Stocks & Equities

Reaction to earnings, hotel business driving market enthusiasm

Priceline.com Inc. surged closer to the $1,000-a-share milestone Friday, as investors reacted positively to a quarterly report that continued to support the firm’s status as the kingpin of the online-travel agency market.

The company reported a profit of $437 million, or $8.39 a share, on $1.68 billion in revenue. During the same period a year ago, Priceline reported a profit of $352 million, or $6.88 a share, on sales of $1.33 billion.

“The main driver [of growth] has been international,” said Aaron Kessler, of Raymond James. “International is now about 90% of profits, and they have become the leading international online travel agency.”

Priceline’s Booking.com business, which lists more than 335,000 hotels around the world, that is the key source of the company’s performance and why the Priceline’s stock price has risen almost 59% this year, and is up 75% over the past year.

Gold is trading $18 higher at 4pm PST in London Trading @ 1331.40, Silver opens up .50 cents higher and is at the moment of this writing trading over $21.00 @ 21.05. Trading in New York at 4pm PST is somewhat delayed but last quotes at time of writing are 1331.20 and 20.94.

One reason for the increase is the holdings in the biggest bullion-backed exchange-traded product SPDR expanded for the first time since June.

We Can’t Take the Chance

A Few Impossible Things

Thinking About Alternatives

14 Years and Counting

Montana, San Antonio, Chicago, Bismarck, Denver, Toronto, NYC…

What would it have been like to be in the decision-maker’s seat at a central bank in the midst of the crisis in 2008-09? You’d know that you won’t have the luxury of going back and making better decisions five years later. Instead, you have to act on the torrent of information that’s coming at you from every quarter, and none of it is good. Major banks are literally collapsing, the interbank market is almost nonexistent, and there is panic in the air. Perhaps you feel that panic in the pit of your stomach. This week we’ll perform a little thought experiment to see if we can extrapolate what is likely to happen in when the next crisis kicks in.

What would it have been like to be in the decision-maker’s seat at a central bank in the midst of the crisis in 2008-09? You’d know that you won’t have the luxury of going back and making better decisions five years later. Instead, you have to act on the torrent of information that’s coming at you from every quarter, and none of it is good. Major banks are literally collapsing, the interbank market is almost nonexistent, and there is panic in the air. Perhaps you feel that panic in the pit of your stomach. This week we’ll perform a little thought experiment to see if we can extrapolate what is likely to happen in when the next crisis kicks in.

This week’s letter was triggered by a semiformal debate in Maine last week. David Kotok assembled about 50 economists, financial analysts, money managers, and media personalities to share a few days of fabulous food, what turned out to be great fishing, and awesome conversation. There were more Federal Reserve economists this year than in the past, as well as more attendees with the title “Chief Economist” on their business cards, many from large institutional names you would recognize. This was my seventh year to attend “Camp Kotok.” David really did a marvelous job of bringing a diverse group of thinkers together, and I think everyone agreed this was the best conference ever. I learned a lot.

Before we get into the letter, a little side note. Luciana Lopez from Reuters attended for the first time this year and wanted to do interviews. David asked me if I would take her out on the lake in our boat, since most of the other attendees went out in small canoes. Trey and I were glad to share our space. While we were out fishing, she asked if she could interview me. I said “Sure” and waited for her to bring out her recorder. She pulled out an iPhone 5 and started asking questions. Not the usual studio setting I am used to. I had serious trepidations about how this was going to look on-screen.

She sent a link to her edited interviews last Monday, and I have to admit I was impressed at what she could do with a simple iPhone 5. I am supposed to be on top of a changing world, but sometimes these things still take me by surprise. I make no representations about the quality of the content of the interviews, at least my portion of them, but the phone is another matter. And in a few years this will be a $100 consumer item.

In her interviews, Luciana asked two questions: “When will the Fed start to taper?” and “Who will be the next Fed chair?” You can see some of our answers at reut.rs/13if7Er and reut.rs/13gegE8.

We Can’t Take the Chance

On Saturday night David scheduled a formal debate between bond maven Jim Bianco and former Bank of England Monetary Policy Committee member David Blanchflower (everyone at the camp called him Danny). Jim Bianco needs little introduction to longtime readers, but for newbies, he is one of the top bond and interest-rate gurus in the world. His research is some of the best you can get – if you can get your hands on it.

Blanchflower needs a little setup. He is currently a professor at Dartmouth and has one of the more impressive resumés you will find. He is not afraid to be a contrarian and voted in the minority in 18 out of 36 meetings in which he participated as an external member of the Bank of England‘s interest rate-setting Monetary Policy Committee (MPC) from June 2006 to June 2009. (The MPC is the British equivalent of the US Federal Open Market Committee.) Blanchflower’s The Wage Curve, drawing on 8 years of data from 4 million people in 16 countries, argued that the wage curve, which plots wages against unemployment, is negatively sloping, reversing the conclusion from generations of macroeconomic theory. “The Phillips Curve is wrong, it’s as fundamental as that,” Blanchflower has stated. Blanchflower is also known as the “happiness guru” for his work on the economics of happiness. He quantified the relationship between age and happiness and between marriage, sex, and happiness. Who knew that people who have more sex are happier? Well, we all did, but now we have economic proof.

I got to spend a good deal of time with Danny on this trip and enjoyed hearing him talk about what it was like to be responsible for setting monetary policy in the midst of a crisis. We also argued late into the night on a variety of subjects. He is an altogether fun guy as well as a professional who takes his economics seriously. He is far more mainstream than your humble analyst, as were many of the denizens of Camp Kotok. On the other hand, I can’t think of a major stream of economic thought that wasn’t represented aggressively at one point or another. If you have thin skin or weak data, this outing is one you might not enjoy. You need to bring your A game with this crowd.

The format for the debate between Bianco and Blanchflower was simple. The question revolved around Federal Reserve policy and what the Fed should do today. To taper or not to taper? In fact, should they even entertain further quantitative easing? Bianco made the case that quantitative easing has become the problem rather than the solution. Blanchflower argued that quantitative easing is the correct policy. Fairly standard arguments from both sides but well-reasoned and well-presented.

It was during the question-and-answer period that my interest was piqued. Bianco had made a forceful argument that big banks should have been allowed to fail rather than being bailed out. The question from the floor to Danny was, in essence, “What if the Bianco is right? Wouldn’t it have been better to let banks fail and then restructure them in bankruptcy? Wouldn’t we have recovered faster, rather than suffering in the slow-growth, high-unemployment world where we find ourselves now?”

Blanchflower pointed his finger right at Jim and spoke forcefully. “It wasn’t the possibility that he was right that preoccupied us. We couldn’t take the chance that he was wrong. If he was wrong and we did nothing, the world would’ve ended and it would’ve been our fault. We had to act.”

That sentence has stayed with me for the past week: “We couldn’t take the chance that he was wrong.” Whether or not you like the implications of what he said, the simple fact is that he was expressing the reigning paradigm of economic thought in the world of central bankers.

Now, let’s hold that train of thought for a few minutes as we introduce an essay by French geophysicist and complex systems analyst Didier Sornette and his colleague Peter Cauwels. Sornette is Professor on the Chair of Entrepreneurial Risks at the Department of Management Technology and Economics of the Swiss Federal Institute of Technology Zurich. (This introduction comes from work I have been doing in collaboration with Jonathan Tepper, my co-author for Endgame.)

By far the biggest advances in understanding the dynamics of bubbles in recent years have come from Sornette. He has developed mathematical models to explain earthquake activity, Amazon book sales, herding behavior in social networks like Facebook, and even stock market bubbles and crashes. He wrote a book titled Why Stockmarkets Crash. He found that most theories do a very poor job of explaining bubbles.

Sornette found that log-periodic power laws do a good job of describing speculative bubbles, with very few exceptions. Classic bubbles tend to have a parabolic advances with shallow and increasingly frequent corrections. Eventually, you begin to see price spikes at one-day, one-hour, and even ten-minute intervals before crashes.

After a crash, journalists go looking for the cause. They’ll blame something like portfolio insurance for the crash of 1987 or the bankruptcy of Lehman Brothers for the Great Recession, rather than blaming a fundamentally unstable market. Sornette disagrees:

Most approaches to explain crashes search for possible mechanisms or effects that operate at very short time scales (hours, days or weeks at most). We propose here a radically different view: the underlying cause of the crash must be searched months and years before it, in the progressive increasing build-up of market cooperativity or effective interactions between investors, often translated into accelerating ascent of the market price (the bubble). According to this “critical” point of view, the specific manner by which prices collapsed is not the most important problem: a crash occurs because the market has entered an unstable phase and any small disturbance or process may have triggered the instability. Think of a ruler held up vertically on your finger: this very unstable position will lead eventually to its collapse, as a result of a small (or absence of adequate) motion of your hand…. The collapse is fundamentally due to the unstable position; the instantaneous cause of the collapse is secondary. In the same vein, the growth of the sensitivity and the growing instability of the market close to such a critical point might explain why attempts to unravel the local origin of the crash have been so diverse. Essentially, anything would work once the system is ripe.

Sornette’s conclusion is that a fundamentally unstable economic system plus human greed means that market bubbles and crashes won’t disappear anytime soon.”

A Few Impossible Things

I want to focus on the recent paper Sornette wrote with Cauwels, entitled “The Illusion of the Perpetual Money Machine.” I’m going to quote a few paragraphs from the introduction. They begin with that marvelous exchange from Alice in Wonderland:

There is no use trying,” said Alice. “One can’t believe impossible things.”

“I daresay you haven’t had much practice,” said the Queen. “When I was your age, I always did it for half an hour a day. Why, sometimes I’ve believed as many as six impossible things before breakfast.”

– Lewis Carroll

Chasing fantasies is not the exclusive pastime of little girls in fairy tales. History is speckled with colorful stories of distinguished scientists and highly motivated inventors pursuing the holy grail of technology: the construction of a perpetual motion machine. These are stories of eccentric boys with flashy toys, dreaming of the fame and wealth that would reward the invention of the ultimate gizmo, a machine that can operate without depleting any power source, thereby solving forever our energy problems. In the mid-1800s, thermodynamics provided the formal basis on what common sense informs us: it is not possible to create energy out of nothing. It can be extracted from wood, gas, oil or even human work as was done for most of human history, but there are no inexhaustible sources.

What about wealth? Can it be created out of thin air? Surely, a central bank can print crispy banknotes and, by means of the modern electronic equivalent, easily add another zero to its balance sheet. But what is the deeper meaning of this money creation? Does it create real value? Common sense and Austrian economists in particular would argue that money creation outpacing real demand is a recipe for inflation. In this piece, we show that the question is much more subtle and interesting, especially for understanding the extraordinary developments since 2007. While it is true that, like energy, wealth cannot be created out of thin air, there is a fundamental difference: whereas the belief of some marginal scientists in a perpetual motion machine had essentially no impact, its financial equivalent has been the hidden cause behind the current economic impasse.

The Czech economist Tomáš Sedláček argues that, while we can understand old economic thinking from ancient myths, we can also learn a lot about contemporary myths from modern economic thinking. A case in point is the myth, developed in the last thirty years, of an eternal economic growth, based in financial innovations, rather than on real productivity gains strongly rooted in better management, improved design, and fueled by innovation and creativity. This has created an illusion that value can be extracted out of nothing; the mythical story of the perpetual money machine, dreamed up before breakfast.

To put things in perspective, we have to go back to the post-WWII era. It was characterized by 25 years of reconstruction and a third industrial revolution, which introduced computers, robots and the Internet. New infrastructure, innovation and technology led to a continuous increase in productivity. In that period, the financial sphere grew in balance with the real economy. In the 1970s, when the Bretton Woods system was terminated and the oil and inflation shocks hit the markets, business productivity stalled and economic growth became essentially dependent on consumption. Since the 1980s, consumption became increasingly funded by smaller savings, booming financial profits, wealth extracted from house prices appreciation and explosive debt. This was further supported by a climate of deregulation and a massive growth in financial derivatives designed to spread and diversify the risks globally.

The result was a succession of bubbles and crashes: the worldwide stock market bubble and great crash of 19 October 1987, the savings and loans crisis of the 1980s, the burst in 1991 of the enormous Japanese real estate and stock market bubbles and its ensuing “lost decades”, the emerging markets bubbles and crashes in 1994 and 1997, the LTCM crisis of 1998, the dotcom bubble bursting in 2000, the recent house price bubble, the financialization bubble via special investment vehicles, speckled with acronyms like CDO, RMBS, CDS, … the stock market bubble, the commodity and oil bubbles and the debt bubbles, all developing jointly and feeding on each other, until the climax of 2008, which brought our financial system close to collapse.

Each excess was felt to be “solved” by measures that in fact fueled following excesses; each crash was fought by an accommodative monetary policy, sowing the seeds for new bubbles and future crashes. Not only are crashes not any more mysterious, but the present crisis and stalling economy, also called the Great Recession, have clear origins, namely in the delusionary belief in the merits of policies based on a “perpetual money machine” type of thinking.

The problems that we have created cannot be solved at the level of thinking we were at when we created them.” This quote attributed to Albert Einstein resonates with the universally accepted solution of paradoxes encountered in the field of mathematical logic, when the framework has to be enlarged to get out of undecidable statements or fallacies. But, the policies implemented since 2008, with ultra-low interest rates, quantitative easing and other financial alchemical gesticulations, are essentially following the pattern of the last thirty years, namely the financialization of real problems plaguing the real economy. Rather than still hoping that real wealth will come out of money creation, an illusion also found in the current management of the on-going European sovereign and banking crises, we need fundamentally new ways of thinking.”

And with that biting critique of central bank policy making, we come back to Blanchflower’s fateful line: “We couldn’t take the chance that he was wrong.”

Without a fundamental shift in economic thought at the highest levels of central banking, there is little doubt that the response of any central bank during the next crisis – and there will always be a next crisis – will be more the same. Central banks will again apply the limited tools they have: low interest rates, quantitative easing, a variety of bailout mechanisms – in short, they will resort to the financial repression of savers in the name of the greater good.

Jim Bianco can argue, far more eloquently than your humble analyst, that savers should be rewarded, not punished; that financial repression should only be practiced in extremis; and that moral hazard should be respected. But the reality is that the people with their hands on the levers simply believe with all their hearts in a different theoretical economic framework and will not take a chance on being wrong. They will act just as they have in the past.

I would argue, and I think Sornette would agree, that the current policies are simply increasing the instability of the entire system, leading up to another major dislocation in the not-too-distant future. In much the same way that everyone loved rising house prices in the middle of the last decade, we all find contentment in a rising stock market now. For Bernanke and his kin, the markets simply confirm the correctness of their policies. “More cowbell!” is the economic order of the day.

As Sornette put it, “Each excess was felt to be ‘solved’ by measures that in fact fueled following excesses; each crash was fought by an accommodative monetary policy, sowing the seeds for new bubbles and future crashes.”

Richard Fisher, Dallas Federal Reserve President, has been arguing forcefully that the Fed needs to begin tapering its quantitative easing. He is part of a growing chorus that is increasingly uncomfortable with the potential unintended consequences of massive accommodation and the financial repression of savers. Let us hope they are gaining a hearing.

Thinking About Alternatives

Last week I started my letter with a simple but vehement question: “What in the world is going on?!” In seeking an answer to that question, we examined some data points in the market and highlighted the idea of diversifying into alternative investment strategies as a means of balancing our portfolios during this precarious period. This week I want to follow up that discussion with a note on an important topic with regard to evaluating alternative investment funds: manager selection and the concept of performance dispersion.

In the alternative investment arena, a manager’s efforts to deliver higher, risk-adjusted returns can produce huge returns … or significant losses. Therefore, performance dispersion – the difference between the best- and worst-performing funds can be quite large. To avoid finding themselves toward the bottom of that spread, investors should select a fund manager carefully

My partners at Altegris have produced a timely strategy paper titled “All Managers Are Not Created Equal” that illustrates why manager selection is such an important part of the alternative investment process. Written by my good friend Jon Sundt, President and CEO of Altegris, the piece does a great job of covering both the opportunities and the challenges presented to investors when they choose an alternative investment manager. I encourage you to download and study this paper in detail if you are looking to diversify into alternative investments.

14 Years and Counting

It was 14 years ago this week that I began publishing Thoughts from the Frontline on the internet, on a more or less weekly basis. All the letters from January 2001 on – the good, the bad, and the embarrassing – can be found in the archives at http://www.mauldineconomics.com. That is close to 7000 pages of commentary, some of which I’m proud of and some of which I’d like to bury in the deepest, darkest parts of the internet. Together, you and I have gone through recessions, bull and bear markets, credit crises, and several bubbles, and we have examined at least 100 different topics.

I started with 2,000 email addresses and must admit I never thought at the beginning that I would attract such a wide audience. We will be doing another survey soon, but the past surveys have shown that about 25% of you live outside of the United States. The majority of you are very well-educated and reasonably affluent; but in a list as large as this we go from people who are self-educated or just beginning their education to PhDs and people with immense experience, and from people who are just beginning to accumulate net worth to a few readers who have already amassed billions. I’ve had the pleasure of meeting many of you and corresponding with many more over the years. I am constantly amazed at the thoughtfulness and diversity of my readers, but the one constant seems to be that you are genuinely nice people. I look at the comments section on other writers’ sites and compare them with the notes from my own readers, and it is obvious that you are a cut above the usual crowd. I am humbled by your support and proud of you as well. I am fully aware that the highest compliment any writer can receive is an allocation of time from his readers. I am truly grateful for being allowed to be part of your life.

My business model has changed over the years, and we anticipate a few more changes at Mauldin Economics in the coming year, all in the effort to serve you better. The one thing that will not change is this letter and my companion letter, Outside the Box. I will still write these every week, and they will remain free. You will continue to get my unvarnished opinions, the most interesting essays I can find, and the best macroeconomic guidance I can muster. When I began writing this letter, my prime motive was to help us all understand how the puzzle pieces fit together. That goal has not changed in 14 years. The puzzle seems to have gotten more complicated, so we have an even greater need today to assemble the jumble of pieces into a coherent picture.

Let me thank you from the bottom of my heart for being one of my readers. While it may sound a little corny, I have always thought of each of you as one of my closest friends. That is the way I approach writing the letter, much as if you and I were sitting at a corner table having a quiet conversation, informal yet intense, and animated with a sense of fun and the anticipation of discovery.

Here’s to another 14 years of continued conversation.

Montana, San Antonio, Chicago, Bismarck, Denver, Toronto, NYC…

The list above sounds like a lot of travel, but somehow I am not gone that many days. I will be in Montana this week for R&R with my friend Darrell Cain at his home on Flathead Lake. I’ll catch up on some reading and have some well-deserved rest, as I have just finished a major project that we will announce in a few months. As those around me know, I’ve been consumed by projects the past few months and am ready for a more normal life. Montana sounds perfect at the moment.

The weekend before Labor Day, I will be in San Antonio for the 71st World Science Fiction Convention, Lone Star Con 3, where I will get to hang out with some of my favorite writers and talk about both history and the future with guys who live in the past and the future (ignoring the present). I have never been to one of these, and the experience has long been on my bucket list.

Then I will be off to Chicago for a presentation (details to follow next week) and after that on to Bismarck, North Dakota, for a few days with BNC National Bank. Lacy Hunt will join me for an all-day conference with their clients, and I am pretty sure it will be open to the public. I’ll also get an update from BNC and Loren Kopseng on the Bakken oil boom. If the stars line up right, I will take an extra day and fly down with my friend Loren to South Dakota. If that works out, I will be able to say I have been in all 50 states.

The next week I fly to Denver for a day to be with the team at Altegris Investments (details to follow), and then that next weekend I fly to Toronto to be with Louis Gave of GaveKal. There will be a seminar on Monday morning, Aug. 23rd. If you would like to attend, you can register at http://gavekal.com/seminar.cfm or contactclightbound@gavekal.com“>Chris Lightbound with any questions. From Denver I will fly on to New York City for a few days for media and meetings. While that schedule may seem busy, it involves only about 10 nights away from home for the month, which is less than half of what I’ve been doing for the last year. I guess it’s all relative.

And speaking of anniversaries, this week marks two years of not drinking. I can’t say that I don’t miss Chardonnays, but I value my health more. As Clint Eastwood said, “A man’s got to know his limitations.” I am seeing a lot of spectacular advances in the biotechnology world that we at Mauldin Economics will be writing about in the next few months, but I haven’t yet come across a company with a pill that will let me metabolize alcohol with no ill effects on my body so that I can just enjoy the taste of the wine. Contrary to company policy, when I find that company I will probably invest in it first and then tell you about it. Just saying…

Have a great week and enjoy your summer. I see a weekend with kids and family and last-minute work on the big project I mentioned. But it’s all good.

Your amazed at how it’s all turned out analyst,

John Mauldin

Category: Think Tank

Sign Up

Register now to access free Mauldin Economics newsletters online, post comments to articles, as well as access your paid subscriptions.

It’s quick and easy just enter your information – Registration is FREE!

Share Your Thoughts on This Article

![]()

….One of the Biggest in America. “Major institutions, such as JP Morgan, are predicting that prices will more than double within the next few years.”

There is a remarkable opportunity emerging in a market where demand growth is running into a serious wall of tightening supplies.

And we’re about to witness a dramatic shift in control for this supply.

I have talked about this change before in many of my past letters.

But the time to act on this change is running out. Literally.

By the end of the year this shift will take place. And it will put America at a major disadvantage.

The global market is about to run headlong into its first major supply deficit; one that will be controlled by a major world player that doesn’t play ball with the West.

Major institutions, such as JP Morgan, are predicting that prices will more than double within the next few years.

But I think that’s being conservative.

There is strong evidence that prices will go even higher; including a recent political change in a major economy.

There has never been a better time to speculate on these events.

In this special edition letter, I am not only going to introduce you to this explosive opportunity, but also introduce you to a Company that is poised to take advantage of this upcoming explosive market.

Analysts are already shooting out buy signals for this Company with prices much higher than where the Company trades today.

Industry experts are already touting that, “this Company is primed for growth” and “sees (its) current price as a gold-plated bargain.”

But before we get into the details of the Company, let’s talk about this explosive sector opportunity first.

Uranium: The Next Explosive Commodity

Before you shut down the prospects of uranium, let me explain why I believe this sector is primed for explosive growth in the coming months and years.

Not only is uranium one of the cheapest and most efficient sources of energy in the world, its also one of the cleanest.

While we continue to hear talks of alternative energy such as wind, solar, or hydro, uranium is the only alternative energy source amongst them that actually creates energy – the others simply capture and store it.

Because of its ability to produce constant and uninterrupted energy, it is perfect for baseload capacity – meaning that it’s always on.

There are only three sources of baseload energy available to us: fossil fuels (coal and gas), hydro, and nuclear.

The Cost of Power

No other form of energy is as cost effective as nuclear.

Solar energy is the most expensive at $250 per megawatt-hour (MWh), while nuclear is the cheapest at around $40 per MWh. In some countries, nuclear only costs $30 per MWh.

Nuclear power plants also have the highest percentage of electricity produced relative to the total capacity of the plant. To draw a comparison, nuclear plants have a capacity of 89.6%; coal 72.6%; natural gas 37.7%; heavy oil 29.8%; hydro 29.3%; wind 26.8%; and solar 18.8%.

Environmental Benefits

Many environmentalists have now turned pro uranium.

That’s because every one pound of uranium used instead of coal decreases CO2 emissions (CO2E ) by around 45,000 pounds.

Let’s put that into perspective:

A passenger vehicle produces on average 4.8 metric tons of CO2E every year, or roughly 10,582 pounds.

That means every pound of uranium used instead of coal removes the equivalent CO2E that four cars produces every year.

According to the World Nuclear Association, current reactors require approximately 176.7 million lbs. of uranium each year.

No wonder why public opinion on the nuclear sector is suddenly turning positive.

Even environmentalist Robert Stone, an award-winning documentary filmmaker, has now changed his views on nuclear energy:

“I’ve considered myself a passionate environmentalist for about as long as I can remember…It’s no easy thing for me to have come to the conclusion that the rapid deployment of nuclear power is now the greatest hope we have for saving us from an environmental catastrophe.”

He recently released his latest documentary, “Pandora’s Promise,” which explores the transformation of anti-nuke environmentalists into believers of the benefits of nuclear power.

He recently released his latest documentary, “Pandora’s Promise,” which explores the transformation of anti-nuke environmentalists into believers of the benefits of nuclear power.

The documentary aims at debunking a lot of the nuclear myths that came post-Fukushima.

Japan, Fukushima and Abe

A resource-poor nation, Japan’s economic growth potential is limited by demographic decline and its dependence on energy imports.

That’s why nuclear power has been a key part of Japan’s energy diversification and security strategy for well over 40 years.

But since the Fukushima meltdown in 2011, which devastated the nuclear sector, all but two of the country’s 54 reactors have been taken off line. As a result, imports of fossil fuels have risen dramatically to compensate.

The high cost of continued fuel imports is destroying Japan’s current focus on restoring economic growth and achieving the 2% inflation that Japan Prime Minister Shinzo Abe has promised.

Abe wants to see Japan’s inflation rate at 2% and has told the Bank of Japan (BOJ) to hit that target by printing more money and doing whatever it can to stimulate the cause.

Despite the insane monetary policy, there is no way Japan can achieve growth without first lessening the effects of energy on the economy.

Power utilities in Japan have already increased liquefied natural gas imports by 18% year-on-year in 2011 and by 5% year-on-year in 2012.

According to BP’s 2013 Statistical Review of World Energy, Japan consumed41% more fuel oil in 2012 compared to 2011, from 577,000 barrels per day to 811,000 barrels per day.

In May 2013 alone, Japan spent $5.4 billion on imports of liquefied natural gas, $11 billion on crude oil (electricity accounts for just under 20 percent of oil product consumption) and nearly $2 billion on coal.

If Abe wants to achieve his 2% target of inflation, he needs get those reactors back online.

Abe Gets His Wish

Last month, Japanese voters gave Abe and his Liberal Democratic Party (LDP) control of the upper house of parliament, meaning that for the first time in six years the LDP will have control of both chambers of The National Diet, Japan’s bicameral legislature.

Essentially, Abe’s control over both houses would be like Obama gaining control of both the Senate (upper house) and the House of Representatives (lower house).

With this new control, Abe will undoubtedly make turning nuclear reactors back on a priority.

Growing Demand Worldwide

Despite the growing rhetoric of countries – such as Germany and Switzerland – phasing out of nuclear power, nuclear power continues to march forward.

While Germany immediately took eight reactors offline and has publicly stated it will phase out its remaining nine reactors by 2022, starting in 2015, it ironically still supports foreign nuclear power and will use public money to guarantee the construction of power plants in other countries

Since Fukushima, Germany has become a net importer of power from France, relying on more costly French nuclear power.

For now, Germany has enough money to continue this for some time. But I don’t believe the nation will continue paying for expensive imported French nuclear electricity when it can do it on home turf at a much cheaper price.

China – The Next Largest Consumer

It’s impossible to talk about world energy without talking about China.

The nation, like many others, reevaluated its nuclear power program since Fukushima, and suspended nuclear plant approvals for a couple of months.

However, that didn’t last long as the government has already decided to continue with its nuclear power developments.

That means they’re on track to quadruple their nuclear capacity by 2020.

The country already has 26 reactors under construction.

By 2050, Mainland China is looking to ramp up to 400 gigawatt (GW).

In order to fuel 400 GW, China will need 195.4 million pounds of uranium per year for its power plants – that’s more uranium than all of the world’s current consumption per year.

Don’t Believe Everything You Hear

Despite what you hear, nuclear is isn’t shrinking – its growing rapidly.

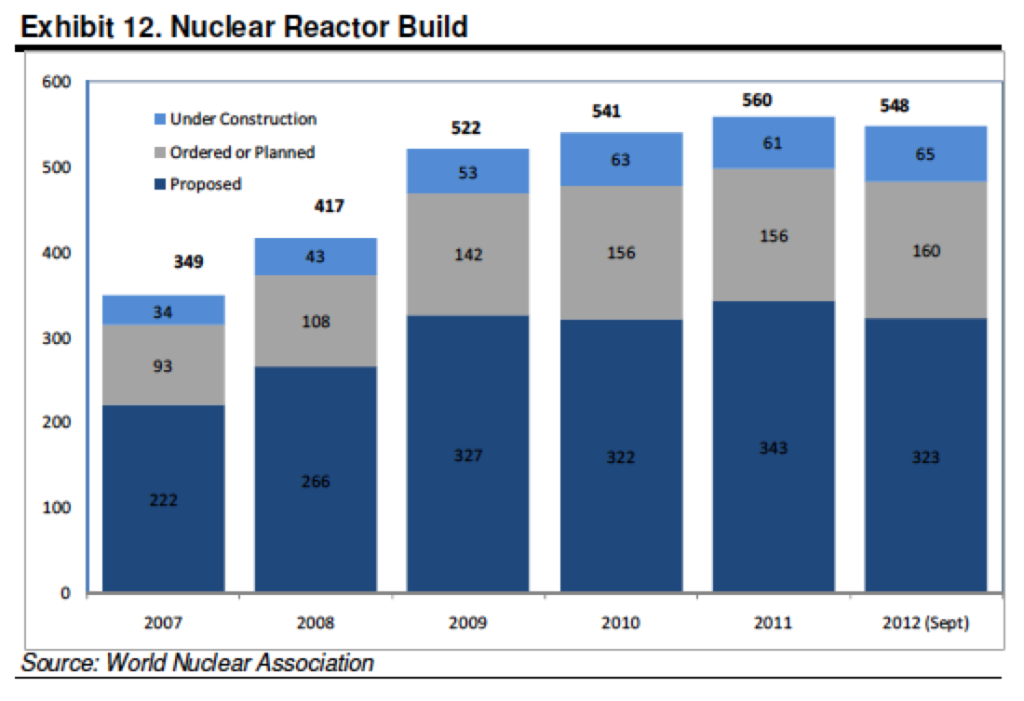

Since 2007, total new reactor builds (under construction, planned, and proposed) have increased by 57%, from 349 to 548 as of September 2012.

Meanwhile, China, India, and Russia have all re-affirmed their support for nuclear power. Combined, those three powerhouses will represent 50% of world nuclear reactor construction.

The World Nuclear Association shows that there are currently 433 operational reactors worldwide, with the U.S. leading the way with 104 reactors.

Here’s where the hurt begins.

The Biggest Energy Consumer

Every year, the United States consumes over 51M lbs. of U3O8 at its 104 reactors, with the power representing nearly 20% of the nation’s total electric energy generation in 2011.

The U.S. is the world’s largest supplier of uranium energy.

Yet the nation only produces 4.3M lbs. of uranium per year at home – meaning they have to rely heavily on imports.

Clearly, nuclear energy is a massive part of U.S. society and security.

That’s why the head of the Department of Energy (DOE) announced a fresh start to its nuclear-disposal issue on January 10, 2013, emphasizing the importance of nuclear power to U.S. energy security.

Despite being the largest consumer of nuclear energy, the U.S. imports the majority of its uranium supply – just like oil.

As a matter of fact, the U.S. is more dependent on foreign uranium supplies than it is on oil.

We’ve already seen what happened to oil prices.

Herein lies a massive problem for Americans.

Losing Control of Energy

Much of the oil imported into the U.S. come from friendly sources and is either under the control or direct influence by America.

Uranium, on the other hand, is mainly controlled by a nation that will likely not be willed into uncomfortable terms by the U.S.

Russia – The Energy Powerhouse

Russia already maintains significant control over oil and gas supplied to the European Union.

It has already used this control to gain political advantage, as I mentioned in my Letter, “The Brink of War“.

As the most energy-dependent country in the world, the U.S. will soon be at the mercy of Russia when it comes to uranium supplies.

Knowing this, Russia has taken advantage of the severely depressed uranium price by leading the acquisitions of uranium assets all over the world.

Russian Buying Spree

In 2011, ARMZ, a Russian state-owned company, bought Australian junior Mantra Resources for C$1.15 billion.

Earlier this year, they purchased Uranium One for C$1.3 billion.

With its purchases, it will gain control of major uranium assets in Kazakhstan, Australia, Tanzania, and the U.S.

Earlier this year, Russia signed the long awaited nuclear power agreement, financing $500M for the supply of two 1000 Megawatt reactors with Bangladesh.

The deal was immediately followed days later by a major arms purchase agreement worth a billion dollars for the delivery of armored vehicles and infantry weapons, air defense systems and Mi-17 transport helicopters.

While Russia continues to snap up uranium assets, the United States hasn’t done much in terms of moving nuclear forward.

Unfortunately, that is going to be a major disadvantage for Americans.

More than 40% of U.S. uranium imports come from Russia, or from locations under the influence of Russia.

Russia and Namibia also plan to launch joint development of uranium deposits, while Niger has already granted Gazprom (another Russian owned entity and the largest extractor of natural gas in the world) uranium-exploration licenses in return for guaranteed investments.

Around 16% of U.S. uranium imports come from Africa.

That means Russia could have influence or control over 56% of U.S. uranium supply.

Remember that nearly 20% of U.S. energy comes from nuclear energy. That mean a whopping 10% of American energy currently relies on Russia for its power.

But that’s just the start of the hurt.

Megatons to Megawatts Set to Expire

The Megatons to Megawatts program was a US-Russian agreement implemented in 1993 to convert 1.1 million pounds of highly-enriched uranium (HEU) taken from dismantled Russian nuclear weapons into low-enriched-uranium (LEU) for nuclear fuel.

Over the past years, up to 10 percent of the electricity produced in the United States has been generated by fuel fabricated using LEU from the Megatons to Megawatts program.

The contract ends at the end of this year.

So what happens when this contract runs out?

The Transitional Supply Contract

The Transitional Supply Contract is a multi-year contract that allows the U.S. to purchase about 21 million separative work units (SWU) through 2022 with a mutual option to purchase up to another 25 million SWU during that period.

However, according to the deal terms from USEC, the United States Enrichment Corporation:

“The low enriched uranium supplied by TENEX (a state owned Russian company which trades uranium fuel and fuel processing services abroad) will now come from Russia’s commercial enrichment activities rather than from downblending of excess Russian highly enriched uranium.”

I want to stress the word “commercial” within that paragraph.

Commercial means doing something for profit.

Furthermore, “The pricing terms for SWU under the contract are proprietary, but are based on a mix of market-related price points and other factors.”

In other words, the Russians will begin to sell uranium to the U.S. for profit.

And they get to set the price.

Tension between Russia and the U.S. continue to grow, and Obama recently cancelled his Moscow Putin Summit visit because of their growing differences.

Do you think Russia will sell uranium to the U.S. for cheap?

Uranium Prices: Not All As it Seems

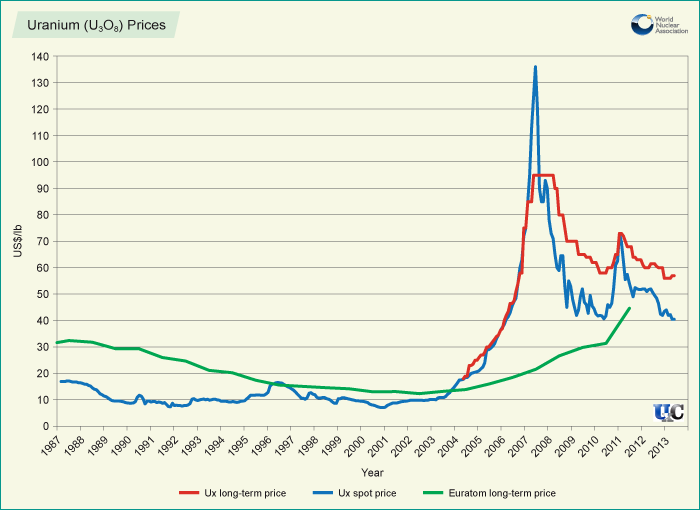

Uranium prices differ dramatically from other commodities and resources such as oil and gas.

While many often reference the spot price of uranium, the long-term price is what really counts.

That’s because less than 15% of uranium is actually traded at spot price. That means more than 85% of uranium is traded in long-term prices.

Take a look, courtesy of UxC and the World Nuclear Association:

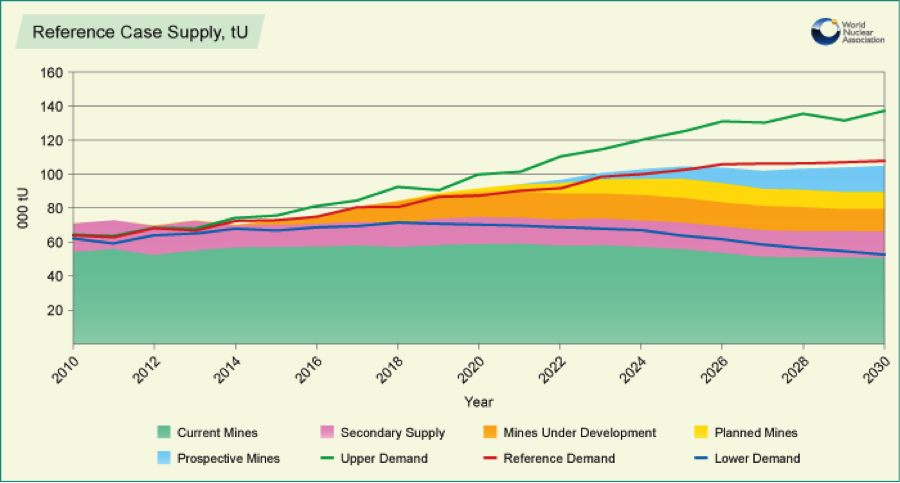

We’re now at the tipping point where both reference demand and upper demand will outpace current production, the secondary supply market, and even the supply by mines that are currently under development.

It’s no wonder the world’s richest people are investing in the sector.

The Richest People on Earth

Both Bill Gates and Warren Buffett are strong advocates of nuclear power, and both believe that the markets have overreacted after the Fukushima meltdown.

They are both actively investing in the sector.

Gates is a strong believer in the safety of nuclear reactors and has put his money where his mouth is by investing millions into the private company TerraPower, which is developing a new nuclear design.

During Berkshire Hathaway’s annual meeting, Warren Buffett stated just how important nuclear power is for the world. MidAmerican Energy, a Buffet company, has applied to build a nuclear plant in Iowa and currently operates a 1,760 MW facility in Illinois.

Miners Outperform

Unlike gold miners, uranium miners have been moving in an inverse relationship to spot commodity price.

Despite spot uranium prices dropping below $40, uranium miners such as Cameco are up over 30 percent since the November low.

That’s because uranium doesn’t trade large volumes on a futures exchange and the spot price of uranium doesn’t actually reflect the actual price of uranium that’s being sold in the market.

Unlike other metals such as copper or nickel, uranium is traded in most cases through contracts negotiated directly between a buyer and a seller.

That means the only viable way to play the uranium sector is to invest in companies that mine and explore for it.

But there’s a problem.

There aren’t many uranium producers that trade in North America.

The Supply and Demand Gap

As I mentioned earlier, current nuclear reactors require about 176.7M lbs. annually to operate.

On a global scale, mine supply is only around 137M lbs., while secondary sources (mainly supplied by HEU) add another 26M lbs.

That’s a shortfall of nearly 14M lbs. per year.

When HEU ends, secondary sources will be almost halved, bringing an even bigger shortfall.

New mine production is very much needed, but simply won’t happen due to a low spot price and the growing costs of production worldwide.

I believe that a spot price of at least US$70/lb. will be required to truly spur new mining production; JP Morgan estimates US$80/lb.

What to Do

In the current low spot price environment, in-situ recovery (ISR) mines are preferable over conventional open pit uranium mines simply because the average production cost for a typical ISR mine is US$15-$40 per lb., whereas an open pit mine can average $30-$70 per lb.

Because of lower costs and political security, I prefer to bet on U.S.-based ISR uranium producers.

To learn more about how ISR Mining works, click here:

Click to enlarge

That is why I am about to introduce you to a Company that I believe is poised for considerable growth.

This Company:

- is working with the Wyoming State administrators to complete the documentation for the closing of a $20M financing; expected to close in the fall

- is poised to be the next U.S. uranium producer

- owns one of the largest uranium land package in one of the most prolific uranium regions in America, the Powder River Basin

- and has a management team that has put many uranium projects into production

It’s no wonder why a Dundee analyst is saying this Company “appears to have amongst the best potential to provide long term sustainability form its cluster of projects on a large land package.”

He’s also saying that this Company “is well positioned to take full advantage of the uranium market for the long-term due to its strategic land holdings.”

That’s because this Company not only owns one of the biggest land packages in one of the most prolific uranium regions in America, but it’s en route to production – just as a major international contract for uranium expires.

What happens when you combine an extremely capable and experienced management team, a near-term uranium producer, and one of the most significant land packages in one of the most prolific regions in America?

Ed Note: Equedia is very bullish on a company named Uranerz Energy Corporation (TSX: URZ)(NYSE MKT: URZ). If you click HERE and scroll down you will find their bullish case for Uranerz laid out in detail.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair