Gold & Precious Metals

New Find Is Three Times as Big as the Bakken

The latest U.S. find isn’t just massive; it’s also yet another sign the U.S. shale oil boom is still in its infancy… That’s why you can still make a fortune in new American energy. And yes, you can still do it in Texas. Just ask Dr. Kent Moors. And ask the drillers, too, because these guys are about to uncork a vast new reserve before anyone else even shows up

The latest U.S. find isn’t just massive; it’s also yet another sign the U.S. shale oil boom is still in its infancy… That’s why you can still make a fortune in new American energy. And yes, you can still do it in Texas. Just ask Dr. Kent Moors. And ask the drillers, too, because these guys are about to uncork a vast new reserve before anyone else even shows up

Investors searching for the best stocks to buy now often look toward the shale oil boom and, in particular, at key finds such as the Bakken formation in North Dakota or the Permian Basin in west Texas.

But a fresh development in the Permian Basin has made the U.S. oil industry take notice – and that’s not easy given the dramatic shale oil finds across the country.

In fact, the U.S. Geological Survey called this find the largest discovery in the last 50 years in the Permian Basin.

I’m talking about the Cline Shale.

Dr. M. Ray Perryman, head of the economic analysis firm The Perryman Group, told Rigzone “The information coming out on the Cline shale indicates up to 30 billion barrels of recoverable oil, which is substantially larger than other large plays.”

To get an idea of what this means, consider that the Eagle Ford in Texas is believed to have approximately 10 billion barrels of recoverable oil and the Bakken 11 billion barrels.

That means the Cline Shale has at least three times the amount of recoverable oil as two of the biggest shale oil finds in the United States.

Clearly, if you’re looking for the best energy stocks to buy now based on the shale oil boom, you need to find out as much as you can about the Cline Shale.

Where the Cline Shale Fits In

Texas has a number of overlapping oil fields, and the Cline Shale happens to be one of them.

And it’s a really, really big one.

The 1.6 million-acre formation lies over a large area on the eastern shelf of the Permian Basin, running about 9,000 feet underneath a 10-county swath of Texas. It averages about 70 miles wide from east to west and roughly 140 miles wide from north to south.

The key target zone for oil production is between 200 and 500 feet thick. The Cline is also known as the Lower Wolfcamp because some of it lies beneath the already-known Wolfcamp shale formation to the west.

That means a few fortunate companies can drill wells with stopping points in both shale formations.

Meanwhile, the potential of the Cline Shale could exceed even the impressive estimate of 30 billion barrels of recoverable oil.

Oil companies like Devon Energy Corp. (NYSE: DVN) have only just begun to drill in this formation.

“We’ve had some encouraging results in the Cline, and we are hopeful and optimistic about our prospects for being successful in this play,” Devon spokesperson Chip Minty told the Texas Tribune.

The company hasn’t made a lot of noise about its results so far because it is so early in the Cline’s development. In total, fewer than 100 wells have been drilled to date in the Cline Shale.

But some of those wells have already produced 400 to 800 barrels per day of oil equivalent with 60% to 75% oil production. That’s just a hint of the extraordinary potential that the Cline Shale holds, both for the oil industry and investors.

The Best Stocks to Buy Now in the Cline Shale

To find the best energy stocks to buy to capitalize on the black gold that’s just starting to flow out of the Cline Shale, one need only look at the companies that got there first…

Of course, there’s Devon Energy, which drilled many of the early wells.

Other companies already drilling in the Cline include Apache Corp.(NYSE: APA), Gulfport Energy Corp. (Nasdaq: GPOR), and another pioneer in the region, Laredo Petroleum Holdings Inc. (NYSE:LPI).

Laredo’s founder, Chairman and Chief Executive Officer (CEO) Randy Foutch, has hinted that the Cline Shale could end up being one of the most profitable shale formations in the United States.

“We believe the Cline shale exhibits similar petrophysical attributes and favorable economics compared to other liquids-rich shale plays, such as in the Eagle Ford and Bakken shale formations,” Foutch told the American Association of Petroleum Geologists Explorermagazine last year.

Another company with drilling operations in the Cline as well as nearby, Breitling Oil & Gas, has planned an initial public offering for late this year or early in 2014.

“We are in a hotbed area with great infrastructure from legacy conventional plays, we have access to a talent pool for workers and equipment is already in the area,” Breitling CEO Chris Faulkner toldRigzone.

But as optimistic as this seems, the Cline Shale picture could get even brighter. As more wells are drilled in the Cline Shale, it is very likely that the estimates of the amount of recoverable oil will keep rising. That’s just what happened with the Bakken and Eagle Ford shale formations.

This exceptionally promising location virtually guarantees success for the companies drilling in the Cline, making them the best energy stocks to buy to take advantage of this new shale oil play.

Note: The profits from the next stage of the shale oil boom could dwarf the initial windfalls, according to Money Morning Global Energy Strategist Dr. Kent Moors. The key to finding the best stocks to buy in the next wave of the boom, Dr. Moors says, is technology…

Related Articles:

- Money Morning:

The Next Best Investments in Oil Come from This Texas Sweet Spot - The Cline Shale:

Cline Shale Brief Overview - Forbes:

Texas’ Amazing Shale Oil and Gas Abundance - New York Times:

Ready (or Not?) for a Great Coming Shale Boom - Fuel Fix:

West Texas Shale Could Dwarf Eagle Ford - Rigzone:

Future Looks Bright for Cline Shale Potential

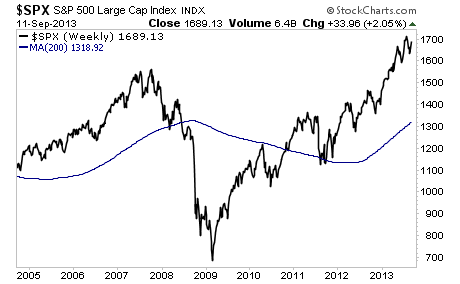

Is the Stock Bubble About to Burst?

Ben Bernanke has created the mother of all bubbles.

Today, the S&P 500 is sitting a full 30% above its 200-weekly moving average. We have NEVER been this overextended above this line at any point in the last 20 years.

Indeed, if you compare where the S&P 500 is relative to this line, we’re even MORE overbought that we were going into the 2007 peak at the top of the housing bubble.

We all know how bubbles end: BADLY.

This time will be no different. The last time a major bubble of these proportions burst, we fell to break through this line in a matter of weeks.

We then plunged into one of the worst market Crashes of all time.

By today’s metrics, this would mean the S&P 500 falling to 1,300 then eventually plummeting to new lows.

This is not doom and gloom. This is a fact. The Fed has created an even bigger bubble than the 2007 one.

The time to prepare for this is not once the collapse begins, but NOW, while stocks are still rallying. Stocks take their time moving up, but when they crash it happens VERY quickly.

Yours in Profits,

Graham Summers

With the above in mind, I’ve already urged my Private Wealth Advisory clients to start prepping. We’ve opened six targetted trades to profit from the stock bubble bursting.

We’ve also taken care to prepare our finances and our loved ones for what’s coming, by following simple easy to follow steps concerning our savings, portfolios, and personal security via my Protect Your Family, Protect Your Savings & Protect Your Portfolio reports.

I’ve helped thousands of investors manage their risk and profit from market collapses. During the EU Crisis we locked in 72 straight winning trades and not one loser, including gains of 18%, 28% and more.

In fact, we’re currently on another winning streak having locked in FOURTEEN winning trades in the last two months, including gains of 10%, 11%, 21% and 25%.

All for the the small price of $299: the annual cost of a Private Wealth Advisory subscription.

To take action to prepare for what’s coming… and start taking steps to insure that when this bubble bursts you don’t lose your shirt.

In today’s Outside the Box, my good friend George Gilder, the well-known techno-utopian, attempts with some success to turn economics on its ear. “The economy is not chiefly an incentive system,” he asserts, “it is an information system.” And information, truly understood, is about the introduction of novelty, or “surprise,” into a system. In the case of the economy, it’s about invention and entrepreneurship. The new information that is injected gets converted into knowledge; and thus, says George, it is accumulated knowledge, rather than money or material, that constitutes true wealth.

In today’s Outside the Box, my good friend George Gilder, the well-known techno-utopian, attempts with some success to turn economics on its ear. “The economy is not chiefly an incentive system,” he asserts, “it is an information system.” And information, truly understood, is about the introduction of novelty, or “surprise,” into a system. In the case of the economy, it’s about invention and entrepreneurship. The new information that is injected gets converted into knowledge; and thus, says George, it is accumulated knowledge, rather than money or material, that constitutes true wealth.

And thus the economy is driven not so much by powerful people and institutions wielding the levers of the economic machine as it is by the ever-increasing power of information and knowledge. Economists and the governments they work for often appear to prefer a deterministic, no-surprises (and too-big-to-fail) economy, but that way lies economic stagnation. If determinism worked, socialism would have thrived.

Knowledge is centrifugal: it’s dispersed in people’s heads, and that has never been more true than in the Age of the Internet. And it is this universal distribution of knowledge which feeds back to the economy through the creative insights and entrepreneurial efforts of people worldwide that constitutes our chief hope for economic growth in the era opening up before us, where the limits of monetary manipulation and material extraction are becoming painfully apparent.

Here is a telling sentence from George:

Whether fueled by debt or seized by taxation, government spending in economic “stimulus” packages necessarily substitutes state power for knowledge and thus destroys information and slows economic growth.

The writing is on the wall: either we reinvent ourselves and our global economy, or the noise that is obviously building in the system will overwhelm the creation and transmission of knowledge, and the great human quest for the democratization of wealth will fail. But, as George says, “[C]apitalism is not a system of equilibrium; it is an engine of disruption and invention…. A capitalist economy can be transformed as rapidly as human minds and knowledge can change.” So we do have plenty of grounds for hope.

For the young among my readers, George Gilder wrote the seminal work Wealth and Poverty(which has been recently updated) back in the early ’80s, selling over 1 million copies and influencing a generation. He was Ronald Reagan’s most-quoted living author. He has written many books since then, but his latest book, Knowledge and Power, is in my opinion even more important.

When you combine Gilder’s work with Nassim Taleb’s Antifragility, along with the ideas that appeared in the recent Outside the Box piece by Charles Gave on the natural rate of interest, you can begin to get a real sense of why the design of the current monetary system is so flawed. Gilder’s work is foundational to that understanding. We have given our central banks a mandate far outside their actual capabilities: we’ve made them responsible for employment. With their limited tools, they have set about to improve employment but are disseminating corruption in their communications to the markets, in ways they neither intend nor understand. The framework that dominates the thinking of current central bankers simply does not encompass the new paradigm being advanced by Gilder, Taleb, Gave, and others.

Once you grasp the futility of the current structure, you can begin to make sense of the direction of the economy and understand how to position portfolios for continuing periods of exceptional volatility. In one of the great human ironies, the drive to reduce the fragility of the system in fact creates an even more fragile system, until we have a Minsky Moment on steroids. But that’s a topic for yet another book. I have talked George into writing a summary of Knowledge and Power for today OTB, but it does no more than skim the surface. His books should be included in your fall reading.

George and I have spent many hours talking about new technologies and their implications. Longtime readers know I have a deep fascination with technology and creativity. I have recently been able to get my great friend Pat Cox (who knows more about such things than I have forgotten) to agree to come and write for Mauldin Economics. We will shortly be launching a newsletter focused on technologies that have the potential to transform our society — and ways to invest in them. Pat Cox should be a familiar name to readers of Outside the Box, and I can’t tell you how thrilled I am to be able to work together with him, exploring the fascinating new world that is being created all around us.

I am still thinking through the implications of what I saw on my recent trip to North Dakota. There was just so much positive energy and potential everywhere that it makes you want to come up with ways to transfer that process in every area of the economy. Ironically, if it was up to the federal government as currently comprised, the Bakken oil play wouldn’t exist. It is messy and chaotic and not at all capable of being directed by a central planner. In short, it is massively successful, without one dollar of government money funding the individual businesses. There are no Solyndras in North Dakota. I’m sure there are lots of small failures here and there, but they haven’t cost taxpayers any equity money.

It is a busy week for me here in Dallas, with lots of meetings and research and writing piling on top of one another, plus family, gym, and other personal commitments. Tomorrow I get to have lunch with my friend Kyle Bass and go from there to spend a few hours with Dr. Woody Brock, who is in town for a speech. However much time I have with Kyle or Woody is not enough, as there are just too many ideas to capture in a few hours. But we all talk fast and try to get in as much as possible. I live for these times.

I think I’ll hit the send button and turn back to my reading. I just had a huge database of over 500 city pension plans pop into my inbox, and that is going to capture my attention for the next few hours. You gotta love having readers who can access just about anything and get it to you. When I come up for air I’ll write about what I learned this week. And speaking of weeks, you have a good one.

Your finding out that yoga hurts analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

The Need for a New Economics

By George Gilder

Why is it that so many Americans seem to believe that government spending, fueled by debt or taxes, can drive economic growth and wealth creation? Why do they believe that low interest rates, enforced by the Federal Reserve, can somehow spur business and investment? Why do they imagine that money and consumer demand impel the economy forward?

The reasons, I believe, are rooted in an economic confusion between knowledge and power. Many economists believe that growth is impelled by the exercise of power, represented by money creation and by government spending and guarantees. By manipulating the so-called “levers of the economic machine,” government power can enlarge demand, inducing businesses to invest and consumers to spend. This process is seen to generate the demand that fuels economic growth.

These images of the economy of power are part of the very creation story of economics in an era of new machines and sources of energy. The first economic models were explicitly based on the dynamics of the steam engine then impelling the industrial revolution. Isaac Newton’s physical “system of the world” became Adam Smith’s “great machine” of the economy, an equilibrium engine transforming coal and steam into economic growth and progress.

Exploring technology investments over recent decades, however, I found myself preoccupied less with sources of power than with webs of knowledge in a field of study called Information Theory. On one level this theory was merely a science of networks and computers. Its implications, however, would change our deepest concepts of the nature of wealth. It would show that wealth is not money or power or demand. It is essentially the accumulation of knowledge.

Information theory effectively began with Kurt Godel’s demonstration in 1930 that all logical systems, including mathematics, are intrinsically incomplete and depend on axioms that they cannot prove. This epochal finding is often obscured by elaborate explanations of the intricate mathematics he used to prove it. But as John Von Neumann in his audience was first to recognize, Godel’s proof put an end to the idea of the universe, or the economy, as a mechanism. Godel’s proof, as he himself understood, implied the existence of autonomous creation.

Godel’s proof led directly to the invention by Alan Turing of a universal generic computer, a so-called Turing machine. By this abstract conception, which became the foundation for all computer science, Turing showed that no mechanistic computer system could be complete and consistent. Turing concluded that all logical systems were intrinsically oracular.

Computers could not be Smithian “great machines” or Newtonian “systems of the world.” They inexorably relied upon human programmers or oracles and could not transcend their creators. As Turing wrote, he could not specify what these oracles would do. All he could say was that “they could not be machines.” In a computer, they are programmers. In an economy, they are entrepreneurs.

In 1948 a rambunctiously creative engineer, Claude Shannon, from Bell Labs and MIT, translated Godel’s and Turing’s findings into a set of technical concepts for gauging the capacity of communications channels to bear information.

Shannon resolved that all information is most essentially surprise. Unless messages are unexpected they do not convey new information. An orderly and predictable mechanism, such as a Newtonian system of the world or Smithian great machine, embodies or generates no new information.

Studying information theory for decades in my exploration of technology, I finally found the resolution to the enigmas that currently afflict most economic thought. A capitalist economy is chiefly an information system, not a mechanistic incentive system. Wealth is the accumulation of knowledge. As Thomas Sowell declared in 1971: All economic transactions are exchanges of differential knowledge, which is dispersed in human minds around the globe. Knowledge is processed information, which is gauged by its news or surprise.

Surprise is also a measure of freedom and criterion of creativity. It is gauged by the freedom of choice of the sender of a message, which Shannon termed “entropy.” The more numerous the possible messages that can be sent, the more uncertainty at the other end about what message was sent and thus the more information there is in the actual message when it is received.

In Knowledge and Power, I sum up information theory as the treatment of human communications or creations as transmissions down a channel, whether a wire or the world, in the presence of the power of noise, with the outcome measured by its “news” or surprise, defined as entropy and consummated as knowledge.

Since these communications or creations can be business plans or experiments, information theory supplies the foundation for an economics driven not by equilibrium and order but by surprises of enterprise that yield knowledge and wealth.

Information theory requires that such a process be experimental and its results be falsifiable. The businesses conducting entrepreneurial experiments must be allowed to fail or go bankrupt. Otherwise there is no yield of knowledge and thus no production of wealth. Wealth does not consist in material capital that can be appropriated by the greedy or the government but in learning processes and knowledge creations that can only thrive in freedom.

After all, the Neanderthal in his cave had all the material resources and physical appetites that we have today. The difference between our own wealth and Stone Age poverty is not an efflorescence of self-interest but the progress of learning, accomplished by entrepreneurs conducting falsifiable experiments of enterprise.

The enabling theory of telecommunications and the internet, information theory offered me a path to a new economics that could place the surprising creations of entrepreneurs and innovators at the very center of the system rather than patching them in from the outside as “exogenous” inputs. It also showed that knowledge is not merely a source of wealth; it is wealth.

Summing up the new economics of information are ten key insights:

1) The economy is not chiefly an incentive system. It is an information system.

2) Information is the opposite of order or equilibrium. Capitalist economies are not equilibrium systems but dynamic domains of entrepreneurial experiment yielding practical and falsifiable knowledge.

3) Material is conserved, as physics declares. Only knowledge accumulates. All economic wealth and progress is based on the expansion of knowledge.

4) Knowledge is centrifugal, dispersed in people’s heads. Economic advance depends on a similar dispersal of the power of capital, overcoming the centripetal forces of government.

5) Creativity, the source of new knowledge, always comes as a surprise to us. If it didn’t, socialism would work. Mimicking physics, economists seek determinism and thus erroneously banish surprise.

6) Interference between the conduit and the contents of a communications system is called noise. Noise makes it impossible to differentiate the signal from the channel and thus reduces the transmission of information and the growth of knowledge.

7) To bear high entropy (surprising) creations takes a low entropy carrier (no surprises) whether the electromagnetic spectrum, guaranteed by the speed of light, or property rights and the rule of law enforced by constitutional government.

8) Money should be a low entropy carrier for creative ventures. A volatile market of gyrating currencies and grasping governments shrinks the horizons of the economy and reduces it to high frequency trading and arbitrage in a hypertrophy of finance.

9) Wall Street wants volatility for rapid trading, with the downsides protected by government. Main Street and Silicon Valley want monetary stability so they can make long term commitments with the upsides protected by law.

10) GDP growth is fraudulent when it is mostly government spending valued retrospectively at cost and thus shielded from the knowledgeable judgments of consumers oriented toward the future. Whether fueled by debt or seized by taxation, government spending in economic “stimulus” packages necessarily substitutes state power for knowledge and thus destroys information and slows economic growth.

11) Analogous to average temperature in thermodynamics, the real interest rate represents the average returns expected across an economy. Analogous to entropy, profit or loss represent the surprising or unexpected outcomes. Manipulated interest rates obfuscate the signals of real entrepreneurial opportunity and drive the economy toward meaningless trading and arbitrage.

12) Knowledge is the aim of enterprise and the source of wealth. It transcends the motivations of its own pursuit. Separate the knowledge from the power to apply it and the economy fails.

The information theory of capitalism answers many questions that afflict established economics. No business guaranteed by the government is capitalist. Guarantees destroy knowledge and wealth by eliminating the precondition of falsifiability. Unless entrepreneurial ideas can fail or businesses go bankrupt, they cannot succeed in creating new knowledge and wealth. Epitomized by heavily subsidized and guaranteed leviathans, such as Goldman Sachs, Archer Daniels Midland, Harvard and Fanny Mae, the crisis of economics today is crony statism.

The message of a knowledge economy is optimistic. As Jude Wanniski wrote, “Growth comes not from dollars in people’s pockets but from ideas in their heads.” Capitalism is a noosphere, a domain of mind. A capitalist economy can be transformed as rapidly as human minds and knowledge can change.

As experience after World War II when US government spending dropped 61 percent in two years, in Chile in the 1970s when the number of state companies dropped from over 500 to under 25, in Israel and New Zealand in the 1980s when their economies were massively privatized almost over-night, and in Eastern Europe and China in the 1990s, and even in Sweden and Canada in recent years, economic conditions can change overnight when power is dispersed and the surprises of human creativity are released.

Perhaps the most powerful demonstration that wealth is essentially knowledge came in the rapid post world war II revival of the German and Japanese economies. Nearly devoid of material resources, these countries had undergone the nearly complete destruction of their physical plant and equipment. As revealed by decades of experience with unsuccessful ministrations of foreign aid, the mere transfer of financial and political power is impotent to create wealth without the knowledge and creativity of entrepreneurs.

Information Theory is a foundation for revitalizing all the arts and sciences, from physics and biology to mathematics and philosophy. All are transformed by a recognition that information is not order but disorder. The universe is not a great machine that is inexorably grinding down all human pretenses of uniqueness and free will. It is a domain of creativity in the image of a creator.

In the same way, capitalism is not a system of equilibrium; it is an engine of disruption and invention. All economic growth and human civilization stem from the surprises of creativity and the growth of knowledge in a domain of constitutional order.

The great mathematician Gregory Chaitin, inventor of algorithmic information theory, explains that to capture the surprising information in any social, economic, or biological science requires a new mathematics of creativity imported from the world of computers. He writes: “Life is plastic, creative! How can we build this out of static, eternal, perfect mathematics? We shall use post-modern math, the mathematics that comes after Godel, 1931, and Turing, 1936, open not closed math, the math of creativity…”

Entropy is a measure of surprise, disorder, randomness, noise, disequilibrium, and complexity. It is a measure of freedom of choice. Its economic fruits are creativity and profit. Its opposites are predictability, order, low complexity, determinism, equilibrium, and tyranny.

Predictability and order are not spontaneous and cannot be left to an invisible hand. It takes a low-entropy carrier (no surprises) to bear high-entropy information (full of surprisal). In capitalism, the predictable carriers are the rule of law, the maintenance of order, the defense of property rights, the reliability and restraint of regulation, the transparency of accounts, the stability of money, the discipline and futurity of family life, and a level of taxation commensurate with a modest and predictable role of government. These low entropy carriers bear all our bounties of surprising wealth and progress.

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com.

To subscribe to John Mauldin’s e-letter, please click here:

http://www.mauldineconomics.com/subscribe

To change your email address, please click here:

http://www.mauldineconomics.com/change-address

To unsubscribe, please refer to the bottom of the email.

Outside the Box and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin’s other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRAand SIPC, through which securities may be offered. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Brok er (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining the Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as wel l as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauld in receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have t otal trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.

Looking for a hedge against the Federal Reserve? Try bitcoin. That at least is the view of Cameron and Tyler Winklevoss, who are heavily invested in the virtual currency.

Looking for a hedge against the Federal Reserve? Try bitcoin. That at least is the view of Cameron and Tyler Winklevoss, who are heavily invested in the virtual currency.

Bitcoin, which is created through a cryptographic process rather than by a central bank, attracted attention earlier this year when its price swung wildly. The supply of bitcoins is set at 21 million, which has led to many comparisons between bitcoin and gold.

Indeed, the Winklevoss brothers, speaking at the Value Investing Congress in New York on Tuesday, mentioned the scarcity and durability of both assets as reasons for why people refer to bitcoin as digital gold or gold 2.0.

….go HERE fjor some of the highlights of their talk

9 Things The Winklevoss Twins Taught Me About Bitcoin

The most noteworthy Bitcoin facts imparted to an audience of investors at the Value Investing Congress are listed HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair