Timing & trends

Congress’s latest attempt at crafting a budget plan is on track to end up the same way as others have in the past decade: with little or no agreement.

Negotiators have little chance of breaking this string of futility, even after a 16-day government shutdown in October that cost the U.S. economy $24 billion. If they do, it’ll only be to curb automatic spending cuts, including $19 billion that hits the Pentagon starting in January.

Now budget experts, labor unions and business groups are saying enough’s enough, and questioning why lawmakers can’t live within their means the way ordinary Americans do and instead lurch from one budget standoff to the next.

“It’s a stupid way to run a country,” said Maya MacGuineas, head of the Campaign to Fix the Debt, a non-partisan advocacy group whose members include business leaders and former lawmakers. “Change comes from two possible things: a crisis or leadership.”

One of the co-chairmen of the campaign is Michael Bloomberg, founder and majority owner of Bloomberg News parent Bloomberg LP and the New York City mayor.

Unlike with previous budget panels, including the failed 2011 supercommittee, there are no immediate consequences if the budget conference misses its Dec. 13 deadline — the U.S. won’t default on its debt and the federal government won’t shut down for lack of funding.

The committee’s lack of progress is frustrating outside groups, especially business executives, who say congressional lawmakers’ habit of governing by crisis and temporary spending bills is hurting the economy and costing jobs.

‘Chilling Effect’

“The uncertainty has a chilling effect on job creators, households and anybody who’s trying to see around a corner,” said MacGuineas, who is also president of the Committee for a Responsible Federal Budget, a fiscal advocacy group.

Congress in 2009 last passed a budget resolution, the equivalent of a household budget that sets spending parameters for the federal government.

In 2010, disagreement over how to handle the scheduled expiration of tax cuts enacted under former President George W. Bush prevented agreement on a budget resolution and Republicans won the House majority, creating a divided Congress.

The current panel is the fifth bipartisan attempt in three years to address the nation’s debt and deficit. The others, starting with the 2010 debt-reduction commission appointed by President Barack Obama, ended in failure.

….continue reading on HERE

Warren Buffett is the most famous investor in the world. He also loves sharing his advice with kids as part of his Secret Millionaires Club.

Warren Buffett is the most famous investor in the world. He also loves sharing his advice with kids as part of his Secret Millionaires Club.

The following are questions he answered in a recent interview, including what he thinks the biggest mistake is that parents make when teaching their kids about money and how he learned about money.

Do you think most parents do a good job teaching their kids about money?

Buffet: Most parents know how important it is to teach kids about money and managing it properly. There was a study many years ago questioning how to predict business success later in life. The answer to the study was the age you started your first business impacted how successful you were later in life. By teaching kids sound financial habits at an early age, gives all kids the opportunity to be successful when they are an adult.

What do you think is the biggest mistake parents make when teaching their kids about money?

Buffet: I think parents need to start teaching kids about the importance of managing money at an early age. Sometimes parents wait until their kids are in their teens before they starting talking about managing money when they could be starting when their kids are in preschool.

What made you want to launch the Secret Millionaires Club? What do you hope kids get out of it?

Buffet: There are a number of educational programs out there, but there are not many programs that teach about Financial Literacy at an early age. Secret Millionaires Club can help kids develop the right habits that will serve them well for the rest of their life. If this program can have some effect on youngsters and help them develop better habits on money, it can have a major impact on their life when they are older.

Where did you learn about money?

Buffet: My dad was my greatest inspiration. He was my hero when I was six and he is still my hero now. He is an inspiration to me in every way. What I learned at an early age from him was to have the right habits early. Savings was an important lesson he taught. I had all kinds of small businesses when I was growing up. When I was six I started my first business. I bought a six pack of Coke for 25 cents and sold the cans for a nickel apiece. I also sold magazines and gum door to door.

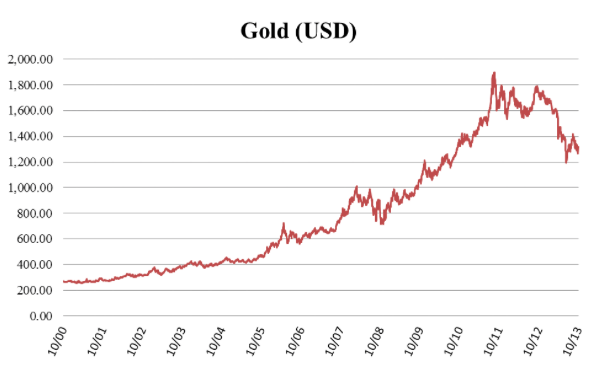

Given the fact that the asset class of precious metals, and more generally commodities became the easiest pick for investors over the latest decade, we really shouldn’t be that perplexed with the idea of how quickly it has now been shunned by the masses. As the price of gold continues in a downtrend, the widely popular SPDR Gold Trust ETF is seeing its lowest levels since 2009. But since the final surge in the price of gold was driven by a herd mentality amongst investors to protect against a stimulus program so complex it was difficult to comprehend, it’s reasonable an asset class associated with fear and uncertainty became a safe harbour of capital. More recently though, what believers of gold and other precious metals learned is the price can go down as quickly as we saw it go up, and that’s not to acknowledge that gold was in a bubble, or by some analysts’ definition has entered a bear market, but perhaps instead, a short period of consolidation.

Given the fact that the asset class of precious metals, and more generally commodities became the easiest pick for investors over the latest decade, we really shouldn’t be that perplexed with the idea of how quickly it has now been shunned by the masses. As the price of gold continues in a downtrend, the widely popular SPDR Gold Trust ETF is seeing its lowest levels since 2009. But since the final surge in the price of gold was driven by a herd mentality amongst investors to protect against a stimulus program so complex it was difficult to comprehend, it’s reasonable an asset class associated with fear and uncertainty became a safe harbour of capital. More recently though, what believers of gold and other precious metals learned is the price can go down as quickly as we saw it go up, and that’s not to acknowledge that gold was in a bubble, or by some analysts’ definition has entered a bear market, but perhaps instead, a short period of consolidation.

It’s not just because of my bias from being in the industry that I believe this Bull Run in gold is far from over. If the chart above illustrates anything, it’s that this market over the last ten years still looks rather healthy. Instead, there are some very distinct reasons why for the long term we can still be bullish on gold despite the noise we see here in the short term, and they are as follows:

- – Outlook is for record low federal funds rate (interest rates) into 2016

- – Taper of Quantitative Easing does not equate to tighter policy

- – Global recovery still remains fragile as the fiscal health governments is no better off than before the crises

The outlook for interest rates along with the fact that any upward manoeuvre in policy rates still remains the upmost threat to economic growth is what has fuelled demand for real assets over the last few years. Furthermore, record low rates have fuelled a consumption binge in the world’s developed economies that now sees the general population saddled with record debt levels. And it’s simple; in order to reign in household imbalances individuals must either save more and consume less, or grow their incomes at a faster rate than their debt. The premise now that we live in a global economy with sub-par 2 percent economic growth is what will constrain individuals and force policy makers to keep rates low for the foreseeable future.

And it’s the Federal Reserve and other central banks that offer the guidance of low rates that will continue to stimulate the economy. We are beginning to learn, and soon accept that the unconventional methods of quantitative easing have run their course. And given the improvement in the US labour market is far less than the US central banks hopes for at this point in the recovery, it’s even more evident this pending policy shift speaks more to the efficacy of its efforts than its arguably somewhat satisfactory achievements.

But finally, and this is the one point surrounding gold that almost everyone seems to have forgotten as of late, and that is the debt burdens of government that seemed to be of paramount focus during and before the great recession are no longer relevant. Paradoxically, they are actually worse than when we entered this crisis five years ago. Despite the efforts of massive stimulus programs from just about every western power, the worlds developed economies actually haven’t returned to full strength, and are even more burdened as a result of the stimulus.

And that quite simply is what kick-started gold’s run back in the beginning of this century. It wasn’t quantitative easing. And for over two years between July of 2004 and November of 2006 interest rates actually went up. But a mix of the aforementioned factors paired with the ineffectiveness of government that opts to devalue their currency in order to attempt to stimulate growth is what will eventually turn around this downturn in gold, and fortunately for some investors has created the buying opportunity of the decade.

This is a review of Technology, Materials, Consumer Discretionary, Industrials, Energy, Financials, Consumer Staples, Health Care & Utilities:

Technology

· Trend remains up (Score: 1.0). Units closed at a 13 year high on Wednesday

· Units remain above their 20 day moving average (Score: 1.0)

· Strength relative to the S&P 500 Index changed from negative to neutral (Score: 0.5)

· Technical score based on above indicators improved to 2.5 from 2.0 out of 3.0

· Short term momentum indicators returned to overbought levels.

Materials

· Trend remains up. Resistance is forming at $46.07.

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index remains negative

· Technical score remains at 2.0 out of 3.0

· Short term momentum indicators are rolling over from overbought levels

Consumer Discretionary

· Trend remains up. Units closed at an all-time high on Wednesday

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index changed from neutral to positive

· Technical score increased to 3.0 from 2.5 out of 3.0.

· Short term momentum indicators returned to an overbought level

Industrials

· Trend remains up. Units closed at an all-time high on Wednesday.

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index improved to positive from neutral

· Technical score increased to 3.0 from 2.5 out of 3.0

· Short term momentum indicators have returned to overbought levels.

Energy

· Trend remains up.

· Units fell below their 20 day moving average on Wednesday

· Strength relative to the S&P 500 Index remains negative

· Technical score fell to 1.0 from 2.0 out of 3.0

· Short term momentum indicators have rolled over from overbought levels.

Financials

· Trend remains up.

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index remains positive

· Technical score remains at 3.0 out of 3.0

· Short term momentum indicators are overbought.

Consumer Staples

· Trend remains up. Resistance is forming at $43.46

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index changed from neutral to negative

· Technical score slipped to 2.0 from 2.5 out of 3.0

· Short term momentum indicators are rolling over from overbought levels.

Health Care

· Trend remains up

· Units remain above their 20 day moving average

· Strength relative to the S&P 500 Index remains positive

· Technical score remains at 3.0 out of 3.0

· Short term momentum indicators are overbought.

Utilities

· Trend changed from up to down on a move below $38.18

· Units remain below their 20 day moving average

· Strength relative to the S&P 500 Index remains negative.

· Technical score dropped to 0.0 from 1.0 out of 3.0

· Short term momentum indicators are trending down.

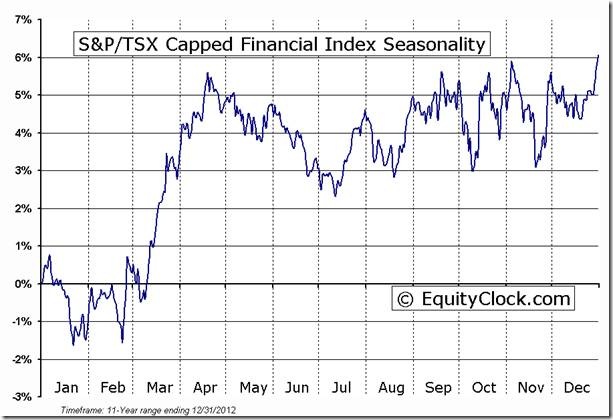

SEASONALITY: Equityclock.com offers free access to seasonal studies on over 1000 big and moderate cap securities and indices, most that have been updated very recently.

To login, simply go to http://www.equityclock.com/charts/

Following is an example:

S&P/TSX Capped Financial Index Seasonal Chart

In our essay on precious metals from Nov. 22, we focused on the markets from the long-term perspective. As we wrote in the summary:

(…) the final bottom for the decline in gold, silver and mining stocks doesn’t seem to be in just yet.

On the next trading day, after the essay was posted, gold, silver and mining stocks declined and dropped to their fresh monthly lows. Although we’ve seens some improvement in recent days, precious metals still have been trading in the narrow range.

Many times in the past, the situation in the U.S. dollar and the euro gave us important clues about future precious metals’ moves. Therefore, today we’ll examine the US Dollar Index (from many perspectives) and the Euro Index to see if there’s anything on the horizon that could drive the precious metal market higher or lower in the near future. We’ll start with the long-term USD Index chart (charts courtesy byhttp://stockcharts.com).

From the long-term perspective, the situation hasn’t changed much recently. The long-term breakout above the declining long-term support line has not been invalidated. Additionally, the USD Index reversed right in the middle of our target area. Therefore, from this perspective, it seems that the downward move – if it’s not already over – will be quite limited because the long-term support line will likely stop any further declines.

Now, let’s examine the weekly chart.

Looking at the above chart, we see that at the beginning of the month the USD Index reached the 50-day moving average, which triggered a corrective move in the following weeks. With this downward move the U.S. dollar dropped to the low that we had seen three weeks ago, therefore, we might see a post-double-bottom rally in the coming weeks.

Keep in mind that from this point of view the current correction is still shallow, which is a bullish signal for the short term. As you can see on the above chart, recent weeks have formed a consolidation, which is likely a pause before further increases.

Let’s check the short-term outlook.

As you can see on the above chart, the USD Index extended its decline and dropped to the previously-broken support/resistance line created by the June low. Last week, the proximity to this support level (or comments from the Fed about the possibility of tapering the QE program – which we don’t believe, by the way) triggered a sharp move up, which took the dollar above the level of 81 once again. Therefore, since this level was reached once again, it seems that we might see a similar rally once again. Additionally, the greenback formed a daily hammer (reversal) candlestick, which is another bullish sign.

On top of that, both happened right after the cyclical turning point, which amplifies their bullish implications. Connecting the dots, it seems that another move up could be seen shortly.

Let’s now take a look at the medium-term Euro Index chart.

As you see on the above chart, since the beginning of the week, the euro has continued its rally. The Euro Index moved above the level of 135 once again and corrected exactly 61.8% of its October-November decline (to 136.09).

At this point, it’s worth mentioning the short-term rising support line based on the July and September lows, which is slightly above the 61.8% retracement. Looking at the above chart, we clearly see that despite the recent corrective upward move, the breakdown below this line hasn’t been invalidated.

Combining these two facts, we can conclude that the move up is quite likely over and the decline can continue. If we see a move below 131.56, the bearish implications will be even stronger.

Having discussed the current situation in the U.S. currency, let’s see how it may translate into the precious metals market. Let’s take a look at the Correlation Matrix.

The Correlation Matrix is a tool which we developed to analyze the impact of the currency markets and the general stock market upon the precious metals sector (namely: gold correlations and silver correlations).

The correlation coefficients remain strongly negative as far as the short-term (30 trading days) link between precious metals and the USD Index is concerned. The 10-day column includes values close to 0, which simply means that gold didn’t respond to dollar’s move lower – which is a bearish sign.

Summing up, looking at the current situation in both currencies, we are likely to see weakness in the Euro Index and improvement in the USD Index on a short-term basis. As mentioned earlier, the USD Index reached its cyclical turning point and, taking this fact into account, it seems that the bottom of the current correction is already in. Additionally, the euro corrected exactly 61.8% of its October-November decline and approached the short-term rising support line without breaking it, which means that the move up is quite likely over. Therefore, currently, the implications for the precious metal market are bearish.

Thank you for reading. Have a great and profitable week!

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Tools for Effective Gold & Silver Investments – SunshineProfits.com

Tools für Effektives Gold- und Silber-Investment – SunshineProfits.DE

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair