Gold & Precious Metals

Millions of investors are soon going to learn about the financial markets the hard way — through giant losses.

Why? Because they’re confusing normal times with abnormal times.

Let me explain. In normal times, rapidly rising interest rates and Fed credit tightening would typically be bearish for commodities and stocks.

But these aren’t normal times. We’re coming out of a period with the lowest interest rates in the history of the country. A period that was fraught with financial failures, even the near-total collapse of the monetary system. And a period when the Fed deliberately kept interest rates at record lows.

Thing is, most investors aren’t making the appropriate distinction. They’re reacting in a knee-jerk fashion to the recent rise in interest rates. So they’re dumping gold and other commodities, and unloading stocks as if a giant bear is back on the scene.

But based on all of my research and long-term indicators, I’ve concluded that those same investors are going to be very sorry.

Why? Because this rise in interest rates, occurring during abnormal times, is going to have precisely the opposite effect. Instead of being bearish, it’s going to be resoundingly bullish for a lot of markets.

Simple logic explains why.

First, rates were at record lows because almost nobody wanted to borrow. The demand for credit simply wasn’t there.

First, rates were at record lows because almost nobody wanted to borrow. The demand for credit simply wasn’t there.

So as rates and the cost of money and credit rises, guess what happens? Demand goes up too. Potential homeowners and businesses will want to suddenly borrow again before interest rates go any higher. And that, in turn, will stoke all sorts of demand, from housing, to commodities, juicing corporate earnings and the stock market.

Second, interest rates are way below the true rate of inflation, which is running north of about 8%. In other words, we would need rates to move higher than the true rate of inflation ? higher than 8% ? to negatively impact any markets. Until that point comes, if at all, rising interest rates will actually become fuel for higher prices, once the knee-jerk selling has passed.

Third, there will come a time in the not-too-distant future when our foreign creditors start to sell U.S. sovereign debt as they lose confidence in our government’s ability to manage its affairs.

The resulting rise in interest rates will be very bullish for most markets, as money leaves the bond market in droves and seeks out alternative investments for appreciation and safety.

So you see, right now millions of investors are selling everything from gold to stocks because they think we’re in normal times, or approaching normal times.

But these are abnormal times. So you simply can’t apply the old rules.

You have to think out of the box, or you’re going to get buried in the box with a whole lot of losses and missed opportunities. And that’s not what I want for you.

Instead, I believe what’s going on now in the markets is a huge gift for savvy investors. For the following reasons:

- It’s helping gold slide into what should prove to be a major low. Ditto for silver. .

- It’s helping the dollar rally. A rally that will, in turn, be aided by Europe’s coming demise. That, in turn, will eventually lead to a huge opportunity to short the dollar, because, ultimately, its long-term bear market will resume, offering you enormous profit opportunities.

- It will eventually drive huge amounts of money into gold. Other commodities as well.

Right now, though, the selling can continue. So don’t be afraid to make hay with it in the short-term.

For instance, if you’ve followed my suggestions in this column, then you’re short stocks via the ProShares UltraPro Short S&P 500 (SPXU) and you’re long the dollar via the PowerShares DB US Dollar Bull (UUP). Hold those positions.

As to gold and silver, I’m loving that they are falling now. Why? Because the declines are setting up one of the greatest buying opportunities of all time.

Best wishes,

Larry

i see further downside not because of the fed statements, but because like always they hedged their bets in the sense that the tapering off would not necessarily stop mr. bernanke said if the economy does not improve along the lines that we expect, we will provide additional support. so i think the markets are worried about something else. first of all, interest rates have been rising now for a year. the ten-year treasury note and 30-year treasury bond yield bottomed out last july. so we’ve been in an uptrend in interest rates. then, as i maintained for a long time, the chinese economy is much weaker than the official statistics suggest. my view would be that at the present time the chinese economy at the very best, the very best, is growing at something like four percent per an um and without a huge cred expansion there would be no growth at all. the other emerging economies are essential flat.

i see further downside not because of the fed statements, but because like always they hedged their bets in the sense that the tapering off would not necessarily stop mr. bernanke said if the economy does not improve along the lines that we expect, we will provide additional support. so i think the markets are worried about something else. first of all, interest rates have been rising now for a year. the ten-year treasury note and 30-year treasury bond yield bottomed out last july. so we’ve been in an uptrend in interest rates. then, as i maintained for a long time, the chinese economy is much weaker than the official statistics suggest. my view would be that at the present time the chinese economy at the very best, the very best, is growing at something like four percent per an um and without a huge cred expansion there would be no growth at all. the other emerging economies are essential flat.

Our recent calls for a bottom have been proven wrong as precious metals plunged to another new low. Two trading rules we have is to always use a 20% stop and never add to a losing position. Note our previous article in which we said use the late May low for a stop. This helps minimize risk and potential losses, though we have a handful of small losses trying to anticipate the coming rebound. We always admit mistakes to subscribers and we never blame manipulation. That is just unprofessional. All being said, a close examination of history tells us that this could be the final capitulation that would lead directly to a huge rebound in the ensuing months.

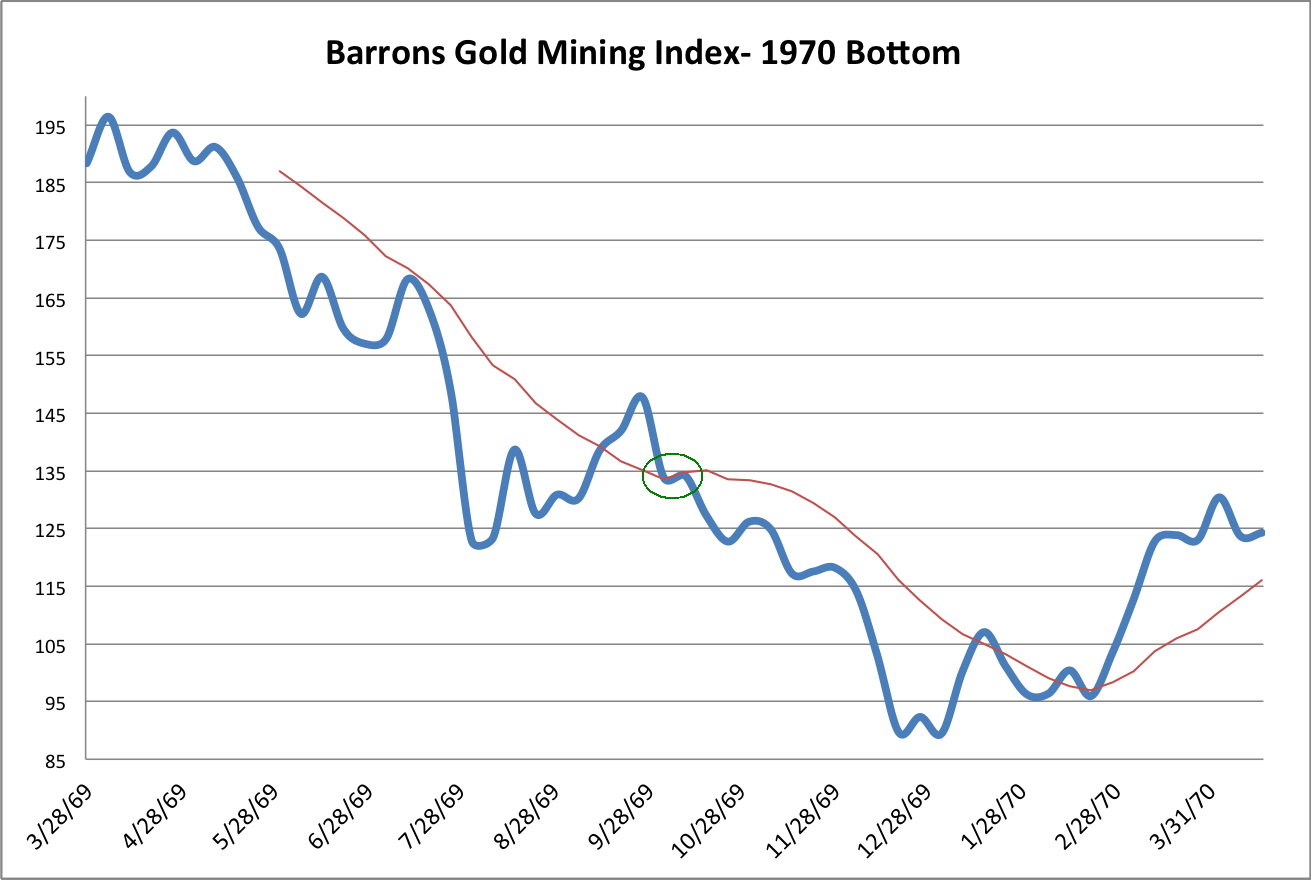

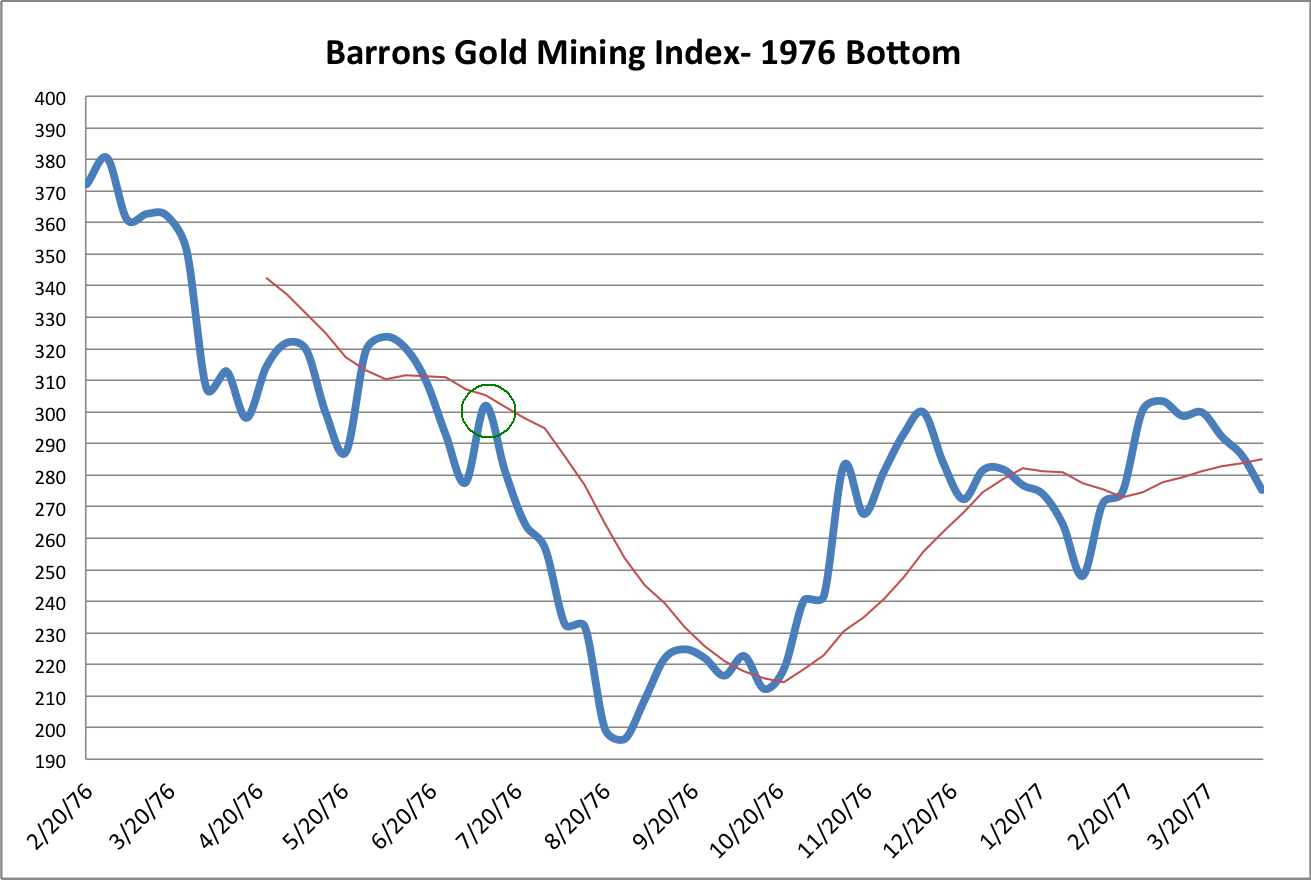

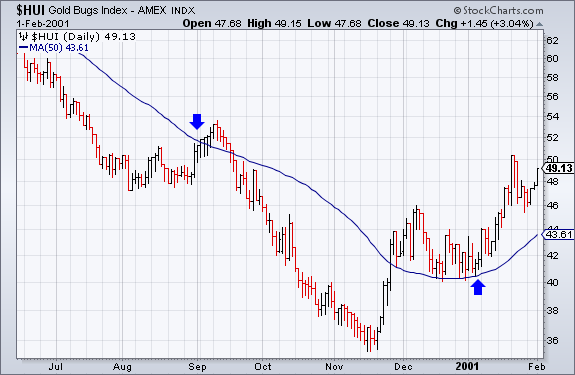

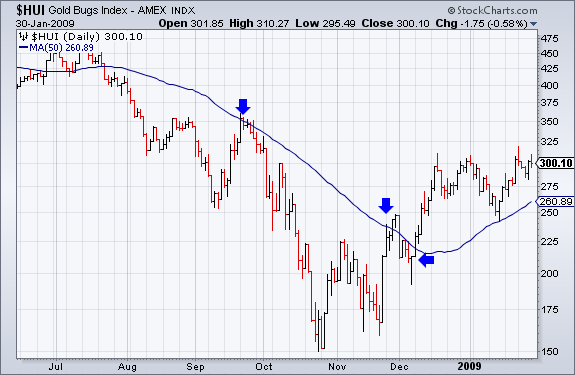

Below we plot the four major downturns within the two secular bull markets in gold stocks. The HUI is now down 64% since 2011 and just surpassed by inches (in time and price) the 1968-1970 downturn. The Barron’s Gold Mining Index (BGMI) lost 67% from 1974-1976 before rising nearly 700% over the next four years.

A 67% downturn would take the HUI down to 210. Interestingly, Fibonacci analysis shows that 210 lines up exactly with the HUI’s 2012 low and 2011 high. So 210 is a target to keep in mind. The GDX equivalent is $21.64.

It’s important to note the 50-day moving average (or the 10-week moving average) as it plays a very important role in how gold stock bottoms evolve. Note that the HUI failed at the 50-day moving average at 283 and has already fallen to 228. Keep that in mind as we go over some important history.

Several months before the bottom at the start of 1970, the BGMI failed at the 10-week moving average. See the circle. From that point, the BGMI declined about 33% to its final bottom.

The BGMI failed at the 10-week moving average in summer of 1976. It declined about 35% to its final bottom.

In September 2000, the HUI rallied above its 50-day moving average but eventually about 35% down to its final bottom.

In September 2008, the HUI failed at its 50-day moving average. It then declined a whopping 57% before hitting its final bottom.

In three of the four cases, the market (after failing at the moving average) declined 33%-35% to its final bottom. At present, the HUI peaked at the moving average at 283. Note that at the recent failure of the 50-day moving average, the market was far more oversold than it was at that specific point in the four historical examples. Thus, we shouldn’t expect the same type of downturn. My downside target of 210 would mark a 26% decline from 283. It’s not 33%-35% but it is substantial.

If you take another look at the four charts, you’ll notice that the moving average plays a key role following the bottom. It provides initial resistance but once it gives way, the recovery begins in earnest. In the chart below we plot the paths of the recoveries that followed the four major bottoms discussed above. It’s not unreasonable to anticipate a 50% rebound in a four month period. In only four months the gold stocks rebounded 85% (starting in Q4 2008) and 60% (starting in Q4 2000).

Gold is a speculative asset that is prone to big declines even in a secular bull market. When inflation is falling and the stock market is performing well, precious metals can really tumble. This is what occurred from 1975 to 1976 and during the last two years. Meanwhile, loose monetary policy and debt monetization since 2008 has already been factored in. Gold ran from $700 to $1900 and Silver surged almost 6-fold. Junior exploration companies went from pennies and dimes to $2 and $5. Junior producers went up 10-fold and more.

The cyclical bear market began with precious metals reaching very overbought conditions as noted above. Fundamentals slowly deteriorated as price inflation declined and Chindia (crucial for metals demand) slowed down economically. Global fear subsided. QE 3 was factored in but didn’t have a sustained impact above and beyond the aforementioned bearish factors. Furthermore, a major technical breakdown intensified the bear market.

Currently, the precious metals complex is plunging but should find a bottom sooner rather than later. A catalyst is definitely needed for the complex to sustain a bottom. Twelve months from now we could see tremendous support for precious metals. The smartest guys are talking about the Fed doing more and not less. By smartest guys I’m talking about folks like Jeff Gundlach and John Brynjolfsson and not fanatical gold bugs. China will have to take action at somepoint to prevent a full blown credit collapse and deflationary spiral. The ECB is talking about pursuing unconventional measures and Mark Carney, the new chair at the BOE, would like to take more action. Does this sound like a bearish recipe for precious metals over the coming quarters?

It’s been a tough road for precious metals but the path ahead has strong potential of being significantly profitable and in a short period of time. The buying opportunity that we’ve spoken of for months could be days away. When precious metals equities rebound, they rebound violently. If you’d be interested in our analysis on the companies poised to recover now and lead the next bull market, we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Signs Of The Times

“Fed’s Fisher: We Cannot Live in Fear of ‘Monetary Cocaine'”

– CNBC, June 5

“We increase our year-end target for the S&P to 1,730 (from 1,640) and introduce an end-2014 target of 1,900.”

– Credit Suisse, June 5

What are these guys tripping out on?

“Goldilocks: This Was the Perfect Job Report for The Market.”

– Business Insider, June, 7

Whatever it is, they seem to be smoking it as well.

Ed Note: Notice the name of one of the Cartoonist’s

In the madness of the “Roaring Twenties”, the head of the New York Fed, Ben Strong, wanted to give the stock market a boost. In 1927 he wished to impress a visiting central banker from France and used the term “coupe de whiskey”.

In the madness of the “Roaring Twenties”, the head of the New York Fed, Ben Strong, wanted to give the stock market a boost. In 1927 he wished to impress a visiting central banker from France and used the term “coupe de whiskey”.

Strange that similar boosts did not work during the collapse in the fall of 1929 and in the fall of 2008.

The last time we referred to the “Coupe” in earnest was in November of 2007. Some years ago, Paul McCulley, then at Pimco observed “When the Fed is the bartender, everybody drinks until they fall down.

Then there is the spoilsport:

“Obama: ‘We don’t want to tax all businesses out of business’.”

– CNS, June 10

With his ambition for unlimited government, this should be read as just the industries that interventionists like such as wind turbines and solar power.

Perspective

In the middle of April the scramble to buy risky bonds was another example of “reaching for yield”. That was one compulsion and it was backed up by “Confidence mounts that central banks will prop up debt markets through year end.”

Essentially the best for the bond future was set at the end of April and the best for lower- grade stuff was set in early May. As of this week, the initial whack has been severe enough that establishment is worrying about “disorderly”.

Oooops!

Our May 9th Pivot described the huge issuance of doubtful bonds as the “biggest Garbage Market in history”, and that what “central bankers propose and market forces dispose”.

Noted a number of times was that the bond frenzy was heading for a seasonal reversal in May. That governments were driving the action was discussed and compared to this time in 1998. That was the government tout that spreads in Europe would narrow. Backed by central bankers, LTCM bet the farm on “Convergence” and the crash was monumental. This disquieting event was also cited a few times.

On this spring’s mania, we noted that once the reversal was accomplished around May, lower-grade bond markets would crash in the fall. “Disorderly” is the polite term for a bond market crash.

There could be times when liquidity pressures will encompass long treasuries. Under such conditions most equities and commodities could suffer forced selling.

Indicators

The storm in the credit markets has been developing over the past few months. Perhaps a pause is due, but the turn is severe and points to a lot of forced liquidation in the fall.

On the stock market, the VIX rising though 19 would mark the breakout from complacency.

On currencies, the DX rising through the 84 level would do it. As a general indicator, the gold/silver ratio rising above 63 would be significant.

Precious Metals

Orthodox markets recorded enthusiasm, excitement and complacency only seen at important tops.

A four-year credit, business and stock market cycle is virtually complete.

In retrospect, the bear market for the precious metal sector started in the summer of 2011. The disaster in March-April created momentum and sentiment readings quite the opposite of the excesses recorded in 2011 and again last September.

That was a trip from one excess to the other. But beyond that it was a cyclical bear market for the sector as orthodox markets were accomplishing a cyclical bull market.

From time to time over the past year this page has wondered about when this opposite action would begin, Well, it was on, but we only noticed it earlier in the year.

Gold markets have recorded bearish sentiment and momentum numbers, gloom and dismay seen only at important bottoms.

The path to a cyclical bull market for this sector could still be difficult. Particularly when stocks and bonds are getting hit hard. At other times good advances are possible with eventually outstanding net gains being accomplished.

We would like to be more precise on this, but it is wild out there.

Mother Nature is seriously working to embarrass interventionist theories and practices – again.

The sector is worth buying on the bad days.

Link to June 15, 2013 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2013/06/this-week-in-money-88/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair