Stocks & Equities

Few things are scarier for smart investors than buying when stock markets are at all-time record highs. With the S&P 500 (SNPINDEX: ^GSPC ) having soared to new records yesterday, sentiment among mainstream investors is unmistakably bullish. But subtler signs of nervousness have started to appear about the health of the economic recovery and the ability of the bull market to continue, raising fears that a stock market correction is imminent.

Ordinarily, investors can expect to see drops of 10% or more in the market roughly once a year, even in the context of an ongoing bull market. But the S&P 500 hasn’t suffered a 10% pullback since December 2011. With such a long period having gone by without a stock market correction, does it make sense to hold off on buying stocks in hopes of getting lower prices? Or should you go ahead and buy, risking getting mauled by a big bearish move?

Are you ready for what you’re wishing for?

Whenever there are extreme market movements in either direction, emotion starts to play a huge role in investing decisions. Extended and uninterrupted stock-market rallies, as we’ve seen throughout the past two years, leave those on the sidelines feeling increasingly worried that they’ve missed out on huge potential gains. This pushes them to invest even as higher share prices make stocks less attractive from a valuation standpoint. In that light, waiting for a correction might seem like the smarter move.

Yet, waiting creates two more challenges. First, you have to have the patience to stick with your decisions, and that can be difficult if the bull market rages higher. For instance, at the beginning of 2013, markets soared after lawmakers averted the threat of a huge tax increase on the entire American public. Those gains led some to decide to wait for a pullback before getting in. They’ve been waiting ever since, and the S&P 500 is now 20% higher.

Second, once the correction comes, you have to have the conviction to follow through with your original commitment to buy. That’s also a tough thing to do, because most stock market corrections hinge on some piece of exceptionally bad news that can make less secure investors question their entire investing plans.

Two smart moves to make now

What makes the most sense is never to stop investing entirely, even as markets keep rising, but also to keep your eyes open for better prospects if a stock market correction occurs. That way, you’ll benefit no matter which way the market moves.

When considering investments at near-record levels, it often pays to focus on areas of the market that most investors have neglected. Lately, consumer-staples stocks have gotten a huge amount of attention, with many investors turning to them for their reliable dividend income and defensive characteristics during pullbacks. Yet all the demand for dividend stocks has pushed their valuations up dramatically.

By contrast, commodity stocks, like gold miners and fertilizer producers, have gotten hammered. In the potash fertilizer space, PotashCorp (NYSE: POT ) and Mosaic (NYSE:MOS ) plunged during the summer when a key player in the global potash market backed out of a cartel agreement with its main partner, spurring speculation that potash prices would drop severely. It’s true that neither Mosaic nor PotashCorp owes its entire fortune to the potash industry, given that both also make other products that don’t rely on potash. Yet, short-term traders sold first and asked questions later, expecting the worst, and not wanting to get caught up in ongoing drama in the industry. For long-term investors who can afford to handle near-term uncertainty, the arguments favoring greater demand for crop-enhancing products like potash remain unchanged, and that should help Mosaic and PotashCorp recover eventually. That makes the two stocks worth looking at for their potential value opportunity.

At the same time, though, it also makes sense to look for stocks you’d want to buy if a stock market correction actually happens. Procter & Gamble (NYSE: PG ) has a lot of growth potential from global markets, but at 21 times trailing earnings, the shares reflect a premium for its 3% dividend yield and reputation as a defensive stock. Investors appreciate P&G’s brand success and its reliable demand from customers who see its products as essential staples. But paying too much for even the highest-quality consumer stock doesn’t make sense, especially when Procter & Gamble hasn’t yet delivered on its promise to expand its earnings power more rapidly. After a stock market correction, though, P&G shares could look a lot more attractive for the long run.

Be correct about a correction

Stock market corrections happen, and it pays to be ready for them. But you also have to be ready for them not to happen on any predictable time frame. Your best solution includes making the most of current opportunities while also setting the stage to jump on cheaper stocks when they emerge.

Start investing today!

Letting the lack of a stock market correction keep you from investing entirely would be a big mistake. Millions of Americans have done exactly that, waiting on the sidelines since the market meltdown five years ago and therefore missing the big bull market that followed. You can learn more about how to overcome your fears and invest by reading our brand-new special report, “Your Essential Guide to Start Investing Today.” Inside, The Motley Fool’s personal finance experts show you why investing is so important, and what you need to do to get started. Click here to get your copy today — it’s absolutely free.

Tune in to Fool.com for Dan’s regular columns on retirement, investing, and personal finance. You can follow him on Twitter @DanCaplinger.

About Dan Caplinger

Wall St Analyst Crams 700 Years Of Data Into Bearish Call On US Stocks

“The starting point of any financial analysis must surely be a consideration of the economic cycle: not just where we stand within the current cycle, but more importantly, where that cycle fits within broader economic history,” writes Paul Jackson in his final note to clients in his role as an equity strategist at Société Générale.

The note — titled “Swan song: 12 pictures you can’t ignore” — builds on the bank’s recent call for clients to rotate out of U.S. stocks and into European stocks. The SocGen asset allocation team predicts the S&P 500 will fall by around 15% when the Federal Reserve winds down its quantitative easing program, then go nowhere for years.

“For now, equity valuations in Europe are attractive and with a bit of economic growth the next few years could be quite rewarding,” says Jackson. “The immediate risks are that growth does not materialise in Europe or that the eurozone project unravels. For the longer term I worry more about latent inflation risks and central banks getting behind the curve. As bond markets react to that policy error, the folly of forcing banks, insurance companies and pension funds to hold so many bonds will become apparent. But that is for another day.”

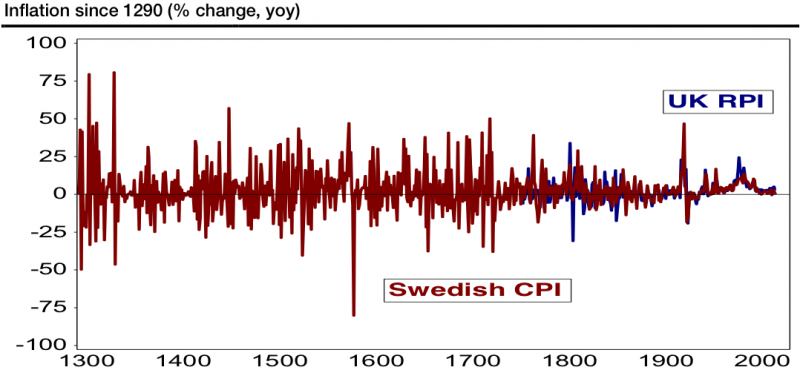

1. Current inflation trends are boringly normal.

“Inflation may feel low compared to the history through which most of us have lived, but in a broader context it is boringly normal,” says Jackson. “Maybe without recent extra-ordinary policy settings, we would now be experiencing deflation, but we will never really know.”

…read and view much more HERE

2. Inflation has little effect on stock market valuation.

3. History suggests low returns ahead for U.S. stocks.

4. U.S. companies may be in for disappointment.

5. Europe’s economy has room to improve.

6. A better European economy means better European profits.

7. European stocks look attractive.

8. Many metrics suggest Europe is undervalued.

9. The real bubble is in the bond market.

10. The ECB’s balance sheet has been shrinking for a while.

11. The euro is getting a boost from ECB inaction.

12. The question is what happens when the Fed pulls back.

- The “most hated metal” tries for a big comeback

- Miners search for a bottom

- Plus: Will Netflix doom Q4 momentum?

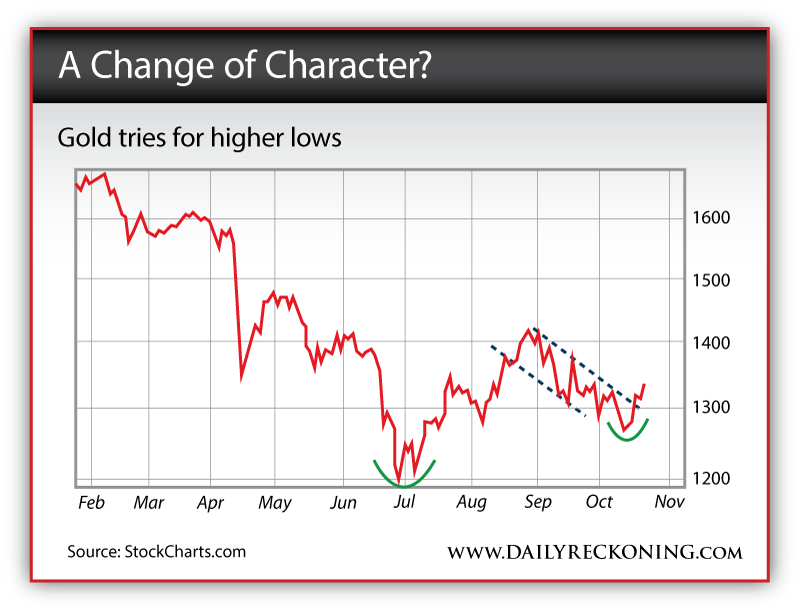

Over the past week, gold has gone from zero to hero, breaking off an $80 run in just five trading days.

I’ve been bearish on gold since earlier this year. But I think this move could have legs. In fact, gold stocks might even move significantly higher before we finish out the year.

Here are the clues indicating gold might be undergoing a change of character:

1. Fakeouts lead to breakouts

On Oct. 15, gold futures plummeted to a low of $1,251. This drop signaled a clear break below critical support at $1,275. That morning, it looked like the floor was about to drop out. I suspected gold futures would soon test their late June lows of $1,179…

That’s when buyers stepped in. Futures haven’t looked back since. Here’s where we stand now:

After faking a move lower, gold futures have broken above resistance, posting the first higher low since early July. This could be a significant short-term bottom—especially since it was preceded by a false move lower.

2. Miners try for a double-bottom

If you want to find an asset class performing worse than gold this year, look no further than gold miners. Investors have slammed these stocks. The group is down nearly 44% on the year. No one wants these stocks…

However, the chart is beginnign to look constructive…

The miner to metal ratio has been dismal all year. If this bottom holds, we could see miners snap back in a big way…

3. Sentiment is in the gutter

Just 10 days ago, CNBC’s gold sentiment survey revealed 83% of those surveyed were expecting prices to fall. That’s way too lopsided. Whenever you see sentiment get to these extremes, it’s time to start looking for a big move in the opposite direction.

So what happens next?

I think gold (and miners) can move higher from here. It will messy. There will be big down days mixed with the intial thrusts higher. But right now, gold appears to be setting up for a solid fourth quarter.

I’m not ready to declare blue skies and new highs in gold’s future just yet. But something is brewing right now that could spark a significant move. If you’re nimble and you don’t mind big swings in both directions, this is your time to trade…

Regards,

Greg Guenthner

for The Daily Reckoning

As long-time readers of The Rude Awakening know… Greg is no gold bug. In fact, this is his first bullish gold prediction all year. So when he changes his tune, it’s time to stand up and take notice. And rest assured, he’ll be following this story very closely in the days to ahead. So you’ll want to get his analysis before anyone else. Sign up for The Rude Awakening, for FREE, right here, and stay one step ahead of the rest of the market.

In the 13th century, Marco Polo wrote with utter astonishment at the paper currency standard he witnessed in China:

“[a]ll these pieces of paper are, issued with as much solemnity and authority as if they were of pure gold or silver… and indeed everybody takes them readily. . .”

In the Europe of Marco Polo’s day, ducats and florins were considered money by anyone with half a brain.

Yet today, this paper currency system has come to dominate our world. We’ve handed total control of the money supply to a tiny banking elite.

These central bankers never once stand for election. And despite the tremendous power they wield, citizens still think that they live in a democratic republic. Very curious indeed.

Yet while this entire concept of paper currency is deeply, deeply flawed… there are some currencies which are more flawed than others.

When evaluating a paper currency, it’s imperative to first look at the financial condition of its issuing authority– in this case, the central bank.

The US Federal Reserve and European Central Bank, for example, are in worse condition than Lehman Brothers when that bank went bust in 2008. This makes the dollar and euro quite risky to hold.

But there are other currencies in even worse shape. Let’s examine a few of them:

1) Canadian dollar

1) Canadian dollar

This one is a shocker for most people; Canada is often considered the darling of Western currencies because (so goes the conventional wisdom) the Canadian economy is strong and natural-resource based.

But if you look at the health of the central bank, Canada wins the award for LEAST capitalized central bank in the west, posting razor thin equity of just 0.53% of total assets.

Given that currency is nothing more than a liability of a central bank, the bank’s poor financial condition weighs heavily on the currency’s resilience.

2) Mexican peso

Mexico’s central bank is actually insolvent. And this is another shocker for those keen to invest in one of Latin America’s largest economies.

In their most recent annual report, Mexico’s central bank posted NEGATIVE equity of 73 billion pesos.

In fairness, this is not an enormous sum of money; however, the amount is growing. And there’s going to come a time when the government will be forced to bail out the central bank.

Yet Mexico’s government is already running a steep budget deficit. And the country’s public debt has been growing rapidly. So the trend clearly shows further deterioration in the fundamentals.

3) Japan

Talk about a train wreck. The Bank of Japan is already in a weak financial position, with net equity of just 1.9% of total assets.

But Japan’s government is forcing them into the most unprecedented monetary expansion in a central banking era where using the word ‘unprecedented’ has become commonplace.

46% of the Japanese government’s budget is financed by debt. Most of this is mopped up by the central bank.

Yet as the government’s debt level already exceeds 200% of GDP, the gross interest payments alone eat up more than 50% of tax revenue.

Japan has no hope of getting out of this alive. The only way out is default, or a currency crisis. Neither of these cases makes the Japanese yen an attractive option to hold.

This list is not exhaustive– the Brazilian real, British pound, etc. also exhibit the same fundamental weaknesses.

As to the ‘healthy currencies’ out there? Norway’s krone is by far the safest currency from a technical perspective; its central bank is the best capitalized on the planet

(Premium members: please refer to your welcome kit for instructions on how to open a Norwegian bank account.)

The Hong Kong dollar also gets high marks, but for unique reasons. More on this in a future letter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair