Timing & trends

Well friends, it’s the holidays again, so I figured it’s not a bad time to write about one of the coolest new toys to hit the market in years…

…The defense market, that is.

You’ve probably been reading more and more about the dramatic expansion of the use of robot technology on the modern battlefield.

The most famous of these are the Reaper drones – for which the Air Force is currently training more personnel than for any other single weapons system.

But while Reapers are great for hitting targets (usually enemy combatant in nature) from afar with things like Maverick air-to-ground missiles and 500 lb GPS guided bombs, the Army now has its own ground-based killer robot system to do what infantry have long referred to as “grunt work.”

Behold, the MAARS:

MAARS, which stands for Modular Advanced Armed Robotic System, is the start of a new trend in surface combat for the U.S. Army.

Adding Teeth and Claws to an Existing Concept

While robots have been used for years to take high-risk pressure off troops – namely in bomb disposal and rescue applications, where human safety is likely to be compromised – the MAARS takes it a step further, doing something which Luddites have been fearing since before Jim Cameron’s android first spoke with an Austrian accent: delivering heavy ordnance directly to the enemy at high velocity.

Armed with a multitude of weapons (pictured above with a .30 caliber machine gun and a quadruple 40mm grenade launcher), the MAARS costs $300,000 for the base platform, with a variety of configurations available depending on mission parameters.

Although other robots are usually tasked with bomb disposal, one of the available attachments for the MAARS is an arm capable of lifting 120 lbs – strong enough to pick up a 155mm artillery round – or dragging a wounded soldier twice that weight.

Now, for those of you thoroughly terrified by science fiction scenarios, I urge you not to worry too much – at least about this iteration of automated combat technology.

The MAARS is really nothing more than a very, very expensive remote control car.

Its range is limited to just over 3000 feet from its human operator, with environmental information provided via a range of visual and infra-red sensors to a control module tucked inside an armored support vehicle.

Being dependent on a human operator, the MAARS is therefore still just a tool designed to put distance between danger and irreplaceable human tissue… However, tactics for the use of the MAARS in unison with other robotic systems are already being developed for future combat situations – most notably working alongside smaller, more specialized ground-based robots and small airborne drones with hover capabilities.

The MAARS has already demonstrated a talent for breaching doors and walls, entering hostile strongholds, and mopping up concentrations of enemy combatants with its machine gun and grenades.

Cheaper Than the Cost of Human Casualties

The question of cost effectiveness has been posed, of course. Just how useful are these expensive machines when a primitive and cheap IED could easily render one useless?

To that, developers of these systems have an equally straightforward response: $300,000 for a robot that can be replaced is still cheaper than a maimed or killed soldier that cannot.

MAARS units are expected to see wide deployment somewhere around 2018, with an expanded array of weapons options including smart munitions and laser targeting equipment designed to designate impact points for air strikes – most likely performed by their airborne brethren.

If the deployment history of flying robots is in any way a model for how their ground-based cousins will fare in the future, then it is, to say the least, a model for growth.

Not only does this technology promise to expand the technical capabilities of NATO’s armed forces, but it shows that an added emphasis on training and education is in store for the soldiers operating this equipment as well.

The MAARS is a product of the British-based defense firm Qinetiq (QQ.L), which is listed on the London stock exchange.

It is the 52nd largest defense contractor in the world, with a total market capitalization of $1.35 billion and subsidiaries in North America and Australia.

Bear in mind, however, that this company is just 12 years old and only in its 7th year on the public exchange.

Given the cutting-edge nature of the company’s products, as well as the ever-expanding defense market niche it’s managed to grab, it’s as exciting a story as you’ll find in the tech sector today.

It isn’t, however, the only such story.

My colleague Chris Dehaemer just recently published a detailed report on three other such outfits specializing in the design and manufacture of robotic systems for distinctly different applications.

Domestic and industrial robotics, just like their military cousins, are entering golden eras of their own.

Now is the time to get informed on where the future will take them.

You can read his full report here.

To Your Wealth,

Brian Hicks

Brian is a founding member and President of Angel Publishing and investment director for the income and dividend newsletter The Wealth Advisory. He writes about general investment strategies for Wealth Daily and Energy & Capital. Known as the “original bull on America,” Brian is also the author of the 2008 book, Profit from the Peak: The End of Oil and the Greatest Investment Event of the Century. In addition to writing about the economy, investments and politics, Brian is also a frequent guest on CNBC, Bloomberg, Fox and countless radio shows. For more on Brian, take a look at his editor’s page.

Yesterday’s pullback came was blamed on concerns the Fed might taper its asset purchase program as early as this month following some better-than-expected initial claims and Q3 GDP data. The headline print for each certainly aided such thinking. Initial claims for the week ending November 30 checked in at just 298,000 (Briefing.com consensus 330,000) while the second estimate for Q3 GDP jumped to 3.6% (Briefing.com consensus 3.0%) from 2.8%.

Yesterday’s pullback came was blamed on concerns the Fed might taper its asset purchase program as early as this month following some better-than-expected initial claims and Q3 GDP data. The headline print for each certainly aided such thinking. Initial claims for the week ending November 30 checked in at just 298,000 (Briefing.com consensus 330,000) while the second estimate for Q3 GDP jumped to 3.6% (Briefing.com consensus 3.0%) from 2.8%.

The headlines had an undeniably encouraging feel to them. That was the first sub-300,000 print for initial claims since early September and the 3.6% growth in Q3 GDP was the strongest since the second quarter of 2010. Upon closer review, though, the headlines were a little misleading.

The Department of Labor acknowledged that seasonal adjustment problems biased the claims number lower (which means we are likely to see a higher print in subsequent weeks) while the change in private inventories accounted for 1.68 percentage points of Q3 GDP growth. Take the change in inventories out of the equation and real final sales were up just 1.9% versus 2.0% in the first estimate. Furthermore, the 1.4% growth rate in personal consumption expenditures was the lowest rate since the fourth quarter of 2009.

A big jump in inventories and a deceleration in personal spending isn’t exactly a combination befitting a robust growth picture. In that context, the tapering trade in our estimation probably had more to do today with the angst surrounding the November employment report on Friday than it did with a true read of today’s data.

Following the strong ADP Employment Change report on Wednesday, there is a presumption that the nonfarm payrolls number on Friday will also produce a positive surprise. The Briefing.com consensus estimate for nonfarm payrolls is set at 188,000 and at 200,000 for nonfarm private payrolls.

Given the four-day losing streak for the S&P 500, one shouldn’t be surprised if individual investors were a little less bullish this week. After last week’s surge in bullish sentiment, that is exactly what we saw. According to the weekly survey from the American Association of Individual Investors (AAII), bullish sentiment declined from 47.3% down to 42.64%. Perhaps the most surprising aspect of individual investor sentiment over the last few weeks is the fact that even after an eight week winning streak for the S&P 500, AAII’s measurement of bullish sentiment never increased above 50%.

While investors turned a little less bullish this week, they didn’t shift into the bearish camp. As shown in the lower chart, bearish sentiment fell this week as well. After coming in at a level of 28.25% last week, bearish sentiment declined to 27.55% this week. Neutral sentiment, on the other hand, saw an increase of 5.4 percentage points to 29.81%.

Friday’s action is sure to be dictated by the details of the November employment report and the direction long-term interest rates take in its wake.

IN THE NEWS:

———————————————

From Yale Hirsch:

My 1987 Stock Trader’s Almanac was dedicated to THE NEW PROGNOSTICATORS. Mark Leibovit was one of them. I evidently had insight as Timer Digest named Mark the “Number One Market Timer for the 10-year period ending in 2007.” For the 10 years ending 2009, he was #2 intermediate Market Timer. He is also their #1 Gold Market Timer for 2011. This book should be REQUIRED READING for anyone who trades.

——————————————–

Writing a book is an adventure. To begin with it is a toy, an amusement; then it is a mistress, and then a master, and then a tyrant.”

-Winston Churchill (British statesman, 1874-1965)

My book,”The Trader’s Book of Volume” (published by McGraw-Hill) is now available both in English and now CHINESE!

Here is the link to Traders Press:

http://www.invest-store.com/vrtrader/

Here is the link to Amazon.com:

http://tinyurl.com/3wms9q2

——————————————–

Check out the Debt Clock. It is ticking against all of us:

http://www.usdebtclock.org/index.html

VRTrader.com

P.O. Box 12665

Scottsdale, AZ 85267

Phone: 928-282-1275

Fax: 623-243-4174

No, it’s not a glandular condition. China’s leaders concluded the third Plenum of the 18th Party Congress a couple of weeks ago. Party Congresses last for five years and Plenums (full meetings) are annual except for the first year of each Congress where there might be two or three full meetings.

No, it’s not a glandular condition. China’s leaders concluded the third Plenum of the 18th Party Congress a couple of weeks ago. Party Congresses last for five years and Plenums (full meetings) are annual except for the first year of each Congress where there might be two or three full meetings.

Traditionally, the third Plenum is the one where new leadership lays out its long term goals and strategies and it has been third Plenums that were the basis for sweeping changes in China’s society and economy in the past 30 years. The mother of them all was the third Plenum in 1978 when Deng Xiaoping started China down the path to “Capitalism with Chinese Characteristics”. This was the first third Plenum since the ascension of Chinese leader Li Keqiang and expected to be particularly important.

Initial reporting from this Plenum showed disappointment, but I think that was due to most of it being written by journalists that don’t usually pay much attention to Beijing or understand its subtleties. Plenums look like consensus building exercises but are still very top down affairs. New leadership lays out a blueprint for the direction they think the party and the economy should be heading. Its not a process that delivers a bunch of new laws that come into effect the next day. Any major changes in direction require plenty of arm twisting that can take years to complete. We won’t really know how successful this Plenum is until after the fact.

If Li can impose the changes he’s calling for the effects could be large and wide ranging. Major reforms are proposed for State Owned Enterprises (“SOE”s), finance, factor pricing and a reform of the “hukou” (residency permit) system and rural land ownership.

There is a lot at stake, especially for resource investors. China has been the 800 pound gorilla in the room when it comes to commodity demand. That isn’t going to change any time soon but the way changes in China impact intensity of use for resources could have profound implications for metals and energy pricing.

The consensus deemed the proposed changes negative for commodities due to decreased reliance on heavy industry investment. This might true as there is over investment and over capacity in the heavy industrial sector. Some of that needs to go away, especially older and dirtier operations that have added to a massive pollution problem.

Changes to SOEs and factor pricing are linked. There is still a lot of state control in China and monopolistic pricing or state price controls in many sectors. This creates a lot of inefficiency and waste-and plenty of graft for those running state companies. A lot of overcapacity that needs to go is old state factories propped up by monopoly pricing and power relationships.

The process of cleaning up state companies has been through a few false starts. I think this may be the toughest part of the program for Beijing. There are a lot of powerful interests involved and, at best, winnowing out these companies will take years.

Reform on the finance and currency fronts has already started and the current Plenum is mainly reiterating they are serious about following the process to its conclusion. Ultimately that means the Yuan as a truly tradable, hopefully floating, currency. This has positive implications for commodities. Another reserve currency would weaken the US Dollar and could generate support for dollar denominated prices, much the way that the creation of the Euro did.

A trickier part of this process will be clearing out the deadwood in the Chinese banking sector. Again, a lot of this is either state owned or deadwood because of too much lending to state owned companies. The same political issues come into play but it’s a necessary change I think will happen. It won’t happen overnight either since it implies a major change of status (and maybe handcuffs) for a lot of current “insiders”. A cleanup in the literal sense is very necessary.

China has horrendous pollution problems and the citizenry is rapidly losing patience with the situation. Heavily polluting and physically dangerous workplaces will see more and more scrutiny and some will be shuttered. This might impact base metals as there are some pretty nasty small to medium sized operations in China that could be shut, and many “informal” ones that would be easy to close from a political standpoint.

Potentially, the most far reaching reforms are those proposed for the Hukou system and for rural land ownership. Hukou determines residency and severely restricts access to things like government services and housing outside of ones registered residency area. This is no small thing. There are at least 2-300 million people from rural China living and working in cities that have no official access to a host of government services. They also cannot legally buy property in the city where they work which may be hundreds or thousands of kilometres from their county of “residence”.

The system was devised to ensure enough workers stayed on the farms and didn’t overcrowd cities. I’m sure the Party liked the additional control it gave them after Tiananmen Square too. That helps explain why the law is still in effect.

For all the hang wringing about Chinese growth it’s still running above 7% and wages have been rising quickly. Due to the one child policy (also partially relaxed last week) there is a demographic trough coming. There are worries about having enough workers, or at least having the right ones, in some sectors. Removing travel and residency restrictions may solve that problem.

That change won’t happen overnight. Beijing has more than its share of control freaks in power. Many of them oppose loosening of Hukou laws on principle. These government owned companies are sinecures and piggy banks for Communist Party bigwigs and one of the biggest shareholders in many large SOEs is the Red Army itself. Not groups to be taken on lightly.

The final change proposed may be the most far reaching. The central government wants to push forward with rural land reform. Under current laws agricultural land is owned collectively. In practice that means farmers cannot sell or mortgage their land. County level officials haven’t had much trouble expropriating it though. Land sales have perhaps been the largest revenue source for this level of government.

Allowing private sale and/or mortgaging of rural property could generate huge amounts of demand. Coupled with a loosening of Hukou it could also make it much easier for migrants to buy property in cities and actually settle there. Farmers that are finally able to monetize some of the land their families have maintained for centuries could be a source of demand for everything from building materials and appliances to educations and health care.

This has actually been tried in a few select areas and it led to a lot of local building and some rationalization of farm holdings; talented farmers enlarging their holdings and others who wanted to move on selling out. It could have a big impact on large towns and smaller cities.

Sales of expropriated land are a main revenue source at the county level. Making these changes will mean Beijing will have to supply funding for a lot of services carried locally now. A doubling on taxed to SOEs is proposed to help cover this.

These changes are necessary to take the Chinese economy to the next level. If government improves medical care and education this could free up vast amounts of savings being and unleash a lot of pent up demand. Delivery of these services would create a lot of jobs too. It won’t be more steel mills or shipyards but I wouldn’t be too quick to assume a big drop in commodity demand. Anything that keeps China growing at 7%+ is going to generate more demand for everything, regardless of which sectors are favored.

Ω

The HRA–Journal and HRA-Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2013 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ, 85071

Toll Free 1-877-528-3958

The US Federal Reserve bond monetization support for government finance support, financial markets, banker welfare, economic props, redemption coverage, and liquidity fire hose functions will continue to expand and definitely not diminish. Only the brain-dead, the system wonks, and the deeply deluded believe the QE volume will taper down. They are paid to think that way in the public forum, their minds compromised, their hearts darkened, their paychecks dependent. As preface in order to properly comprehend the national situation, keep in mind that the USEconomy is stuck in a nightmarish quagmire, with growth steadily in decline at between minus 3% and minus 5% annually, when reality is required. The propaganda must be pushed off the road, the price inflation not labeled as growth, and the system perceived for what it is. The USEconomy is in grotesque deterioration with absent critical mass of industry, widespread debt defaults, retail liquidations, idle plant and equipment (including malls), and systemic capital destruction from the monetary hyper inflation and the imminent specter of ObamaCare tax. In queer fashion, the modern day US factories have become shopping malls. They suffer from at least a 25% vacancy rate nationally.

Therefore the USGovt deficits will rise, not fall. All economic forecasts offered from official podiums and stages are loaded with nonsense, deceptions, and propaganda at worst, but wishful thinking, delusion, and hope at best. None contain any accuracy required like in a business setting where competence is rewarded and excellence is expected. In the national offices, loyalty, marketing, and toeing the party line are rewarded, just like in a Central European nation in the 1930 decade. The Jackass prefers to call it Reich Economics laced with Soviet Central Planning. The United States has become an unsavory mix of fascism and marxism, the common threads being systemic decay during the eradication of civil liberties.

The major channels will force the USFed to turn up the volume. The May Taper Talk was definitive in its result. The entire financial markets, credit market, liquidity pipes, and economy depend upon the USFed funding. The system cannot sustain itself through vitality, and surely not through savings. So the USFed relented, they blinked, and when they briefly told the truth, they admitted the QE volume would continue forever and a day. Given the political pressures, and some reflection in corner office lavatories, they toy with the concept of tapering again. They realize the hyper monetary inflation has turned into a deadly toxic dependence. It is useful for the mere mortals among the 99% crowd to absorb the realities behind QE and its true nature, better described as QE to Infinity. The sidebar is Zero Percent Forever. The USFed is stuck in the destructive monetary policy, as the Jackass has described since early 2009. The ultra-low rate would not be temporary. The bond purchase plans with printed money would not be temporary. Many are the channels that must be covered by USFed bond monetization. They run parallel to the channels of USTreasury Bonds being returned to sender, listed in July. Regard this article as an update, required to counter the never ending propaganda and deception directed at the public with media scatterguns. It will be illegal someday before long to warn the masses.

PREFACE ON US ECONOMY IN DETERIORATION

People must always bear in mind two concepts. When the USGovt, directed by its Wall Street handlers, marshaled the movement of industry to China, it delivered the nation a death sentence with a timer. The low cost solution was a legitimate income drain that led to deeper asset bubble dependence. The inevitable outcome of systemic failure motivated the launch of the Hat Trick Letter. The results are obvious to those with open eyes, which means only 10% of the masses. Secondly, the USFed monetary policy of hyper monetary inflation, directed at covering USGovt debt issuance and turnover, has a clear effect to kill capital. The rising cost structure from inflation hedging results in reduced profitability, followed bybusiness shutdown and retirement of equipment. This too is obvious to under 10% of the masses, including the crack corps of clueless economists. Review some features.

The October 2012 pre-election Non-Farm Jobs Report was falsified. Nothing new in following orders from the camp commandants in officialdom. The reduced jobless rate from 8.1% to 7.8% permitted the occupant of the White House to report the success of the economic recovery. With dark humor unintended, the new catch phrase has become the non-recovery recovery. Jack Welch was proved right in doubting the data, accusing in tweets that the Administration had altered the numbers. So the BLS, the Bureau Of Lies & Scatology, manipulated the most important jobs report in Obama’s career. At least Obama looked presidential as he reviewed the Hurricane Sandy damage, where no natural hurricane had ever hit in the NorthEast corridor so brutally, and where microwave patterns were detected from its August hatching. (Psst: microwaves are man-made and not natural.) In the most recent quarter, the Q3 Gross Domestic Product has been managed at 2.8% in a travesty of deception. The same tricks are used with hedonic adjustments and calling price inflation as growth. The king is dead, long live the king. The QE to Infinity will be needed in defense and support.

A tell-tale report came from California. The multi-unit properties in California are not being foreclosed, despite being in deep arrears. The banks seem unwilling to take on more REO property on their loaded portfolios. Perhaps private equity firms are only pursuing single family residence properties. The reporter has been in contact with numerous people not making payments and not making decisions, since no pressure. The dire signal is that 20% of all mortgages are delinquent but with no foreclosure activity. Even short sales are prevalent, meaning final sales below the equity level of the seller. Chase has not foreclosed and not responded to a short sale of a delinquent $3 million home in San Diego. The implication is that the bank suffers the loss, the difference. Rumor has it that the USFed is purchasing all the bad debt and will then sell it for deep discounts for other parties willing to take the risk with the courts in the foreclosure process. Think Wall Street cousins in private equity firms like Blackstone. The problem is so deep that foreclosures of condominium units are occurring, for failure to make payment of homeowner association fees. Reports are of HOA non-payment rate of 25% in the sketchy areas. The HOA entities are not dumping the properties. A gaggle of properties that the HOA foreclosed on three years ago are still owned by the HOAssns, many in Riverside and San Bernardino counties. The entire commercial trade has gone underground between the banks, private equity firms, and foreign buyers. A colleague in Los Angeles reports that the same is true with small strip malls, which sport 50 to 90% visible vacancies. The QE to Infinity will be needed in defense and support.

Ten US cities are almost totally out of cash. Their bankruptcy will soon be tested. Meredith Whitney was not wrong, just way too early to earn the acclaim. She will be back in the spotlight to take credit for a correct call. The report is that the ten cities have under ten days of cash on hand. The Detroit court ruling is also interesting. A judge ruled the city pensions and bonds can be reduced in value (called haircut) under legal applications. Next comes the outcome, as the percentages are to be decided. Some bold economists like Laurence Kotlikoff of Boston University have openly declared the USGovt finances worse than Detroit’s. The wave appears next to strike Chicago. The QE to Infinity will be needed in defense and support.

Recovery is nowhere as 4.6 million mortgages going unpaid in the United States. Either the people cannot pay under duress and pressure to make payment, or they scoff at the banks and dare them to take possession, even to locate the property title. At least a couple million Americans are living in soon-to-be bank owned homes for free. That aint recovery. Furthermore, the American consumers are going for the 7-year car loans, as the banks adopt a stupid lending policy. Within 18 months, the loans will have zero collateral from basic car depreciation. The important point is that the bank holds negative equity loans after 3 years or less, with false accounting on the bank books as well. The break to people is a curse for banks, a stupid desperate policy. That aint recovery. The QE to Infinity will be needed in defense and support.

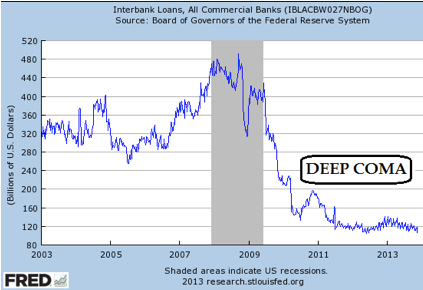

A handy comatose meter is found in the Chicago Economic Diffusion index. It fell in October. The more representative three-month moving average improved to 0.06 from -0.02, indicating the economy has leveled off in its coma. The employment indicators fell, as the labor participation rate is at its most dismal level ever, working its way under the magic 60% level. No recovery is evident. The QE to Infinity will be needed in defense and support.

So conclude that with continued USEconomic deterioration, the tax revenues will be way short. The USGovt deficits will rise above $1 trillion per year again easily. The USFed will be forced to cover the deficits, since national savings is nowhere. The debt issuance will continue to from the capital dome, covered by phony money coming off the press running side by side. The Jackass has not even mentioned the wet blanket known as ObamaCare, with its forced membership, higher costs than advertised, deceptions in keeping other health plans, refusals of cancer treatment, refusals of joint replacement, and broken website done by Michele Obama’s classmate at Princeton. Remember in a fascist business model system, loyalty and crony win over competence and quality, always.

CHANNELS TO BE FUNDED BY Q.E. TO INFINITY

a) Government Finance Support

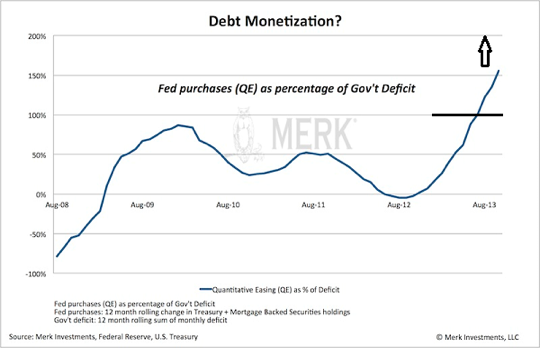

Axel Merk has concluded that the USFed is monetizing 50% more than the USGovt deficits. The key elements are USTreasury Bond issuance, refund activity of USTBonds, along with the ample coverage of USAgency Mortgage Bonds and some private label mortgage bonds. The printing press with Weimar nameplate is under heavy pressure. Those refundings (bond turnover at maturity) are a bitch, and rarely figure in the rosy analyses put out by the wonks, hacks, and stooges. One should really brace for a reality check. The USFed has announced repeatedly that it is executing on $85 billion in bond monetizations per month. The disclosed level represents a staggering volume of $1.02 trillion per year. Amazingly, few economists or bank analysts are troubled by the official steady unrelenting hyper monetary inflation. To be sure, some competent and responsible members of officialdom express their reservations, without much disgust, but with some courage. What would have passed as insanity and reckless policy in the 1990 decade, nowadays is accepted as the norm, the present reality, the exigent necessity, the urgent requirement, the responsible obligation. Focus on the true volume of the USFed bond purchases, the real QE volume when all items are added together. The reality is much worse than admitted reported. This is a banking crime syndicate, which should never be accepted for its word. They are the greatest bond fraud kings in modern history, the greatest thieves probably in world history. They steal the wealth of entire nations, if not from central bank gold bullion then from bonds and home equity, with a kicker in near zero interest loans to themselves.

Some hedge fund managers and bank analysts have come forward to share their privileged information from contacts deep within the USFed system, whether regional bank presidents or economists within the USFed marbled offices on Weimar Street. THE REALITY IS THE USFED IS MONETIZING AT LEAST $200 BILLION PER MONTH, MORE THAN DOUBLE THE OFFICIAL VOLUME STATED AND ADMITTED. The USFed is monetizing much more than basic USTreasurys and USAgency bonds to cover the USGovt deficits, their rollover refunding, and the raft of mortgage bonds. The USFed is monetizing a small mountain of Fannie Mae bonds and collateralized debt obligations with a mortgage core, which went bad, turned worthless. The USFed is monetizing a large mountain of interest rate derivatives that went deeply in the red in the last year, especially this past summer during the self-inflicted Taper Talk disaster. The mortgage debt and its leverage toxic vat amounts to a few $trillion yet to be fully monetized. Furthermore, the interest rate derivatives amount to hundreds of $trillion yet to be fully monetized. This hyper inflation output does not hit Main Street, which would result in price inflation for products and services. Worse, this hyper inflation output wrecks the USDollar and its primary vehicle the USTreasury Bond. It burns the King Dollar throne. The United States is Greece times one hundred.

b) Support for Financial Markets

During the Taper Talk trial balloon, the USTreasury 10-year yield rose to 2.95%, at which time some flash trading was moved from stocks to bonds. They halted the rise, but also put to use the IRS tax revenue tool, tied to Interest Rate derivatives. The Boyz wished to prevent a crease of the 3.0% mark. The damage done was colossal. The Interest Rate Derivative festered with leveraged outsized losses, all kept quiet. The JPMorgan headquarter complex was sold for half price to the Chinese property conglomerate, probably related to the derivative losses and a mandated requirement to manage the gold vaults from Beijing. Call it a hidden indirect margin call, a foreign managed inventory check. The emerging market national bourses took major hits. The Hot Money exited the United States, an early warning signal of the US showing symptoms of Third World.

c) Banker Welfare

The banker welfare, feeding at the trough, knows no end. It came into the open with the TARP Fund bait & switch tactic deployed to garner $700 billion. The funds were largely used to cover big bank bonds and preferred stock, a favorite asset holding by the bankers and their families. It has become a national priority to preserve the college funds for their children, not to mention their lunch accounts and many mistresses (see Jamie Dimon). The inside word has it that the QE3 includes a hidden chamber, to cover the toxic fraud-ridden mortgage bonds and collateralized debt obligations that clog the housing market itself.

d) Economic Props

To begin with, the housing market remains a key sector within the USEconomy. It requires ultra-low mortgage rates, not to stimulate the real estate market. Instead, it requires ultra-low mortgage rates in order to avoid collapse of the real estate market the rest of the way, and in rapid fashion in sudden manner. The car industry requires ultra-low loan rates in order to remain in intensive care, and not in the morgue. The retail industry requires ultra-low credit card rates in order to sustain itself without collapse also. The entire USEconomy could not function without the absurdly low rates. By the way, such harsh low rates provide the legitimate savers with almost nothing in return yields. They are victims to the steady consistent 7% to 9% price inflation year in and year out.

e) Redemption Coverage

Not only Wall Street and London big bank portfolios of impaired bonds must be redeemed and covered. The amplified and ever growing Indirect Exchange of USTBonds must be redeemed and covered as well. The foreign entities holding USTBonds from Chinese acquisitions, Russian energy deals, Brazilian bankruptcies, and other buyouts across the world have become center stage news. The sellers wish to cash in their currency from the big deals. The Eastern nations led by China are buying hard assets. The USFed and Bank of England cannot refuse the bond holders at the window of redemption, since their native sovereign debt. The USFed might ultimately be forced to print money to pay the bond holders. A couple $trillion could end up coming to the window.

GOLD MARKET EFFECT

The Gold Trade Settlement system is moving closer to reality each month. No amount of pressure and obstruction can prevent its progress, its development, and its evolution. The movement to create a non-USDollar alternative to trade, with serious banking reserves management system consequences, will not be deterred or halted. The Global Currency Reset is an extremely complicated undertaking for the major nations of the world. Most people, and many analysts, believe it involves the currency market and the banking systems. That is true enough. However, my informed sources indicate that the entire Reset initiative involves around 8 to 10 very complex, very thorny, very disruptive factors. The fallout from the reset will bring changes to the world order, changes to the balance of geopolitical power, changes to castle lords, changes to Third World residence, and great unclear threats to nuclear proliferation. To regard the main items as currency exchange rates and defaulting banks is painfully naive, but all too prevalent. The reset initiative must be done with respect to careful agreements forged and delicate recalibration of the global balance of power. Both sides possess nuclear weapons and other nefarious devices like electro-magnetic pulse weapons.

The winner will be the Gold Market. The loser will be the United States, the United Kingdom, and Western Europe. These regions will tiptoe into the Third World if lucky, and fall head first into the Third World if not careful. They should have thought more fully about the Chinese Most Favored Nation pact back in 1999. The low cost solution as center piece to globalization effectively destroyed the Western economies, by removing the industrial core. It was far more carefully planned than the great majority of people believe. The ultimate goal in my opinion was to wreck the cradle of capitalism in the United States. The compromise was to create the newly industrialized Chinese superpower, which will fall victim to fascism soon enough. It is the natural course, given human nature and the proclivity toward corruption, inefficiency, power, and greed. The winner will be Gold. It will reign over banks again. It will serve as arbiter over trade again. Its bright yellow lights and strong whips will emanate from the East.

FOOTNOTES

The Iran Talks should be better reported by the alternate press in the West. It was plain and simple a Petro-Dollar Surrender Summit. For the last several years, it has been clear that the primary defense of the USDollar has been military. Many major nations of the world are busy making plans and implementing them toward the creation of systems in bypass, as in Alternative Dollar systems for trade and settlement. The USDollar has turned toxic, widely confirmed by the QE to Infinity adopted policy by the USFed, the Euro Central Bank, and the Bank of England. The many major nations require assurance of not being attacked by the banks with SWIFT weapons, not being attacked with sanctions that hinder commerce to isolate their nations, not being strangled in economies to suffer from price inflation episodes, since their motive has become crystal clear of survival from the current interminable financial crisis. The designers and perpetrators of the crisis have no interest in pursuing solutions, only to defend the USDollar and their right to print themselves $trillions in wealth, the old self-dealing card to the extreme. The summit talks over Iran should be taken with a grain of salt on the detailed promulgated news releases, since loaded with propaganda and rubbish. They sound comical. Expect Iran to continue to make oil & gas sales, but to announce a top-line USDollar transaction which will be executed in gold. The trade settlements will continue in gold on a bilateral net basis, but the official lines (of bull) on ledgers will be etched from USD chisels. It is all about saving face for the dying King Dollar, and to protect the Eastern Alliance nations from retaliation, including potentially nuclear devices suddenly discharged in their home camps. Call the Iran Talks also the Petro-Dollar Surrender SALT Summit.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts regarding the bailout parade, numerous nationalization deals such as for Fannie Mae and the grand Mortgage Rescue.

“Jim Willie is a gift to our age who is the only clear voice sounding the alarm of the extreme financial crisis facing the Western nations. He has unique skills of unbiased analysis with synthesis of information from his valuable sources. Since 2007, he has made over 17 correct forecast calls, each at least a year ahead of time. If you read his work or listen to his interviews, you will see what has been happening, know what to expect, and know what to do.”

(Charles in New Mexico)

“I commend the Jackass for being the most accurate of all newsletter writers. Others called for the big move in Gold right away, but you understand that the enormous fraud in the system needs to play out before free market forces can begin to assert themselves. You seem to have the best sources and insights into the soap opera that is our global financial system. Most importantly, you have advised readers to be patient, stay safe, and avoid mining shares like the plague. Calling the top in the USTreasury Bond (10-yr yield at 1.4% yield) stands out as a recent fine accomplishment. The Jackass understands the markets, understands the fraud, and also has the sources to keep him the most up-to-date on the big geopolitical and financial events and scandals. Few or no other writers have all three of these resources.”

(Austin in California)

“A Paradigm change is occurring for sure. Your reports and analysis are historic documents, allowing future generations to have an accurate account of what and why things went wrong so badly. There is no other written account that strings things along on the timeline, as your writings do. I share them with a handful of incredibly influential people whose decisions are greatly impacted by having the information in the Jackass format. The system is coming apart on such a mega scale that it is difficult to wrap one’s head around where all this will end. But then, the universe strives for equilibrium and all will eventually balance out.”

(The Voice, a European gold trader source)

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com. For personal questions about subscriptions, contact him at JimWillieCB@aol.com

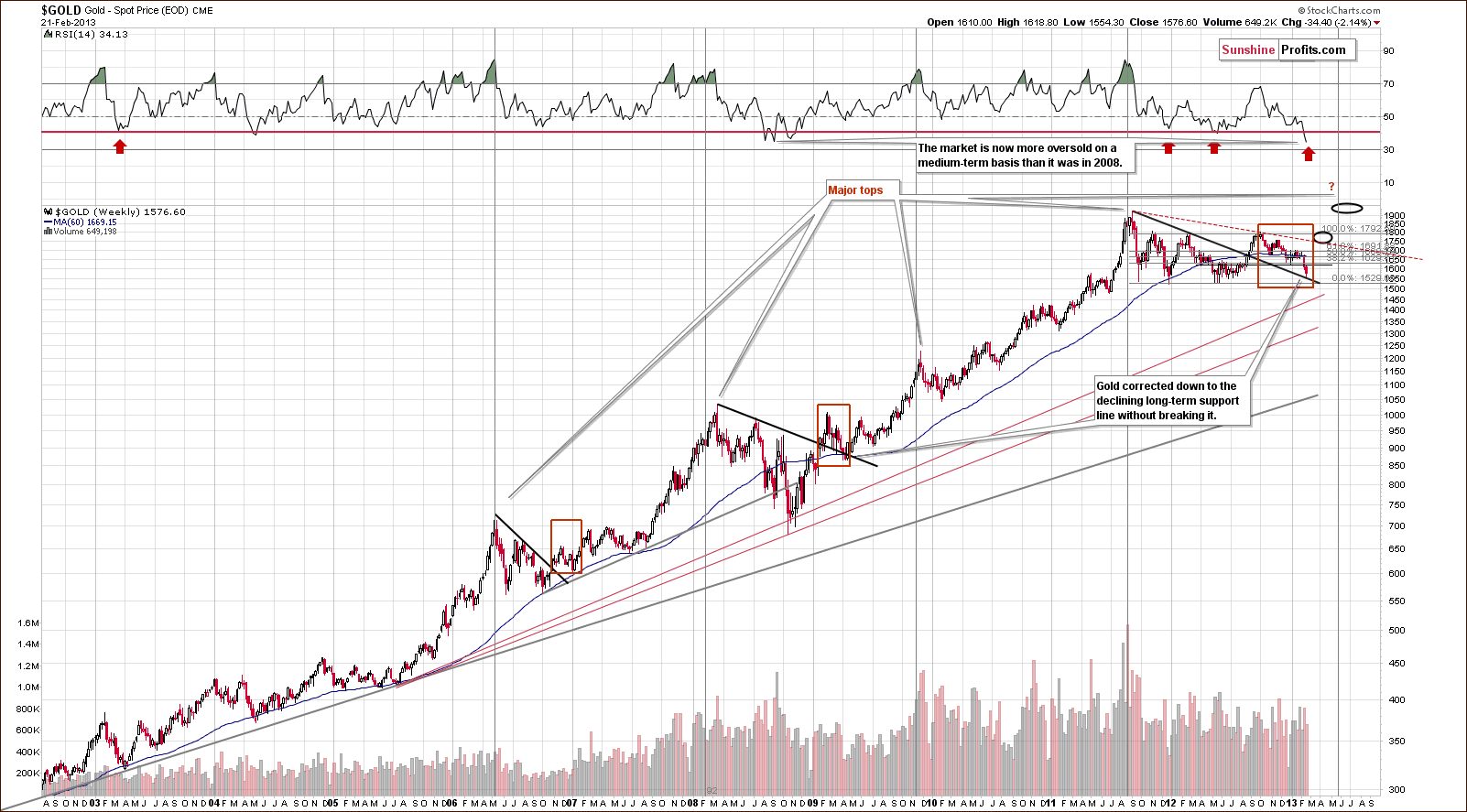

In our last essay we examined the situation in the U.S. Dollar Index (from many perspectives) and the Euro Index, as many times in the past it gave us important clues about future precious metals’ moves. Back then we wrote that the implications for the precious metal market were bearish just as the outlook for the Euro Index and just as it was bullish for the USD Index.

In our last essay we examined the situation in the U.S. Dollar Index (from many perspectives) and the Euro Index, as many times in the past it gave us important clues about future precious metals’ moves. Back then we wrote that the implications for the precious metal market were bearish just as the outlook for the Euro Index and just as it was bullish for the USD Index.

On the next trading day, after the essay was posted, gold, silver and mining stocks declined along with the European currency and hit their fresh monthly lows. Does it mean that the final bottom for the decline in gold, silver and mining stocks is already in?

Many times in our previous essays we wrote that if you want to be an effective and profitable investor, you should look at the situation from different perspectives and make sure that the actions that you are about to take are really justified. That’s why in today’s essay we’ll examine gold and silver mining stocks to find out what kind of impact they can have on precious metals’ future moves.

Additionally, it’s been almost a month since we wrote in greater detail about the precious metals mining stock sector, so we thought that you might appreciate an update. As a reminder, on Nov. 8 we wrote that the outlook remained bearish and even though we couldn’t rule out a few days of strength, it didn’t seem that a rally would be a sustainable development.

Let’s start with two of the most followed commodity stock indices – the Philadelphia Gold/Silver XAU Index and the AMEX Gold Bugs HUI Index (charts courtesy of http://stockcharts.com).

This week we saw a major breakdown below two critical support levels: the long-term rising support line and the 2013 low. Taking this fact into account, we can conclude that the implications are clearly bearish for the coming weeks.

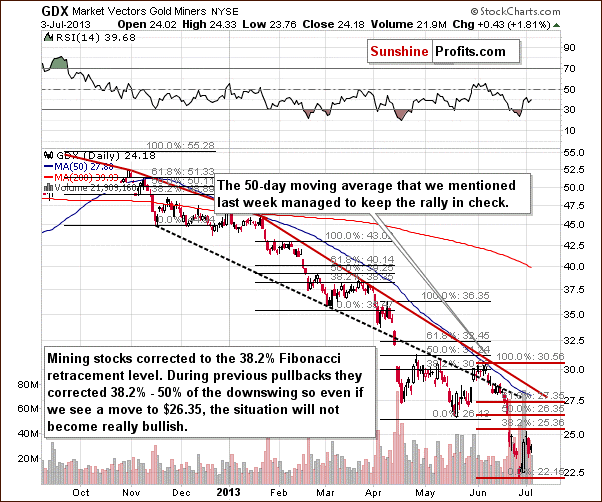

Now, let’s have a look at the HUI Index. The chart below expresses a simplicity that betrays potential information on where this market may ultimately be heading. (Click on image for larger view)

In our previous Premium Update, we wrote that the HUI Index extended declines and dropped below the previous 2013 low, which was a very bearish sign. Back then we also mentioned that a similar breakdown in mining stocks preceded the plunge in the entire precious metals sector in April and taking this fact into account we could expect big moves to the downside in the days or weeks ahead.

Looking at the above chart, we see that we have indeed seen a big move to the downside, even though it’s been only a few days since the above was posted. This is another bearish confirmation, as back in 2008 the breakdown below the previous local low meant that the final sharp downswing was already underway. We expect the final bottom to be seen close to the 150 level.

What about the short term?

Let’s start by quoting what we wrote in Friday’s Premium Update:

From the short-term point of view, we see that the situation has deteriorated recently. At the beginning of the week mining stocks declined below the previous 2013 low and stayed there for three consecutive trading days. This means that the breakdown is confirmed at the moment and the implications are bearish.

As you can see on the above chart, miners reached the medium-term declining support line created by the August and September high – similarly to what we saw at the beginning of the month. Back then, this line triggered a consolidation (just like now); however, as it turned out it was just a pause within a short-term decline.

Taking this fact into account and combining it with the confirmed breakdown below the previous 2013 low, the current decline could become a major, medium-term decline.

It seems that we indeed see mining stocks in a major medium-term term decline as they dropped significantly this week.

There was even another breakdown – below the declining support line based on the August and September highs. The implications of the above chart remain bearish.

Finally, we would like to discuss the current situation in the gold-stocks-to-gold ratio.

On the above chart, we clearly see that the situation has again deteriorated in recent days. On Monday, the HUI-to-gold ratio dropped slightly below its previous 2013 low and we saw it close there on Tuesday as well. The breakdown is not confirmed at the moment but just one more daily close below the previous 2013 low will make the situation much more bearish.

Summing up, the medium-term trend remains down, the decline is quite likely to accelerate shortly and the outlook for the mining stocks sector is very bearish. It seems that practically all markets – gold, silver, main stock indices – are going down right now (except for crude oil, where we just saw a major breakout on huge volume) and mining stocks are declining along with them. Actually, they are leading the way.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair