Gold & Precious Metals

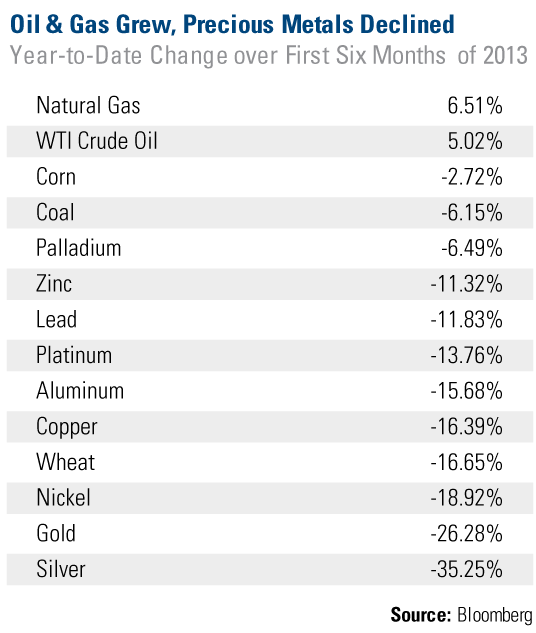

It was a challenging first half of the year for most commodities, with only two resources we track on our Periodic Table of Commodities Returns rising in value. Natural gas and oil rose 6.5 percent and 5 percent, respectively, while silver lost a third of its value and gold lost a quarter of its price from the beginning of the year.

At first glance, the correction seems to support naysayers who believe the supercycle in commodities has ended, such as Credit Suisse analysts, who had declared that the “era is over,” in its digital magazine, The Financialist.

We disagree. Instead, we see severe price declines as possible buying opportunities during this ongoing commodity supercycle.

Consider the extreme pessimism on gold. As one measure of how bears have ganged up against the yellow metal, take a look at the spike in the level of short positions on the precious metal since the beginning of the year. As of the beginning of July, the number of outstanding gold short contracts was close to 140,000!

In June, while I was on CNBC’s Squawk Box, Howard Ward, the chief investment officer of GAMCO Investors, made a bullish call based on the severity of the speculative short position:

“It was off the charts, just like it was a week ago for the short position and the yen, the pound and euro. Well, we’ve seen what happened to that. You wanted to be on the other side of that trade. I’ll take the other side of the gold trade as well. Whenever so many people are on one side, I will take the other side. I think gold probably rallies between here and the end of the year.”

There is certainly a pervasive sense of doom and gloom not only for gold, but for the entire resources space. BCA Research’s Commodity & Energy Strategy report points to a recent Bank of America-Merrill Lynch fund manager survey, which shows that exposure to commodities is as low as it was at the end of 2008. The firm’s first-hand experience reveals a similar investor reaction to resources: “Recent client visits to Europe, Australia and Asia confirm widespread pessimism towards the outlook for ‘anything outside the U.S.,’” says BCA.

This is all music to a contrarian’s ears because it’s another sign of a bottom, but BCA advises taking a “patient approach to front-running the eventual cyclical rally in commodities.” It’s all about your time horizon, says the firm.

Supercycles are not short-term; rather, they are long, continuous waves of boom and bust that can last several decades. While the overall trend is up, there are often short-term bursts of volatility. And looking over the next decade or so, the trends driving the current commodity supercycle remain in place.

I recently read an insightful report on the subject from ETF Securities. In it, analysts highlight two primary long-term drivers.

One entails the urbanization and industrialization trends that are “resource-intensive,” specifically, those found in emerging markets with large populations. Take their energy use, for example, which is “only a fraction of the developed world equivalent,” says ETF Securities. Developed markets, including Australia, France, Germany, Japan and the U.S., all have a higher GDP per capita as well as greater energy use than the emerging markets of Brazil, India, Mexico and China. These countries have significantly large populations, and “a relatively modest rise in per capita energy use will transform into a large absolute increase in global energy use.”

According to ExxonMobil’s 2013 “Outlook for Energy” report, the energy demand in developing nations “will rise 65 percent by 2040 compared to 2010, reflecting growing prosperity and expanding economies.”

The second driver of the supercycle is the rising cost to produce many commodities, says ETF Securities. I’ve discussed on numerous occasions the difficulties facing gold miners, which have seen lower grades and a lack of discoveries. This has made mining the yellow metal more expensive. And, as I indicated in a recent post, with a lower gold price, miners are rethinking projects that are too costly.

With many other commodities, resources companies are increasingly facing labor strikes, increased taxes and a backlog of projects that ultimately drive up the cost to mine and produce.

We agree with ETF Securities that the supercycle in commodities is alive and well. We are also in agreement with Credit Suisse when the firm explains that “the prices of individual commodities will no longer rise and fall together as they have for the last five years.” Instead, investors “are going to have to focus on the specific supply and demand dynamics for individual commodities.”

In this environment, an active manager with a wealth of experience can thrive. In our experience, commodity prices can move quickly and an active manager is able to tactically shift assets into areas of opportunity.

So, instead of trying to guess which commodity will outshine all others, we suggest diversifying across all commodities to try to smooth out the inherent volatility. See the approach that the Global Resources Fund (PSPFX) takes here.

And when it comes to gold, my position remains: Maintain a 5 percent weighting in gold bullion and a 5 percent weighting in gold stocks, selling when the price moves up significantly and buying when the opportunity presents itself.

Frank Holmes

website: www.usfunds.com

Want to receive more investing tips? Sign up to receive email updates from Frank Holmes and the rest of the U.S. Global Investors team, follow us on Twitter or like us on Facebook.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. Diversification does not protect an investor from market risks and does not assure a profit.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. Because the Global Resources Fund concentrates its investments in a specific industry, the fund may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries.

Gold futures reversed course to trade sharply lower after rising to a three-week high earlier in Wednesday’s U.S. session.

On the Comex division of the New York Mercantile Exchange, gold futures for August delivery slid 1% to USD1,277.55 per troy ounce in U.S. trading Wednesday after earlier flirting with USD1,300 an ounce.

Traders bid bullion higher earlier in the session after Federal Reserve Chairman Ben Bernanke said the pace of the central bank’s bond purchases are not a “preset course” In prepared remarks released before his testimony to Congress later in the day, Fed Chair Bernanke said the pace of the central bank’s bond purchases are not a “preset course”.

“I emphasize that, because our asset purchases depend on economic and financial developments, they are by no means on a preset course,” Bernanke said.

Bernanke reiterated that the Fed will continue to maintain its accommodative monetary policy for the foreseeable future.

The Fed chief also overtly pointed out that the central bank’s USD85 billion-a-month bond-buying program will in fact be tapered later this year and perhaps ended outright by the middle of 2014. Easing programs are seen as destructive currencies, which in turn boosts dollar-denominated commodities such as gold.

Elsewhere, Comex silver for September delivery plunged 2.47% to USD19.443 per ounce while copper for September delivery shed 1.76% to USD3.130 per ounce.

Background

Let me start by stating that I am a gold and silver bull and that the precious metals sector has been very good to me. However, any stock or commodity doesn’t not go up or down in a straight uninterrupted line. There are bear phases in a bull market just as there are bullish rallies in a bear market. Gold prices are in a long term bull market despite being in a bear phase at the moment. With that being our starting point then being short rather than long in the near term, makes sense to me.

As retail investors we should be able to change and implement a new strategy all in one day. This is not so easy to do for the bigger players who hold sizeable stakes in some mining companies, but this should not be a stumbling block for retail investors. We have the advantage of being small enough and therefore nimble enough to recognize change and position ourselves accordingly.

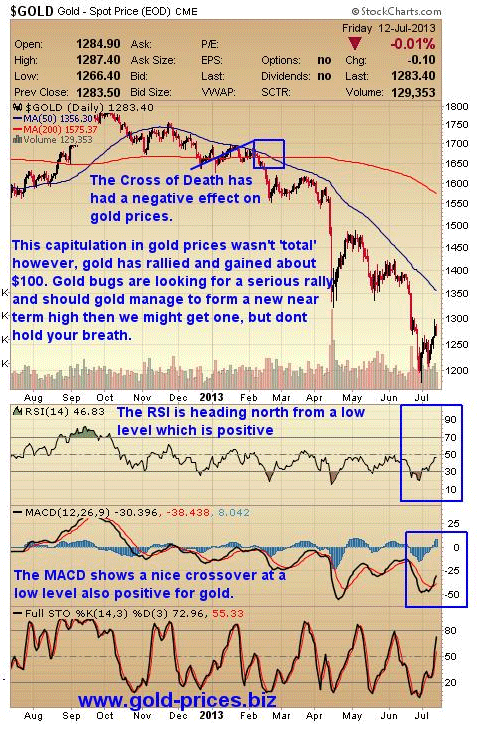

The Gold Chart

This capitulation in gold prices isn’t ‘total’ in that it feels more like death by a thousand cuts than a total wash out of the weak hands. Gold has rallied and gained about $100/oz recently and should gold manage to form a new near term high; get above $1400/oz then we might get a decent rally, but don’t count on it.

The Illusive Ignition

Last week’s fire side chat by Ben Bernanke changed nothing other than to calm the market participants who feared that the punch bowl was about to be drained. The dollar dropped and gold rallied bringing forth a chorus of ‘that’s the bottom in’ from the Perma-Bulls. The point here is that the employment figures are viewed as good enough to justify no further increase in QE and that deprives gold of the oxygen that it needs to rally.

The demand for physical gold continues unabated; however it is not strong enough to overcome the paper market as defined by the COMEX, at least not just yet. The bears have a tight grip of the paper market and until the selling is truly exhausted any rally in the precious metals sector will be capped.

The argument that gold can’t go any lower because this is what it costs to produce it is a strange one; if it were true then we wouldn’t have any bankruptcies as the price wouldn’t go any lower. When the pendulum swings it doesn’t stop at equilibrium, it tends to overshoot the mark and gold is well capable of doing just that. Mining companies will consider their options such as staff layoffs, a wage freeze, shelve expansion programs, spend some of their cash and reduce dividends, etc., in order to keep mining. The bigger operations would need to be moth balled which is an expense in itself. Gold may not go any lower, but it won’t be due to this sort of reasoning as it is flawed.

A resurgence of bank bail-ins in the southern EU countries could cause a few investors to seek refuge in the precious metals sector as the fear grows that their hard earned cash could be confiscated. However, there are many alternatives to cash which an investor can utilize and as gold does not pose a rosy picture at the moment alternatives will be sort.

There is the possibility of social unrest given the high levels of youth unemployment across the Eurozone but they have tolerated the current situation up to now. Although we have had riots from Istanbul to Stockholm, gold prices didnt head higher, they drifted lower.

A Black Swan Event could boost prices; however, by definition this is an unexpected event and can hardly be depended upon as a reason for gold prices to boom.

Conclusion

We are still in a bear phase of this bull market and so we can profit from it if we trade on what we know and not on what we imagine. If you think this bear phase is set to continue then you could consider deploying some of your ‘opportunity cash’ to your change of view. A well thought out strategy involving put options or a few straight out ‘short’ positions could be well worth your consideration.

Ed Note: Read Bob’s later article – Bounce in Gold Is a Dead Cat – Fade The Rally

In 2013 this strategy has served us well and helped us to build cash pile in readiness for the resumption of this bull market or indeed opportunities out with this market sector. This consolidation period may have further to run so we’ll need a fair amount of patience to get through it. However, as investors we can make money whether gold goes up, down or sideways, all we have to do is take the blinkers off and recognize the current situation for it is and not for what we would like it to be.

Back at the ranch our ‘Stock Trader’ service has closed two profitable trades as shown on our trading record so this new venture is finally off the mark.

Take care.

About Gold-Prices.biz

Michael Lewitt is one of my favorite credit analysts. If I want to know what is happening in the credit markets, one of my first calls is to Michael. He has been doing deep dives into some rather esoteric markets as well as traditional bonds over the course of his career, and he really understands what is happening under the surface.

In the latest issue of The Credit Strategist, which Michael has given me special permission to pass on to you as today’s Outside the Box, he gets our attention right off the bat by comparing the recent big move in the benchmark 10-year Treasury yield to a comparable two-month move in 1994, a year that, as he says, was “generally viewed as Armageddon for bond investors.” But in percentage terms, the 1994 move was only 20% over that period while the recent move was 40%.

And what caused that move? Ben Bernanke blinked, that’s all. It’s high time, says Michael, for investors to prepare their portfolios for the eventual termination of the Fed’s monetary fun and games, since:

The comparison between the recent interest rate spike and 1994 underlines just how Fed-dependent markets have become and how incredibly difficult it is going to be for Mr. Bernanke and his colleagues to alter policy without causing serious market dislocations….

Mr. Bernanke is creating the conditions for a violent market reversal. As I wrote last month (“Delusions of Stability”), the dependence of markets on the continued beneficence of the Federal Reserve is profoundly unhealthy.

Then Michael takes us straight into the nitty-gritty of how to put in protection. Read and learn – then act while the acting is good.

You’ll notice that in this issue of The Credit Strategist, in addition to the first-rate macroeconomic analysis, there are sections on equities, credit, currencies, and gold. And it’s this way every month – Michael is comprehensive and he’s astute. You can learn more and subscribe to The Credit Strategist by going to www.thecreditstrategist.com.

I am in Dallas tonight and feeling much better, trying to catch up on my reading as well as some deadlines that slipped while I was sick. I am taking it easy and letting my body recover, though. It is raining in Dallas, and is a cool night with open windows in July. Not sure I remember the last time that happened.

I am looking over the shoulder of my architect/designer and general contractor as the two ladies work on getting my new abode ready. They tell me late October is a real possibility. I am ready. We are trying to find someone to do the work on the media room and all the networking, as it is no longer a simple matter of dropping in a few wall connections. Now, everything talks to everything else. We are looking at systems that let you control everything from a mini-iPad-type device: sound, TVs, lights, screens, security, locks, pretty much everything but the refrigerators. I am seriously open to suggestions from readers who know what I should be looking at installing now and thinking about for the future.

Have a great week, and if someone knows an exec at eBay I would like to talk with them.

Your glad to be back at work analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

The Mirror Cracks

“Life invests itself with inevitable conditions, which the unwise seek to dodge, which one and another brags that he does not know, that they do not touch him; but the brag is on his lips, the conditions are in his soul. If he escapes them in one part they attack him in another more vital part. If he has escaped them in form and in the appearance, it is because he has resisted his life and fled from himself, and the retribution is so much death.”

– Ralph Waldo Emerson

The financial markets have now seen what a world without quantitative easing is going to look like, and they don’t like what they see one bit. In fact, the mere possibility of an end to the Federal Reserve’s monetary experiment sent credit markets to some of their biggest losses in recent history both in absolute and percentage terms. All of these losses were triggered by a move in the benchmark 10-year Treasury yield from a low of 1.63% on May 2 to a high of 2.66% just a few days before ending the quarter at 2.49%. ISI Group has done some great work placing this move in context. In 1994, a year generally viewed as Armageddon for bond investors, the 10-year Treasury only increased by 90 basis points during a comparable 2-month period that started a sustained increase in rates. Moreover, in percentage terms, the 1994 move was only 20% over that period while the current move was 40%.

Conditions today are far different than those in 1994, however; today they are far more conducive to rates staying low. During that period in 1994, the Federal Reserve hiked the Federal Funds rate by 70 basis points (the first leg of a move that would see the Federal Reserve raise rates by another 175 basis points by the end of that year – with 10 year Treasury yields following by another 100 basis points). In contrast, today there is no chance that the Federal Funds rate will be increased for at least the next two years. For another, the Federal Reserve’s balance sheet has already increased by more than $400 billion this year and is expected to increase by another $450-500 billion by year end. So while the Federal Reserve tightened by 250 basis points in 1994, the Federal Reserve’s bond purchases are effectively lowering interest rates on the order of 70 basis points (ISI’s estimate) today. The comparison between the recent interest rate spik e and 1994 underlines just how Fed-dependent markets have become and how incredibly difficult it is going to be for Mr. Bernanke and his colleagues to alter policy without causing serious market dislocations. What investors should learn from this is that they should be preparing their portfolios now for serious – perhaps unprecedented – volatility when the Federal Reserve finally does what it needs to do and stops propping up the markets. Some of us began doing this several months ago and avoided damage to our portfolios in May and June (while still earning decent returns in the interim).

The pain in credit markets was widespread. High yield bonds, which were trading at an oxymoronic yield of 4.8% in early May, closed June at 6.66% after reaching a high of 6.9%. Average bond prices fell about 6 points from a high of 107 in early May and spreads widened by more than 100 basis points. Historically, spreads have contracted when yields have increased, but as with many traditional correlations this one did not hold in an era of unprecedented central bank policy manipulation. This is likely because the duration of high yield portfolios has lengthened as issuers steadily stretched their debt maturities through refinancings. Despite all the talk of the importance of keeping portfolio durations short, many managers succumbed to the temptation to lengthen them as stable credit conditions persisted. The sell-off created some interesting anomalies (i.e. opportunities), including an inversion of high-quality cash curves, a widening of the cash/credit default swap basis, outperformance of high quality loans, and underperformance of high quality high yield bonds. For example, BB-rated bonds performed worse than CCC-rated bonds (the reverse of what has normally happened in the past), while the reverse happened in the loan space. As for credit default swaps, it appears that the use of these instruments by mortgage hedgers to protect their structured portfolios forced single name credit default swap spreads to widen; this has made it more attractive for investors to sell protection rather than own cash bonds in many credits. Before too many observers get too tempted by near 7% yields, however, they should take a deep breath and remind themselves that high yield bonds (and their derivatives) are hybrid debt-equity securities that on averagestill offer far too little reward for the risk involved in owning them. Relative value is not value.

Investors have clearly been shaken. High yield mutual funds and ETFs have reportedly seen $12 billion of outflows over the last five weeks, representing about 7% of their total assets. According to Citigroup, this reversed the total inflows of the past 14 months. Investors in this asset class are nothing if not fickle. Put another way, these assets – at least at the margin, which is what matters in markets – are held by weak hands. There lies the risk … and the opportunity.

By way of comparison, leveraged loans saw their average price drop by less than $1.00 in June; their yields increased by 56 basis points and their spreads widened by only 33 basis points according to J.P. Morgan, demonstrating again why they remain extremely compelling defensive holdings.

Investments that are considered the most conservative (not by me but by the consensus) – municipal and investment grade bonds – were also battered. For example, the iShares S&P National AMT-Free Muni Bond ETF (MUB) sold off from 111.60 on May 1 to a low of 100.28 before recovering to end the month at 105.04 (a loss of 5.88%). The iShares iBoxx Investment Grade Corporate Bond ETF (LQD) saw a loss of 3.56% in June (from $117.85 to $113.65). While significant, these losses should be seen in the context of the significant returns that these asset classes have generated in recent years. Mortgage-backed securities suffered their worst performance since 1994 with a 2% loss in the second quarter. Subprime mortgage bonds also lost 2% during the quarter including a whopping 4.9% drop in June alone. This is hardly surprising in view of the obvious dependence of the mortgage market on the Federal Reserve’s $40 billion monthly bid for paper. These losses may be painful but they are hardly catastrophic as long as they don’t persist.

Some of the best bond investors with the most impressive long-term track records were badly hurt. Bill Gross’s $285 billion Pimco Total Return Bond Fund (PTTRX) lost 2.8% in June (dropping from $11.07 to $10.76) and is down -4.27% for the year (from $11.24 on December 31, 2012), while his colleague Mark Kiesel’s $11 billion Pimco Investment Grade Corporate Bond Fund (PBDAX) lost -4.08% in June (from $11.01 to $10.56) and is down -5.04% for the year (from $11.12 on December 31, 2012). Even Jeffrey Gundlach was taken by surprise by the sudden sell-off in the 10-year Treasury as his DoubleLine Total Return Fund (DLTNX) lost 2.13% in June (from $11.26 to $11.02) and is down -2.38% for the year (from $11.33 at year end). Both Mr. Gross and Mr. Gundlach were apologetic about their performance, but neither man has anything to apologize for in view of their outstanding long-term records. Nonetheless, the fact that two of the market’s greatest long-term perf ormers were unprepared for the market’s reaction to Mr. Bernanke’s words suggests just how deeply embedded Fed-dependency has become in the financial markets. Both men have stated that they believe that Mr. Bernanke’s forecast of 3.0-3.5% GDP growth in 2014 is too optimistic, and both have reiterated their view that Treasuries are attractive at 2.5% (views first stated when Treasuries were at 2% after selling off from their low of just over 1.6% at the beginning of May). I concur with them that the economy is unlikely to grow at better than 3.0% in 2013, but I find nothing remotely compelling about lending to the U.S. government for ten years at 2.5%. Buying 10-year Treasuries as a trade may make sense for the most nimble, but it is difficult to be nimble when managing tens or hundreds of billions of dollars. Investing in Treasuries at their currently artificially depressed yields is playing with fire. It is one of the wonderful ironies of the English language that the word “taper” not only means to “gradually withdraw” but is also a noun used to describe a long, thin candle or a long, waxed wick used to light candles or fires. Perhaps the Princeton economics professor was playing with the market in more ways than people realize when he used that term to describe his future policy moves.

There is little question that markets were overdue for a correction. That is why I advised investors to reduce their equity holdings two months ago and why I have been recommending limiting credit exposure to short duration corporate bonds and floating rate bank loans since the beginning of the year. By April, the most prudent posture was to be hedged against rising interest rate risk and widening spreads. In high yield, there are three risks that have to be addressed at any given time: interest rates, credit and systemic/macroeconomic risk. For the moment, credit risk is well-contained (the default risk is about 3.0% and any capable manager should be able to avoid defaults), so the focus is on hedging rising rates and an equity market correction. It is likely that the 4.8% average yield on high yield bonds reached in early May will prove to be a generational low, just as some believe that the March 2009 S&P 500 level of 666 will serve as a generational low for s tocks. The difference, of course, is that the S&P 500 low was expressing the depths of investor despair while the May 2013 low in yields was the apogee of investor complacency. And while it took only a short time (about six weeks) for high yield investors to be dealt a dose of reality, average yields of under 7% remain far below what is appropriate to reward them adequately for the equity risk inherent in the asset class.

Spreads of about 550 basis points over still shrunken Treasury yields may seem like a reasonable risk premium in historical terms, but it is highly misleading in measuring the true risk of these instruments. First, the prices of all financial assets – including high yield credit – is still being artificially depressed and distorted by years of zero interest rate policy and successive bouts of quantitative easing by the Federal Reserve and other central banks. Second, “spread” is a fixed income measurement tool being applied to a financial instrument – a high yield bond – that shares both fixed income and equity attributes. I often tell investors that high yield bonds are like a child who has inherited the worst attributes of both of his parents. When the bond market sells off, high yield bonds sell off; when stocks sell off, high yield bonds sell off as well! As the ultimate “risk-on” asset class, high yield bonds find any excuse to pile on to the “risk-on” trade and any excuse to run for the hills when the “risk-off” button flashes red. Any equity investor will tell you – or should tell you – that 7% is an inadequate return for taking equity risk (which involves the risk of loss of all or part of your principal).

Ben Bernanke, of course, is trying to lower investors’ threshold regarding the return they require for taking risk, but investors should not be fooled. By doing what he is doing, Mr. Bernanke is actually significantly increasing the systemic and other risks that investors are facing. And for that reason, investors should actually be demanding higher, not lower, real returns on their investments. I realize that last statement is directly contrary to the consensus that argues that the Federal Reserve (and other central banks) have taken the tail risk out of the markets with their extraordinary market interventions. My response to the consensus is that central banks have done nothing of the kind; at best, they have delayed the occurrence of tail risks, but in doing so have guaranteed that the consequences of trail risks will be far more severe when they inevitably materialize. The policies that are being employed to create the appearance of economic and market sta bility are not effectively addressing the underlying symptoms of economic malaise; in fact, they are exacerbating them. Debt is being used to cure a debt crisis in the hope that fiscal policies will be implemented that will foment sufficiently high economic growth to create the income necessary to service and ultimately repay that debt. But even in the best of all possible worlds such an outcome would be a long shot since the sheer amount of debt being generated to keep economies afloat is too large to be serviced or repaid. And as we are all painfully aware, we don’t live in the best of all possible worlds – we live in a world populated by corrupt and narcissistic politicians and business leaders who refuse to effect the necessary fiscal reforms that would at least give monetary policy a chance to work. As a result, the post-crisis world has been left more indebted and more interconnected than the pre-crisis world. The tails may be buried a little deeper than they were, but they are fatter than ever.

Mr. Bernanke is creating the conditions for a violent market reversal. As I wrote last month (“Delusions of Stability”), the dependence of markets on the continued beneficence of the Federal Reserve is profoundly unhealthy. When Mr. Bernanke said that the Federal Reserve expects 2014 growth to clock in at 3-3.5% (too high in my opinion – I expect 2.75-3.0%), and that if this growth comes to pass, the Fed will then begin to taper (which means to reduce gradually, not to stop suddenly) its bond purchases at the end of the year, the market’s reaction was sudden and violent. Yet at the end of the day, the S&P 500 barely lost 5% before Mr. Bernanke sent his minions out into the media to dispel any fears that the Federal Reserve would abandon the markets. Such backpedaling is highly dysfunctional. As David Rosenberg wrote, “I guess the premise is there should never ever be periodic setbacks even for a market that has surged 135% from the c ycle lows. Incredible.” (David Rosenberg, Gluskin Sheff, Breakfast with Dave, June 26, 2013, p. 3.) Mr. Bernanke mentioned at his post-FOMC news conference in June that he was surprised by the rise in interest rates after his May 22 testimony, which suggests that he may not appreciate just how Fed-dependent the financial markets have become since the financial crisis. Now that is really incredible.

Sometimes it seems like our central bankers populate a parallel universe completely detached from the real world of markets. Take their fear of deflation. There is an enormous difference between a debt-induced deflation of the kind we saw during the financial crisis, where massive debt destruction led to systemic stresses, and the type of low consumer inflation (which I don’t believe for a second, but that is a separate conversation) that the Federal Reserve is now obsessing about. As David Rosenberg notes, “as for ‘goods deflation’, what is wrong with consumers being able to buy more eggs, bread and T-shirts with the dollar they earn? This push against deflation is remarkable in its own right – historically, this was the norm and inflation was the hallmark of wartime, and the economy looking back at centuries of data did quite well in this respect, thank you very much.” (David Rosenberg, Gluskin Sheff, Breakfast with Dave , June 26, 2013, p. 3.) Uber-dovish St. Louis Fed President James Bullard not only dissented from the most recent Federal Reserve Open Committee statement (because he thought it was too hawkish), but later stated that the Fed might have to provide more accommodation to protect its inflation goal. In view of the trillions of dollars of direct and indirect accommodation that has already been provided, the gross distortion of the value of all financial assets (even after the recent minor correction), and the long-term risks of such an unprecedented policy, it would not be inappropriate to consider Mr. Bullard’s stance a form of lunacy. The United States is hardly at risk of experiencing a deflationary spiral downward in consumer prices, and the Federal Reserve’s focus on deflation is profoundly misguided.

Equities

The hysteria over a 5% correction suggests that the only thing that matters for stock market investors is what the Federal Reserve says and does (or doesn’t do). I believe that Ben Bernanke was trying to take some air out of the financial markets, including both stocks and bonds, with his cautionary comments about the possibility of the Federal Reserve tapering its bond purchases by year end if economic growth meets his expectations. Some argue it will happen as soon as September; others that it will not begin until sometime in 2014. Regardless of when it happens, what stock market investors need to be concerned about is the weak support for stock prices above 1600 on the S&P 500 (or above 15,000 on the Dow Jones Industrial Average) without the Federal Reserve’s current level of bond purchases (zero interest rates are here to stay until at least 2015). From that perspective, stocks may be living on borrowed time. Earnings momentum alone is unlikely to sustain stock prices in the next few quarters. Companies warning investors to expect disappointing results outnumbered those promising better results by a 6.5-to-1 margin, the worst ratio since 2001. And analysts are projecting second quarter profits growth of a modest 3%, down from the 8.4% they were expecting in January. Revenue growth, which disappointed in the first quarter, is projected to increase by only 1.8% in the second quarter. GDP growth is stretching to reach 2.0%. At this point, the strongest factor supporting the case for higher stock prices is the 90% correlation between rising stock prices and the growth of the Federal Reserve’s balance sheet. That balance sheet is likely to rise by another $450 billion over the rest of 2013. Investors willing to count on that correlation persisting may be rewarded, but they should limit their holdings to special situations (i.e. stocks where there is an identifiable catalyst to higher value) or those trading at discoun ts to the market’s price/earnings multiple (i.e. value stocks). I would expect growth stocks and dividend stocks to lag as growth struggles and interest rates edge higher over the next 12-18 months.

Credit

Many investors will be tempted to see value in suddenly battered debt instruments of all kinds – munis, investment grade and high yield bonds, mortgage-backed securities. It needs to be pointed out that this is only relative value – in absolute terms, all of these instruments – on an average basis – are still trading at artificially depressed yields as a result of the Federal Reserve’s policies (which, just to be clear, haven’t yet changed and are unlikely to change for at least several months). The fact that so few investors in credit were prepared for the recent sell-off is a classic example of Hyman Minsky’s financial-instability hypothesis whereby stability breeds instability: as stable financial market conditions persisted and extended since 2009, credit investors grew increasingly complacent and added leverage, duration and illiquidity to their portfolios. The correct approach was to do the opposite – as the cycle became more extended, they should have been shortening duration, eliminating leverage and selling their least liquid holdings. They might have been “early” and sacrificed some returns in the short-run, but in the long-run their returns would be much better. At this point, investments should be focused with managers who understood this. In the high yield space, the sell-off has created a new set of opportunities in short duration bonds and loans with low ratings (that overstate their default risk) issued by some of the large buyouts of the mid-2000s (these securities held up extremely well during the sell-off). In general, investments in credit need to be focused on event-driven special situations where there is (like in the equity space) an identifiable catalyst to near-term value realization. Investors do not want long-term exposure to interest rate or macroeconomic risk.

Currencies

I expect the Yen to resume its weakening against the U.S. Dollar and Euro again shortly. Japan remains set on its policy course and will not stop until the Yen trades at much weaker levels (at least 120 to the U.S. Dollar). This should allow the Yen carry trade (properly hedged) to remain attractive for a while longer. For the moment it appears that Japanese Government Bond rates have stopped rising although the possibility remains that the Bank of Japan could lose control over the long end of the curve at any time. The Euro continues to maintain its strength as the region’s economies wither on the vine, but there is no reason to believe that the currency’s strength will persist forever (although every time I recommend that investors stay short the euro, Keynes’ words “in the long run we are all dead” run through my head). Europe is still a mess and little is being done to fix it. Interestingly enough, the European Central Bank’s b alance sheet has actually been shrinking over the past year, something that is hardly conducive to economic growth. The fact that the European currency remains above $1.30 in the face of all of these factors has to make this among the most frustrating trades in recent memory. It is also a great example of why financial markets work in practice but not in theory and why investors have to be very careful using leverage when investing in currency markets. All that being said, the Euro will crack sooner or later and I would remain short (without leverage obviously).

Gold

Gold has been decimated in recent weeks, with the spot price closing the quarter at $1,234.57/oz. Gold was down -27% over the first half of the year (-23% in the second quarter), about twice the inverse of the rise in the equity markets. Even as a hedge, therefore, gold didn’t work. I would attribute the plunge in gold to several factors. First, a lot of gold was held by leveraged speculators who were forced out of the market as prices dropped. Second, investors who view gold as an inflation hedge are abandoning the trade based on the low level of reported consumer price inflation in the U.S. Third, investors who view gold as a hedge against the inevitable demise of the fiat paper standard are coming to believe – wrongly in my view – that central banks are going to change their ways. For all of these reasons, gold is back to levels last seen in 2010.

Gold remains an insurance policy against the inevitable decline of the fiat paper standard. There is far too much debt in the world that can never be repaid in constant dollars. This debt can only be repaid in one of three ways: (1) partially, which means through defaults and restructurings (see, for example, Greece, Cyprus); (2) through inflation; and (3) through currency devaluation. The global economy is simply incapable of generating sufficient income to service and then repay the trillions of dollars of debt on the balance sheets of the central banks not to mention all of the other public and private sector debt, nor the hundreds of trillions of dollars of future entitlement obligations of its governments. In the end, paper money will continue to be devalued and gold will be the beneficiary of that phenomenon. I would be perfectly comfortable adding to gold positions at this level as a long-term trade, and would strongly advise investors who do so to purchase phy sical gold.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair