Currency

“When I read dozens of advisories, I sometimes dream that economics could be simple. How about this: the US Treasury issues bonds, the Federal Reserve buys these bonds with money it creates with the computer, money brought about from thin air. It’s money that nobody worked for an nobody took risks for. The newly created money amounts to over one trillion a year. It’s taking more and more newly created money to produce less and less in the Gross Domestic Product. That’s a trend that could easily end in hyperinflation.

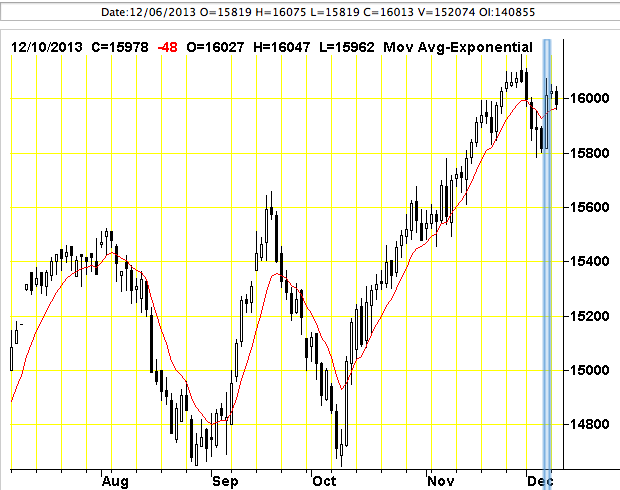

Friday’s market provided a hint of a melt-up. (Ed Note: Friday he refers to is Dec 6th)

Subscribers with strong stomachs may be indulging in this melt-up. Others with weaker stomachs are probably on the sidelines. My original thinking is that this melt-up would be so powerful and so insistent that few would be able to sit on the sidelines and watch. In investing, the ticket to success is to take big profits and small losses.

Philosophically, what do you gain when you make a killing in the market? Probably a more luxurious life, and a feeling of well being. But nobody can take his profits with him. Which is why Warren Buffett and Bill Gates are giving their money away while they are alive.

I never ask subscribers to do what I wouldn’t do. And what am I doing? If I buy anything here, unless I hold it for a year, I’ll be subject to short-term capital gains tax. Since I can’t be sure that this advance will last for over a year, and thus give me tax break, I’m not going to enter this market.

Gold is another story. I continue to think that gold is building a base and that somewhere ahead gold is going to surge. For now I’ll sit with my bullion and cash and patiently await developments.

Is this the beginning of the melt-up I’ve been talking about? It’s too early to tell. But if there was a time to speculate, this may be the time. Personally, I haven’t got the nerve to join in on the festivities. Boils down to a matter of – to each his own. I like the gold action. And this is where I put the bulk of my money.

By the way Sotheby’s just sold a pink 59-karat diamond for $83.1 million, a world’s record for any jewel. It’s a mad, mad world. Who can forget the Graff Pink that sold for $46 million by Sotheby’s in Geneva. Big money is putting millions into one-of-a-kind tangibles. Like Chinese gold-buying, it’s all an escape from the dollar. And it may well lead to hyperinflation, assuming the Fed continues on its course. I continue to believe that gold is constructing a huge base.

Everybody knows that it’s dangerous to arrive late at the party, but it seems that’s where we are. Is the stock market really on thin ice? And is the gold market really on the edge of an upside explosion? Nobody knows. Meanwhile the Fed controls the sword of Damocles, which is hanging over the market.

I can’t prove it but I suspect an inflection point for gold is close at hand. The Chinese, who own a massive amount of US securities, have become openly worried about the US dollar. The gold that has been shaken out of weak and worried US hands, has been shipped to the East, and particularly China. China has imported a net 986 tons of gold through Hong Kong during the first 10 months of the year.

China may not be so much intent on backing its currencies with gold, but in protecting itself from a potential collapse in the US dollar. From the US standpoint, it’s now a case of “inflate or die,” and much of the world knows this. Thus if the US decides not to default on its massive debts, it will have to resort to hyperinflation. If this happens, the US will single-handedly tear the world monetary system apart.

What worries me is that governments will do whatever they have to in order to remain in power. This can result in confiscation of the assets of US citizens. In the end, we only borrow the wealth during our lifetimes. We don’t take it with us. But the government can take it from us. Should this happen, I’m afraid we’ll see blood in the streets. America’s massive debts will ultimately upset the world’s monetary system. There will be no escape, but there will be a diversion into spirituality. This is not the time to give up on your gold. I suspect gold’s inflection point is near.

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE. (Ed Note: Richard Russell is 89 years old and began writing a newsletter he still writes every day in the early 1950’s)

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

(and where I do park my investment capital)

(and where I do park my investment capital)

Earlier this week, Start-Up Chile announced the next round of new businesses who have been accepted to the program.

If you’re not familiar with it, Start-Up Chile is a government program that provides $40,000 in equity-free seed capital (plus a residency visa) to entrepreneurs and their startup companies who make the cut.

Now… in my worldview, this program shouldn’t even exist. This is a government program funded by Chilean taxpayers, and I don’t agree with the idea of government stealing people’s income for any reason.

Unfortunately we don’t get to live in a world where politicians cannot plunder the wealth of citizens.

But the compromise is that we get to vote with our feet and live where we want; we can choose to thrive in a place where taxation is relatively low… and where the politicians fund startups with taxpayer money rather than drones that drop bombs on children by remote control.

Chile is one of those places. It’s far from perfect, but the fundamentals are solid. The government balance sheet is strong– Chile has ZERO net debt. Yet the level of taxation here is among the lowest in the developed world.

So far Start-Up Chile has been a great success for the country.

I know many of the alumni who have come through the program, both foreign and local; several still operate their businesses here and have become successful, creating additional wealth and jobs in the local economy.

This latest round will bring in startups from 28 countries in industries as diverse as agriculture, travel, medical care, advertising, and cryptocurrencies. (Some of my students from our summer entrepreneurship camps have been accepted as well…)

I follow this closely, mostly because I’m an avid investor in startup companies.

With global markets trading at nose-bleed valuations, and almost every possible objective metric suggesting that a crash is coming, a conventional approach to investing seems crazy.

Besides, it’s clear that fundamentals no longer matter. Central bankers are spraying so much money into the system that the only thing driving stocks and bonds is the expectation of further printing. Central bankers have completely hijacked the markets.

I’m simply not willing to take Ben Bernanke on as my silent partner. This is why I invest in real assets– primarily, high quality agricultural properties and private operating businesses.

(Note- I didn’t say precious metals because gold and silver are a form of money to me, not an investment or speculation).

Given the long-term supply, demand, and policy fundamentals of agriculture, I think this sector is exactly the right place to be for the next decade. And owning physical, productive land is as close to the source as it gets.

Private businesses also make a lot of sense, allowing you to invest on the cutting edge of emerging trends and technologies, as opposed to big behemoth corporate bureaucracies. And while the risk potential is greater, so are the potential rewards.

I think any of us would have rather invested in Apple when it was just a startup in the Jobs family garage rather than the slow-moving bureaucracy it is today.

But just like great agriculture properties, such deals and talent are hard to find; this is one of the reasons I hold my entrepreneurship camps each summer, why my team and I travel the world looking at global opportunities, and why we follow programs like Startup Chile so closely.

We’re launching a new service after the holidays for investors who agree with this premise, but need help sourcing and navigating quality deals. More to follow on that in a future letter.

Last week I looked at breaking developments that suggest the Duvernay shale may be the most profitable play in Canadian history.

Consider just two points on the play—hot off the press at a tight-knit gathering of Duvernay insiders put on by TD Securities in Toronto a few weeks ago:

- Well costs all-in are probably running $10 to $15 million right now—with most producers agreeing that $12 million is likely, going forward.

- EnCana’s (ECA-TSX) recently-completed 8-5 well generated $9 million in cash flow in under six months.

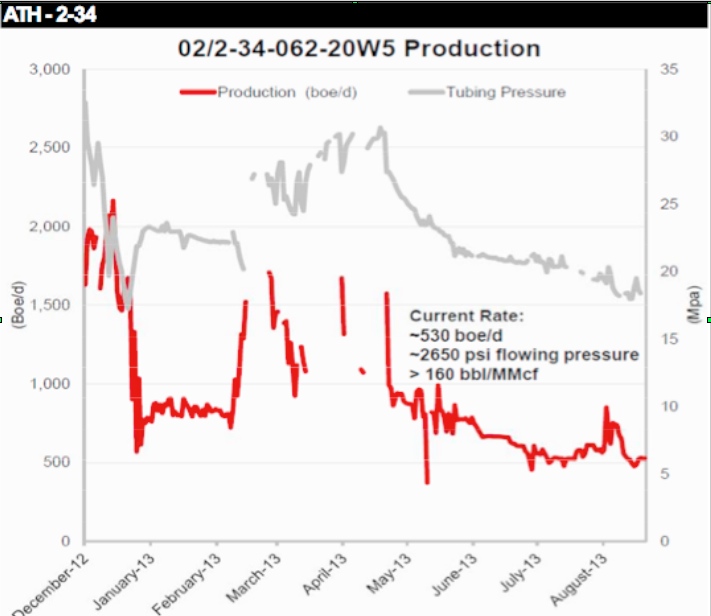

- Athabasca Oil’s (ATH-TSX) 2-34 has pumped $11 million in cash flow in just eight months (see graph of production from TD below)

Incredibly, those figures make the one-year payouts predicted by Duvernay operators like Chevron (CVX-NYSE) and Trilogy (TET-TSX) look conservative.

Numbers like this are creating a lot of excitement.

Like the Viking oil play in 2012, fat returns from drilling here may be setting the stage for a big round of M&A in this acreage—to the tune of millions or even billions of dollars. We’ve already seen that international plays are willing to put up that kind of money for Canadian shales—just look at Progress/Petronas paying $1.5 billion this month for Talisman’s (TLM-TSX) Montney land package.

The question is: which companies are best-positioned to benefit from Duvernay profits?

A Sneak Peak At Financial Returns

There’s two parts to this. Firstly—who’s drilling right now and starting to get a bump from Duvernay production in their cash flow numbers? Then—who has the land holdings to scale drilling out and offer the kind of “factory” that incoming majors want?

In terms of financial results, it’s still early days for the play. You’d expect drilling results to start having a material, bottom-line effect only for the smallest, least-diversified juniors here—the ones most exposed to Duvernay production.

The company that fits this bill is Yoho Resources (YO-TSX Venture). This small developer today gets about 30% of its overall production from the Duvernay.

Financials from Yoho are thus an important indication about Duvernay profitability. And so far they look pretty good.

In 2012, the company spent just under $35 million in the field and added about $58 million in proven and probable reserves. Overall, each dollar spent created about $1.70 in 2P reserves value. That’s very good—not quite the 140% returns some analysts have modeled for the Duvernay, but we may not be fully seeing yet the effect of recent wells.

Other, bigger players in the Duvernay like Athabasca Oil (TSX: ATH) and Trilogy Energy (TSX: TET) have yet to show much bump in profitability from their drilling here. Both companies saw returns on their invested capital in 2012 come in negative (victims of the higher costs that are hampering the industry).

But these firms may simply need more time for the Duvernay to trickle through to their bottom line. Both have significant operations outside of the play, which are likely affecting their stats. And a lot of their best Duvernay wells have been drilled only during the past year—we’ll need to look at the new reserves evaluations that come out early in 2014.

The Leaders in the Land Rush

But let’s assume for the moment that phenomenal early drilling results like the ones mentioned above are going to make the Duvernay a profitable play. Which companies have the land positions to develop it at scale?

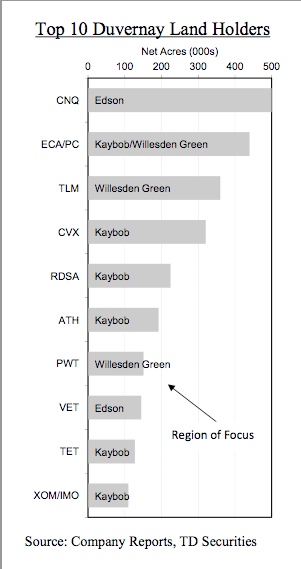

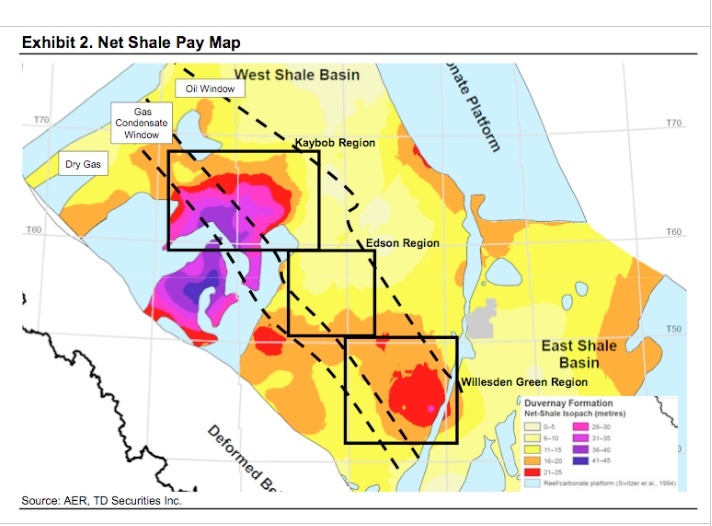

The chart below from TD shows the top 10 Duvernay land holders. These holdings span three different core areas in Alberta for the Duvernay—from north to south, Kaybob, Edson and Willesden Green. Locations are shown in the map from TD. These land holdings are dominated by majors—with the smaller end represented by Athabasca, Vermillion (TSX-VET) and Trilogy.

But it’s obvious from the map above that not all acreage is equal. The thickness of the Duvernay (what geo-wonks call the “isopach”) is much greater in the Kaybob area than the other cores (the purple sections are the thickest). Companies drilling in Kaybob get up to 30 metres more shale pay than those in Edson and Willesden.

One key factor appears to be making the difference: natural gas liquids.

That’s important because liquids are the main driver for gas drilling in North America today. They are why producers can still make a profit at $3/mcf gas in Canada.

For the Duvernay, liquids are especially critical—because the play produces mainly high-value condensate, which right now in Canada sells for a 10% premium to crude oil.

This condensate output is the key to the Duvernay’s outstanding well economics. The Athabasca 2-34 well that cash flowed $11 million in 8 months has seen averagecondensate production of 377 b/d. The big EnCana 8-5 well is the best liquids producer so far drilled in the play (at least that we know about), at 501 b/d ofcondensate.

Both of these wells were drilled in the Kaybob area—where EnCana and Athabasca are focused. Liquids production here looks to be significantly higher than in the other Duvernay operating areas.

Research from Canadian brokerage boutique Peters & Co. shows that the best liquids-producing wells in the Willesden area are only doing 140 b/d—less than half of what the good Kaybob wells are putting out.

This might be why big landholders in Edson/Willesden like Penn West (TSX-PWT) are putting their acreage up for joint venture rather than drilling it themselves.

The Best Producers in the Best Part of the Play

So, who are the leaders in the liquids-rich Kaybob area then?

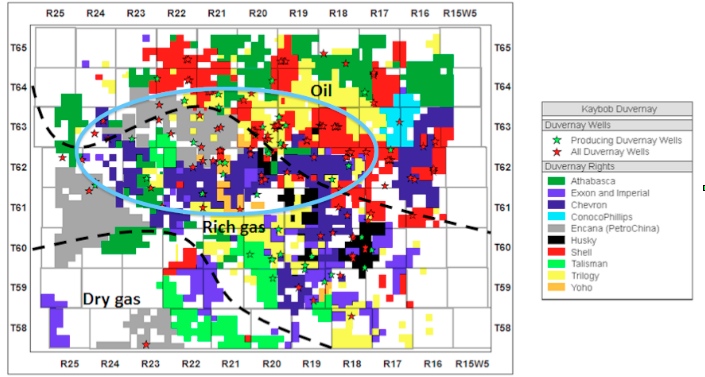

Again, you need to look beyond the raw acreage numbers—to see who is in the right part of Kaybob. In this case, the liquids window.

As the map below from Dundee Capital Markets shows, the Kaybob area is oil-prone to the northeast, and produces dry gas (no liquids) to the southwest. Only in the central portion (between the two dotted black lines) does the Duvernay produce liquids-rich gas. Of course, the lines are approximate—I’ve circled in blue the approximate area that’s so far seen wells with high average condensate production of a few hundred barrels per day.

Looking at it this way changes the picture a lot.

A big landholder like Athabasca looks great on paper—except that most of its holdings (shown in dark green above) are in the oil-prone part of the Duvernay. The jury is still out on the oil window thus far. This could prove profitable too—but the big numbers on economics we’re talking about are for liquids-rich gas wells. You have to make sure you’re comparing apples to apples.

Athabasca did have the big 2-34 gas well. But this was drilled on one of only a few sections of its land that push south into the liquids-rich window.

Exxon/Imperial have also missed the spot to some degree. Although these companies have scattered holdings in the liquids-rich window, their biggest contiguous land packages are in the dry gas part of the play.

The core of the liquids-rich acreage is really held by four companies: Chevron (dark blue), EnCana (grey), Shell (red) and Trilogy (yellow). Yoho also holds a strip of land in the right area (orange)—small in the grand scheme of things, but probably material to a company with a $150 million market cap.

While Yoho is indeed a pure play, their challenge is that they are not in the data sharing group with the majors so it’s likely they will be behind on how/what technologies are improving production and lowering costs. So capital efficiencies—the cost to bring up a barrel of oil/condensate/gas–will be poorer.

Shell and Chevron are too big to get much recognition for this play in their share price. EnCana might—maybe helping them shed their reputation as an unexciting dry gas play.

Trilogy is running quickly in the Duvernay, having drilled 11 horizontals here as of October. The company will dedicate $75 million to the play in 2013—a good chunk of its total budgeted capex of $350 million for the year.

Trilogy also holds a unique advantage when it comes to producing Duvernay liquids-rich gas. The firm has a liquids processing agreement with an extraction plant in Illinois—allowing it to ship high-liquids gas here. That means two great things–they don’t have to finance expensive separation facilities—and they accessbetter product pricing in Chicago.

This will be the company to watch to see how wells here ultimately affect the bottom line.

– Keith

Related posts:

- Duvernay Oil & Gas Stocks: Which Companies Will Emerge the Winners?

- Duvernay Shale – It’s Make or Break for this Huge Shale Play

- The Duvernay: North America’s Most Profitable Condensate Play?

- Payout Times: My #1 Factor in Valuing Junior Oil Stocks

- Sizing Up Today’s Dividend Paying Exploration & Production (E&P) Companies

As Prices Successfully Retest Cycle Lows For First Time

Fed tapering may already be priced in.

Gold and silver rebounded notably this week amid a combination of short covering and physical buying. Last week, gold and silver reached as low as $1,211 and $18.90, respectively—just above the cycle lows of $1,180 and $18 put in during July.

When prices failed to move any lower on Monday, shorts began covering their positions and buyers who had been waiting on the sidelines began to enter the market as well. Bulls should be encouraged by this first successful retest of the July cycle lows. It’s a positive first sign that the Fed’s upcoming tapering may already be priced into the market.

The Federal Reserve may finally act—or at least hint that action is imminent—in its next meeting on Dec. 18. If precious metals shrug off the news, that may spark another round of short covering and physical buying that sends gold above $1,300 and toward $1,400.

GOLD (YTD)

SILVER (YTD)

PLATINUM (YTD)

PALLADIUM (YTD)

….read page 2 HERE

Digital marketing as a mega-trend is quickly revealing Early Adopters and Laggards. Where are you on that spectrum?

A brief history of business technology:

- In the late 1980s you had to have a fax machine (and fax number on your business card) in order to be seen as a credible business

- In the late 1990s, no legitimate company would be caught dead without a website (in fact, any company without a website was probably dying as a result)

- In the late 2000s (and more so everyday), any business without a proactive plan to manage social media was falling behind its competition

- In the 2010s, if you still have a fax machine (and fax number on your business card), you may be in more trouble than you thought

Increasing your web presence and social media footprint has never been more urgent. Whether you’re just starting a business or trying to make an existing one more accessible and appealing to customers, now is the time to dump the fax machine, jump on SEO, and avoid extinction. Take a look at the Diffusion of Innovation bell curve.

With respect to a viable web presence, where would you plot your company on this adoption curve? The latest adopters in this familiar model have traditionally been labeled “Laggards,” but in the world of SEO and social media, latecomers are plain old Dinosaurs because of the extinction-level event that is created by their inattention.

Finding a good SEO partner

Forbes.com contributor Joshua Steimle wrote an excellent article, 4 Tips For Hiring The Right SEO Firm, that might help those in need of this service cut through the fog that shrouds the overly crowded SEO industry. It is perhaps the ultimate irony that anyone searching the Internet for a company that can help them become more visible on the Internet, can easily experience confusion and information overload.

My company has used several SEO firms over the years. Some I would recommend and others I wouldn’t. Here are two that have done well by me.

Boostability. After interviewing Boostability’s CEO, and writing an articleabout the company, I was impressed enough to sign up as a client. Not having used them for very long, it’s hard to say what the long-term results will be, but their attention to detail and service levels have been stellar. Also, they seem to understand my business. For example, my rep is helping me extend the reach of my writing beyond Forbes.com, which is a good thing for a writer. So far, so good.

Mabbly. After using Mabbly for a while, I saw a relatively quick positive impact. What I like about Mabbly is the fact that they will work without a long-term contract. Also, they have a startup package that is pretty reasonably priced.

Whichever SEO vendors you choose, and however you find them, go forward with this strategy as fast as you can. Don’t be a dinosaur. And if you ever want to contact me—no faxes, please!

Follow me on Twitter @larrymyler, “Like” me on Facebook, or Contact me at lmyler@bymonday.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair