Bonds & Interest Rates

Today, Minneapolis Fed President Narayana Kocherlakota, is suggesting we may need even more stimulus to get unemployment down and the economy humming.

Today, Minneapolis Fed President Narayana Kocherlakota, is suggesting we may need even more stimulus to get unemployment down and the economy humming.

The dovish Fed official employs buzz phrases like “whatever it takes,” and he even suggests the Fed should ignore warnings of asset bubbles as it stimulates.

…..read it all HERE

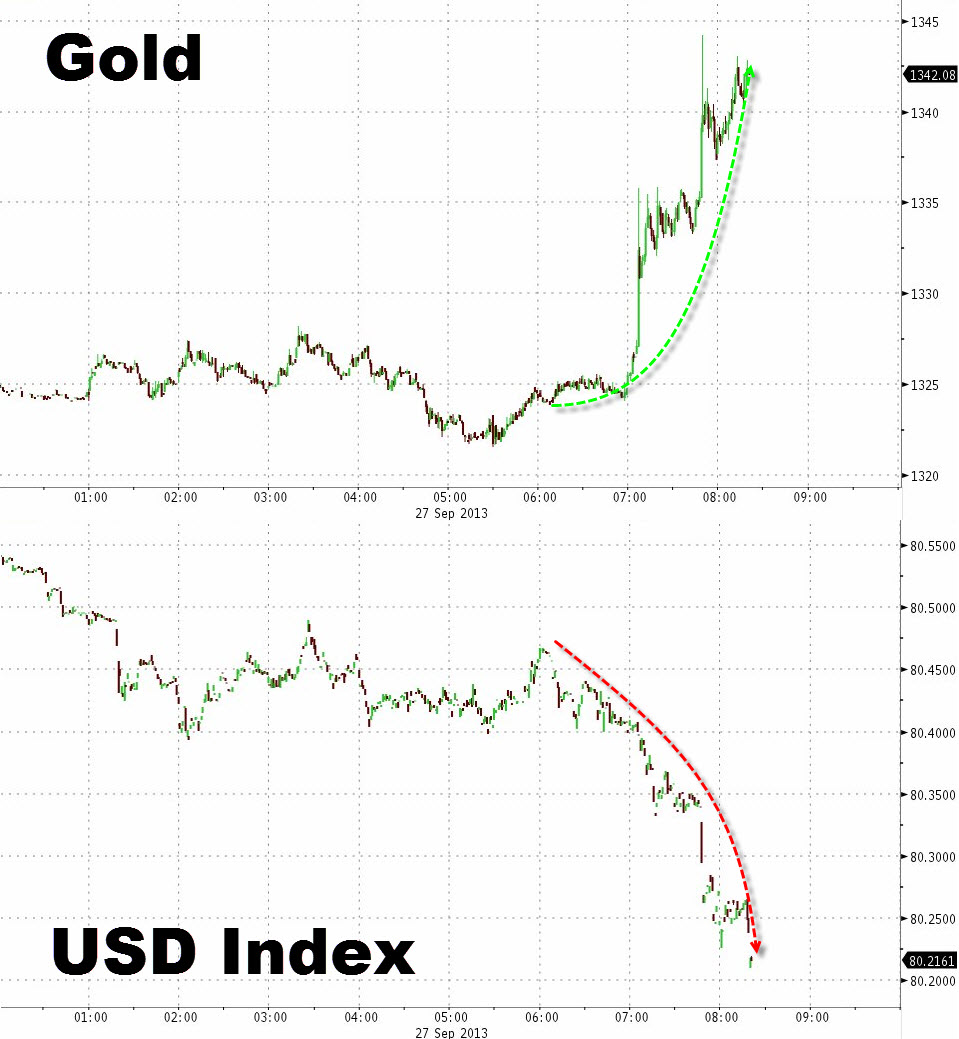

It would appear that between the fears of a government shutdown and the battle over the ‘full faith and credit’ of the US, traders have decided that the stroke-of-midnight agreement is potentially less viable this time as both parties feel the other has more to lose. The USD is being sold against all majors and gold, silver, and WTI crude is well bid as investors seek the safety of hard assets over printable fiat. Of course, that could all change on the next economic data or Washington headline… buckle up…

Chart: Bloomberg

EUR is nearing 8-month highs at 1.3550 as the USD Index presses down to near 7 months lows.

….read ZeroHedge’s feature article on Gold HERE

Gold Markets are not Efficient, Don’t Reflect Fundamentals & Understate Gold’s Market Value (part 1)

This is a series on how and why the gold markets fail to reflect the true balance of demand and supply in gold and silver prices. Many investors expect and believe that the gold price is an accurate reflection of demand and supply, but it isn’t.

This is a series on how and why the gold markets fail to reflect the true balance of demand and supply in gold and silver prices. Many investors expect and believe that the gold price is an accurate reflection of demand and supply, but it isn’t.

In a perfect market the exact weight of demand and supply on a daily basis would be reflected in the daily prices. In both gold and silver markets this is just not true. Many of these factors are common to all markets, but in the gold market the different factors on a broad front are wider and more complex than most. The extent of market liquidity is a key factor in the efficiency of markets so we need to know just how responsive to prices is the liquidity of the gold market.

It’s naïve to expect markets to be perfect in a very imperfect world and where large investors have a disproportionate power to influence precious metal prices –aided by the different structures of different global markets and their relationships to each other—so the most important point for both traders and investors is that they realize this and adjust their trading and investment with these factors in mind. Of course, the real skill is being able to synthesize these factors into an understanding of where gold and silver prices will go and when.

But this subject has major relevance today. We know that global demand for gold is as strong as ever right now, if not stronger, so why isn’t this being reflected in the gold price?

Will the demand eventually find its way into the open global market and impact the gold price? Or has it been knocked away from doing so?

Why does New York have such an impact on precious metal prices when, particularly in the case of gold it is a minor player in terms of demand and supply [7% of global annual demand]?

With China and India the main physical gold buyers, why isn’t the market in one of those countries and dominating it when combined they account for around 70% of global demand?

How easy is it for prices to be managed and manipulated?

We hear much talk about market manipulation by various institutional bodies, but have you thought just how the different gold markets can do this by their structure and through the institutions that provide market liquidity?

Seashore

As we start this series, it’s good to have an analogy on which to hang the picture so we have a clear picture at the end of the series. An analogy that best portrays the interaction of different market influences in the gold and silver market is the seashore. There are three influences: the current, tide and waves. The current is the most dominant influence as it dominates the other two influences.

But the tides are the most dominant noticeable influence to us. They dominate the wave action completely. But in the increasingly short-term world of financial markets, it’s the moment to moment wave action that absorbs the media and unfortunately the traders and often investors. This wave action can be gently and placid on wind free days, but can be whipped up into a raging surf with its furious mist just as easily. But the surf and wind has barely any influence on the actions of the sea, even though they rivet our attention.

Here again we would be naïve to believe that the sea-shore of financial markets would be allowed to act and react smoothly to the underlying influences.

In a commodity market, the bulk of the product is negotiated between user and supplier by an ongoing contract for a specific amount. Anything above or below that amount is supplied to or bought from the open market or exchange. But surprisingly enough, it is the marginal amount bought and sold and the price at which this is done that determines the price that the bulk of demand and supply is priced at.

In the gold market, we will look at the most efficient part of the market where 90% of physical gold is traded, the London Gold Fix.

The Gold Fix

One market where there is close communication between the various professionals is the London gold Fix. Think of a pyramid shape with the 5 gold bullion banks in London (seewww.goldFixing.com) at the top. These communicate on a twice daily basis at 10.30 in London’s morning and at 3.00 p.m. there to set the gold price at which all gold deals dealt there are priced. Each of these banks has its own clients who are buying and selling and many of these have internal clients buying and selling within their own walls. Each professional ‘nets’ out the supply and demand before he takes his ‘net’ position up the pyramid to the higher level until the overall, net position of his bullion bank in the structure is netted out and used as a basis for determining the Fix. If the price they are considering changes their net position and raises the demand or supply, he has another price is looked at. Once the five banks are in agreement over a particular price, then the price is set for all deals being transacted at that particular fix.

In this way demand and supply as reflected in the banking system is smoothed out. But there are so many other factors that influence the gold market that detract from an accurate picture. It’s these that we will examine. You will then see just how easily gold prices can be deflected from giving and accurate balance of demand and supply. In some cases, such ‘deflections’ are outright price manipulations without the manipulators buying and selling physical gold. We have seen this year, in April alone, cases where buying and selling of gold has been engineered by banks and their largest clients, and very successfully so. But we will also look at other ways this can be done. It can even be done with the banks absent from the picture.

We conclude this first part by emphasizing that if the gold market were truly efficient the gold price would be much higher and with far less volatility.

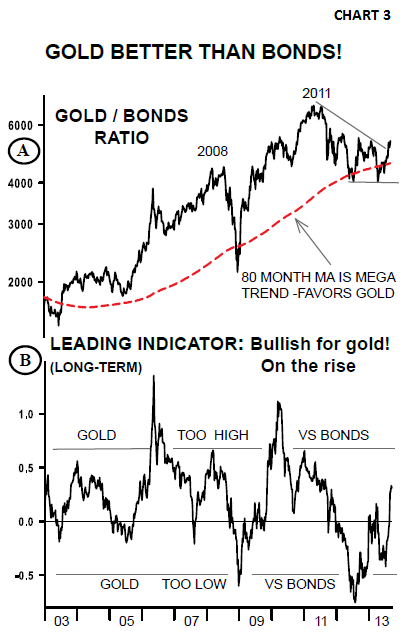

This chart is so important we really want you to take a hard look at what it’s telling us.

Very simply, this ratio chart compares gold to bonds. When it rises, gold is stronger than bonds. And when it declines, gold is weaker than bonds.

We call this our inflation-deflation barometer. Why?

Gold tends to rise during inflationary or generally good economic times. That’s why the ratio’s been rising over the past decade.

Ed Note: This is just a portion of this article, more charts and points made in the article Seeds of Change Growing

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair