The Greatest Trader Who Ever Lived

The Greatest Trader Who Ever Lived

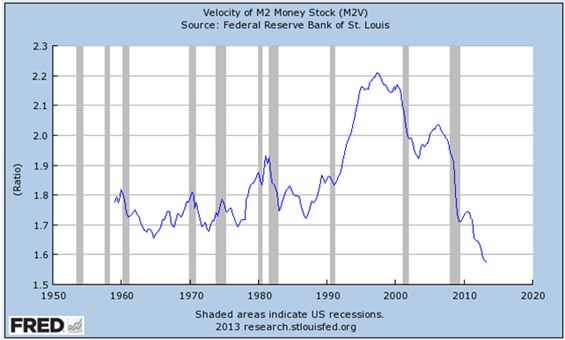

The Fed is trying to stoke inflation and lower unemployment through its bond-buying scheme. Attempting to solve a non-monetary problem (unemployment) with monetary tools (interest rates) has not been and likely will not be successful.

To be fair, there are some nascent economic bright spots. Industrial base expansion, capacity utilization, Purchasing Managers Index data and related metrics are improving globally. It remains to be seen, however, if this can be sustained.

The other side of The Economic Tug-of-War is the emerging world growth story. I remain very bullish on the long-term prospects in the developing economies despite the slowdown in growth rates across the region. According to The Economist, for 18 of the past 20 centuries, India and China combined had the largest GDP in the world. When viewed through this prism, the current slowdown is a mere blip.

Much of the debate surrounding emerging world growth centers on China (as it should). We know that the official (and debatable) growth rate of the Chinese economy is 7.8%. Despite the fact that the economy isn’t growing at double-digit rates anymore, China is a much larger economy than it was even a few years ago. So you’re seeing slower growth, but from a much larger base. There are numerous challenges the country faces, including reigning in shadow banking, pollution control and shaky demographics, but I still believe the country serves as a model for the shift in economic power we’re seeing from West to East.

What is the takeaway for a junior mining investor? In the near term, you can expect the uncertainty and volatility to continue. With no specific reason for commodities to rocket higher in the near term as a group, this offers you the most valuable commodity of all—time—to take a closer look at select commodities and their trajectories.

TMR: What types of juniors are going to be rewarded by this type of market?

CB: As an investor in the sector, my top priorities are to identify juniors with the best financial sustainability and the best financial management. Financial sustainability is about having a clean and strong balance sheet. I want to see cash. I want to see liquid assets. I want to see a company that can stay away from debt instruments like convertible bonds, short-term debt or anything more exotic. In this market, I view balance sheet debt as a red flag. It’s important to remember that all debt must be serviced, or repaid. When a company repays debt, they are not drilling or advancing a project forward. It’s hard to see share price appreciation when a company must focus on rewarding creditors instead of shareholders.

Of course, with so many variables out of our control, the depth of experience of management and their ability to navigate through these environments and focus on shareholder returns is extremely important.

Despite the challenging environment, there are excellent opportunities hidden in the sector. We are still active in the space and we think that for patient investors, it’s an interesting place to be because many of these companies have promising assets. Because the whole sector is under pressure, many of the better juniors are being ignored. This won’t always be the case, which again is why it’s important to look at the space with a two- to three-year window. If you think the world will be smaller in the future and commodity demand will not increase, this isn’t the space for you. If you believe the opposite, as I do, then now is the time to conduct thorough analysis.

TMR: In some of your recent writings, you look to the future and see continued global urbanization. Given the tug-of-war between developed and emerging economies, do you still see a valid investment thesis in the commodity sector?

CB: Absolutely. There have been several articles in newspapers recently reporting on the sustainability and evolution of global urbanization. The basic point is that society needs to look beyond “growth for growth’s sake.” In other words, quarterly GDP only tells part of the story; it doesn’t reveal the total societal costs to get that number. The New York Times has published images of Beijing and Harbin where the citizens can’t see three feet in front of them at mid-day. The pollution is almost acting as a drag on economic growth and this is unacceptable to the powers that be in China. Yet urbanization will continue and evolve. The authorities in China will achieve growth rates no matter what, but increasingly more attention will be paid to growing in a more sustainable, cleaner and greener fashion.

The investment case for many of the energy metals I follow, like graphite, rare earth elements (REEs) or cobalt, is even more compelling given what I mentioned above, but has been muted due to a slowdown in global growth rates. It’s a long-term thesis. China will continue to face extreme environmental pressures if it continues to develop using the same roadmap. Improving quality of life in the emerging economies is an investment theme that continues to be valid.

TMR: What are some examples that are outperforming the market?

CB: Of the juniors that I follow in the lithium space, my favorite is Orocobre Ltd. (ORL:TSX; ORE:ASX). This company has a diversified business model. They are developing a lithium project in South America. They have also acquired a borates business from Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK). The diversity in the business model is a selling point. The company is on the verge of adding to the global lithium supply with a fully funded project in Argentina, which is a tough business to break into.

Northern Graphite Corporation (NGC:TSX.V; NGPHF:OTCQX) remains among the leaders in the graphite space. The company, deposit and project economics are all well known and the economics, in particular, have improved. Production of value-added products like spherical graphite can help solidify margins. The current challenge for the company is the need to raise adequate initial capital (roughly $100 million) to build the mine and achieve commercial production. There are a number of other graphite companies with various economic profiles and costs, but we like this one because it’s so far ahead of the others and has a real chance to shine in a risk-off environment.

TMR: Is Northern Graphite considered a near-term production story?

CB: Near-term production probably means different things to different people, but yes, I believe it is. The current production target is 2015. In the graphite space, that’s near-term production because few other companies are realistically as close.

Flinders Resources Ltd. (FDR:TSX.V) is another near-term production story in graphite with numerous strengths. The company’s geographic proximity to graphite users in Europe can keep a lid on transportation costs, whereas the flake size distribution of the deposit and scalability offer the opportunity to sell graphite to a diversity of end users. The fact that this mine was a past producer should give investors added comfort. The project capex is much lower than any other project I’ve seen up to this point. Both Flinders and Northern Graphite are substantially derisked, near-term producers that I believe are relatively undervalued—even in this depressed market.

TMR: Since you mentioned depressed markets and energy metals, I wanted to get your impressions from the U2013 Global Uranium Symposium you attended and reported on in your newsletter. How has your view on the uranium market evolved and have your investment plans changed?

CB: I’m a long-term optimist on uranium. However, I’m neutral in the near-term. There are several reasons for this. The extreme effect of the Fukushima accident on investor psychology for the entire industry has really given many pause regarding just how positive the future for nuclear energy is. At the conference, a panelist talked about the psychological effects of nuclear accidents lasting for a generation in the psyche of investors and stakeholders. Never mind the facts. Never mind that nuclear energy is still the cleanest most reliable form of baseload power available. Fear can be a powerful motivator. By now, a lot of people, myself included, thought that Japan would have restarted at least some of its reactors. That hasn’t happened for a number of different reasons. I believe 14 reactors in Japan are being inspected for re-start and so we are inching closer. Some of the uranium that would have powered Japan’s reactors has hit the market and has created a glut. That will take time to work through.

Regardless, the fact is that the spot uranium price is near $35 per pound ($35/lb) and the forward price closer to $50/lb. I’m not worried about a short-term price of $35/lb, but it does affect what I will invest in at this stage of the cycle. I am more interested in the global uranium demand in two or three years. The ultimate demand for uranium from new reactors coupled with the need for the current global reactor fleet to be refueled dictate a higher price for uranium in the coming years, which should add leverage to the share prices of those uranium juniors that are near-term production stories.

Another way to invest in the nuclear power generation thesis is through new reactor technology. One example is small modular reactors, or SMRs. Building a full-scale nuclear reactor can cost billions of dollars and take more than a decade. A modular nuclear reactor has a dramatically lower upfront capex. Modular reactors can be shipped in manageable pieces by rail. In some designs, the reactors are encased underground and offer passive safety systems (they shut themselves down). It is an interesting evolution in technology and we are following companies like Babcock & Wilcox Co. (BWC:NYSE) that are leaders in that space. Full-scale adoption of the technology is not imminent but numerous parties, including the U.S. government, have shown interest.

A current favorite uranium junior is Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.MKT). The company anticipates production in Wyoming within a year. It has three, five-year offtake contracts in place with two separate operators. So once production commences, cash flow will follow. The exact prices Uranerz will receive are confidential, but even at current long term contract prices of $50, Uranerz can operate profitably.

Because this is in-situ mining, the cost of production and environmental impact is much lower relative to traditional mining methods. A company like Uranerz can exist and thrive in a low uranium price environment. Any uptick in the uranium price provides leverage. That should add to the company’s margins and, as contracts lapse and are re-negotiated, should encourage a higher share price in the future.

TMR: So your recommended strategy for investors interested in the uranium space would be to get started on due diligence in both new technologies and near-term production stories. And then be ready to act as the markets improve.

CB: Yes. It is instructive to look at the situation that the United States finds itself in regarding uranium fuel supply. The U.S. has approximately 100 reactors. A couple of them have received a lot of press for announcing plans to close—one in Vermont and then one in California. Unfortunately, these stories grab headlines but miss the larger point of the necessity to provide reliable and affordable electricity to the grid in the U.S. It would make eminently more sense to rely on a domestic source of critical fuel and to embrace and develop new nuclear technologies on our own soil. Most of the uranium used in the United States comes from outside the country. Now that ARMZ has taken Uranium One private, the Russians are one of the largest producers of uranium in the United States. This is not widely known. That should make some people in Washington D.C. uncomfortable.

TMR: Is there anything novel that you’re hearing on conference calls or reports? Are there trends that the mainstream financial media is missing?

CB: One positive ongoing development in the mining sector is the evolution of cost reporting, especially by the majors. There’s always a lot of confusion around what it actually costs a specific company to get an ounce or pound of a commodity out of the ground. More detailed numbers are becoming more common through reporting of “all in sustaining costs”. These metrics aren’t perfect, either, but do give investors a clearer picture of a company’s cost structure. These metrics also have significant implications for the financials of a company. I pay particular attention when companies talk about changes in cost structure or tax rates, for example.

I also listen for clues to future growth projections. Specifically, where is a company seeing growth? In a number of the calls I have listened to recently, CEOs are becoming more optimistic about the prospects for the European Union. This is in stark contrast to recent quarters where the EU economic contraction has served to hurt company bottom lines. This trend appears to have changed and is an example of the type of analysis I do to come to the conclusion that the global economy has bottomed.

Another trend I follow concerns R&D spending patterns. R&D spending drives innovation, which leads to new products and ultimately to new markets. As integrated as global supply chains are, achieving “first mover” status with a new product or market can deliver immediate benefits to the bottom line. Diversification of revenue streams is also a positive. For example, W.R. Grace & Co. (GRA:NYSE) is rolling out new fluid cracking catalysts. That could have implications for the REE space. Gaining an understanding of these products and the amount and types of REEs they use can help gain a better understanding of the overall REE demand picture going forward.

A final indicator I look for in earnings calls is to make sure a company is maintaining or increasing market share. I want to see a company that is focused on being first or second in the world in a specific line of business. These are the sector leaders that typically have pricing power and have achieved economies of scale. A good case study is Rockwood Holdings Inc. (ROC:NYSE). It is the number-one lithium compound producer in the world. Developing trends in the lithium market are likely to be evident in their earnings calls and investor communications.

TMR: In parting, do you have any words of wisdom, or even a pep talk, for junior investors so they can keep their heads up and not miss the inevitable upswing?

CB: Don’t lose your nerve. This is a cyclical business. It always has been and it always will be. Across the entire commodities space we are going to need more of everything, not just to survive, but to prosper in the future. I still believe that the commodity super cycle is intact, despite the subdued commodity price environment. The super cycle looks as though it will become more consumption-centric rather than investment-centric.

Technology will also play a role. New markets will be created, spurred by R&D, and this will create opportunities for investors in and around the commodities sector. But it will be a stock pickers market. It’s not a market where you can just invest in XYZ graphite company and watch it appreciate in price. Going forward, a diversified portfolio of select companies across the right metals and minerals will serve the patient investor very well. It’s just a timing issue. Again, we’re at the bottom of the cycle right now: it’s time for voracious due diligence.

TMR: As always, it has been great to talk with you.

CB: Looking forward to speaking with you in the future.

Chris Berry, with a lifelong interest in geopolitics and the financial issues that emerge from these relationships, founded House Mountain Partners in 2010. The firm focuses on the evolving geopolitical relationship between emerging and developed economies, the commodity space and junior mining and resource stocks positioned to benefit from this phenomenon. Chris holds an Master of Business Administration in finance with an international focus from Fordham University, and a Bachelor of Arts in international studies from The Virginia Military Institute.

Want to read more Mining Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit The Mining Report.

DISCLOSURE:

1) J. Alec Gimurtu conducted this interview for The Mining Report and provides services to The Mining Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Mining Report: Northern Graphite Corporation and Uranerz Energy Corp. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Chris Berry: I or my family own shares of the following companies mentioned in this interview: Northern Graphite, Flinders Resources and Uranerz Energy. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Michael has yet to hear a single realistic proposal from Big Environment Groups as to how we will get the energy we use, where we will get the increasing amounts we’ll use and how we are going to transport it. The other major issue concerns employment in that sector….

Michael has yet to hear a single realistic proposal from Big Environment Groups as to how we will get the energy we use, where we will get the increasing amounts we’ll use and how we are going to transport it. The other major issue concerns employment in that sector….

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}