Personal Finance

According to the thought-provoking Michael Mauboussin, making an important decision is never easy and making the right decision is even more difficult.

According to the thought-provoking Michael Mauboussin, making an important decision is never easy and making the right decision is even more difficult.

Effective decision making isn’t just about accumulating information and going with what seems to make the most sense. Sometimes, internal biases can impact the way we seek out and process information, polluting the conclusions we reach in the process.

Mauboussin says it is critical to be conscious of those tendencies and to accumulate the sort of fact-based and unbiased inputs that will result in the highest likelihood that a decision actually leads to the desired outcome.

In the video below he lays out three steps that can help with this process:

China’s future may be brighter than anyone expects – it’s time to buy

A lot of people are negative on China these days.

A lot of people are negative on China these days.

The bears worry that China relies too much on investment, and not enough on consumer spending. If it wants to continue to grow sustainably, consumers need to pick up the slack. Otherwise there could be an almighty crash.

But research from a couple of Chinese academics suggests that Chinese consumers are in fact spending significantly more than official figures suggest.

If they’re right, it means that the Chinese economy is less likely to ‘hit the wall’ in the next few years.

That means, investing in China is less risky than many people think.

And that leaves the Chinese stock market looking pretty cheap…

Why over-investment can lead to crashes

If you’re wondering why too much investment might lead to a crash, it’s because you get diminishing returns if you invest too much.

If you build roads and railways that no one ever uses for example, then they won’t generate any revenue. So you’ve spent a load of money on a project that will never cover its costs, let alone generate a return.

If this continues, there will come a time when businesses realise it’s pointless, because they’re not getting any return on their latest investments.

When that happens, workers in construction and heavy industry will get laid off. That means rising unemployment and recession. There’s also the risk to the banking system if all of these dud projects have been funded with borrowed money.

If you look at China, it’s not hard to find signs of over-investment. The country is famously dotted with ‘ghost cities’. There are also some plain weird follies, like this giant copper-plated puffer fish.

So the question is: can China achieve a relatively smooth and pain-free transition from an investment-led economy to one based more on consumption?

Could the future be brighter for Chinese consumers?

Well, if you believe the official Chinese government figures, it’s a massive challenge. Household consumption comprises just 34% of China’s GDP, according to official figures. That’s way lower than the UK, on 65%, and the US on 70%.

The sort of dramatic shift in economic focus needed to get the Chinese consumption figure up from 34% to, say, 50%, could easily end in tears.

However, an article in yesterday’s FT gives grounds for optimism. It cites research from two Chinese academics, Jun Zhang and Tjan Zhu, which suggests that Chinese consumption has been under-reported for some time.

Indeed, Zhang and Zhu believe that a more accurate figure for household consumption would be around 45% of GDP.

How do they get to this figure? Well, arguably it’s by taking a more realistic view of corruption in the country. High earners prefer to hide the true extent of their consumption from government bureaucrats. Some even avoid being surveyed altogether.

This strikes me as a very plausible argument. And if it’s true, it suggests that the chances of a big Chinese crash are lower than many people realise.

Granted, even a 45% figure for household consumption isn’t really sustainable in the long-term. But it’s a much better place to begin a transition from, than the 34% official figure.

China looks cheap

Don’t get me wrong, there’s still a real risk that China could crash. But the point I’m making is that the risk is lower than widely thought.

And that matters, because right now, Chinese share prices look very cheap on many measures. That means they are pricing in a lot of potential drama.

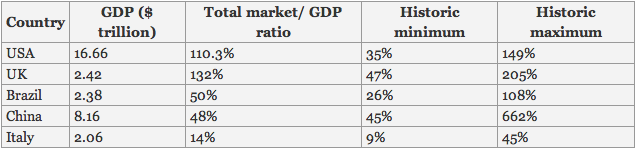

For example, look at the table below, which compares the value of a country’s stock market to its GDP.

Source: GuruWatch

Just to explain – the total market/GDP ratio is just the value of the country’s stock market expressed as a percentage of the economy.

As you can see, the US is currently on the high side compared to history (the total value of the stock market is a little bit higher than the value of the economy, compared to a historic maximum of 149%). The UK is somewhere in the middle of its historic range, and Brazil is on the low side.

But China – with a stock market valued at half of GDP – is only just above its historic low. (As is Italy, another market we’ve viewed as cheap for some time).

I have to say, this table certainly increased my own interest in investing in China. What’s more, Pictet Asset Management says that we’re now seeing early signs of improved corporate governance in the country.

How to profit from a Chinese rebound

So what’s the best way to profit from a smooth transition to a consumption-based economy in China?

Well, the lowest risk approach is to invest in Western companies that do a lot of business in China. I’m thinking of consumer goods giants such as Diageo (LSE: DGE) or Unilever (LSE: ULVR).

Or you could take a bet on growth in Chinese tourism. The number of visitors to Thailand has doubled over the last year, according to the China Market Research Group. And I’m sure that we’ll see many more Chinese tourists here in Britain in the future.

InterContinental Hotels Group (LSE: IHG) looks well placed to benefit as it has a decent estate of hotels in China, plus many more in other major tourist destinations.

If you have an appetite for taking more risk – and have more of an eye for a potential bargain – you could buy shares in Chinese companies themselves. The danger here is you may not trust the Chinese government to treat overseas shareholders fairly – and you’d be right to be cautious.

Still, I quite like the JP Morgan Chinese Investment Trust (LSE: JMC). It’s been running since 1993 and has managed to avoid some of the riskiest Chinese shares.

Moreover, 45% of the fund is invested in shares listed in either Hong Kong or Taiwan where the governance should be better and the risk lower. It’s also trading on a 13% discount, so in effect you’re getting £1 of assets for 87p. If sentiment changes towards China, not only could the underlying shares rise, but the discount will probably close too – boosting your returns.

• Stay up to date with MoneyWeek: Follow us on Twitter, Facebook and Google+

Our recommended articles for today

How to use the best minds in Britain to find blockbuster stocks

Some of the most exciting small-cap tech stocks have their roots in Britain’s world-class universities. David Thornton looks at one to keep an eye on.

Making sizzling profits from solar power

SUBSCRIBERS ONLY

The investment trend for cutting out the middle man is throwing up lucrative opportunities in solar power, say John Stepek and Matthew Partridge. Here’s how to profit.

In an excellent new piece entitled, “The growing 90% club and why gold production is going to go to zero”, Hinde Capital’s Co-Founder and CFO, Mark Mahaffey, asserts that it’s only a matter of time before world gold production goes to zero. That end-point is approaching quickly he implies, as the cost to pull an oz. of gold out of the ground is growing faster than ever before.

Here is an excerpt from Mark’s piece:

“If gold prices stay at the current levels for a prolonged period of time, do not be surprised if gold production falls much closer to zero. From an investor’s perspective it is a treacherous minefield. Of course, there are companies who really do have high grade ore reserves who can really claim to mine at $800/ ounce but these are very rare, maybe less than 5% of the 2000 quoted companies. The Northern Miner writes that out of their survey of 1400 Toronto listed firms, 721 currently have less than $200k cash in the treasury.

…read more plus the conclusion HERE

SNC Lavalin used to be the darling of brokerage firm analysts, garnering almost unanimous BUY recommendations from the Street for a number of years. Then, when it was revealed that a number of employees and officials of the firm were implicated in a bribery scandal, many of the analysts cut bait and ran. According to Bloomberg, seven analysts currently have a BUY on the stock, however six say it is a HOLD and one says that it is a SELL.

The bribery scandal news was serious, and it was not good. However, we at McIver Wealth Management have always believed it was first, and foremost, a governance issue and not an operations issue. During and following a number of investigations, there has been a wholesale replacement of officials at the firm.

Now that those associated with the scandal are gone, operations are once again the focus. That said, yesterday SNC cut their outlook and the stock fell a couple of percentage points. That would suggest that operations are weakening. However, upon closer examination, there are a number of one-time charges which contributed to that negative guidance.

Our Richardson GMP colleague Gareth Watson, appearing on BNN Television, stated that the appearance of one-time charges suggests that management is adamant about “cleaning house” as it move past the scandal. We would agree.

Another one of our holdings, Manulife Financial, went through a similar evolution following a difficult period for the company. Again, a number of analysts became neutral or negative on the stock. We were attracted by their “cleaning house” strategy in that it can provide a cathartic experience for the firm as it says goodbye to the previous regime and absorbs costs associated with old projects and divisions. No one is left to defend or rationalize the previous strategies or mistakes. The new management proceeds unhindered and with an objective and fresh outlook.

It is our hope that Manulife’s resulting good fortune can also be seized by SNC and it moves into a new era.

Both SNC Lavalin Group Inc. and Manulife Financial Corp. are held in the McIver-Jasayko Model Portfolios. Comments about these investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

With the fiscal negotiations kicked down the road for a couple of months and the idea of tapering pushed further out as well the S&P Futures made new all time highs!

The S&P is going into the close on its highs at 1728.50, rising an impressive 88.5pts since the recent low on October 9th.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair