The implications of the aforementioned underperformance are bearish for the precious metals sector.

For the full version of this essay and more, visit Sunshine Profits’ website.

Twitter: @SunshineProfits

Read more: http://www.minyanville.com/trading-and-investing/commodities/articles/Have-Gold-and-Silver-Stopped-Responding/6/14/2013/id/50351#ixzz2WCpG06lK

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair