Stocks & Equities

It’s no secret to anyone following the Canadian stock market that the TSX Venture exchange has fallen on hard times over the last three years. Comprised largely of speculative, junior resources stocks, the exchange has lost over 55% of its value over this period. Fortunately for the exchange this loss has been somewhat mitigated by the few small cap stocks that are actually producing real earnings and growth. But for the people who have made a habit of buying heavily into the speculative junior resource plays, it would appear that a mere 50% loss (however nauseating this may be) is the least of their worries when liquidity has dried up to the point where they can’t even sell the shares they have (essentially equating to a 100% loss).

It is no secret what KeyStone thinks of revenue-less and profitless, capital-sucking predators. In our view, the junior resource sector in Canada has been fought with what are essentially shell companies, never generating a penny of economic value and existing solely for the purpose of raising capital from unsuspecting investors and then funneling this money into management salaries and corporate expense accounts. With very few exceptions, they have been nothing but capital-destroyers and essentially represent the antithesis of our fundamental, cash flow based investing strategy.

After years of collapsing share prices and deteriorating liquidity, most of these so-called companies are largely losing their ability to raise additional capital with many now sitting on the verge of financial destitution. But in the wake of their darkest hour, a glimpse of light has risen on the horizon…or as the case may be…a puff of smoke. Sweeping regulatory changes with respect to the production and distribution of medical marijuana have taken effect this month. The industry is becoming industrialized and many people smell an opportunity for businesses that can take advantage of the change. This transition has piqued the interest of investors and speculators which has prompted dozens of “resource companies” to issue new releases over the past few months outlining their intentions to investigate the prospects of being reborn into the new marijuana industry.

After years of collapsing share prices and deteriorating liquidity, most of these so-called companies are largely losing their ability to raise additional capital with many now sitting on the verge of financial destitution. But in the wake of their darkest hour, a glimpse of light has risen on the horizon…or as the case may be…a puff of smoke. Sweeping regulatory changes with respect to the production and distribution of medical marijuana have taken effect this month. The industry is becoming industrialized and many people smell an opportunity for businesses that can take advantage of the change. This transition has piqued the interest of investors and speculators which has prompted dozens of “resource companies” to issue new releases over the past few months outlining their intentions to investigate the prospects of being reborn into the new marijuana industry.

Of course almost none of these three dozen or so companies actually have a plan for entering an industry which essentially has little to no similarities to their own. But thankfully for them, in many cases that doesn’t seem to matter. The mere mention of a strategic refocus into medical marijuana has resulted in a significant increase in the share prices for many of these companies. It is completely unknown to us how these companies plan to leverage what experience and expertise they have into this completely new marketplace. But speculation surrounding the new industry has created a new buzzword in the stock market and simply replacing the word “gold” (just for example) with “medical marijuana” in a corporate presentation may be exactly what some of these nearly destitute corporate capital-killers need in order to hit the street for a few quick capital raises.

What we do know about the industry right now is that there are approximately 40,000 individuals that are licenced to use medical marijuana in Canada and this number is expected to grow. Up until now, most of these people were able to grow their supply in their own homes or else contract another individual (who is licensed) to grow it for them. But these rules changed as of April 1st under a federal government initiative to industrialize marijuana grow operations into commercial facilities. Health Canada has so far received thousands of applications for licenses to grow commercial marijuana and (to our knowledge) to date has issued only 12. The number of licenses issued to public “resource-to-marijuana” companies is currently exactly zero. This may be an industry with good long-term potential but currently there are too many unknowns to actually conduct a fundamental analysis. First off, none of the public companies that are planning to be in medical marijuana have generated a dime of profit or revenue. They are unproven at best and many are simply opportunistic (and not in a good way). Government regulations, costs, distribution, and a plethora of other factors are all currently unknowns as well. Plus there is price sensitivity…how much money are these 40,000 patients (many of whom are on disability) able to pay for medical marijuana when many are accustom to growing it themselves. The list of uncertainties goes on. There is currently one single company which recently became public (not a resource convert) that does have a federal license and plans to build out a production facility. But once again, this particular company has yet to produce a dime of revenue to prove out its business model but still somehow commands a market capitalization of almost $100 million.

In spite of all these unknowns, investor interest and the prospects for further speculation appears to be increasing. Over the next several months, we expect to see many more new releases from unsuccessful companies in unrelated industries, announcing their intentions to pursue a medical marijuana focus. Our advice to investors is to be cautious (or in plain English…don’t buy them). Getting wrapped up in the “hype” of a sector or technology, without consideration of the underlying fundamentals, typically proves to be disastrous over time. This becomes especially true when many of the companies have a track record of doing little more than destroying investor capital.

KeyStone’s Latest Reports Section

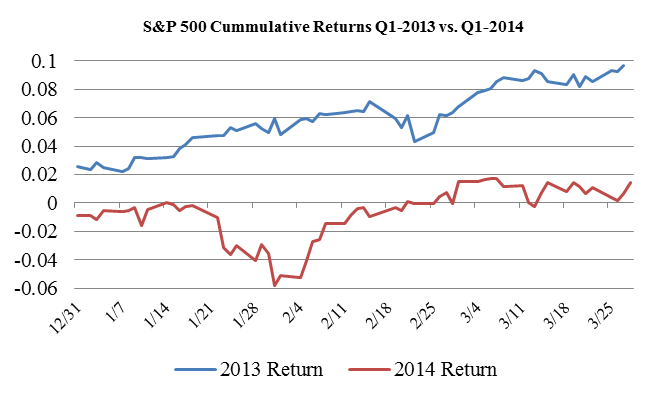

Friday’s US payroll numbers revealed a key milestone for the US labour market. Private employer payrolls surged to 116.09 million positions, a level not surpassed since January of 2008. That confirms two key factors about the economy. One, the US labour market continues on its path of modest gains as more Americans rejoin the labour force each month. Two, the slump through the first quarter of this year was in large part weather related and looks to be short-lived. In essence, this is exactly what the markets have told us as the S&P 500 gained a modest 1.3 per cent in the first quarter of 2014 verses 10.03 percent in the quarter a year prior.

The US labour market however, isn’t on a clear path to prosperity just yet. Population growth alone has seen an increase of 2 million American workers since 2008. And given the budget cuts and trimming of positions at government agencies, private payrolls are yet to pick up the slack created by the public sector. Although its easy to find optimism each month as the broader market shows signs of improving, there are the unavoidable facts that 3.7 million of 10.5 million unemployed Americans have been out of work for 6 months or longer, and 7.4 million Americans are working part time, but would prefer full time hours.

It’s the structural problems of the US economy that continue to exhibit investors’ uncertainty, and that is what is leading to the volatility of these markets. As many leading analysts seemed to suggest, 2014 would be a much more volatile year than 2013, and as the chart indicates, the first quarter of 2014 was rather directionless. Moreover, it was with that forecasted volatility that the market finished the quarter within a per cent of where it started.

The real question going forward this year surrounds what path policy makers, particularly at the US Federal Reserve, but also in Washington, will take. Without doubt accommodative monetary policy has been what directed these markets since 2009. Recent developments at the Fed, however, indicated Janet Yellen’s direction to be slightly unclear as her message has wavered between being hawkish to dovish. Furthermore, one of the leading voices on financial stability, Harvard’s Jeremy Stein resigned his seat as a Fed Governor this week. This is the third vacancy to be filled at the US Fed this year, and certainly opens up the possibility for a more accommodative tone, as it is the Fed Governors that dictate policy as they carry the majority of the votes on Federal Open Market Committee.

To make investors jobs more difficult, Washington kicks into campaign mode for the 2014 mid-term elections, and there are two probable outcomes. One is where Obama continues his lame duck presidency with strong Republican opposition, or a Democrat majority that support his anti-business agenda. Either scenario doesn’t really provide optimism for robust economic growth. Instead, more of the same moderate advances should be expected from the economy.

And this returns us back to the likely scenario of stock market volatility. The Fed has played a role in maintaining a steady hand for their unconditional support for the US economy. That is now being questioned. If the Fed choses to subside their proactive role in providing a predetermined level of assistance, investors may very well lose confidence in these markets, and they shouldn’t expect Washington to fill that void.

…also:

David Morgan is interviewed by Michael Campbell today on Money Talks.

David Morgan is interviewed by Michael Campbell today on Money Talks.

In this 18 minute interview with David, best known as one of the world’s top silver analysts, Michael asks David to spell out his favorite picks in silver stocks & how he’s positioned in bullion & the futures market.

Michael also gets David’s perspective on the debt, currency pitfalls including the all important US Dollar, plus short and long term economic trends. David is the founder of silver-investor.com

{mp3}mtapr514davidmorganfp2{/mp3}

To catch the entire Money Talks Show go to http://www.cknw.com/audio-vault/ then scroll down to April 5th to catch both the first 1/2 hour plus the following full hour.

If you are interested in David’s Monthly Report PLUS 16 additional reports click the graphic below.

MoneyTalks Editor

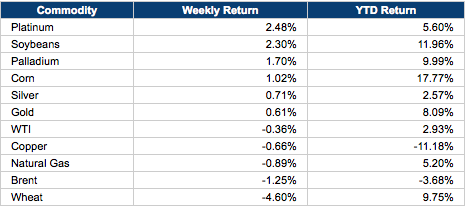

WEEK IN REVIEW: GOLD REBOUNDS; CONFLICTING SIGNALS FROM LIBYA SINK OIL; CORN UP

Gold finally rebounded back above the $1,300 level, while Brent briefly hit a five-month low.

Precious metals, soybeans and corn were the big winners in commodity markets this week, while oil, copper and wheat fared poorly. Stocks touched all-time highs, but finished the period off their best levels. The S&P 500 increased 0.8 percent, bringing its year-to-date gain to 1.3 percent. On Friday, the index briefly touched 1,897—a new intraday record.

Macroeconomic Highlights

The biggest economic release of the week was the monthly employment report in the U.S. According to the Bureau of Labor Statistics, private employers added 192K jobs in March, just a tad below the 200K that was expected. At the same time, the unemployment rate held steady at 6.7 percent.

In other news, ISM reported that the manufacturing sector in the U.S. accelerated slightly in March. The ISM manufacturing index rose from 53.2 to 53.7 in March. Meanwhile, ISM reported that its U.S. non-manufacturing gauge for March rebounded from 51.6 to 53.1. Levels above 50 represent expansion, while levels below 50 represent contraction.

Elsewhere, the ECB kept its benchmark overnight interest rate steady at a record-low 0.25 percent, as was widely expected. Speaking to journalists after the policy decision, ECB President Mario Draghi said the central bank does not exclude further monetary easing. He also said that ECB officials were unanimous on using unconventional policy tools if necessary—including quantitative easing.

The ECB has kept monetary policy extremely accommodative amid low levels of inflation and high levels of unemployment. Eurostat reported that the CPI in the eurozone in March grew by only 0.5 percent year-over-year, down from 0.7 percent the previous month and the slowest pace since 2009. The core CPI, which excludes food and energy prices, grew by 0.8 percent in March, down from 1 percent in February.

Finally, in China, the government released its official manufacturing PMI for March. The index edged up from 50.2 in February to 50.3, close to expectations. At the same time, HSBC’s manufacturing gauge for China—which measures smaller firms in the country—edged down from 48.1 to 48, also close to expectations. Levels above 50 represent expansion, while levels below 50 represent contraction.

Commodity Wrap

Gold bounced back this week as bargain hunters entered the market following recent losses. As we wrote earlier this week (see Rising Interest Rates Won’t Push Gold To New Lows; Buy On Pullbacks), the recent $112 decline in prices was a short-term reaction to the Fed’s hawkish outlook for interest rates laid out in its last meeting on March 19.

However, gold is not at risk of falling into a major downtrend or hitting new lows below the cycle low at $1,180. We remain buyers on the dips and see the likelihood of another rally to $1,400 or higher later this year.

….read page 2 and the rest of the commodity wrap HERE

It’s been a while since we looked at Gold in a vacuum. We’ve focused on the gold stocks as they have led the sector. We covered Silver last week. Gold is more interesting because in its current state its more difficult to draw a strong conclusion. One could look at the evidence and go either way. Today Gold is back above $1300. Is this the start of a run to and past $1400? I don’t know. My gut says more range bound activity is ahead.

First lets take a look at the Gold bear analog chart. This includes the major bears of the past 35 years, excluding a super long (1987-1993) bear that was very mild in its price decline. The Gold bear analog isn’t quite as black and white as the previous analogs shown for Silver and the gold stocks. One could look at this chart and surmise that the bear has longer to go while others could say it has gone far enough and deep enough already.

At the June 2013 and December 2013 lows, Gold was very close to plunging to that final low as it did in 1982 and particularly in 1976 and 1985. The fact that it didn’t happen and the fact that this bear has dragged on renders it less likely that we get a final plunge. The longer a bear market is, the less severe it tends to be in price and the less likely it terminates with a final plunge. For example, the 1996-1999 bear declined only 3% in its last 11 weeks. In other words, if this bear is to make a new low and break $1200 on a weekly basis, I doubt it plunges from there as much as people would think. There aren’t as many players left in this market as there were a year ago, two years ago and three years ago.

At the June 2013 and December 2013 lows, Gold was very close to plunging to that final low as it did in 1982 and particularly in 1976 and 1985. The fact that it didn’t happen and the fact that this bear has dragged on renders it less likely that we get a final plunge. The longer a bear market is, the less severe it tends to be in price and the less likely it terminates with a final plunge. For example, the 1996-1999 bear declined only 3% in its last 11 weeks. In other words, if this bear is to make a new low and break $1200 on a weekly basis, I doubt it plunges from there as much as people would think. There aren’t as many players left in this market as there were a year ago, two years ago and three years ago.

Aside from the typical Gold in US$ chart it’s always important to consider Gold in the context of various currencies and the equity market. In the chart below we plot Gold against a foreign currency basket and against the S&P 500. The first plot shows that Gold hasn’t made a double bottom but is still in a series of lower lows and lower highs. The positive is Gold is has rallied up to trendline resistance several times already. I think Gold will be in position to break the trendline by the end of summer. If that happens, the bear market is over.

Meanwhile, Gold has obviously struggled against the S&P 500. We all are aware of the negative correlation between the two markets which started just after Gold peaked in August 2011. If Gold is to begin a new bull market in earnest then it really needs to reverse itself against the S&P 500. The ratio has clear resistance at 0.75 which is important resistance dating back to July 2013. The ratio has traded below 0.75 for the past five months, a period in which many stocks rebounded strongly. If the ratio can move back above 0.75 it would make a very strong case for Gold’s bottom being in place.

We just don’t have enough evidence to know at this point. I continue to maintain that the mining stocks (and definitely the juniors) have bottomed. GDXJ and SILJ would have to decline 24% to test their daily lows. GLDX would have to decline 27%. The mining stocks led the move down and have led this fledgling recovery. I think they continue to lead. However, it appears that they won’t sustain a rebound and push much higher until after the metals have bottomed.

My conclusion on Gold is if it breaks to a new low then a final bottom is imminent. If it breaks above $1400 and the resistance in the aforementioned charts, then it has bottomed. Yet, Gold and the mining stocks could continue to be range bound for several months and deny us an immediate answer. At worst it would bring us much closer to the end and the start of a new bull market. Rick Rule, who was very prescient during the recent downturn recently stated that he thinks we are seeing a saucer type bottom and that 12 to 18 months from now we will be in a rip roaring bull market. Consider that it takes an uptrend to develop to create the momentum that leads to the rip roaring part. I believe we have no more than several months left to accumulate the best stocks which are positioned to benefit from the coming resumption of the secular bull market. If you’d be interested in learning about the companies poised to outperform, then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair