, “Bullion’s Day in Sun is Long Gone”,

Gold bullion prices touched fresh three-year lows Friday at $1269 an ounce before recovering a little by lunchtime in London, as stocks and commodities also regained some ground after sharp falls yesterday.

Spot silver prices fell as low as $19.41 an ounce, as with gold their lowest level since September 2010, before they too recovered a little, as other commodities also ticked higher while the US Dollar weakened slightly.

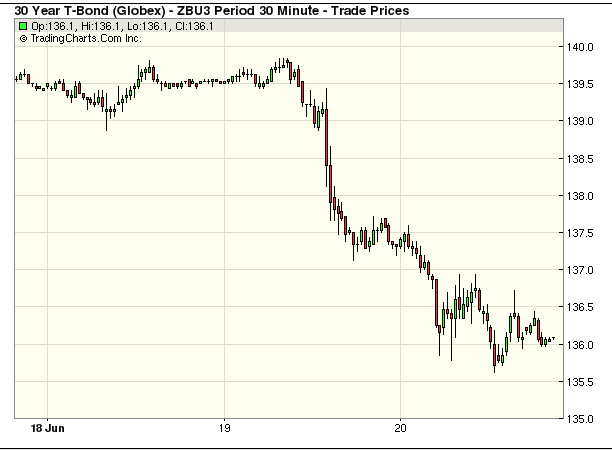

A day earlier, gold fell more than 5% between the London open and US close, while the S&P 500 recorded its biggest daily drop since November 11 2011, with volumes reaching a 2013 high, a day after US Federal Reserve chairman Ben Bernanke said the Fed could begin scaling down its asset purchases “later this year”.

CME Group, which operates the New York Comex exchange on which gold futures are traded, announced yesterday it is increasing margin requirements on gold trading by 25% to $8800 per 100-ounce contract. The new initial margin requirement will come into effect after close of trading today.

“That is definitely affecting gold,” says Joyce Liu, investment analyst at Phillip Futures in Singapore.

“For those who cannot put out margin calls on time, they will be squeezed out even when they don’t want to get out.”

Heading into the weekend, gold in Dollars was down 7% on the week by late morning in London, with silver down 10%.

Gold in Sterling meantime looks set for a drop of more than 5% on the week, trading below £840 an ounce. Gold in Euros was down around 6% on the week at €982 an ounce.

Going by London Fix prices, gold in Dollars looks set for its worst week since April, although a fix price of $1273 an ounce or below would make for the worst week since at least October 2008.

“In the precious metals markets, nothing is simple and now we are at the lows, market sentiment is needless to say very negative,” says David Govett, head of precious metals at broker Marex Spectron.

“I am now hearing from people how a thousand Dollars is the next stop. These are the same people who were predicting two thousand Dollars this year, so I take it all with a pinch of salt. However, there is no doubt that the bull market in gold has had its back broken and its day in the sun is long gone.”

Over in India, traditionally the world’s biggest source of private gold demand, financial services firm Reliance Capital has suspended sales of gold. The Reliance Gold Savings Fund had assets equivalent to eight tonnes of gold under management at the end of the first quarter, newswire Reuters reports. Indian imports last month amounted to 162 tonnes, according to the country’s finance ministry.

The announcement follows the introduction by India’s authorities of new measures aimed at curbing gold imports, such as restricting imports on consignment and raising duties to 8%. The objective is to reduce India’s current account deficit and thus support its currency.

The Rupee however touched an all-time low of Rs.60 to the Dollar Thursday, as the Dollar strengthened and emerging market assets sold off following the Fed’s announcement.

“We are not insulated from what is happening in the rest of the world,” India’s finance minister P. Chidambaram told a press conference in response to the Rupee’s fall.

“My request is we should not react and panic. It is happening around the world.”

In contrast with Reliance, jeweler Shree Ganesh, which in recent years has imported around 70 tonnes of gold a year, said earlier this week that it plans to issue short-term debt to fund bullion imports now that the rules prevent it from obtaining credit from suppliers shipping the gold on a consignment basis.

Indian gold demand usually drops during the summer months during the period known as Chaturmas.

Ben Traynor

BullionVault

Gold value calculator | Buy gold online at live prices

Editor of Gold News, the analysis and investment research site from world-leading gold ownership service BullionVault, Ben Traynor was formerly editor of the Fleet Street Letter, the UK’s longest-running investment letter. A Cambridge economics graduate, he is a professional writer and editor with a specialist interest in monetary economics. Ben can be found on Google+

(c) BullionVault 2013

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

Bill Gross, the co-manager ot the 2 Trillion dollar Pimco Bond fund, is one man whose interpretation of what Ben Bernanke had to say yesterday is worth listening to.

Bill Gross, the co-manager ot the 2 Trillion dollar Pimco Bond fund, is one man whose interpretation of what Ben Bernanke had to say yesterday is worth listening to.